Cloudflare Acquires AI Data Marketplace Human Native to Enhance Creator Monetization

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Jan 15 2026

0mins

Should l Buy NET?

Source: CNBC

- Acquisition Strategy: Cloudflare announced the acquisition of AI data marketplace Human Native to establish a more efficient transaction platform between AI developers and content creators, thereby enhancing creators' control over their work.

- Tool Development: This acquisition will enable Cloudflare to develop tools that allow AI developers to find, access, and purchase high-quality data through fair and transparent channels, further enhancing its competitiveness in the AI sector.

- Content Monetization: Cloudflare CEO Matthew Prince stated that the acquisition will accelerate the development of a new system where AI developers pay creators for using their content to train models, evolving the monetization model for content creators.

- Market Reaction: Cloudflare's cybersecurity products have contributed to a stock price increase of over 60% in the past year, and this acquisition is expected to further solidify its position in the AI market and attract more investor interest.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy NET?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on NET

Wall Street analysts forecast NET stock price to rise

25 Analyst Rating

15 Buy

10 Hold

0 Sell

Moderate Buy

Current: 212.360

Low

131.00

Averages

253.24

High

318.00

Current: 212.360

Low

131.00

Averages

253.24

High

318.00

About NET

Cloudflare, Inc. is a connectivity cloud company. The Company delivers a range of services to businesses of all sizes and in all geographies, enhancing the performance of business-critical applications. Its full suite of products consists of application services that help deliver security, performance, and reliability for any organization's applications connected to the Internet, including Websites and application programming interfaces (APIs) and its secure access service edge (SASE) platform, which contains its suite of and workplace security services and network services solutions to help ensure traffic in and out of an organization’s network and devices is verified and authorized and data is protected and secured, as well as to securely connect data centers, cloud services, and branch offices to an organization with its connectivity cloud. The Company also offers developer-based solutions which build and deploys serverless and artificial intelligence applications.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Cloudflare Reports 34% Revenue Growth in Q4

- Significant Revenue Growth: Cloudflare achieved $614.5 million in revenue for Q4, marking a 34% year-over-year increase, driven in part by the launch and scaling of AI agents, showcasing the company's robust performance in digital infrastructure.

- Increased Contract Value: The average annual contract value (ACV) surged nearly 50% year-over-year to $42.5 million, with the company closing its largest one-year deal in history, indicating its growing competitiveness among larger clients.

- Strong Profitability: Cloudflare reported a non-GAAP net income of $89.6 million in Q4, achieving a 15% net income margin, which reflects the company's ability to enhance profitability alongside sales growth, further solidifying its market position.

- Optimistic Future Outlook: For 2023, Cloudflare projects sales between $2.785 billion and $2.795 billion, representing approximately 29% growth at the midpoint, while adjusted earnings per share are expected to rise from $0.93 last year to between $1.11 and $1.12, indicating strong growth potential over the next decade.

See More

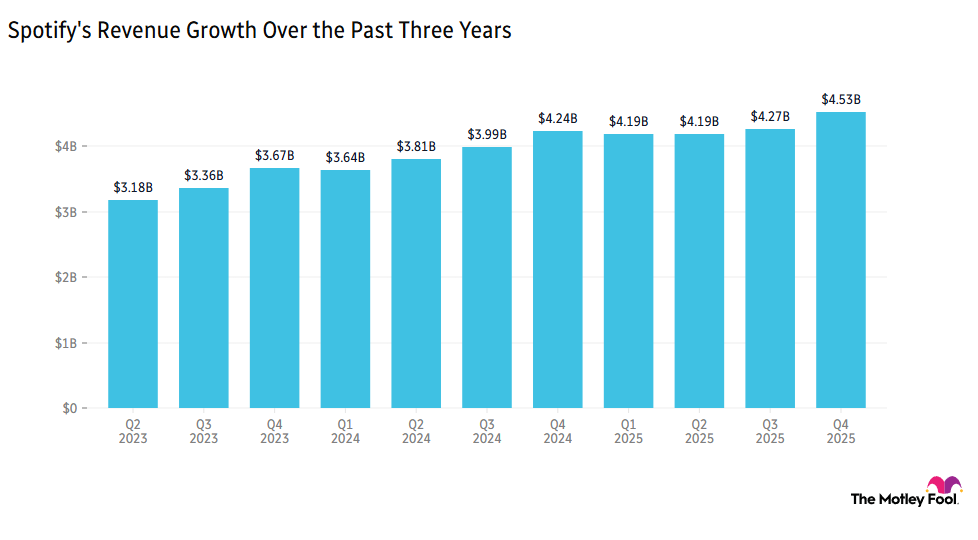

Spotify's Profit Forecast Falls Short of Expectations

- Ad Revenue Decline: Spotify's ad-supported revenue fell by 5% year-over-year, causing the stock to drop over 9% ahead of market open, reflecting concerns about growth, particularly in major markets like the U.S.

- Disappointing Profit Guidance: While overall revenue grew by 10%, the outlook for operating income and premium subscriber growth for the upcoming quarter disappointed investors, indicating challenges in major markets.

- User Growth Drivers: All key performance indicators met or exceeded expectations, with advanced AI-powered personalization tools and enhancements to the mobile free tier driving accelerated user growth, despite a weak overall growth outlook.

- Strong Market Performance: Since January 2022, Spotify's stock has outperformed the S&P 500 by 78%, demonstrating robust performance under specific market conditions, even as current profit forecasts raise investor concerns.

See More

SpaceX Aims for Record IPO Valuation

- IPO Potential: SpaceX is planning a record IPO with a projected valuation of up to $1.75 trillion, which, if successful, would make it the largest IPO in history, reflecting strong market confidence in its future growth.

- Diversified Business: In addition to rocket launches, SpaceX owns the Starlink satellite internet service and the AI business xAI, which merged with SpaceX at a valuation of $1.25 trillion, further strengthening the company's market position.

- Retail Investor Opportunities: SpaceX plans to allocate a significant portion of shares for retail investors, although specific arrangements are not yet clear, this move could make it easier for ordinary investors to participate in the IPO, breaking the traditional focus on institutional investors.

- Historical Insights: Historical data shows that many tech companies experience price fluctuations post-IPO, indicating that investors often find multiple reasonable entry points after the market debut, suggesting that there is no need to rush into the SpaceX IPO.

See More

Cloudflare Sees 50% Growth in Annual Contract Value

- Significant Revenue Growth: Cloudflare achieved $614.5 million in revenue for Q4 last year, marking a 34% year-over-year increase, driven in part by the launch and scaling of AI agents, showcasing the company's strong performance in the rapidly evolving web services market.

- Contract Value Increase: The company's average annual contract value (ACV) surged nearly 50% year-over-year to $42.5 million, indicating that Cloudflare is securing larger contracts among major clients while also upselling additional services to small and mid-sized customers, further solidifying its market position.

- Strong Profitability: Cloudflare reported a non-GAAP net income of $89.6 million in Q4, achieving a 15% net income margin, which reflects the company's ability to maintain high gross margins while also enhancing profitability, suggesting potential for future earnings expansion.

- Optimistic Future Outlook: Cloudflare is guiding for sales between $2.785 billion and $2.795 billion for 2023, representing approximately 29% growth at the midpoint, while adjusted earnings per share are expected to rise from $0.93 last year to between $1.11 and $1.12, indicating strong growth momentum driven by AI opportunities.

See More

SentinelOne Stock Investment Thesis Overview

- Market Positioning Advantage: SentinelOne stands out in the rapidly evolving cybersecurity landscape due to its AI-native architecture, enabling machine-speed threat detection and rapid remediation, serving 35% of Fortune 500 companies, including Tesla and Amazon, showcasing its strong competitive edge in the market.

- Financial Health: The company boasts $750 million in cash with no debt, supporting its growth and innovation initiatives, with projected revenue reaching $2.5 billion by 2030, implying a potential market cap of $18.75 billion—nearly four times its current valuation, highlighting its investment appeal.

- Product Growth Potential: Emerging AI products have seen quarterly ARR doubling, with triple-digit growth in data and cloud solutions, indicating rapid market share expansion amid rising demand for integrated cybersecurity solutions.

- Valuation Attractiveness: Trading at a FY27 sales multiple of 3.5x compared to 16x for CrowdStrike, along with a PEG of 0.4, SentinelOne presents a compelling investment opportunity due to its significant discount relative to peers, drawing investor interest.

See More

Analysis of Cloud Computing ETF Performance

- SKYY Fund Performance: The First Trust Cloud Computing ETF (SKYY) is down 10% year-to-date but up 20% over the past year, currently priced around $118, indicating its stability in the cloud computing sector, particularly as AI capital expenditures attract infrastructure-heavy investors.

- WCLD Fund Volatility: The WisdomTree Cloud Computing Fund (WCLD) has declined 22% year-to-date and 12% over the trailing year, trading near $27, primarily impacted by AI disruption concerns, reflecting the vulnerability of pure-play software companies amid market fluctuations.

- CLOD Fund Positioning: The Themes Cloud Computing ETF (CLOD) launched as a lower-cost thematic fund, down 14% year-to-date but up 1% over the past year, currently priced around $28, providing a new option for cost-sensitive investors despite its shorter trading history.

- Market Trend Analysis: Enterprise digital transformation and AI-driven infrastructure spending are propelling cloud demand; however, profit pressures and interest rate sensitivity faced by pure software companies create divergent performance across different ETF types, necessitating investors to choose funds based on their risk tolerance.

See More

Cloudflare Reports 34% Revenue Growth in Q4

- Significant Revenue Growth: Cloudflare achieved $614.5 million in revenue for Q4, marking a 34% year-over-year increase, driven in part by the launch and scaling of AI agents, showcasing the company's robust performance in digital infrastructure.

- Increased Contract Value: The average annual contract value (ACV) surged nearly 50% year-over-year to $42.5 million, with the company closing its largest one-year deal in history, indicating its growing competitiveness among larger clients.

- Strong Profitability: Cloudflare reported a non-GAAP net income of $89.6 million in Q4, achieving a 15% net income margin, which reflects the company's ability to enhance profitability alongside sales growth, further solidifying its market position.

- Optimistic Future Outlook: For 2023, Cloudflare projects sales between $2.785 billion and $2.795 billion, representing approximately 29% growth at the midpoint, while adjusted earnings per share are expected to rise from $0.93 last year to between $1.11 and $1.12, indicating strong growth potential over the next decade.

See More

Spotify's Profit Forecast Falls Short of Expectations

- Ad Revenue Decline: Spotify's ad-supported revenue fell by 5% year-over-year, causing the stock to drop over 9% ahead of market open, reflecting concerns about growth, particularly in major markets like the U.S.

- Disappointing Profit Guidance: While overall revenue grew by 10%, the outlook for operating income and premium subscriber growth for the upcoming quarter disappointed investors, indicating challenges in major markets.

- User Growth Drivers: All key performance indicators met or exceeded expectations, with advanced AI-powered personalization tools and enhancements to the mobile free tier driving accelerated user growth, despite a weak overall growth outlook.

- Strong Market Performance: Since January 2022, Spotify's stock has outperformed the S&P 500 by 78%, demonstrating robust performance under specific market conditions, even as current profit forecasts raise investor concerns.

See More

SpaceX Aims for Record IPO Valuation

- IPO Potential: SpaceX is planning a record IPO with a projected valuation of up to $1.75 trillion, which, if successful, would make it the largest IPO in history, reflecting strong market confidence in its future growth.

- Diversified Business: In addition to rocket launches, SpaceX owns the Starlink satellite internet service and the AI business xAI, which merged with SpaceX at a valuation of $1.25 trillion, further strengthening the company's market position.

- Retail Investor Opportunities: SpaceX plans to allocate a significant portion of shares for retail investors, although specific arrangements are not yet clear, this move could make it easier for ordinary investors to participate in the IPO, breaking the traditional focus on institutional investors.

- Historical Insights: Historical data shows that many tech companies experience price fluctuations post-IPO, indicating that investors often find multiple reasonable entry points after the market debut, suggesting that there is no need to rush into the SpaceX IPO.

See More

Cloudflare Sees 50% Growth in Annual Contract Value

- Significant Revenue Growth: Cloudflare achieved $614.5 million in revenue for Q4 last year, marking a 34% year-over-year increase, driven in part by the launch and scaling of AI agents, showcasing the company's strong performance in the rapidly evolving web services market.

- Contract Value Increase: The company's average annual contract value (ACV) surged nearly 50% year-over-year to $42.5 million, indicating that Cloudflare is securing larger contracts among major clients while also upselling additional services to small and mid-sized customers, further solidifying its market position.

- Strong Profitability: Cloudflare reported a non-GAAP net income of $89.6 million in Q4, achieving a 15% net income margin, which reflects the company's ability to maintain high gross margins while also enhancing profitability, suggesting potential for future earnings expansion.

- Optimistic Future Outlook: Cloudflare is guiding for sales between $2.785 billion and $2.795 billion for 2023, representing approximately 29% growth at the midpoint, while adjusted earnings per share are expected to rise from $0.93 last year to between $1.11 and $1.12, indicating strong growth momentum driven by AI opportunities.

See More

SentinelOne Stock Investment Thesis Overview

- Market Positioning Advantage: SentinelOne stands out in the rapidly evolving cybersecurity landscape due to its AI-native architecture, enabling machine-speed threat detection and rapid remediation, serving 35% of Fortune 500 companies, including Tesla and Amazon, showcasing its strong competitive edge in the market.

- Financial Health: The company boasts $750 million in cash with no debt, supporting its growth and innovation initiatives, with projected revenue reaching $2.5 billion by 2030, implying a potential market cap of $18.75 billion—nearly four times its current valuation, highlighting its investment appeal.

- Product Growth Potential: Emerging AI products have seen quarterly ARR doubling, with triple-digit growth in data and cloud solutions, indicating rapid market share expansion amid rising demand for integrated cybersecurity solutions.

- Valuation Attractiveness: Trading at a FY27 sales multiple of 3.5x compared to 16x for CrowdStrike, along with a PEG of 0.4, SentinelOne presents a compelling investment opportunity due to its significant discount relative to peers, drawing investor interest.

See More

Analysis of Cloud Computing ETF Performance

- SKYY Fund Performance: The First Trust Cloud Computing ETF (SKYY) is down 10% year-to-date but up 20% over the past year, currently priced around $118, indicating its stability in the cloud computing sector, particularly as AI capital expenditures attract infrastructure-heavy investors.

- WCLD Fund Volatility: The WisdomTree Cloud Computing Fund (WCLD) has declined 22% year-to-date and 12% over the trailing year, trading near $27, primarily impacted by AI disruption concerns, reflecting the vulnerability of pure-play software companies amid market fluctuations.

- CLOD Fund Positioning: The Themes Cloud Computing ETF (CLOD) launched as a lower-cost thematic fund, down 14% year-to-date but up 1% over the past year, currently priced around $28, providing a new option for cost-sensitive investors despite its shorter trading history.

- Market Trend Analysis: Enterprise digital transformation and AI-driven infrastructure spending are propelling cloud demand; however, profit pressures and interest rate sensitivity faced by pure software companies create divergent performance across different ETF types, necessitating investors to choose funds based on their risk tolerance.

See More