Monopar Unveils New Findings on Enhanced Copper Balance in Wilson Disease Patients Treated with Tiomolybdate Choline at AASLD - The Liver Meeting® 2025

Presentation of New Data: Monopar Therapeutics is presenting new findings from the Phase 2 ALXN1840-WD-204 study at the AASLD 2025 conference, highlighting the effectiveness of ALXN1840 (tiomolybdate choline) in improving copper balance in Wilson disease patients.

Significant Results: The study showed a rapid and sustained improvement in daily copper balance, with increased fecal copper excretion among patients treated with ALXN1840, indicating a significant reduction compared to pre-treatment levels.

Company Overview: Monopar Therapeutics is a clinical-stage biopharmaceutical company focused on developing treatments for unmet medical needs, including late-stage ALXN1840 for Wilson disease and various radiopharmaceutical programs for cancer.

Forward-Looking Statements: The press release includes forward-looking statements regarding the company's future plans and potential risks associated with regulatory processes, market acceptance, and funding for ongoing and future projects.

Trade with 70% Backtested Accuracy

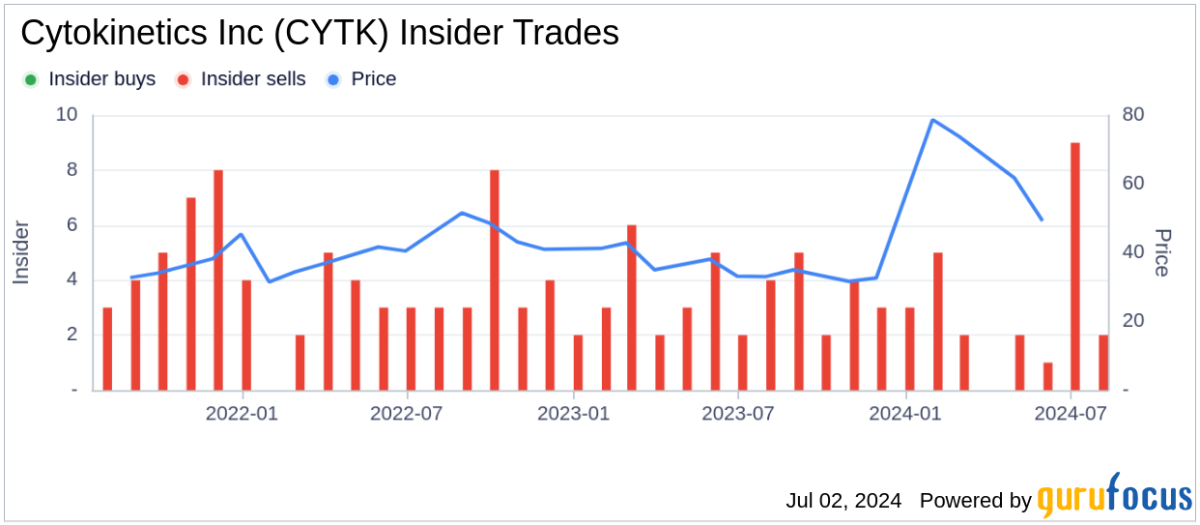

Analyst Views on MNPR

About MNPR

About the author

Monopar Releases New Analysis Data on ALXN1840

- Clinical Trial Results: In the randomized controlled FoCus trial, ALXN1840 demonstrated significant neurologic improvement in Wilson disease patients, with 45% of treated patients achieving clinically meaningful improvement at Week 48 compared to only 32% in the standard care group, indicating ALXN1840's potential to address critical unmet medical needs.

- Reduced Worsening Rates: At Week 48, clinically meaningful neurologic worsening was observed in 25% of patients receiving standard care versus only 9% in the ALXN1840 group (p=0.038), highlighting not only the efficacy of ALXN1840 but also its potential to transform the treatment landscape for Wilson disease.

- Sustained Long-term Efficacy: The neurologic benefits of ALXN1840 continued to increase during long-term follow-up, with a median treatment duration of 2.58 years and a maximum exceeding 8 years, indicating a favorable safety and tolerability profile for long-term use.

- FDA Application Plans: These positive clinical results support Monopar's planned New Drug Application (NDA) submission to the U.S. FDA in mid-2026, which will provide new treatment options for Wilson disease patients and further enhance the company's market position.

Monopar Therapeutics Reports Q4 Earnings Miss

- Earnings Report Disappointment: Monopar Therapeutics reported a Q4 GAAP EPS of -$0.61, missing expectations by $0.16, indicating challenges in profitability that may affect investor confidence.

- Cash Position Overview: As of December 31, 2025, the company had $140.4 million in cash, cash equivalents, and short-term investments, which, while providing some liquidity, raises concerns about capital efficiency and future funding needs.

- Market Reaction Analysis: The earnings miss has led to market concerns regarding Monopar's growth potential, likely putting downward pressure on the stock price and impacting its competitive position in the biopharmaceutical sector.

- Investor Focus: Analysts' quant ratings on Monopar Therapeutics reflect market scrutiny over its financial health, prompting investors to closely monitor future financial performance and strategic adjustments.

Monopar Reports 2025 Financial Results and Drug Development Updates

- Financial Performance Boost: Monopar completed an underwritten public offering generating approximately $91.9 million in 2025, significantly strengthening its balance sheet, with current funds expected to support operations through December 31, 2027, ensuring smooth regulatory and commercial activities for ALXN1840.

- Significant R&D Progress: The NDA for ALXN1840 targeting Wilson disease is planned for submission in mid-2026, with recent presentations at EASL and ANA showcasing long-term efficacy and safety data from 255 patients, indicating statistically significant improvements in copper balance.

- Leadership Team Strengthening: Monopar appointed Susan Rodriguez as Chief Commercial and Strategy Officer to prepare for the potential launch of ALXN1840, further enhancing the company's competitive position in the Wilson disease treatment market.

- R&D Expense Control: R&D expenses for Q4 2025 were $3.9 million, significantly down from $9.9 million in Q4 2024, primarily due to the absence of one-time costs, while reflecting increased investments in personnel and clinical materials.

MONOPAR RELEASES FINANCIAL RESULTS FOR FOURTH QUARTER AND FULL YEAR 2025 ALONG WITH BUSINESS UPDATE

Financial Results Overview: The report presents the financial results for the fourth quarter and the full year of 2025, highlighting key performance metrics and overall financial health.

Business Update: The document provides a comprehensive business update, detailing operational developments and strategic initiatives undertaken during the reporting period.

Goldman Sachs Cuts Netflix Price Target to $112 Ahead of Earnings

- Price Target Adjustment: Goldman Sachs has cut its price target for Netflix from $130 to $112, reflecting a cautious outlook ahead of the upcoming earnings report, which is expected to show solid performance by the end of 2025 as management executes its core strategic focus.

- Content Strategy: Goldman emphasizes that Netflix will continue to rely on original and returning original content to drive user engagement and growth, a strategy that may impact user retention and market share in the competitive streaming landscape.

- Market Expectations: While Goldman maintains a neutral rating on Netflix, the market's reaction to the forthcoming earnings report could lead to stock price volatility, particularly given the uncertainties in the macroeconomic environment.

- Competitive Pressure: Netflix faces competitive pressures from other streaming platforms, especially regarding content richness and user experience, which could affect its growth potential moving forward.

Biotech Stocks Surge at Year-End 2025, ETFs Gain 35.84%

- Sector Recovery: The iShares Biotechnology ETF surged 29.51% year-to-date by December 2025, while the State Street SPDR S&P Biotech ETF achieved an even higher gain of 35.84%, indicating a significant recovery in investor confidence in the biotech sector.

- Surge in M&A Activity: Six of the year's ten largest biopharma deals occurred in Q4, with Johnson & Johnson spending $14.6 billion on Intra Cellular Therapies, signaling a strong commitment from big pharma to expand their pipelines through acquisitions.

- FDA Approvals Boost Innovation: The FDA approved 44 new therapies in 2025, with 26 approvals in the second half, including Cytokinetics' Myqorzo after 27 years, highlighting a supportive regulatory environment for innovation.

- Clinical Trial Successes: Structure Therapeutics saw its stock more than double after its obesity drug trials showed over 15% weight loss in patients, demonstrating the direct impact of clinical success on company valuations.

Monopar Releases New Analysis Data on ALXN1840

- Clinical Trial Results: In the randomized controlled FoCus trial, ALXN1840 demonstrated significant neurologic improvement in Wilson disease patients, with 45% of treated patients achieving clinically meaningful improvement at Week 48 compared to only 32% in the standard care group, indicating ALXN1840's potential to address critical unmet medical needs.

- Reduced Worsening Rates: At Week 48, clinically meaningful neurologic worsening was observed in 25% of patients receiving standard care versus only 9% in the ALXN1840 group (p=0.038), highlighting not only the efficacy of ALXN1840 but also its potential to transform the treatment landscape for Wilson disease.

- Sustained Long-term Efficacy: The neurologic benefits of ALXN1840 continued to increase during long-term follow-up, with a median treatment duration of 2.58 years and a maximum exceeding 8 years, indicating a favorable safety and tolerability profile for long-term use.

- FDA Application Plans: These positive clinical results support Monopar's planned New Drug Application (NDA) submission to the U.S. FDA in mid-2026, which will provide new treatment options for Wilson disease patients and further enhance the company's market position.

Monopar Therapeutics Reports Q4 Earnings Miss

- Earnings Report Disappointment: Monopar Therapeutics reported a Q4 GAAP EPS of -$0.61, missing expectations by $0.16, indicating challenges in profitability that may affect investor confidence.

- Cash Position Overview: As of December 31, 2025, the company had $140.4 million in cash, cash equivalents, and short-term investments, which, while providing some liquidity, raises concerns about capital efficiency and future funding needs.

- Market Reaction Analysis: The earnings miss has led to market concerns regarding Monopar's growth potential, likely putting downward pressure on the stock price and impacting its competitive position in the biopharmaceutical sector.

- Investor Focus: Analysts' quant ratings on Monopar Therapeutics reflect market scrutiny over its financial health, prompting investors to closely monitor future financial performance and strategic adjustments.

Monopar Reports 2025 Financial Results and Drug Development Updates

- Financial Performance Boost: Monopar completed an underwritten public offering generating approximately $91.9 million in 2025, significantly strengthening its balance sheet, with current funds expected to support operations through December 31, 2027, ensuring smooth regulatory and commercial activities for ALXN1840.

- Significant R&D Progress: The NDA for ALXN1840 targeting Wilson disease is planned for submission in mid-2026, with recent presentations at EASL and ANA showcasing long-term efficacy and safety data from 255 patients, indicating statistically significant improvements in copper balance.

- Leadership Team Strengthening: Monopar appointed Susan Rodriguez as Chief Commercial and Strategy Officer to prepare for the potential launch of ALXN1840, further enhancing the company's competitive position in the Wilson disease treatment market.

- R&D Expense Control: R&D expenses for Q4 2025 were $3.9 million, significantly down from $9.9 million in Q4 2024, primarily due to the absence of one-time costs, while reflecting increased investments in personnel and clinical materials.

MONOPAR RELEASES FINANCIAL RESULTS FOR FOURTH QUARTER AND FULL YEAR 2025 ALONG WITH BUSINESS UPDATE

Financial Results Overview: The report presents the financial results for the fourth quarter and the full year of 2025, highlighting key performance metrics and overall financial health.

Business Update: The document provides a comprehensive business update, detailing operational developments and strategic initiatives undertaken during the reporting period.

Goldman Sachs Cuts Netflix Price Target to $112 Ahead of Earnings

- Price Target Adjustment: Goldman Sachs has cut its price target for Netflix from $130 to $112, reflecting a cautious outlook ahead of the upcoming earnings report, which is expected to show solid performance by the end of 2025 as management executes its core strategic focus.

- Content Strategy: Goldman emphasizes that Netflix will continue to rely on original and returning original content to drive user engagement and growth, a strategy that may impact user retention and market share in the competitive streaming landscape.

- Market Expectations: While Goldman maintains a neutral rating on Netflix, the market's reaction to the forthcoming earnings report could lead to stock price volatility, particularly given the uncertainties in the macroeconomic environment.

- Competitive Pressure: Netflix faces competitive pressures from other streaming platforms, especially regarding content richness and user experience, which could affect its growth potential moving forward.

Biotech Stocks Surge at Year-End 2025, ETFs Gain 35.84%

- Sector Recovery: The iShares Biotechnology ETF surged 29.51% year-to-date by December 2025, while the State Street SPDR S&P Biotech ETF achieved an even higher gain of 35.84%, indicating a significant recovery in investor confidence in the biotech sector.

- Surge in M&A Activity: Six of the year's ten largest biopharma deals occurred in Q4, with Johnson & Johnson spending $14.6 billion on Intra Cellular Therapies, signaling a strong commitment from big pharma to expand their pipelines through acquisitions.

- FDA Approvals Boost Innovation: The FDA approved 44 new therapies in 2025, with 26 approvals in the second half, including Cytokinetics' Myqorzo after 27 years, highlighting a supportive regulatory environment for innovation.

- Clinical Trial Successes: Structure Therapeutics saw its stock more than double after its obesity drug trials showed over 15% weight loss in patients, demonstrating the direct impact of clinical success on company valuations.