Putting It All Together: SPUS May Have a Value of $52

ETF Analysis: The SP Funds S&P 500 Sharia Industry Exclusions ETF (SPUS) has an implied analyst target price of $51.68, indicating an 11.66% upside from its current trading price of $46.28.

Notable Holdings: Key underlying holdings with significant upside potential include Nordson Corp. (14.72% upside), Equifax Inc (13.46% upside), and First Solar Inc (12.48% upside) based on their respective average analyst target prices.

Market Sentiment: Analysts' target prices may reflect optimism about future performance but could also lead to downgrades if they are based on outdated information or fail to account for recent developments in the companies or industries.

Investor Considerations: Investors are encouraged to conduct further research to determine whether analysts' targets are justified or overly optimistic regarding the future stock performance of these companies.

Trade with 70% Backtested Accuracy

Analyst Views on EFX

About EFX

About the author

Ontario to Launch Credit Lock Service for Identity Theft Prevention

- Launch of Credit Lock Service: Starting July 1, 2026, residents of Ontario will be able to place a digital lock on their Equifax Canada credit report to prevent identity theft, marking a significant advancement in consumer protection by the provincial government.

- Legal Protection Mechanism: Once consumers activate the Credit Lock, Equifax Canada is legally prohibited from providing their credit scores and personal information to lenders, effectively preventing potential identity theft and fraud, thereby enhancing consumer financial security.

- Free Service Advantage: The Credit Lock service is completely free and does not impact consumers' credit score calculations, allowing them to set, remove, or suspend the lock immediately through the myEquifax platform, phone, or mail, thus improving service accessibility and convenience.

- National Anti-Fraud Commitment: The introduction of Credit Lock is part of Equifax Canada's broader commitment to combat fraud nationwide, combined with credit monitoring and educational resources, aimed at helping consumers better protect themselves against fraud and identity theft.

Significant Decline in Canadian Entrepreneurship

- Decline in Entrepreneurship: In Q1 2026, Canadian entrepreneurship saw a sharp decline, with the number of active young businesses dropping by 38.7%, indicating that high operating costs and persistent inflation are negatively impacting new enterprise creation.

- Reduced Credit Usage: Businesses cut back on short-term credit, with total line of credit balances falling 21.3% year-over-year to $1.55 billion, suggesting a more cautious approach to cash flow management that could affect future growth potential.

- Rising Delinquencies: The 60+ day delinquency rate for financial trades rose to 3.83% in Q1 2026, indicating increased pressure on businesses to meet obligations to banks and credit cards, which may lead to future credit losses.

- Provincial Disparities: Ontario recorded the highest financial trade delinquency rate at 4.22%, up 13.93% year-over-year, while Quebec showed a different pressure pattern, highlighting the varying economic pressures across provinces.

GB Group Reports 3.2% Revenue Growth and Launches New Platform

- Revenue Growth: GB Group reported revenue of £285 million, reflecting a 3.2% increase that aligns with expectations, indicating a successful recovery in the Americas and effective strategic partnerships.

- Strategic Partnership: The partnership with Equifax enhances the company's competitive advantage in the identity verification market, expected to improve fraud detection capabilities by integrating Equifax's proprietary data, thereby expanding market reach.

- New Platform Launch: The AI-powered GBG Go identity platform has exceeded expectations with strong demand, securing over 100 customer wins, demonstrating the company's success in technological innovation and market acceptance.

- Capital Return: The company returned £56 million to shareholders in FY26, showcasing strong capital allocation discipline despite challenges such as declining profit margins and goodwill impairment charges.

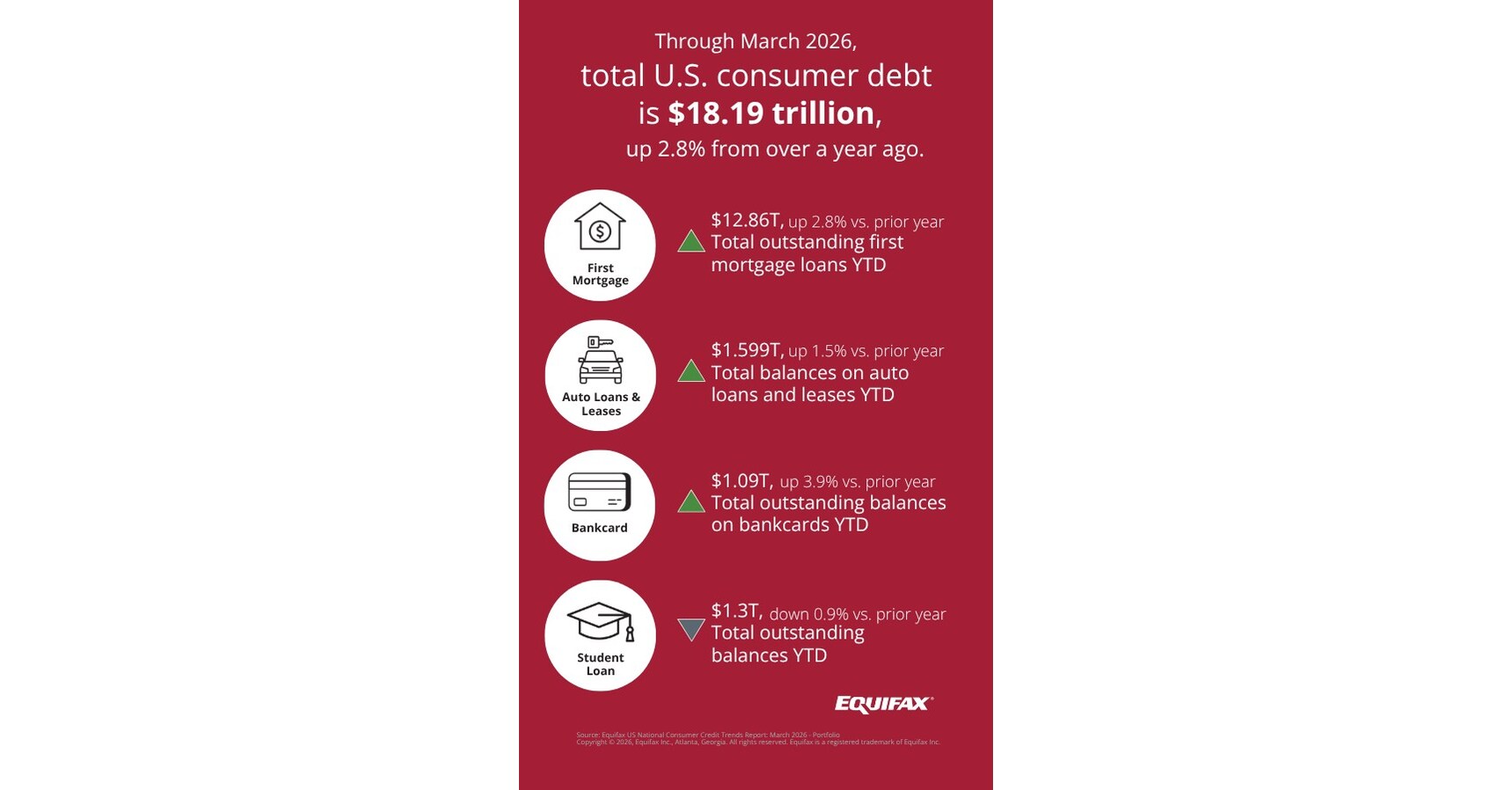

Subprime Borrower Activity Fuels Bankcard Growth

- Record Consumer Debt: As of March 2026, U.S. consumer debt balances reached an all-time high of $18.19 trillion, primarily driven by subprime borrowers opening new bankcards and carrying higher balances, indicating a deepening reliance on credit among lower-income groups in the economy.

- Growth in Bankcard Accounts: New bankcard accounts grew by 8.1% year-over-year as of January 2026, with subprime originations specifically increasing by 18.6%, suggesting that financial institutions are expanding credit support for the subprime market to address rising living costs.

- Rising Student Loan Delinquencies: Although the number of new student loan accounts declined by over 10% in January 2026, the delinquency rate reached 17.01% in March, reflecting the impact of rising education costs on borrowers' repayment capabilities and potentially disrupting traditional payment hierarchies.

- Improving Delinquency Rates but Rising Write-Offs: Most consumer credit indicators showed improvements in 60+ day delinquency rates, yet rising write-off rates in bankcard and auto loans indicate that financial institutions are adjusting risk levels to meet the challenges of the 2026 fiscal year.

Canada's Q1 2026 Credit Trends Report Highlights Rising Insolvencies

- Consumer Debt Growth: As of Q1 2026, total consumer debt in Canada reached CAD 2.66 trillion, a 3.8% year-over-year increase, although non-mortgage debt fell by over CAD 487 million in the first quarter, indicating a post-holiday financial restraint among consumers.

- Rising Bankruptcy Rates: In Q1 2026, insolvency volumes hit their highest level since 2009, increasing by 18.8% year-over-year, suggesting that many consumers may have reached a financial inflection point amid escalating economic pressures.

- Decline in Credit Demand: Following reduced spending at the end of 2025, new credit card originations fell to a four-year low in Q1 2026, with average credit limits for higher-risk consumers reduced by 15% to 20%, reflecting tightening credit market conditions.

- Automotive Loan Slowdown: Despite lower vehicle prices, new captive auto loans fell nearly 5% year-over-year in Q1 2026, while bank installment loan volumes dropped by 9.5%, indicating that consumers are becoming more cautious before committing to new vehicle purchases due to rising insurance and maintenance costs.

Equifax Expands Partnership with GBG in the U.S.

- Partnership Expansion: Equifax and GBG announced an expansion of their partnership in the U.S., integrating Equifax's identity and fraud solutions into GBG's adaptive identity platform, GBG Go, to tackle increasingly sophisticated fraud threats.

- Enhanced Real-Time Verification: The integration will enable customers to improve real-time identity verification, detect synthetic identity fraud, and combat credit ghosting, thereby enhancing customer trust and security.

- Future Plans: Equifax plans to integrate GBG's data verification capabilities into the U.S. market later this year, with broader global implementation scheduled for 2027, indicating a long-term strategy for global market penetration.

- Market Impact: According to the Deloitte Center for Financial Services, synthetic identity fraud is projected to cause at least $23 billion in losses by 2030, underscoring the significance of this partnership in mitigating financial losses.

Ontario to Launch Credit Lock Service for Identity Theft Prevention

- Launch of Credit Lock Service: Starting July 1, 2026, residents of Ontario will be able to place a digital lock on their Equifax Canada credit report to prevent identity theft, marking a significant advancement in consumer protection by the provincial government.

- Legal Protection Mechanism: Once consumers activate the Credit Lock, Equifax Canada is legally prohibited from providing their credit scores and personal information to lenders, effectively preventing potential identity theft and fraud, thereby enhancing consumer financial security.

- Free Service Advantage: The Credit Lock service is completely free and does not impact consumers' credit score calculations, allowing them to set, remove, or suspend the lock immediately through the myEquifax platform, phone, or mail, thus improving service accessibility and convenience.

- National Anti-Fraud Commitment: The introduction of Credit Lock is part of Equifax Canada's broader commitment to combat fraud nationwide, combined with credit monitoring and educational resources, aimed at helping consumers better protect themselves against fraud and identity theft.

Significant Decline in Canadian Entrepreneurship

- Decline in Entrepreneurship: In Q1 2026, Canadian entrepreneurship saw a sharp decline, with the number of active young businesses dropping by 38.7%, indicating that high operating costs and persistent inflation are negatively impacting new enterprise creation.

- Reduced Credit Usage: Businesses cut back on short-term credit, with total line of credit balances falling 21.3% year-over-year to $1.55 billion, suggesting a more cautious approach to cash flow management that could affect future growth potential.

- Rising Delinquencies: The 60+ day delinquency rate for financial trades rose to 3.83% in Q1 2026, indicating increased pressure on businesses to meet obligations to banks and credit cards, which may lead to future credit losses.

- Provincial Disparities: Ontario recorded the highest financial trade delinquency rate at 4.22%, up 13.93% year-over-year, while Quebec showed a different pressure pattern, highlighting the varying economic pressures across provinces.

GB Group Reports 3.2% Revenue Growth and Launches New Platform

- Revenue Growth: GB Group reported revenue of £285 million, reflecting a 3.2% increase that aligns with expectations, indicating a successful recovery in the Americas and effective strategic partnerships.

- Strategic Partnership: The partnership with Equifax enhances the company's competitive advantage in the identity verification market, expected to improve fraud detection capabilities by integrating Equifax's proprietary data, thereby expanding market reach.

- New Platform Launch: The AI-powered GBG Go identity platform has exceeded expectations with strong demand, securing over 100 customer wins, demonstrating the company's success in technological innovation and market acceptance.

- Capital Return: The company returned £56 million to shareholders in FY26, showcasing strong capital allocation discipline despite challenges such as declining profit margins and goodwill impairment charges.

Subprime Borrower Activity Fuels Bankcard Growth

- Record Consumer Debt: As of March 2026, U.S. consumer debt balances reached an all-time high of $18.19 trillion, primarily driven by subprime borrowers opening new bankcards and carrying higher balances, indicating a deepening reliance on credit among lower-income groups in the economy.

- Growth in Bankcard Accounts: New bankcard accounts grew by 8.1% year-over-year as of January 2026, with subprime originations specifically increasing by 18.6%, suggesting that financial institutions are expanding credit support for the subprime market to address rising living costs.

- Rising Student Loan Delinquencies: Although the number of new student loan accounts declined by over 10% in January 2026, the delinquency rate reached 17.01% in March, reflecting the impact of rising education costs on borrowers' repayment capabilities and potentially disrupting traditional payment hierarchies.

- Improving Delinquency Rates but Rising Write-Offs: Most consumer credit indicators showed improvements in 60+ day delinquency rates, yet rising write-off rates in bankcard and auto loans indicate that financial institutions are adjusting risk levels to meet the challenges of the 2026 fiscal year.

Canada's Q1 2026 Credit Trends Report Highlights Rising Insolvencies

- Consumer Debt Growth: As of Q1 2026, total consumer debt in Canada reached CAD 2.66 trillion, a 3.8% year-over-year increase, although non-mortgage debt fell by over CAD 487 million in the first quarter, indicating a post-holiday financial restraint among consumers.

- Rising Bankruptcy Rates: In Q1 2026, insolvency volumes hit their highest level since 2009, increasing by 18.8% year-over-year, suggesting that many consumers may have reached a financial inflection point amid escalating economic pressures.

- Decline in Credit Demand: Following reduced spending at the end of 2025, new credit card originations fell to a four-year low in Q1 2026, with average credit limits for higher-risk consumers reduced by 15% to 20%, reflecting tightening credit market conditions.

- Automotive Loan Slowdown: Despite lower vehicle prices, new captive auto loans fell nearly 5% year-over-year in Q1 2026, while bank installment loan volumes dropped by 9.5%, indicating that consumers are becoming more cautious before committing to new vehicle purchases due to rising insurance and maintenance costs.

Equifax Expands Partnership with GBG in the U.S.

- Partnership Expansion: Equifax and GBG announced an expansion of their partnership in the U.S., integrating Equifax's identity and fraud solutions into GBG's adaptive identity platform, GBG Go, to tackle increasingly sophisticated fraud threats.

- Enhanced Real-Time Verification: The integration will enable customers to improve real-time identity verification, detect synthetic identity fraud, and combat credit ghosting, thereby enhancing customer trust and security.

- Future Plans: Equifax plans to integrate GBG's data verification capabilities into the U.S. market later this year, with broader global implementation scheduled for 2027, indicating a long-term strategy for global market penetration.

- Market Impact: According to the Deloitte Center for Financial Services, synthetic identity fraud is projected to cause at least $23 billion in losses by 2030, underscoring the significance of this partnership in mitigating financial losses.