Adient (ADNT) Q1 2026 Earnings Call Transcript

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Feb 04 2026

0mins

Should l Buy ADNT?

Source: NASDAQ.COM

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy ADNT?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on ADNT

Wall Street analysts forecast ADNT stock price to rise

8 Analyst Rating

2 Buy

5 Hold

1 Sell

Hold

Current: 20.500

Low

20.00

Averages

23.06

High

28.00

Current: 20.500

Low

20.00

Averages

23.06

High

28.00

About ADNT

Adient PLC is an automotive seating supplier company. The Company’s automotive seating solutions include complete seating systems, frames, mechanisms, foam, head restraints, armrests and trim covers. The Company designs, manufactures and markets a full range of seating systems and components for passenger cars, commercial vehicles and light trucks, including vans, pick-up trucks and sport/crossover utility vehicles. The Company manages its business on a geographic basis and operates in three reportable segments: Americas, which is inclusive of North America and South America; Europe, Middle East, and Africa (EMEA), and Asia Pacific/China (Asia). The Company operates approximately 200 wholly- and majority-owned manufacturing or assembly facilities, with operations in approximately 29 countries. The Company provides production and service parts to its customers under multi-year programs.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

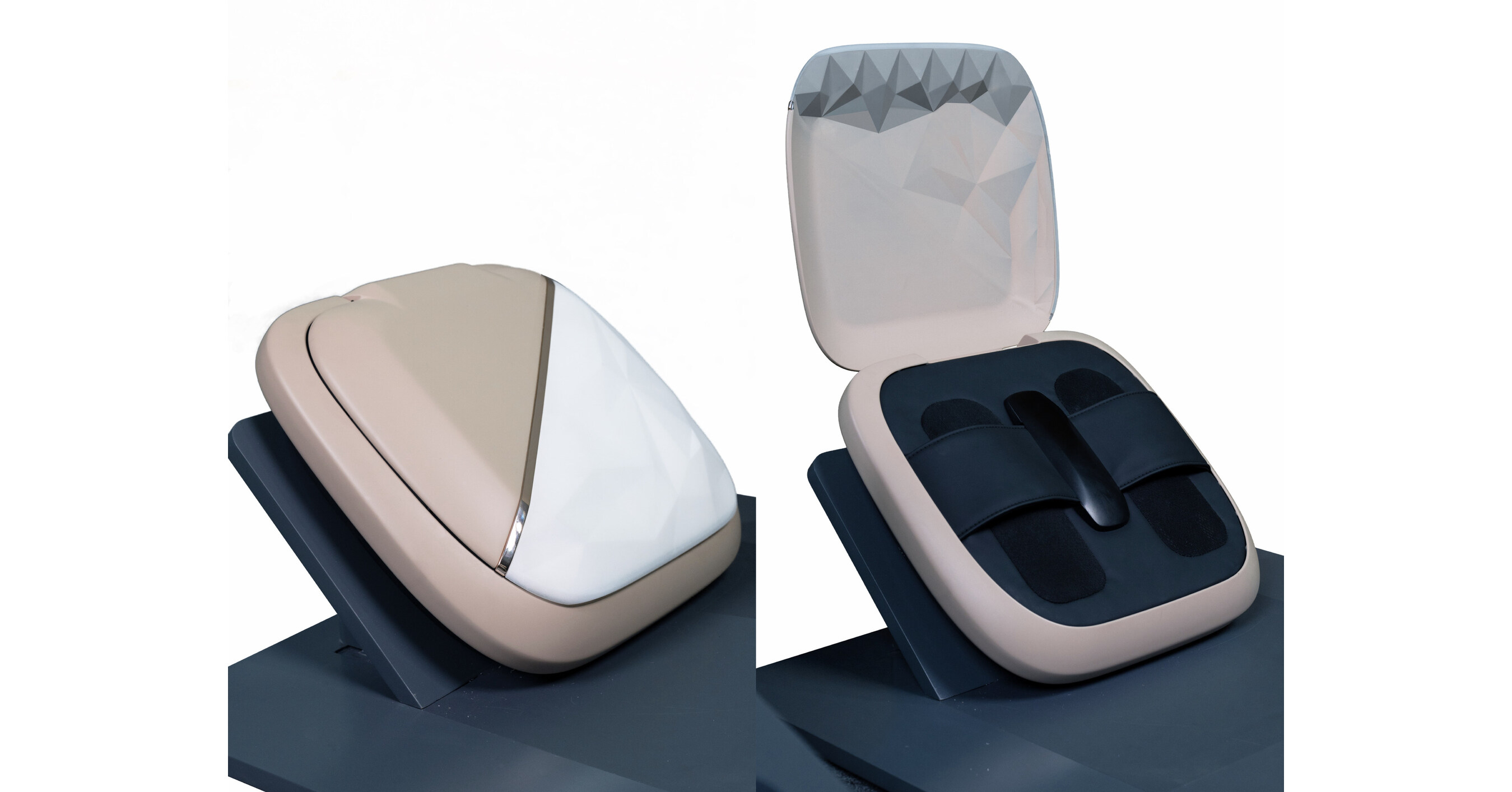

Adient Launches StepJoy Foot Massage System for Vehicles

- Innovative Massage Experience: Adient's StepJoy foot massage system, first introduced in the NIO ES9 model, delivers an automotive-grade deep foot relaxation experience, addressing rising consumer expectations for in-vehicle comfort.

- Space-Saving Design: The compact design of StepJoy integrates seamlessly into the seating layout, stowing away in the seatback when not in use and functioning as a footrest when deployed, enhancing space utilization within the vehicle.

- Durability and Technology Validation: Incorporating Adient's Magic Trim seat cover assembly, the system ensures long-term durability and a premium feel while meeting automotive durability standards, significantly enhancing user comfort.

- Market Differentiation: By expanding its seating comfort portfolio, Adient enables automakers to differentiate their cabin experience, providing passengers with a more relaxing journey and enhancing competitive positioning in the market.

See More

Adient to Host Q2 2026 Earnings Call on May 6

- Earnings Call Scheduled: Adient will host its Q2 2026 earnings call on May 6, 2026, at 8:30 a.m. ET, aiming to provide detailed insights into its financial performance, thereby enhancing transparency and boosting investor confidence.

- Live Webcast Link: A link to the live webcast and presentation materials will be available on Adient's Investor Relations website, ensuring that all investors can access real-time information, which enhances interaction between the company and its investors.

- Telephone Participation: Investors can join the call by dialing 888-566-1827 (U.S.) or 773-799-3976 (international) 15 minutes prior to the start time, ensuring they receive the latest updates from the company and fostering a sense of engagement among investors.

- Company Background: Adient, a global leader in automotive seating, employs over 65,000 people across approximately 200 manufacturing/assembly plants, dedicated to providing comprehensive seating systems and components for major OEMs, showcasing its expertise throughout the automotive seat-making process.

See More

Adient Unveils Innovative Sculpted Soft Trim for Automotive Seating

- Material Innovation: Adient has launched Sculpted Soft Trim, a new soft trim solution that reduces sewing requirements through automation, significantly enhancing the aesthetics and flexibility of seat designs, which is expected to redefine standards in the automotive seating market.

- Efficiency Gains: The forming cycle for this material is reduced to 50% of traditional methods, not only increasing production speed but also ensuring consistent high-end craftsmanship, helping OEMs maintain a competitive edge in a challenging market.

- Increased Design Freedom: Sculpted Soft Trim can replace up to 12 traditional sewing patterns, simplifying complex seat designs, particularly in challenging areas like child seat anchor points, thereby elevating craftsmanship and design possibilities.

- Global Market Deployment: The material is now available globally and will be in production in multiple OEM vehicles, marking Adient's ongoing innovation and market expansion in the automotive seating sector.

See More

Adient Unveils Innovative Sculpted Soft Trim for Automotive Seating

- Material Innovation: Adient's Sculpted Soft Trim is a soft, breathable trim solution that allows for the creation of larger or more intricate trim panels, significantly enhancing the aesthetic and design freedom of automotive seating.

- Efficiency Gains: The material utilizes an automated process that reduces the sewing required compared to traditional trim covers, cutting production cycle times to roughly 50% of conventional methods, thereby improving manufacturing efficiency and product quality.

- Complexity Reduction: Sculpted Soft Trim can replace up to twelve individual patterns traditionally needed for components like child seat anchor locations, simplifying production and enhancing craftsmanship while reducing labor costs.

- Global Market Deployment: This innovative material is now available globally and will be in production on seats for multiple OEM vehicles this year, reinforcing Adient's leadership position in the automotive seating market.

See More

Latest Wall Street Rating Updates

- Goldman Sachs Reiterates Nvidia: Goldman Sachs maintains a Buy rating on Nvidia ahead of its earnings report, expecting investors to focus on visibility into 2027, non-traditional customer demand, and trends in the Chinese market, indicating strong market confidence in Nvidia's future growth.

- Benchmark Initiates Cava Rating: Benchmark initiates coverage of CAVA Group with a Buy rating and an $80 price target, reflecting its leadership position in the rapidly emerging Mediterranean dining market, which is expected to attract more investor interest in this burgeoning sector.

- BMO Capital Upgrades Brookfield: BMO upgrades Brookfield Asset Management from Market Perform to Outperform, citing attractive mid-teens distributable earnings growth prospects underpinned by continued fundraising momentum and fee rate resilience, showcasing the company's robust financial health.

- Bank of America Downgrades Qualcomm: Bank of America downgrades Qualcomm from Buy to Neutral, lowering the price target from $215 to $155 due to concerns over cyclical and structural weaknesses in the handset market, which may adversely affect its future performance.

See More

Adient plc Reports Q1 2026 Earnings with Raised Guidance and Strong Cash Flow

- Revenue Growth: Adient plc reported $3.6 billion in revenue for Q1 2026, marking a 4% year-over-year increase primarily driven by favorable FX impacts from Europe and significant growth in China, effectively offsetting production challenges in North America and demonstrating the company's resilience in global markets.

- Adjusted EBITDA Performance: The adjusted EBITDA for the first quarter stood at $207 million, reflecting a 6% increase compared to the same period last year, with an EBITDA margin of 5.7%, indicating ongoing improvements in cost control and operational efficiency, which bolster confidence in future profitability.

- Shareholder Returns and Liquidity: The company repurchased $25 million in shares during the quarter, ending with a cash balance of $855 million and total liquidity of $1.7 billion, showcasing strong financial health and commitment to shareholders, which is expected to support future investments and growth.

- Outlook Enhancement: Adient raised its full-year 2026 sales guidance to approximately $14.6 billion, with adjusted EBITDA expectations of around $880 million and free cash flow of $125 million, reflecting the company's confidence in future growth, particularly through investments in automation and onshoring opportunities that will drive business performance.

See More

Adient Launches StepJoy Foot Massage System for Vehicles

- Innovative Massage Experience: Adient's StepJoy foot massage system, first introduced in the NIO ES9 model, delivers an automotive-grade deep foot relaxation experience, addressing rising consumer expectations for in-vehicle comfort.

- Space-Saving Design: The compact design of StepJoy integrates seamlessly into the seating layout, stowing away in the seatback when not in use and functioning as a footrest when deployed, enhancing space utilization within the vehicle.

- Durability and Technology Validation: Incorporating Adient's Magic Trim seat cover assembly, the system ensures long-term durability and a premium feel while meeting automotive durability standards, significantly enhancing user comfort.

- Market Differentiation: By expanding its seating comfort portfolio, Adient enables automakers to differentiate their cabin experience, providing passengers with a more relaxing journey and enhancing competitive positioning in the market.

See More

Adient to Host Q2 2026 Earnings Call on May 6

- Earnings Call Scheduled: Adient will host its Q2 2026 earnings call on May 6, 2026, at 8:30 a.m. ET, aiming to provide detailed insights into its financial performance, thereby enhancing transparency and boosting investor confidence.

- Live Webcast Link: A link to the live webcast and presentation materials will be available on Adient's Investor Relations website, ensuring that all investors can access real-time information, which enhances interaction between the company and its investors.

- Telephone Participation: Investors can join the call by dialing 888-566-1827 (U.S.) or 773-799-3976 (international) 15 minutes prior to the start time, ensuring they receive the latest updates from the company and fostering a sense of engagement among investors.

- Company Background: Adient, a global leader in automotive seating, employs over 65,000 people across approximately 200 manufacturing/assembly plants, dedicated to providing comprehensive seating systems and components for major OEMs, showcasing its expertise throughout the automotive seat-making process.

See More

Adient Unveils Innovative Sculpted Soft Trim for Automotive Seating

- Material Innovation: Adient has launched Sculpted Soft Trim, a new soft trim solution that reduces sewing requirements through automation, significantly enhancing the aesthetics and flexibility of seat designs, which is expected to redefine standards in the automotive seating market.

- Efficiency Gains: The forming cycle for this material is reduced to 50% of traditional methods, not only increasing production speed but also ensuring consistent high-end craftsmanship, helping OEMs maintain a competitive edge in a challenging market.

- Increased Design Freedom: Sculpted Soft Trim can replace up to 12 traditional sewing patterns, simplifying complex seat designs, particularly in challenging areas like child seat anchor points, thereby elevating craftsmanship and design possibilities.

- Global Market Deployment: The material is now available globally and will be in production in multiple OEM vehicles, marking Adient's ongoing innovation and market expansion in the automotive seating sector.

See More

Adient Unveils Innovative Sculpted Soft Trim for Automotive Seating

- Material Innovation: Adient's Sculpted Soft Trim is a soft, breathable trim solution that allows for the creation of larger or more intricate trim panels, significantly enhancing the aesthetic and design freedom of automotive seating.

- Efficiency Gains: The material utilizes an automated process that reduces the sewing required compared to traditional trim covers, cutting production cycle times to roughly 50% of conventional methods, thereby improving manufacturing efficiency and product quality.

- Complexity Reduction: Sculpted Soft Trim can replace up to twelve individual patterns traditionally needed for components like child seat anchor locations, simplifying production and enhancing craftsmanship while reducing labor costs.

- Global Market Deployment: This innovative material is now available globally and will be in production on seats for multiple OEM vehicles this year, reinforcing Adient's leadership position in the automotive seating market.

See More

Latest Wall Street Rating Updates

- Goldman Sachs Reiterates Nvidia: Goldman Sachs maintains a Buy rating on Nvidia ahead of its earnings report, expecting investors to focus on visibility into 2027, non-traditional customer demand, and trends in the Chinese market, indicating strong market confidence in Nvidia's future growth.

- Benchmark Initiates Cava Rating: Benchmark initiates coverage of CAVA Group with a Buy rating and an $80 price target, reflecting its leadership position in the rapidly emerging Mediterranean dining market, which is expected to attract more investor interest in this burgeoning sector.

- BMO Capital Upgrades Brookfield: BMO upgrades Brookfield Asset Management from Market Perform to Outperform, citing attractive mid-teens distributable earnings growth prospects underpinned by continued fundraising momentum and fee rate resilience, showcasing the company's robust financial health.

- Bank of America Downgrades Qualcomm: Bank of America downgrades Qualcomm from Buy to Neutral, lowering the price target from $215 to $155 due to concerns over cyclical and structural weaknesses in the handset market, which may adversely affect its future performance.

See More

Adient plc Reports Q1 2026 Earnings with Raised Guidance and Strong Cash Flow

- Revenue Growth: Adient plc reported $3.6 billion in revenue for Q1 2026, marking a 4% year-over-year increase primarily driven by favorable FX impacts from Europe and significant growth in China, effectively offsetting production challenges in North America and demonstrating the company's resilience in global markets.

- Adjusted EBITDA Performance: The adjusted EBITDA for the first quarter stood at $207 million, reflecting a 6% increase compared to the same period last year, with an EBITDA margin of 5.7%, indicating ongoing improvements in cost control and operational efficiency, which bolster confidence in future profitability.

- Shareholder Returns and Liquidity: The company repurchased $25 million in shares during the quarter, ending with a cash balance of $855 million and total liquidity of $1.7 billion, showcasing strong financial health and commitment to shareholders, which is expected to support future investments and growth.

- Outlook Enhancement: Adient raised its full-year 2026 sales guidance to approximately $14.6 billion, with adjusted EBITDA expectations of around $880 million and free cash flow of $125 million, reflecting the company's confidence in future growth, particularly through investments in automation and onshoring opportunities that will drive business performance.

See More