AMD Named Among Top Stocks to Outperform S&P 500

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 3 days ago

0mins

Should l Buy AMD?

Source: Yahoo Finance

- Price Target Increase: TD Cowen raised AMD's price target from $290 to $500 while reiterating a Buy rating, indicating increased market confidence in AMD's future growth, particularly in the expanding server CPU market.

- Strong Quarterly Performance: Cantor Fitzgerald lifted AMD's price target from $450 to $500, highlighting the company's accelerated growth in server CPUs and AI GPUs, with revenue and earnings per share exceeding market expectations, showcasing its robust market performance.

- Growing Market Demand: AMD's decision to double its total addressable market forecast for server CPUs reflects the company's confidence in future data center opportunities, especially against the backdrop of rising AI-related demand.

- Challenges and Opportunities: Despite facing some margin pressures and supply chain constraints, analysts believe AMD still has significant growth potential, particularly driven by new product launches and expanding data center demand.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy AMD?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on AMD

Wall Street analysts forecast AMD stock price to fall

33 Analyst Rating

25 Buy

8 Hold

0 Sell

Strong Buy

Current: 458.790

Low

210.00

Averages

289.13

High

377.00

Current: 458.790

Low

210.00

Averages

289.13

High

377.00

About AMD

Advanced Micro Devices, Inc. is a global semiconductor company. The Company is focused on high-performance computing and artificial intelligence (AI). Its segments include Data Center, Client and Gaming, and Embedded. Data Center segment includes AI accelerators, microprocessors (CPUs) for servers, graphics processing units (GPUs), accelerated processing units (APUs), data processing units (DPUs), Field Programmable Gate Arrays (FPGAs), and Adaptive system-on-Chip (SoC) products for data centers. Client and Gaming segment includes CPUs, APUs, chipsets for desktops and notebooks, discrete GPUs, and semi-custom SoC products and development services. Embedded segment includes embedded CPUs, APUs, FPGAs, system on modules (SOMs), and Adaptive SoC products. It markets and sells its products under the AMD trademark. Its products include AMD EPYC, AMD Ryzen, AMD Ryzen PRO, Virtex UltraScale+, among others.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

AMD's Data Center Business Shows Significant Growth

- Data Center Growth: AMD's data center revenue reached $5.8 billion in Q1, marking a 57% year-over-year increase, indicating strong market demand, with expectations of accelerating growth at over 80% annually, potentially generating tens of billions in revenue.

- New Product Launch: AMD plans to release the MI450 series AI accelerators later this year, which are expected to deliver an unprecedented 36 times performance improvement within the integrated Helios data center architecture, further enhancing its competitive edge in the data center market.

- Customer Contracts: AMD has signed agreements with Meta and OpenAI to deploy 6 gigawatts of computing capacity over the next few years, reflecting the company's growing appeal among large clients and strengthening demand.

- Profitability Improvement: AMD's non-GAAP earnings per share reached $1.37 in Q1, a 43% year-over-year increase, and despite a P/E ratio of 92, nearly double that of Nvidia, there is still potential for upside in the next 18 months, attracting long-term investor interest.

See More

AI Drives Semiconductor Industry Growth

- Surging Market Demand: McKinsey predicts that by 2030, AI inference will account for over 50% of computing power in data centers, reflecting the urgent demand from enterprises and consumers for AI integration, thereby driving sustained growth in the semiconductor industry.

- Arm's Market Potential: Arm Holdings anticipates over $2 billion in customer demand for its AGI CPU in fiscal years 2027 and 2028, indicating strong competitiveness in the AI inference market and the potential to generate $15 billion in annual revenue over the next five years.

- Technological Innovation and Partnerships: Arm's collaboration with Meta Platforms on the AGI CPU promises to save up to $10 billion in data center capital expenditures while delivering double the computing performance of AMD and Intel's x86 processors, further solidifying its market position.

- Optimistic Financial Outlook: Arm's revenue increased by 23% to $4.92 billion in fiscal 2026, with expectations of reaching $25 billion by fiscal 2031, indicating robust growth potential, and projected earnings per share rising to $9.00, suggesting a 51% upside in stock price.

See More

GameStop's $56B eBay Bid Rejected as Unviable

- Acquisition Proposal Rejected: eBay has officially rejected GameStop's unsolicited $56 billion acquisition bid, labeling it as 'neither credible nor attractive,' with concerns over a significant funding gap and high debt load, which could undermine GameStop's market confidence.

- Financing Challenges Emerge: Despite CEO Ryan Cohen's commitment to provide $20 billion in financing, analysts warn that GameStop's $10 billion market cap makes acquiring a $48 billion giant nearly impossible without extreme equity dilution, highlighting the fragility of its financing capabilities.

- Market Reaction Tepid: Following eBay's rejection, GameStop's stock fell 2.37% in pre-market trading, indicating investor concerns about its acquisition ability, which may impact its future stock performance and market positioning.

- Unclear Strategic Direction: eBay's board reiterated its focus on luxury goods and trading cards, believing this will yield superior shareholder returns, while GameStop's acquisition intentions could distract from its core resources and strategic focus.

See More

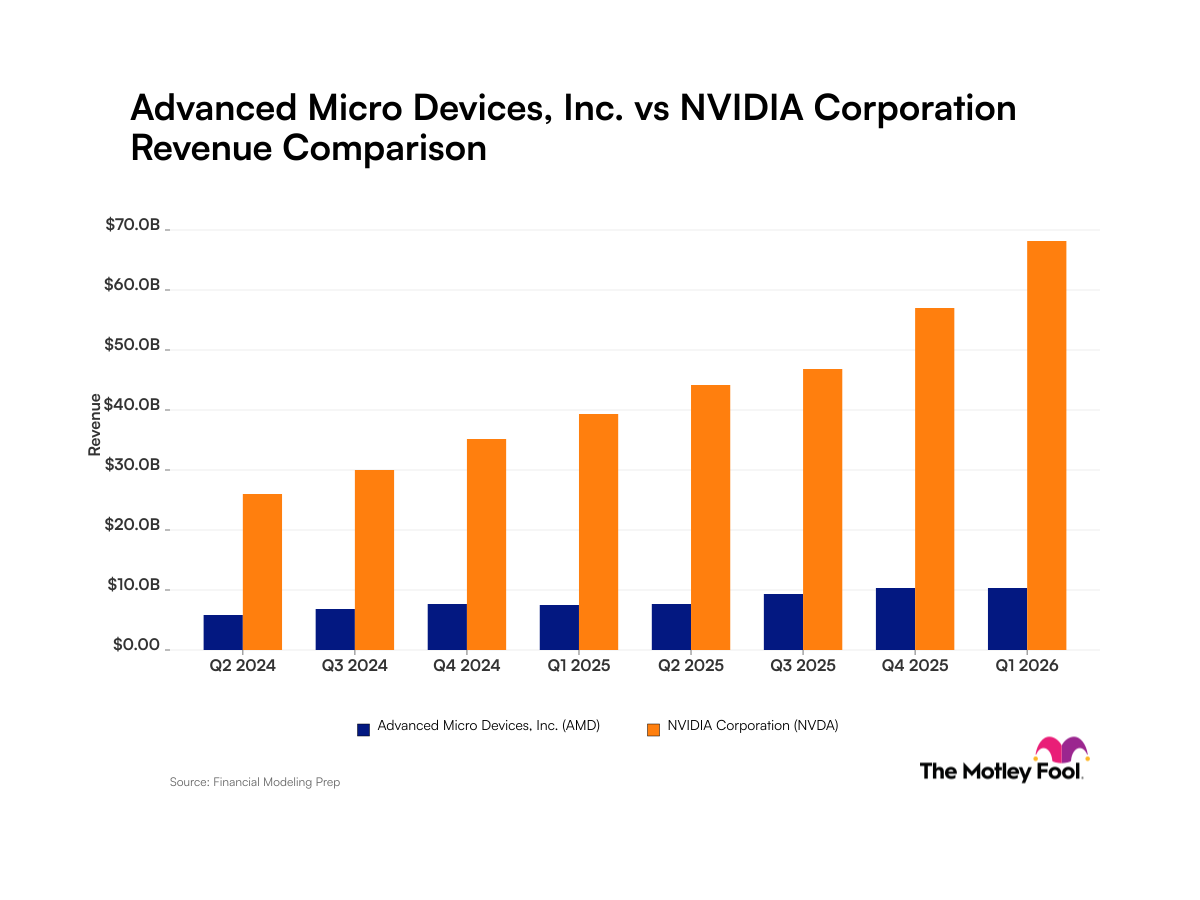

Analysis of Revenue Growth for AMD and Nvidia

- AMD Revenue Growth: AMD reported a revenue of $10.3 billion in Q1 2026 with a net income margin of approximately 13%, indicating stable growth in consumer and enterprise computing markets, although it still lags behind Nvidia.

- Nvidia Market Dominance: Nvidia achieved a revenue of $68.1 billion in Q1 2026 with a net income margin of around 63%, and its consistent quarter-over-quarter growth underscores its leadership position in the AI sector, surpassing AMD's market performance.

- Surge in AI Demand: The rise of artificial intelligence has led to a skyrocketing demand for high-performance computing components from both AMD and Nvidia, particularly as Nvidia leverages its CUDA software and the Vera Rubin platform to further solidify its market advantage, putting AMD under greater competitive pressure.

- Quarterly Revenue Comparison: In Q2 2024, AMD's revenue was $5.8 billion compared to Nvidia's $26.0 billion, highlighting the significant revenue disparity between the two companies and reflecting Nvidia's robust performance and market share in the semiconductor industry.

See More

Market Outlook: Inflation Pressures and Tech Stock Dynamics

- Inflation Data Surprises: April's Consumer Price Index (CPI) rose 3.8% year-over-year, exceeding the 3.7% expectation, while core CPI also slightly surpassed forecasts at 2.8%, putting pressure on Fed rate cut hopes and potentially affecting market sentiment.

- Nvidia's Earnings Outlook Positive: Despite Nvidia's stock hitting a record high with a 16% gain over the past month, analysts maintain a bullish stance, believing the stock, trading at under 20 times 2028 earnings estimates, is worth buying, with price targets raised from $265 to $315.

- AMD and Super Micro Price Target Increases: Mizuho raised AMD's price target from $414 to $515, citing agentic AI driving server demand, while Super Micro's target was increased to $36 due to strong AI server demand, although concerns linger about the company's ties to China.

- Qnity Electronics Strong Performance: Qnity Electronics reported better-than-expected earnings with a 17% organic sales growth driven by the AI boom, leading to a more than 3% stock increase, indicating strong market demand and future growth potential.

See More

Tech Futures Decline as Oil Prices Exceed $100

- Oil Price Surge: Oil prices have surpassed the $100 mark, intensifying concerns over rising inflation, which has led to a widespread decline in tech futures and shaken investor confidence.

- South Korea News Impact: News from South Korea has triggered losses in Q1 stocks, exacerbating worries about the economic outlook in the region and increasing risk-averse sentiment among investors.

- CPI Inflation Rise: The Consumer Price Index (CPI) inflation has picked up, indicating heightened price pressures during the economic recovery, which may prompt the Federal Reserve to adopt a more hawkish monetary policy stance.

- Market Reaction: The decline in tech futures reflects investor uncertainty regarding future economic growth, particularly under the dual pressures of rising oil prices and inflation, which could lead to increased market volatility.

See More

AMD's Data Center Business Shows Significant Growth

- Data Center Growth: AMD's data center revenue reached $5.8 billion in Q1, marking a 57% year-over-year increase, indicating strong market demand, with expectations of accelerating growth at over 80% annually, potentially generating tens of billions in revenue.

- New Product Launch: AMD plans to release the MI450 series AI accelerators later this year, which are expected to deliver an unprecedented 36 times performance improvement within the integrated Helios data center architecture, further enhancing its competitive edge in the data center market.

- Customer Contracts: AMD has signed agreements with Meta and OpenAI to deploy 6 gigawatts of computing capacity over the next few years, reflecting the company's growing appeal among large clients and strengthening demand.

- Profitability Improvement: AMD's non-GAAP earnings per share reached $1.37 in Q1, a 43% year-over-year increase, and despite a P/E ratio of 92, nearly double that of Nvidia, there is still potential for upside in the next 18 months, attracting long-term investor interest.

See More

AI Drives Semiconductor Industry Growth

- Surging Market Demand: McKinsey predicts that by 2030, AI inference will account for over 50% of computing power in data centers, reflecting the urgent demand from enterprises and consumers for AI integration, thereby driving sustained growth in the semiconductor industry.

- Arm's Market Potential: Arm Holdings anticipates over $2 billion in customer demand for its AGI CPU in fiscal years 2027 and 2028, indicating strong competitiveness in the AI inference market and the potential to generate $15 billion in annual revenue over the next five years.

- Technological Innovation and Partnerships: Arm's collaboration with Meta Platforms on the AGI CPU promises to save up to $10 billion in data center capital expenditures while delivering double the computing performance of AMD and Intel's x86 processors, further solidifying its market position.

- Optimistic Financial Outlook: Arm's revenue increased by 23% to $4.92 billion in fiscal 2026, with expectations of reaching $25 billion by fiscal 2031, indicating robust growth potential, and projected earnings per share rising to $9.00, suggesting a 51% upside in stock price.

See More

GameStop's $56B eBay Bid Rejected as Unviable

- Acquisition Proposal Rejected: eBay has officially rejected GameStop's unsolicited $56 billion acquisition bid, labeling it as 'neither credible nor attractive,' with concerns over a significant funding gap and high debt load, which could undermine GameStop's market confidence.

- Financing Challenges Emerge: Despite CEO Ryan Cohen's commitment to provide $20 billion in financing, analysts warn that GameStop's $10 billion market cap makes acquiring a $48 billion giant nearly impossible without extreme equity dilution, highlighting the fragility of its financing capabilities.

- Market Reaction Tepid: Following eBay's rejection, GameStop's stock fell 2.37% in pre-market trading, indicating investor concerns about its acquisition ability, which may impact its future stock performance and market positioning.

- Unclear Strategic Direction: eBay's board reiterated its focus on luxury goods and trading cards, believing this will yield superior shareholder returns, while GameStop's acquisition intentions could distract from its core resources and strategic focus.

See More

Analysis of Revenue Growth for AMD and Nvidia

- AMD Revenue Growth: AMD reported a revenue of $10.3 billion in Q1 2026 with a net income margin of approximately 13%, indicating stable growth in consumer and enterprise computing markets, although it still lags behind Nvidia.

- Nvidia Market Dominance: Nvidia achieved a revenue of $68.1 billion in Q1 2026 with a net income margin of around 63%, and its consistent quarter-over-quarter growth underscores its leadership position in the AI sector, surpassing AMD's market performance.

- Surge in AI Demand: The rise of artificial intelligence has led to a skyrocketing demand for high-performance computing components from both AMD and Nvidia, particularly as Nvidia leverages its CUDA software and the Vera Rubin platform to further solidify its market advantage, putting AMD under greater competitive pressure.

- Quarterly Revenue Comparison: In Q2 2024, AMD's revenue was $5.8 billion compared to Nvidia's $26.0 billion, highlighting the significant revenue disparity between the two companies and reflecting Nvidia's robust performance and market share in the semiconductor industry.

See More

Market Outlook: Inflation Pressures and Tech Stock Dynamics

- Inflation Data Surprises: April's Consumer Price Index (CPI) rose 3.8% year-over-year, exceeding the 3.7% expectation, while core CPI also slightly surpassed forecasts at 2.8%, putting pressure on Fed rate cut hopes and potentially affecting market sentiment.

- Nvidia's Earnings Outlook Positive: Despite Nvidia's stock hitting a record high with a 16% gain over the past month, analysts maintain a bullish stance, believing the stock, trading at under 20 times 2028 earnings estimates, is worth buying, with price targets raised from $265 to $315.

- AMD and Super Micro Price Target Increases: Mizuho raised AMD's price target from $414 to $515, citing agentic AI driving server demand, while Super Micro's target was increased to $36 due to strong AI server demand, although concerns linger about the company's ties to China.

- Qnity Electronics Strong Performance: Qnity Electronics reported better-than-expected earnings with a 17% organic sales growth driven by the AI boom, leading to a more than 3% stock increase, indicating strong market demand and future growth potential.

See More

Tech Futures Decline as Oil Prices Exceed $100

- Oil Price Surge: Oil prices have surpassed the $100 mark, intensifying concerns over rising inflation, which has led to a widespread decline in tech futures and shaken investor confidence.

- South Korea News Impact: News from South Korea has triggered losses in Q1 stocks, exacerbating worries about the economic outlook in the region and increasing risk-averse sentiment among investors.

- CPI Inflation Rise: The Consumer Price Index (CPI) inflation has picked up, indicating heightened price pressures during the economic recovery, which may prompt the Federal Reserve to adopt a more hawkish monetary policy stance.

- Market Reaction: The decline in tech futures reflects investor uncertainty regarding future economic growth, particularly under the dual pressures of rising oil prices and inflation, which could lead to increased market volatility.

See More