Apple Appoints New CEO, Market Outlook Uncertain

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 1 hour ago

0mins

Should l Buy AAPL?

Source: Fool

- Leadership Transition: Apple has announced that CEO Tim Cook will step down on September 1, with John Ternus taking over; while this change has been anticipated, the market remains uncertain about the company's future direction given the stark contrast in identity between Cook's and Steve Jobs' leadership.

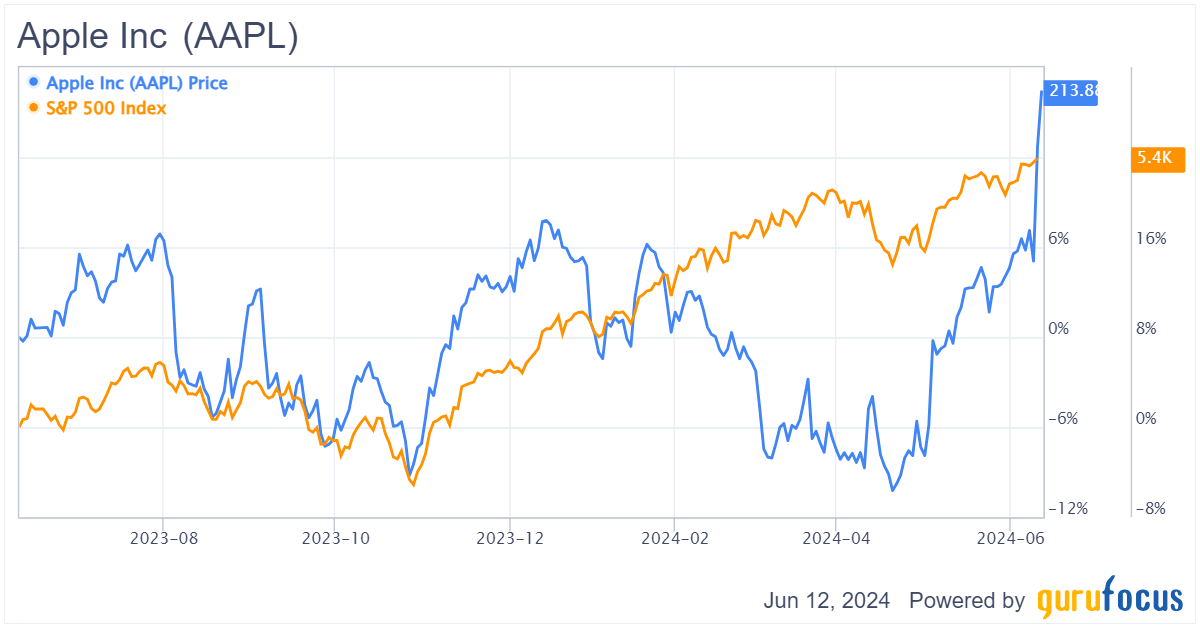

- Valuation Pressure: Currently trading at a price-to-earnings ratio of 34, Apple is at the high end of its valuation range over the past five years, and despite recent improvements, the lack of growth context makes its premium over peers appear unjustified, leading to pessimistic investor expectations for future growth.

- AI Strategy Lagging: Apple's performance in the artificial intelligence sector has disappointed investors, as AI is considered one of the largest tech revolutions; the company's strategy in this area has left it trailing behind competitors, further exacerbating market concerns about its growth prospects.

- Investment Shift: Given Apple's shortcomings in AI, analysts suggest investors consider other rapidly growing companies like Nvidia, Microsoft, and Alphabet, which are demonstrating strong growth driven by cloud computing and AI demand, making them potentially more attractive investment options than Apple.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy AAPL?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on AAPL

Wall Street analysts forecast AAPL stock price to rise

27 Analyst Rating

17 Buy

9 Hold

1 Sell

Moderate Buy

Current: 270.170

Low

239.00

Averages

306.89

High

350.00

Current: 270.170

Low

239.00

Averages

306.89

High

350.00

About AAPL

Apple Inc. designs, manufactures and markets smartphones, personal computers, tablets, wearables and accessories, and sells a variety of related services. Its product categories include iPhone, Mac, iPad, Wearables, Home and Accessories. Its services include advertising, AppleCare, cloud services, digital content, and payment services. The Company operates various platforms, including the App Store, that allow customers to discover and download applications and digital content, such as books, music, video, games and podcasts. It also offers digital content through subscription-based services, including Apple Arcade, Apple Fitness+, Apple Music, Apple News+, and Apple TV+. Its wearables include smartwatches, wireless headphones, and spatial computers. Its products include iPhone 16 Pro, iPhone 16, iPhone 15, iPhone 14, iPhone SE, MacBook Air, MacBook Pro, iMac, Mac mini, Mac Studio, Mac Pro, iPad Pro, iPad Air, AirPods, AirPods Pro, AirPods Max, Apple TV, Apple Vision Pro and others.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Apple Inc. to Release Q2 Earnings on April 30

- Earnings Release Announcement: Apple Inc. is set to release its Q2 2023 earnings after market close on April 30, with analysts anticipating an EPS of $1.94 and revenue of $109.73 billion, indicating sustained strong demand in global markets.

- Analyst Expectations: The projected EPS of $1.94 and revenue of $109.73 billion will provide critical financial health indicators for investors, potentially influencing stock price movements as the earnings date approaches.

- Market Reaction: As the earnings report date nears, investor anticipation for Apple's performance is high, and changes in analyst ratings could significantly impact market sentiment, particularly in the current economic climate where Apple's results will serve as a bellwether for the industry.

- Industry Impact: Apple's earnings report is expected to not only affect its own stock price but also create ripples across the technology sector, influencing investor confidence amid increasing competition and market uncertainties.

See More

Apple Announces Dividend Increase and $100B Buyback Plan

- Dividend Increase: Apple has raised its quarterly dividend by 3.8% to $0.27 per share, reflecting the company's strong cash flow and profitability, aimed at boosting investor confidence and attracting more long-term investors.

- Buyback Plan: The company also announced a $100 billion stock buyback program, which is expected to further enhance earnings per share, increase shareholder value, and demonstrate confidence in future growth prospects.

- Revenue Performance: In Q2, Apple's iPhone revenue approached $57 billion, showcasing robust sales performance despite competitive market pressures, indicating sustained consumer demand for Apple products.

- Market Reaction: Although Apple's stock price slipped following the announcement, the combination of the dividend increase and buyback plan is expected to have a positive impact on shareholders, enhancing market expectations regarding Apple's future financial health.

See More

Apple Reports Strong Q2 Growth Driven by iPhone and Services

- Significant Revenue Growth: Apple reported second-quarter revenue of $111.2 billion, a 16.5% increase from $95.4 billion year-over-year, indicating strong market demand and product appeal, further solidifying its leadership in the global smartphone market.

- Profit Increase: The company's net income reached $29.6 billion, or $2.01 per share, up from $24.8 billion and $1.65 per share a year ago, reflecting successful cost control and operational efficiency improvements.

- Strong iPhone and Services Revenue: iPhone revenue rose from $46.8 billion to $57.0 billion, while services revenue increased from $26.6 billion to $31.0 billion, demonstrating sustained consumer preference for Apple products and rapid growth in its services business, enhancing revenue diversification.

- Shareholder Return Plan: The board declared a quarterly dividend of $0.27 per share and authorized an additional $100 billion share repurchase program, showcasing the company's confidence in future cash flows while providing substantial returns to shareholders.

See More

Intel's Stock Soars 114%, Marking a Historic Market Comeback

- Stock Surge: Intel's stock skyrocketed by 114% in April, marking its best monthly performance ever and reaching a new high for the first time since 2000, reflecting strong market confidence in its turnaround strategy.

- Surge in Demand: With a resurgence in AI demand, Intel's central processing unit (CPU) demand exceeds supply, and the CPU market is projected to double by 2030, reinforcing Intel's core position in the AI era.

- Strategic Investment: The U.S. government invested $8.9 billion in Intel through the CHIPS Act, becoming its largest shareholder, with the current stake valued at over $40 billion, highlighting the importance placed on the U.S. semiconductor industry.

- Manufacturing Capability Boost: Intel's new Arizona plant is producing 18A chips, signaling a recovery in its manufacturing capabilities, while its collaboration with Tesla provides new growth opportunities for future chip production.

See More

Intel Shares Surge 114%, Reaching Historic Highs

- Stock Surge: Intel's stock skyrocketed by 114% in April, pushing its market cap past $470 billion, marking the best month in its 55-year history on Nasdaq and reflecting strong market confidence in its turnaround efforts.

- Performance Recovery: Following a staggering 60% drop in 2024, Intel's stock has nearly quintupled, indicating investor optimism driven by the promising demand for its new 18A chips, particularly as data center CPU demand exceeds supply.

- Strategic Investment: The U.S. government invested $8.9 billion in Intel through the CHIPS Act, becoming its largest shareholder, with the current stake valued at over $40 billion, highlighting the government's commitment to reshaping the semiconductor industry.

- Manufacturing Capability Boost: Intel is set to collaborate with Musk's Terafab in Texas to design and manufacture ultra-high-performance chips, further solidifying its market position in advanced packaging and manufacturing, which is expected to drive significant revenue growth in the future.

See More

Apple Appoints New CEO, Market Outlook Uncertain

- Leadership Transition: Apple has announced that CEO Tim Cook will step down on September 1, with John Ternus taking over; while this change has been anticipated, the market remains uncertain about the company's future direction given the stark contrast in identity between Cook's and Steve Jobs' leadership.

- Valuation Pressure: Currently trading at a price-to-earnings ratio of 34, Apple is at the high end of its valuation range over the past five years, and despite recent improvements, the lack of growth context makes its premium over peers appear unjustified, leading to pessimistic investor expectations for future growth.

- AI Strategy Lagging: Apple's performance in the artificial intelligence sector has disappointed investors, as AI is considered one of the largest tech revolutions; the company's strategy in this area has left it trailing behind competitors, further exacerbating market concerns about its growth prospects.

- Investment Shift: Given Apple's shortcomings in AI, analysts suggest investors consider other rapidly growing companies like Nvidia, Microsoft, and Alphabet, which are demonstrating strong growth driven by cloud computing and AI demand, making them potentially more attractive investment options than Apple.

See More

Apple Inc. to Release Q2 Earnings on April 30

- Earnings Release Announcement: Apple Inc. is set to release its Q2 2023 earnings after market close on April 30, with analysts anticipating an EPS of $1.94 and revenue of $109.73 billion, indicating sustained strong demand in global markets.

- Analyst Expectations: The projected EPS of $1.94 and revenue of $109.73 billion will provide critical financial health indicators for investors, potentially influencing stock price movements as the earnings date approaches.

- Market Reaction: As the earnings report date nears, investor anticipation for Apple's performance is high, and changes in analyst ratings could significantly impact market sentiment, particularly in the current economic climate where Apple's results will serve as a bellwether for the industry.

- Industry Impact: Apple's earnings report is expected to not only affect its own stock price but also create ripples across the technology sector, influencing investor confidence amid increasing competition and market uncertainties.

See More

Apple Announces Dividend Increase and $100B Buyback Plan

- Dividend Increase: Apple has raised its quarterly dividend by 3.8% to $0.27 per share, reflecting the company's strong cash flow and profitability, aimed at boosting investor confidence and attracting more long-term investors.

- Buyback Plan: The company also announced a $100 billion stock buyback program, which is expected to further enhance earnings per share, increase shareholder value, and demonstrate confidence in future growth prospects.

- Revenue Performance: In Q2, Apple's iPhone revenue approached $57 billion, showcasing robust sales performance despite competitive market pressures, indicating sustained consumer demand for Apple products.

- Market Reaction: Although Apple's stock price slipped following the announcement, the combination of the dividend increase and buyback plan is expected to have a positive impact on shareholders, enhancing market expectations regarding Apple's future financial health.

See More

Apple Reports Strong Q2 Growth Driven by iPhone and Services

- Significant Revenue Growth: Apple reported second-quarter revenue of $111.2 billion, a 16.5% increase from $95.4 billion year-over-year, indicating strong market demand and product appeal, further solidifying its leadership in the global smartphone market.

- Profit Increase: The company's net income reached $29.6 billion, or $2.01 per share, up from $24.8 billion and $1.65 per share a year ago, reflecting successful cost control and operational efficiency improvements.

- Strong iPhone and Services Revenue: iPhone revenue rose from $46.8 billion to $57.0 billion, while services revenue increased from $26.6 billion to $31.0 billion, demonstrating sustained consumer preference for Apple products and rapid growth in its services business, enhancing revenue diversification.

- Shareholder Return Plan: The board declared a quarterly dividend of $0.27 per share and authorized an additional $100 billion share repurchase program, showcasing the company's confidence in future cash flows while providing substantial returns to shareholders.

See More

Intel's Stock Soars 114%, Marking a Historic Market Comeback

- Stock Surge: Intel's stock skyrocketed by 114% in April, marking its best monthly performance ever and reaching a new high for the first time since 2000, reflecting strong market confidence in its turnaround strategy.

- Surge in Demand: With a resurgence in AI demand, Intel's central processing unit (CPU) demand exceeds supply, and the CPU market is projected to double by 2030, reinforcing Intel's core position in the AI era.

- Strategic Investment: The U.S. government invested $8.9 billion in Intel through the CHIPS Act, becoming its largest shareholder, with the current stake valued at over $40 billion, highlighting the importance placed on the U.S. semiconductor industry.

- Manufacturing Capability Boost: Intel's new Arizona plant is producing 18A chips, signaling a recovery in its manufacturing capabilities, while its collaboration with Tesla provides new growth opportunities for future chip production.

See More

Intel Shares Surge 114%, Reaching Historic Highs

- Stock Surge: Intel's stock skyrocketed by 114% in April, pushing its market cap past $470 billion, marking the best month in its 55-year history on Nasdaq and reflecting strong market confidence in its turnaround efforts.

- Performance Recovery: Following a staggering 60% drop in 2024, Intel's stock has nearly quintupled, indicating investor optimism driven by the promising demand for its new 18A chips, particularly as data center CPU demand exceeds supply.

- Strategic Investment: The U.S. government invested $8.9 billion in Intel through the CHIPS Act, becoming its largest shareholder, with the current stake valued at over $40 billion, highlighting the government's commitment to reshaping the semiconductor industry.

- Manufacturing Capability Boost: Intel is set to collaborate with Musk's Terafab in Texas to design and manufacture ultra-high-performance chips, further solidifying its market position in advanced packaging and manufacturing, which is expected to drive significant revenue growth in the future.

See More

Apple Appoints New CEO, Market Outlook Uncertain

- Leadership Transition: Apple has announced that CEO Tim Cook will step down on September 1, with John Ternus taking over; while this change has been anticipated, the market remains uncertain about the company's future direction given the stark contrast in identity between Cook's and Steve Jobs' leadership.

- Valuation Pressure: Currently trading at a price-to-earnings ratio of 34, Apple is at the high end of its valuation range over the past five years, and despite recent improvements, the lack of growth context makes its premium over peers appear unjustified, leading to pessimistic investor expectations for future growth.

- AI Strategy Lagging: Apple's performance in the artificial intelligence sector has disappointed investors, as AI is considered one of the largest tech revolutions; the company's strategy in this area has left it trailing behind competitors, further exacerbating market concerns about its growth prospects.

- Investment Shift: Given Apple's shortcomings in AI, analysts suggest investors consider other rapidly growing companies like Nvidia, Microsoft, and Alphabet, which are demonstrating strong growth driven by cloud computing and AI demand, making them potentially more attractive investment options than Apple.

See More