Cytokinetics (CYTK) Q4 2025 Earnings Transcript

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Feb 25 2026

0mins

Should l Buy CYTK?

Source: NASDAQ.COM

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy CYTK?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on CYTK

Wall Street analysts forecast CYTK stock price to rise

17 Analyst Rating

15 Buy

2 Hold

0 Sell

Strong Buy

Current: 65.420

Low

61.00

Averages

89.33

High

136.00

Current: 65.420

Low

61.00

Averages

89.33

High

136.00

About CYTK

Cytokinetics, Incorporated is a late-stage, specialty cardiovascular biopharmaceutical company focused on discovering, developing and commercializing muscle biology-directed drug candidates as potential treatments for debilitating diseases in which cardiac muscle performance is compromised. The Company is engaged in the commercialization of aficamten, a cardiac myosin inhibitor, and is being evaluated in additional clinical trials enrolling patients with obstructive and non-obstructive hypertrophic cardiomyopathy. The Company is also developing omecamtiv mecarbil, a cardiac myosin activator, in patients with heart failure with severely reduced ejection fraction (HFrEF); CK-586, a cardiac myosin inhibitor for the potential treatment of heart failure with preserved ejection fraction (HFpEF) and CK-089, a fast skeletal muscle troponin activator with potential therapeutic application to a specific type of muscular dystrophy and other conditions of impaired skeletal muscle function.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

DAFNA Capital Management Reduces Stake in Biotechnology ETF

- Share Reduction: DAFNA Capital Management sold 34,405 shares of iShares Biotechnology ETF (IBB) in Q4 2025, resulting in a $3.31 million decrease in quarter-end position value, reflecting both trading activities and stock price fluctuations.

- Asset Management Impact: This transaction reduced IBB's share of DAFNA's 13F reportable assets to 2.67%, indicating that IBB is no longer among the fund's top five holdings, which highlights its diminishing significance in the investment portfolio.

- Market Performance: As of February 17, 2026, IBB's price stood at $174.02, marking a 27.2% increase over the past year, with an alpha of 15.84 percentage points compared to the S&P 500, showcasing the ETF's strong performance in the biotechnology sector.

- Investment Strategy: The iShares Biotechnology ETF primarily invests in large, commercial-stage biotech companies and employs a passive investment strategy aimed at efficient index replication and liquidity management, although it remains sensitive to interest rates and investor risk appetite.

See More

DAFNA Capital Management Reduces Stake in iShares Biotechnology ETF

- Stake Reduction Details: According to an SEC filing dated February 17, 2026, DAFNA Capital Management reduced its stake in the iShares Biotechnology ETF by 34,405 shares during Q4 2025, resulting in a $3.31 million decrease in position value, highlighting the impact of market fluctuations on the portfolio.

- Asset Allocation Shift: Following the sale, the iShares Biotechnology ETF now comprises 2.67% of DAFNA Capital's 13F reportable assets, indicating a relative decline in the ETF's significance within the overall investment strategy.

- Top Holdings Overview: As of February 17, 2026, DAFNA's top five holdings include NASDAQ:RVMD at $48.15 million (11.3% of AUM) and NYSEMKT:XBI at $41.03 million (9.7% of AUM), reflecting a continued focus on large-cap biotech firms in its investment approach.

- ETF Performance Analysis: As of February 17, 2026, the iShares Biotechnology ETF was priced at $174.02, up 27.2% over the past year, demonstrating stable performance in the biotech sector, though it remains sensitive to shifts in market risk appetite for growth-oriented healthcare stocks.

See More

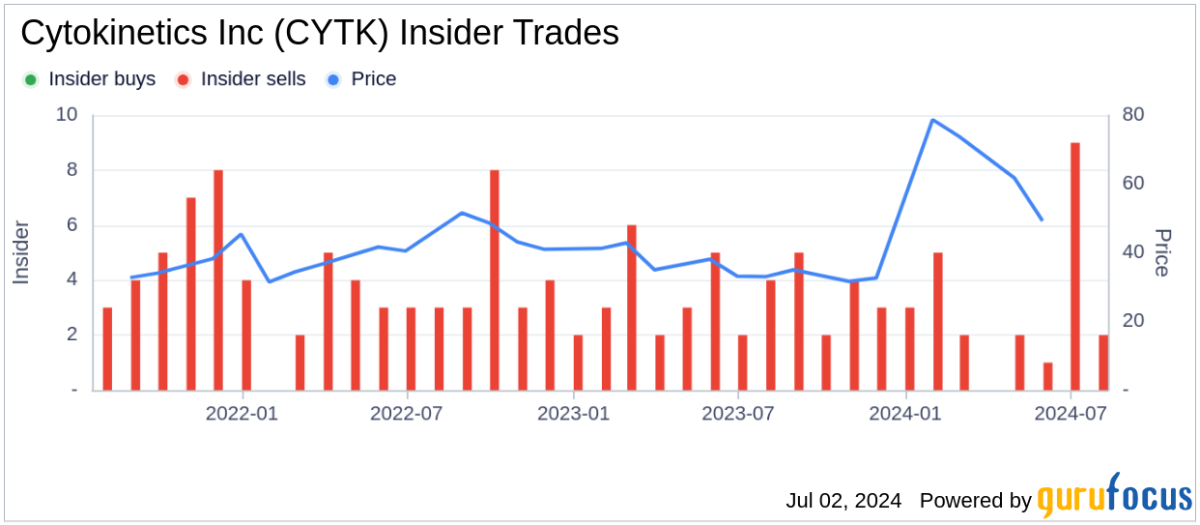

Cytokinetics Executive's Major Stock Sale Raises Eyebrows

- Executive Stock Transaction: On February 5, 2026, Cytokinetics' Executive Vice President Andrew Callos exercised 15,000 stock options and immediately sold them for approximately $928,950, indicating a liquidity-driven decision.

- Ownership Percentage Shift: Following the transaction, Callos' direct ownership decreased from 65,440 shares to 50,440 shares, lowering his direct equity stake to 0.04%, which reflects a significant reduction in his equity exposure within the company.

- Market Reaction Analysis: The sale price of around $61.93 per share was slightly above the market close of $60.24 on the same day, suggesting favorable execution that could positively influence investor confidence.

- Company Strategic Context: Cytokinetics is at a commercial stage with its first product myqorzo recently launched, and despite a net loss of nearly $785 million in 2025, its potential in the cardiovascular sector attracts high-risk investors looking for growth opportunities.

See More

Cytokinetics Executive Sells Stock Options

- Stock Option Sale: On February 5, 2026, Andrew Callos, Chief Commercial Officer of Cytokinetics, exercised 15,000 stock options and sold them for approximately $928,950, indicating his confidence in the company's future prospects.

- Reduction in Holdings: This transaction reduced Callos' direct holdings from 65,440 shares to 50,440 shares, accounting for 22.9% of his total holdings, reflecting a strategic decision to decrease his stake in the company.

- Market Reaction: Following the FDA's approval of myqorzo in December 2025, Cytokinetics' stock surged over 92% in six months, and the timing of this sale coincides with the launch of the company's first commercial product, potentially impacting investor sentiment.

- Financial Position: Despite Cytokinetics reporting a net loss of nearly $785 million in 2025, its strategic focus on the cardiovascular sector and the introduction of new products provide potential for future growth.

See More

MongoDB and Warner Bros Options Trading Activity

- MongoDB Options Volume: As of now, MongoDB Inc's options volume has reached 12,327 contracts, equivalent to approximately 1.2 million shares, indicating a trading activity level that is 72.8% of its average daily volume over the past month, reflecting heightened market interest in the stock.

- High-Frequency Trading Insight: Notably, the $200 strike put option expiring on February 27, 2026, has seen a trading volume of 865 contracts today, representing about 86,500 underlying shares, which suggests investor expectations regarding future price volatility.

- Warner Bros Options Activity: Concurrently, Warner Bros Discovery Inc's options volume stands at 165,162 contracts, translating to approximately 16.5 million shares, which constitutes 70.4% of its average daily trading volume over the past month, indicating sustained market interest in the company.

- Bullish Call Options: For the $30 strike call option expiring on March 20, 2026, today's trading volume has reached 26,710 contracts, or about 2.7 million shares, reflecting investor optimism regarding Warner Bros' future performance.

See More

Cytokinetics Q4 2025 Earnings Call Highlights

- FDA Approval Milestone: Cytokinetics achieved a significant milestone in Q4 2025 with the FDA approval of MYQORZO for symptomatic obstructive HCM, marking a successful transition from discovery to commercialization and enhancing its global market position.

- Market Promotion Strategy: CEO Blum emphasized the company's focus on implementing systems, education, and market access pathways to support physicians, patients, and payers, aiming for over 50% new patient preference share for MYQORZO by the end of 2026.

- Financial Performance Review: Total revenues for Q4 2025 reached $17.8 million, up from $16.9 million in the same period of 2024, although the net loss was $183 million, highlighting the financial challenges faced during market expansion.

- Future Outlook: CFO Lee indicated ongoing investments in R&D and marketing for 2026, and while no product sales guidance was provided, the launch of MYQORZO and the submission of the supplemental NDA for MAPLE-HCM are expected to lay the groundwork for future growth.

See More

DAFNA Capital Management Reduces Stake in Biotechnology ETF

- Share Reduction: DAFNA Capital Management sold 34,405 shares of iShares Biotechnology ETF (IBB) in Q4 2025, resulting in a $3.31 million decrease in quarter-end position value, reflecting both trading activities and stock price fluctuations.

- Asset Management Impact: This transaction reduced IBB's share of DAFNA's 13F reportable assets to 2.67%, indicating that IBB is no longer among the fund's top five holdings, which highlights its diminishing significance in the investment portfolio.

- Market Performance: As of February 17, 2026, IBB's price stood at $174.02, marking a 27.2% increase over the past year, with an alpha of 15.84 percentage points compared to the S&P 500, showcasing the ETF's strong performance in the biotechnology sector.

- Investment Strategy: The iShares Biotechnology ETF primarily invests in large, commercial-stage biotech companies and employs a passive investment strategy aimed at efficient index replication and liquidity management, although it remains sensitive to interest rates and investor risk appetite.

See More

DAFNA Capital Management Reduces Stake in iShares Biotechnology ETF

- Stake Reduction Details: According to an SEC filing dated February 17, 2026, DAFNA Capital Management reduced its stake in the iShares Biotechnology ETF by 34,405 shares during Q4 2025, resulting in a $3.31 million decrease in position value, highlighting the impact of market fluctuations on the portfolio.

- Asset Allocation Shift: Following the sale, the iShares Biotechnology ETF now comprises 2.67% of DAFNA Capital's 13F reportable assets, indicating a relative decline in the ETF's significance within the overall investment strategy.

- Top Holdings Overview: As of February 17, 2026, DAFNA's top five holdings include NASDAQ:RVMD at $48.15 million (11.3% of AUM) and NYSEMKT:XBI at $41.03 million (9.7% of AUM), reflecting a continued focus on large-cap biotech firms in its investment approach.

- ETF Performance Analysis: As of February 17, 2026, the iShares Biotechnology ETF was priced at $174.02, up 27.2% over the past year, demonstrating stable performance in the biotech sector, though it remains sensitive to shifts in market risk appetite for growth-oriented healthcare stocks.

See More

Cytokinetics Executive's Major Stock Sale Raises Eyebrows

- Executive Stock Transaction: On February 5, 2026, Cytokinetics' Executive Vice President Andrew Callos exercised 15,000 stock options and immediately sold them for approximately $928,950, indicating a liquidity-driven decision.

- Ownership Percentage Shift: Following the transaction, Callos' direct ownership decreased from 65,440 shares to 50,440 shares, lowering his direct equity stake to 0.04%, which reflects a significant reduction in his equity exposure within the company.

- Market Reaction Analysis: The sale price of around $61.93 per share was slightly above the market close of $60.24 on the same day, suggesting favorable execution that could positively influence investor confidence.

- Company Strategic Context: Cytokinetics is at a commercial stage with its first product myqorzo recently launched, and despite a net loss of nearly $785 million in 2025, its potential in the cardiovascular sector attracts high-risk investors looking for growth opportunities.

See More

Cytokinetics Executive Sells Stock Options

- Stock Option Sale: On February 5, 2026, Andrew Callos, Chief Commercial Officer of Cytokinetics, exercised 15,000 stock options and sold them for approximately $928,950, indicating his confidence in the company's future prospects.

- Reduction in Holdings: This transaction reduced Callos' direct holdings from 65,440 shares to 50,440 shares, accounting for 22.9% of his total holdings, reflecting a strategic decision to decrease his stake in the company.

- Market Reaction: Following the FDA's approval of myqorzo in December 2025, Cytokinetics' stock surged over 92% in six months, and the timing of this sale coincides with the launch of the company's first commercial product, potentially impacting investor sentiment.

- Financial Position: Despite Cytokinetics reporting a net loss of nearly $785 million in 2025, its strategic focus on the cardiovascular sector and the introduction of new products provide potential for future growth.

See More

MongoDB and Warner Bros Options Trading Activity

- MongoDB Options Volume: As of now, MongoDB Inc's options volume has reached 12,327 contracts, equivalent to approximately 1.2 million shares, indicating a trading activity level that is 72.8% of its average daily volume over the past month, reflecting heightened market interest in the stock.

- High-Frequency Trading Insight: Notably, the $200 strike put option expiring on February 27, 2026, has seen a trading volume of 865 contracts today, representing about 86,500 underlying shares, which suggests investor expectations regarding future price volatility.

- Warner Bros Options Activity: Concurrently, Warner Bros Discovery Inc's options volume stands at 165,162 contracts, translating to approximately 16.5 million shares, which constitutes 70.4% of its average daily trading volume over the past month, indicating sustained market interest in the company.

- Bullish Call Options: For the $30 strike call option expiring on March 20, 2026, today's trading volume has reached 26,710 contracts, or about 2.7 million shares, reflecting investor optimism regarding Warner Bros' future performance.

See More

Cytokinetics Q4 2025 Earnings Call Highlights

- FDA Approval Milestone: Cytokinetics achieved a significant milestone in Q4 2025 with the FDA approval of MYQORZO for symptomatic obstructive HCM, marking a successful transition from discovery to commercialization and enhancing its global market position.

- Market Promotion Strategy: CEO Blum emphasized the company's focus on implementing systems, education, and market access pathways to support physicians, patients, and payers, aiming for over 50% new patient preference share for MYQORZO by the end of 2026.

- Financial Performance Review: Total revenues for Q4 2025 reached $17.8 million, up from $16.9 million in the same period of 2024, although the net loss was $183 million, highlighting the financial challenges faced during market expansion.

- Future Outlook: CFO Lee indicated ongoing investments in R&D and marketing for 2026, and while no product sales guidance was provided, the launch of MYQORZO and the submission of the supplemental NDA for MAPLE-HCM are expected to lay the groundwork for future growth.

See More