China's Smartphone Market Continues Decline

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 1 day ago

0mins

Should l Buy TTGT?

Source: Newsfilter

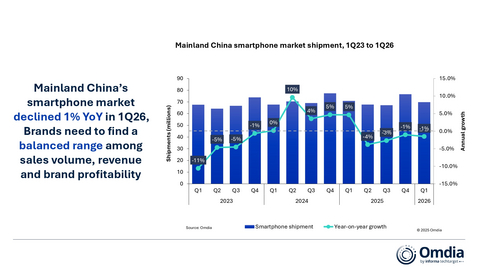

- Market Shipment Decline: According to Omdia's latest research, the smartphone market in Mainland China saw a 1% year-on-year decline in Q1 2026, with shipments reaching 69.8 million units, indicating weak overall market demand and a projected 10% contraction for the year.

- Top Vendors Performance: Huawei led the market with shipments of 13.9 million units, capturing a 20% market share, while Apple followed closely with 13.1 million units and a 19% share, demonstrating their competitive advantages in the current landscape.

- Pricing Strategy Impact: Several major vendors, including Xiaomi, OPPO, and vivo, raised retail prices on select models by 10-30% in Q1, which negatively affected consumer purchasing sentiment, whereas Huawei and Apple avoided broad price hikes, successfully capturing market share and achieving better sales results.

- Innovation and Market Outlook: Omdia forecasts that meaningful innovations in flagship and foldable devices will help stabilize overall demand, with breakthroughs in AI functionalities becoming crucial for vendors to enhance brand perception and establish strategic advantages, despite ongoing challenges from memory price volatility.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy TTGT?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on TTGT

Wall Street analysts forecast TTGT stock price to rise

3 Analyst Rating

3 Buy

0 Hold

0 Sell

Strong Buy

Current: 4.020

Low

10.00

Averages

11.67

High

15.00

Current: 4.020

Low

10.00

Averages

11.67

High

15.00

About TTGT

TechTarget, Inc., which also refers to itself as Informa TechTarget, is a business-to-business (B2B) growth accelerator that informs, influences and connects the world’s technology buyers and sellers, helping accelerate growth from R&D to return on investment (ROI). It has scale in permissioned B2B first-party data and a unique end-to-end portfolio of data-driven solutions that services the full B2B product lifecycle, from R&D to ROI: from strategy, messaging and content development to in-market activation via brand, demand generation, purchase intent data and sales enablement. In intelligence and advisory, it offers expert analyst, data-driven intelligence products and advisory services to product managers, corporate strategists and the C-suite, challenging market strategies and sharpening product roadmaps. In brand and content, it provides expert editorial, data-driven brand products and content marketing services for brand marketers, product marketers and content marketers.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

VIDAA Expected to Overtake LG's webOS in European Shipments by 2025

- Market Share Growth: Omdia forecasts that VIDAA will surpass LG's webOS in 2025, becoming the leading smart TV operating system in Europe, indicating a significant shift in market dynamics and the rise of Chinese brands globally.

- Strong Shipment Volume: Hisense has significantly increased VIDAA's market share through competitive pricing and a broad distribution network, with shipments expected to exceed LG's for the first time this year, further solidifying its position in Europe.

- Industry Structural Shift: Omdia analysts note that as Chinese manufacturers like Hisense and TCL rapidly expand in both hardware and platform, traditional Korean brands face increasing challenges, leading to heightened competition in the market.

- Multi-Platform Strategy Challenges: As audiences spread across multiple platforms, advertisers and content providers will need more sophisticated multi-platform strategies to achieve scale, presenting new challenges for the industry while also facilitating the rise of emerging operating systems like Titan OS.

See More

Enterprises Urged to Address Five Key Risk Areas in AI Networking

- Importance of Network Infrastructure: Omdia's study reveals that while 50 neocloud providers have scaled compute for AI workloads, networking infrastructure has become a critical constraint, impacting AI performance and the ability to securely process data.

- Skills Gap and Accountability: 43% of neoclouds are seeking network engineers and security specialists to fill urgent competency gaps, while over a third minimize contractual liability regarding network uptime, security, and data sovereignty, necessitating enhanced scrutiny.

- Cloud Access and IP Assets: More than half of neoclouds do not utilize Internet peering exchanges, which affects efficient cloud connectivity, and 46% only control small IPv4 address blocks, limiting their rapid growth and traffic localization capabilities.

- IP Transit Resilience Risks: One in five neoclouds relies on a single IP transit provider, creating a potential single point of failure, highlighting the evolving neocloud networking strategies and increasing dependence on infrastructure globally.

See More

China's Smartphone Market Continues Decline

- Market Shipment Decline: According to Omdia's latest research, the smartphone market in Mainland China saw a 1% year-on-year decline in Q1 2026, with shipments reaching 69.8 million units, indicating weak overall market demand and a projected 10% contraction for the year.

- Top Vendors Performance: Huawei led the market with shipments of 13.9 million units, capturing a 20% market share, while Apple followed closely with 13.1 million units and a 19% share, demonstrating their competitive advantages in the current landscape.

- Pricing Strategy Impact: Several major vendors, including Xiaomi, OPPO, and vivo, raised retail prices on select models by 10-30% in Q1, which negatively affected consumer purchasing sentiment, whereas Huawei and Apple avoided broad price hikes, successfully capturing market share and achieving better sales results.

- Innovation and Market Outlook: Omdia forecasts that meaningful innovations in flagship and foldable devices will help stabilize overall demand, with breakthroughs in AI functionalities becoming crucial for vendors to enhance brand perception and establish strategic advantages, despite ongoing challenges from memory price volatility.

See More

2026 Analysis of China's Smartphone Market

- Market Shipment Decline: In Q1 2026, China's smartphone shipments fell by 1% year-on-year to 69.8 million units, primarily due to rising component costs, especially memory prices, prompting major vendors to raise product prices and further exacerbating market decline.

- Strong Performance by Huawei and Apple: Huawei led with shipments of 13.9 million units, capturing a 20% market share, while Apple followed closely with 13.1 million units and a 19% share, demonstrating their strategic advantages in the competitive landscape.

- Price Strategy Impact on Consumer Sentiment: Major vendors like Xiaomi, HONOR, OPPO, and vivo raised retail prices on select models by 10-30% in Q1, which negatively affected consumer purchasing sentiment, while Huawei and Apple attracted market share by largely avoiding broad price hikes.

- Market Outlook Forecast: Omdia projects that China's smartphone market will shrink by 10% in 2026 due to ongoing rising memory costs, which will have profound implications for the competitive landscape, necessitating vigilance in supply chains, R&D, and innovation among vendors.

See More

Global Smartphone Market Grows 1% Amid Cost Pressures

- Market Growth Overview: According to Omdia's latest research, the global smartphone market grew by 1% year-on-year in Q1 2026, although this growth does not fully reflect the rising supply-side costs, indicating a fragile demand outlook.

- Escalating Cost Pressures: Mobile DRAM and NAND prices surged by approximately 90% quarter-on-quarter in Q1 and are expected to rise another 30% in Q2, significantly increasing bill-of-materials and forcing vendors to raise prices to protect margins.

- Brand Performance Disparities: Samsung reclaimed the top market position in Q1, supported by strong pre-orders for the Galaxy S26 series, while Apple performed well due to stable demand for the iPhone 17 series, despite facing regional supply disruptions.

- Future Outlook: Omdia anticipates a 15% decline in global smartphone shipments in 2026, prompting vendors to focus on margin protection and high-value opportunities to navigate intensifying cost pressures and macroeconomic volatility.

See More

Global Traditional TV and Online Video Revenues to Exceed $1 Trillion

- Revenue Growth Forecast: According to Omdia, global traditional TV and online video revenues are projected to rise from $775 billion in 2025 to $1.03 trillion by 2030, indicating a significant structural shift in the media and entertainment industry, primarily driven by digital formats.

- Advertising-Led Growth: Online video advertising is expected to be the main growth engine, increasing from $309 billion in 2025 to $540 billion in 2030, with its share of total revenues rising from 40% to 53%, reflecting the robust growth of advertising models.

- Impact of Social Video Platforms: Platforms like Meta, TikTok, and YouTube are set to play a crucial role in online video advertising, generating approximately $400 billion in streaming ad revenues by 2030, fundamentally transforming content consumption and monetization strategies.

- Decline of Traditional Models: Linear TV advertising revenue is forecasted to decline from $123 billion in 2025 to $113 billion by 2030, with its market share dropping from 16% to 11%, highlighting the ongoing trend of audience migration towards digital platforms.

See More

VIDAA Expected to Overtake LG's webOS in European Shipments by 2025

- Market Share Growth: Omdia forecasts that VIDAA will surpass LG's webOS in 2025, becoming the leading smart TV operating system in Europe, indicating a significant shift in market dynamics and the rise of Chinese brands globally.

- Strong Shipment Volume: Hisense has significantly increased VIDAA's market share through competitive pricing and a broad distribution network, with shipments expected to exceed LG's for the first time this year, further solidifying its position in Europe.

- Industry Structural Shift: Omdia analysts note that as Chinese manufacturers like Hisense and TCL rapidly expand in both hardware and platform, traditional Korean brands face increasing challenges, leading to heightened competition in the market.

- Multi-Platform Strategy Challenges: As audiences spread across multiple platforms, advertisers and content providers will need more sophisticated multi-platform strategies to achieve scale, presenting new challenges for the industry while also facilitating the rise of emerging operating systems like Titan OS.

See More

Enterprises Urged to Address Five Key Risk Areas in AI Networking

- Importance of Network Infrastructure: Omdia's study reveals that while 50 neocloud providers have scaled compute for AI workloads, networking infrastructure has become a critical constraint, impacting AI performance and the ability to securely process data.

- Skills Gap and Accountability: 43% of neoclouds are seeking network engineers and security specialists to fill urgent competency gaps, while over a third minimize contractual liability regarding network uptime, security, and data sovereignty, necessitating enhanced scrutiny.

- Cloud Access and IP Assets: More than half of neoclouds do not utilize Internet peering exchanges, which affects efficient cloud connectivity, and 46% only control small IPv4 address blocks, limiting their rapid growth and traffic localization capabilities.

- IP Transit Resilience Risks: One in five neoclouds relies on a single IP transit provider, creating a potential single point of failure, highlighting the evolving neocloud networking strategies and increasing dependence on infrastructure globally.

See More

China's Smartphone Market Continues Decline

- Market Shipment Decline: According to Omdia's latest research, the smartphone market in Mainland China saw a 1% year-on-year decline in Q1 2026, with shipments reaching 69.8 million units, indicating weak overall market demand and a projected 10% contraction for the year.

- Top Vendors Performance: Huawei led the market with shipments of 13.9 million units, capturing a 20% market share, while Apple followed closely with 13.1 million units and a 19% share, demonstrating their competitive advantages in the current landscape.

- Pricing Strategy Impact: Several major vendors, including Xiaomi, OPPO, and vivo, raised retail prices on select models by 10-30% in Q1, which negatively affected consumer purchasing sentiment, whereas Huawei and Apple avoided broad price hikes, successfully capturing market share and achieving better sales results.

- Innovation and Market Outlook: Omdia forecasts that meaningful innovations in flagship and foldable devices will help stabilize overall demand, with breakthroughs in AI functionalities becoming crucial for vendors to enhance brand perception and establish strategic advantages, despite ongoing challenges from memory price volatility.

See More

2026 Analysis of China's Smartphone Market

- Market Shipment Decline: In Q1 2026, China's smartphone shipments fell by 1% year-on-year to 69.8 million units, primarily due to rising component costs, especially memory prices, prompting major vendors to raise product prices and further exacerbating market decline.

- Strong Performance by Huawei and Apple: Huawei led with shipments of 13.9 million units, capturing a 20% market share, while Apple followed closely with 13.1 million units and a 19% share, demonstrating their strategic advantages in the competitive landscape.

- Price Strategy Impact on Consumer Sentiment: Major vendors like Xiaomi, HONOR, OPPO, and vivo raised retail prices on select models by 10-30% in Q1, which negatively affected consumer purchasing sentiment, while Huawei and Apple attracted market share by largely avoiding broad price hikes.

- Market Outlook Forecast: Omdia projects that China's smartphone market will shrink by 10% in 2026 due to ongoing rising memory costs, which will have profound implications for the competitive landscape, necessitating vigilance in supply chains, R&D, and innovation among vendors.

See More

Global Smartphone Market Grows 1% Amid Cost Pressures

- Market Growth Overview: According to Omdia's latest research, the global smartphone market grew by 1% year-on-year in Q1 2026, although this growth does not fully reflect the rising supply-side costs, indicating a fragile demand outlook.

- Escalating Cost Pressures: Mobile DRAM and NAND prices surged by approximately 90% quarter-on-quarter in Q1 and are expected to rise another 30% in Q2, significantly increasing bill-of-materials and forcing vendors to raise prices to protect margins.

- Brand Performance Disparities: Samsung reclaimed the top market position in Q1, supported by strong pre-orders for the Galaxy S26 series, while Apple performed well due to stable demand for the iPhone 17 series, despite facing regional supply disruptions.

- Future Outlook: Omdia anticipates a 15% decline in global smartphone shipments in 2026, prompting vendors to focus on margin protection and high-value opportunities to navigate intensifying cost pressures and macroeconomic volatility.

See More

Global Traditional TV and Online Video Revenues to Exceed $1 Trillion

- Revenue Growth Forecast: According to Omdia, global traditional TV and online video revenues are projected to rise from $775 billion in 2025 to $1.03 trillion by 2030, indicating a significant structural shift in the media and entertainment industry, primarily driven by digital formats.

- Advertising-Led Growth: Online video advertising is expected to be the main growth engine, increasing from $309 billion in 2025 to $540 billion in 2030, with its share of total revenues rising from 40% to 53%, reflecting the robust growth of advertising models.

- Impact of Social Video Platforms: Platforms like Meta, TikTok, and YouTube are set to play a crucial role in online video advertising, generating approximately $400 billion in streaming ad revenues by 2030, fundamentally transforming content consumption and monetization strategies.

- Decline of Traditional Models: Linear TV advertising revenue is forecasted to decline from $123 billion in 2025 to $113 billion by 2030, with its market share dropping from 16% to 11%, highlighting the ongoing trend of audience migration towards digital platforms.

See More