PennyMac Mortgage Investment Trust (PMT): Assessing Valuation Following Impressive Earnings Performance and 22.7% Revenue Increase

Strong Quarterly Performance: PennyMac Mortgage Investment Trust (PMT) reported a 23% year-on-year revenue increase, surpassing Wall Street estimates for earnings and net interest income, which has positively influenced investor sentiment.

Valuation Insights: The current share price of $12.70 is below the fair value estimate of $13.43, raising questions about whether PMT is undervalued or if future growth is already priced in, especially given the challenges of falling revenues and rising profitability.

Operational Efficiency and Risks: PMT's digital transformation and ability to create securitizations are expected to enhance net margins, but ongoing interest rate volatility and reliance on non-agency securitizations pose risks to book value and investor confidence.

Investment Opportunities: The article suggests exploring various stock screening options for undervalued stocks, early-stage growth potential, and AI penny stocks, while emphasizing that the analysis is not financial advice and does not account for individual financial situations.

Trade with 70% Backtested Accuracy

Analyst Views on PMT

About PMT

About the author

PMET Partners with Koch Technology Solutions to Develop Caesium Chemicals

- Strategic Partnership Initiated: PMET has launched a strategic testwork program with Koch Technology Solutions to convert Shaakichiuwaanaan caesium concentrates into high-value caesium chemical products, which is expected to support supply chains for critical industries such as defense, aerospace, and energy in the U.S.

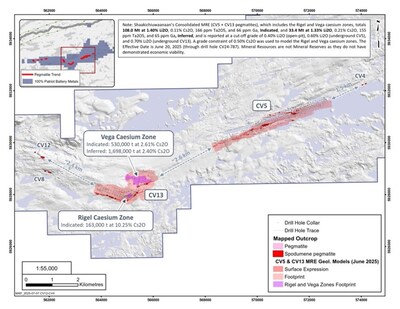

- Significant Resource Potential: The Shaakichiuwaanaan project hosts the world's largest caesium resource, with 0.69 Mt at 4.40% Cs2O and 1.70 Mt at 2.40% Cs2O, establishing a strong foundation for PMET's leadership in the caesium market.

- Innovative Technology Application: Koch Technology Solutions will leverage its proprietary caesium chemical production techniques to drive efficient extraction, with pathways for producing various value-added caesium chemicals expected to be developed over the next four months, enhancing PMET's market competitiveness.

- Broad Market Prospects: Through collaboration with Koch, PMET aims to not only enhance the commercial value of its caesium resources but also explore applications of caesium chemicals in the emerging solar panel industry, further expanding market opportunities.

Analysis of PMT Dividend Predictions and Performance

- Dividend Yield Assessment: PMT's current estimated annualized dividend yield stands at 13.45%, and while dividends are not always predictable, historical data aids in assessing the reasonableness of future yields, thereby influencing investor decisions.

- Price Volatility Range: PMT's 52-week low is $11.145 per share, with a high of $13.81, while the latest trade price is $11.89, indicating that the stock is hovering at a low level, which may affect investor confidence.

- ETF Holding Proportion: PMT constitutes 3.07% of the Invesco KBW High Dividend Yield Financial ETF (KBWD), and although the ETF is trading relatively unchanged on the day, PMT's performance could impact the overall attractiveness of the ETF.

- Preferred Stock Structure: According to Preferred Stock Channel, there are three series of preferred stock senior to PMT, which may affect its dividend payment priority and investors' risk assessments.

Analysis of Pennymac Preferred Shares Dividend History

- Dividend History Overview: The 8.125% Series A Preferred Shares (PMT.PRA) of Pennymac Mortgage Investment Trust demonstrate a stable dividend payment history, reflecting the company's robust capital management.

- Market Performance: In Monday trading, PMT.PRA preferred shares fell about 0.6%, while common shares (PMT) rose approximately 1%, indicating a dynamic market difference between preferred and common stocks.

- Yield Comparison: The preferred shares attract investor attention due to their high yield, potentially influencing asset allocation decisions among investors in the market.

- Investor Perspective: Despite market fluctuations, the author's views emphasize the potential value of preferred shares, suggesting that investors should consider their stable dividend characteristics when selecting preferred stocks.

PennyMac Declares $0.40 Cash Dividend for Q1 2026

- Dividend Declaration: PennyMac Mortgage Investment Trust announced a cash dividend of $0.40 per common share for Q1 2026, reflecting the company's confidence in its future cash flows and financial stability.

- Payment Schedule: The dividend will be paid on April 24, 2026, to shareholders of record as of April 9, 2026, ensuring eligible investors receive timely returns and bolstering investor confidence in the company.

- Company Overview: PennyMac Mortgage Investment Trust is a mortgage REIT primarily investing in residential mortgage loans and related assets, externally managed by PNMAC Capital Management, LLC, a wholly-owned subsidiary of PennyMac Financial Services, Inc., highlighting its expertise in the market.

- Forward-Looking Statements: The announcement includes forward-looking statements regarding potential impacts on financial results and operations due to various factors such as interest rate changes and market conditions, cautioning investors to consider these risks.

PennyMac Mortgage Trust Declares $0.40 Quarterly Dividend

- Quarterly Dividend Declaration: PennyMac Mortgage Investment Trust has declared a quarterly dividend of $0.40 per share, consistent with previous distributions, indicating the company's stable cash flow and commitment to shareholder returns.

- Yield Performance: The forward yield of 13.46% reflects the attractiveness of the investment, particularly in the current interest rate environment, potentially drawing in more investors seeking stable income.

- Shareholder Record Dates: The dividend will be payable on April 24, with a record date of April 9 and an ex-dividend date also on April 9, ensuring shareholders receive their earnings in a timely manner.

- Future Outlook: PennyMac projects 30 securitizations in 2026 as portfolio rotation accelerates, demonstrating the company's proactive strategic positioning in the market, which may further enhance its financial performance.

Dividend Stocks Gain Favor Amid Market Turbulence

- Investor Preference Shift: Amid market turbulence and uncertainty, many investors are turning to dividend-yielding stocks, which typically have high free cash flows and reward shareholders with substantial dividends, indicating a strong desire for stable income.

- Analyst Rating Overview: Benzinga provides the latest analyst ratings on high-yield stocks, allowing investors to review the latest analyses of their favorite stocks by visiting the Analyst Stock Ratings page, thereby enhancing transparency in investment decisions.

- High-Yield Stock Recommendations: In the financial sector, PennyMac Mortgage Investment Trust (NYSE:PMT), Blue Owl Capital Corp (NYSE:OBDC), and Saratoga Investment Corp (NYSE:SAR) are highlighted as three high-yield stocks, reflecting market confidence in these companies.

- Analyst Accuracy: Benzinga's database enables traders to sort ratings by analyst accuracy, which not only improves investors' understanding of market dynamics but may also influence their investment strategies and choices.

PMET Partners with Koch Technology Solutions to Develop Caesium Chemicals

- Strategic Partnership Initiated: PMET has launched a strategic testwork program with Koch Technology Solutions to convert Shaakichiuwaanaan caesium concentrates into high-value caesium chemical products, which is expected to support supply chains for critical industries such as defense, aerospace, and energy in the U.S.

- Significant Resource Potential: The Shaakichiuwaanaan project hosts the world's largest caesium resource, with 0.69 Mt at 4.40% Cs2O and 1.70 Mt at 2.40% Cs2O, establishing a strong foundation for PMET's leadership in the caesium market.

- Innovative Technology Application: Koch Technology Solutions will leverage its proprietary caesium chemical production techniques to drive efficient extraction, with pathways for producing various value-added caesium chemicals expected to be developed over the next four months, enhancing PMET's market competitiveness.

- Broad Market Prospects: Through collaboration with Koch, PMET aims to not only enhance the commercial value of its caesium resources but also explore applications of caesium chemicals in the emerging solar panel industry, further expanding market opportunities.

Analysis of PMT Dividend Predictions and Performance

- Dividend Yield Assessment: PMT's current estimated annualized dividend yield stands at 13.45%, and while dividends are not always predictable, historical data aids in assessing the reasonableness of future yields, thereby influencing investor decisions.

- Price Volatility Range: PMT's 52-week low is $11.145 per share, with a high of $13.81, while the latest trade price is $11.89, indicating that the stock is hovering at a low level, which may affect investor confidence.

- ETF Holding Proportion: PMT constitutes 3.07% of the Invesco KBW High Dividend Yield Financial ETF (KBWD), and although the ETF is trading relatively unchanged on the day, PMT's performance could impact the overall attractiveness of the ETF.

- Preferred Stock Structure: According to Preferred Stock Channel, there are three series of preferred stock senior to PMT, which may affect its dividend payment priority and investors' risk assessments.

Analysis of Pennymac Preferred Shares Dividend History

- Dividend History Overview: The 8.125% Series A Preferred Shares (PMT.PRA) of Pennymac Mortgage Investment Trust demonstrate a stable dividend payment history, reflecting the company's robust capital management.

- Market Performance: In Monday trading, PMT.PRA preferred shares fell about 0.6%, while common shares (PMT) rose approximately 1%, indicating a dynamic market difference between preferred and common stocks.

- Yield Comparison: The preferred shares attract investor attention due to their high yield, potentially influencing asset allocation decisions among investors in the market.

- Investor Perspective: Despite market fluctuations, the author's views emphasize the potential value of preferred shares, suggesting that investors should consider their stable dividend characteristics when selecting preferred stocks.

PennyMac Declares $0.40 Cash Dividend for Q1 2026

- Dividend Declaration: PennyMac Mortgage Investment Trust announced a cash dividend of $0.40 per common share for Q1 2026, reflecting the company's confidence in its future cash flows and financial stability.

- Payment Schedule: The dividend will be paid on April 24, 2026, to shareholders of record as of April 9, 2026, ensuring eligible investors receive timely returns and bolstering investor confidence in the company.

- Company Overview: PennyMac Mortgage Investment Trust is a mortgage REIT primarily investing in residential mortgage loans and related assets, externally managed by PNMAC Capital Management, LLC, a wholly-owned subsidiary of PennyMac Financial Services, Inc., highlighting its expertise in the market.

- Forward-Looking Statements: The announcement includes forward-looking statements regarding potential impacts on financial results and operations due to various factors such as interest rate changes and market conditions, cautioning investors to consider these risks.

PennyMac Mortgage Trust Declares $0.40 Quarterly Dividend

- Quarterly Dividend Declaration: PennyMac Mortgage Investment Trust has declared a quarterly dividend of $0.40 per share, consistent with previous distributions, indicating the company's stable cash flow and commitment to shareholder returns.

- Yield Performance: The forward yield of 13.46% reflects the attractiveness of the investment, particularly in the current interest rate environment, potentially drawing in more investors seeking stable income.

- Shareholder Record Dates: The dividend will be payable on April 24, with a record date of April 9 and an ex-dividend date also on April 9, ensuring shareholders receive their earnings in a timely manner.

- Future Outlook: PennyMac projects 30 securitizations in 2026 as portfolio rotation accelerates, demonstrating the company's proactive strategic positioning in the market, which may further enhance its financial performance.

Dividend Stocks Gain Favor Amid Market Turbulence

- Investor Preference Shift: Amid market turbulence and uncertainty, many investors are turning to dividend-yielding stocks, which typically have high free cash flows and reward shareholders with substantial dividends, indicating a strong desire for stable income.

- Analyst Rating Overview: Benzinga provides the latest analyst ratings on high-yield stocks, allowing investors to review the latest analyses of their favorite stocks by visiting the Analyst Stock Ratings page, thereby enhancing transparency in investment decisions.

- High-Yield Stock Recommendations: In the financial sector, PennyMac Mortgage Investment Trust (NYSE:PMT), Blue Owl Capital Corp (NYSE:OBDC), and Saratoga Investment Corp (NYSE:SAR) are highlighted as three high-yield stocks, reflecting market confidence in these companies.

- Analyst Accuracy: Benzinga's database enables traders to sort ratings by analyst accuracy, which not only improves investors' understanding of market dynamics but may also influence their investment strategies and choices.