Momentum Stocks Surge as Wall Street Optimism Grows

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 3 days ago

0mins

Should l Buy INTC?

Source: CNBC

- Record for Momentum ETF: The iShares MSCI USA Momentum Factor ETF (MTUM) hit a new high on Thursday, marking its tenth consecutive winning session, reflecting strong market confidence in growth stocks and suggesting a potential upward trend for the overall market.

- Market Rebound Signs: MTUM, which was down over 7% year-to-date, has now risen 8%, coinciding with the S&P 500's recovery, indicating that the market may be experiencing a broader rebound as investor sentiment turns optimistic.

- Outstanding Stock Performance: Since the onset of the Iran war, Bloom Energy's stock has surged over 40%, while Intel has also risen more than 40%, showcasing the appeal of momentum stocks, particularly following expanded partnerships with major tech companies.

- Momentum Drives Market: Jeff Kilburg, founder of KKM Financial, emphasized that momentum is the primary driver of market gains, predicting that the S&P 500 will reach new all-time highs, with the return of momentum providing strong support for the market.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy INTC?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on INTC

Wall Street analysts forecast INTC stock price to fall

29 Analyst Rating

5 Buy

19 Hold

5 Sell

Hold

Current: 68.500

Low

20.00

Averages

39.30

High

52.00

Current: 68.500

Low

20.00

Averages

39.30

High

52.00

About INTC

Intel Corporation is a global designer and manufacturer of semiconductor products. The Company operates through three segments: Intel Products, Intel Foundry, and All Other. Its Intel Products segment includes Client Computing Group (CCG), Data Center and AI (DCAI), Network and Edge (NEX). The CCG is bringing together the operating system, system architecture, hardware, and software application integration to enable PC experiences. DCAI delivers workload-optimized solutions to cloud service providers and enterprises, along with silicon devices for communications service providers, network and edge, and HPC customers. NEX helps networks and edge compute systems from fixed-function hardware to general-purpose compute, acceleration, and networking devices running cloud native software on programmable hardware. The Intel Foundry segment comprises technology development, manufacturing and foundry services. All Other segments include Altera, Mobileye, Other.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Intel's First Quarter Earnings Outlook is Optimistic

- Strong Earnings Expectations: Intel is expected to report $12.3 billion in revenue for its first quarter earnings on April 23, reflecting analysts' confidence in its profitability and the market's optimistic outlook for future growth.

- Terafab Project Boost: Intel's involvement in the multi-billion-dollar Terafab project enhances its competitiveness in high-end chip production, with the initiative featuring two dedicated production lines that will allow new chip iterations to be manufactured and tested in under a week.

- Analyst Rating Upgrade: Northland analyst Gus Richard raised Intel's price target from $54 to $92 while maintaining an 'Outperform' rating, indicating market recognition of its crucial role in the global artificial intelligence infrastructure buildout.

- Retail Sentiment Extremely Bullish: According to Stocktwits, retail sentiment around Intel remains in 'extremely bullish' territory, with the stock gaining over 89% year-to-date, showcasing strong investor confidence in the company's future prospects.

See More

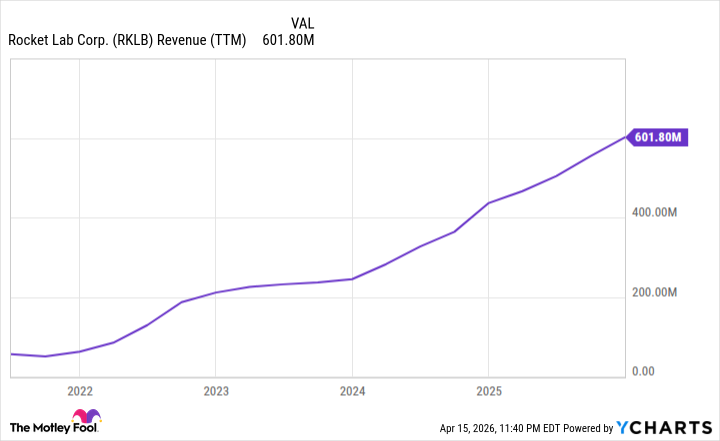

Rocket Lab Stock Up Nearly 250%: A Buy-and-Hold Space Investment?

- Significant Revenue Growth: Rocket Lab achieved record revenue of $602 million in 2025, marking a 38% year-over-year increase, while its backlog surged by 73% to nearly $1.9 billion, indicating strong demand and growth potential in the aerospace market.

- Success Rate and Contracts: The company executed 21 missions last year with a 100% success rate, which helped secure an $816 million contract from the Space Development Agency, further solidifying its leadership position in the aerospace sector.

- Competitive New Rocket: The upcoming Neutron medium-lift rocket will enable Rocket Lab to compete directly with SpaceX's Falcon 9 at a launch price of approximately $15 million less, expected to significantly enhance the company's market share and profitability.

- Investment Risks and Opportunities: Although the stock is trading at about 66 times sales and the company reported a nearly $200 million loss in 2025, the improving margins and potential success of Neutron present substantial growth opportunities, especially in light of SpaceX's IPO plans.

See More

Intel's Stock Soars 66% Amid Nasdaq Rally and Strategic Partnerships

- Market Sentiment Recovery: Since March 30, the Nasdaq Composite index has risen by 17.7%, propelling Intel's stock up by 66% and adding over $137 billion to its market cap, reflecting strong investor confidence in tech stocks.

- Strategic Partnerships Drive Growth: Intel's long-term collaboration with Google, which involves supplying multiple generations of Xeon 6 CPUs for AI workloads, has heightened investor enthusiasm, indicating the company's ongoing commitment to the AI sector.

- Major Project Involvement: Intel's participation in Elon Musk's Terafab project, with initial investments estimated between $20 billion and $25 billion, could lead to significant revenue growth in the long run, further solidifying its market position.

- Valuation Pressure Emerges: Despite the stock's impressive rise, Intel's price-to-earnings ratio stands at 904, with a forward P/E of 135, prompting investors to closely monitor the upcoming earnings report on April 23 to avoid potential price drops due to disappointing results.

See More

Intel's Stock Soars 66% Amid Positive Developments

- Stock Surge: Intel's stock has surged 66% since March 30, adding over $137 billion to its market cap, reflecting market optimism about its growth prospects, particularly as the Nasdaq Composite index rose 17.7% during the same period.

- Collaboration with Google: Intel announced a long-term partnership with Google Cloud to supply its latest Xeon 6 CPUs for AI workloads, which not only enhances its competitiveness in the cloud computing sector but also has the potential to significantly boost future revenues.

- Involvement in Terafab Project: Intel will participate in Elon Musk's Terafab project, with initial investments expected to range from $20 billion to $25 billion, which could lead to substantial revenue growth in the long run and further solidify its position in the semiconductor industry.

- Valuation Risks: Despite the stock's rise, Intel's current P/E ratio stands at 904, with a forward P/E of 135, prompting investors to closely monitor the upcoming earnings report on April 23 to avoid potential price corrections due to disappointing results.

See More

Wall Street Earnings Season Faces Major Test

- Earnings Season Significance: Wall Street is set for a packed earnings season featuring key companies like Capital One and Boeing, with investors eager to glean insights into the economic impact of the Iran war from these reports.

- Capital One Performance Focus: Capital One is scheduled to report earnings on Tuesday, with market attention on its consumer health metrics and the progress of its acquisitions of Discover and Brex, particularly amid rising economic uncertainties.

- Boeing Earnings Outlook: Boeing is expected to release its earnings report on Wednesday, with market focus on order volumes in both its commercial and defense sectors, as well as free cash flow performance, especially after previous unexpected losses.

- GE Vernova Order Growth: GE Vernova will report alongside Boeing, with first-quarter new orders anticipated to reach $14.4 billion, reflecting a 65% year-over-year increase, indicating strong market performance amid rising electricity demand.

See More

Nvidia Stock Retreats but Optimistic Outlook Persists

- Market Performance Retreat: Nvidia's stock price has retreated nearly 4% over the past six months from its 52-week high in October, despite the company continuing to deliver significant growth each quarter, indicating a potential market skepticism about its future performance.

- Analyst Optimism: With a 12-month median price target of $267.50 from 70 analysts, which is 33% higher than Friday's closing price, Nvidia's market cap could rise to $6.5 trillion if this target is met, reflecting strong confidence in its growth prospects.

- Revenue Growth Potential: Nvidia anticipates generating up to $1 trillion in revenue from its Blackwell and Vera Rubin data center lines in 2026 and 2027, significantly exceeding analysts' revenue expectations for the next two years, indicating robust market demand.

- Valuation vs. Growth Comparison: Trading at a forward P/E ratio of 24, slightly above the S&P 500's 21, Nvidia's expected 74% earnings growth this year far surpasses the S&P 500's 17%, suggesting that Nvidia deserves a premium valuation in the market.

See More

Intel's First Quarter Earnings Outlook is Optimistic

- Strong Earnings Expectations: Intel is expected to report $12.3 billion in revenue for its first quarter earnings on April 23, reflecting analysts' confidence in its profitability and the market's optimistic outlook for future growth.

- Terafab Project Boost: Intel's involvement in the multi-billion-dollar Terafab project enhances its competitiveness in high-end chip production, with the initiative featuring two dedicated production lines that will allow new chip iterations to be manufactured and tested in under a week.

- Analyst Rating Upgrade: Northland analyst Gus Richard raised Intel's price target from $54 to $92 while maintaining an 'Outperform' rating, indicating market recognition of its crucial role in the global artificial intelligence infrastructure buildout.

- Retail Sentiment Extremely Bullish: According to Stocktwits, retail sentiment around Intel remains in 'extremely bullish' territory, with the stock gaining over 89% year-to-date, showcasing strong investor confidence in the company's future prospects.

See More

Rocket Lab Stock Up Nearly 250%: A Buy-and-Hold Space Investment?

- Significant Revenue Growth: Rocket Lab achieved record revenue of $602 million in 2025, marking a 38% year-over-year increase, while its backlog surged by 73% to nearly $1.9 billion, indicating strong demand and growth potential in the aerospace market.

- Success Rate and Contracts: The company executed 21 missions last year with a 100% success rate, which helped secure an $816 million contract from the Space Development Agency, further solidifying its leadership position in the aerospace sector.

- Competitive New Rocket: The upcoming Neutron medium-lift rocket will enable Rocket Lab to compete directly with SpaceX's Falcon 9 at a launch price of approximately $15 million less, expected to significantly enhance the company's market share and profitability.

- Investment Risks and Opportunities: Although the stock is trading at about 66 times sales and the company reported a nearly $200 million loss in 2025, the improving margins and potential success of Neutron present substantial growth opportunities, especially in light of SpaceX's IPO plans.

See More

Intel's Stock Soars 66% Amid Nasdaq Rally and Strategic Partnerships

- Market Sentiment Recovery: Since March 30, the Nasdaq Composite index has risen by 17.7%, propelling Intel's stock up by 66% and adding over $137 billion to its market cap, reflecting strong investor confidence in tech stocks.

- Strategic Partnerships Drive Growth: Intel's long-term collaboration with Google, which involves supplying multiple generations of Xeon 6 CPUs for AI workloads, has heightened investor enthusiasm, indicating the company's ongoing commitment to the AI sector.

- Major Project Involvement: Intel's participation in Elon Musk's Terafab project, with initial investments estimated between $20 billion and $25 billion, could lead to significant revenue growth in the long run, further solidifying its market position.

- Valuation Pressure Emerges: Despite the stock's impressive rise, Intel's price-to-earnings ratio stands at 904, with a forward P/E of 135, prompting investors to closely monitor the upcoming earnings report on April 23 to avoid potential price drops due to disappointing results.

See More

Intel's Stock Soars 66% Amid Positive Developments

- Stock Surge: Intel's stock has surged 66% since March 30, adding over $137 billion to its market cap, reflecting market optimism about its growth prospects, particularly as the Nasdaq Composite index rose 17.7% during the same period.

- Collaboration with Google: Intel announced a long-term partnership with Google Cloud to supply its latest Xeon 6 CPUs for AI workloads, which not only enhances its competitiveness in the cloud computing sector but also has the potential to significantly boost future revenues.

- Involvement in Terafab Project: Intel will participate in Elon Musk's Terafab project, with initial investments expected to range from $20 billion to $25 billion, which could lead to substantial revenue growth in the long run and further solidify its position in the semiconductor industry.

- Valuation Risks: Despite the stock's rise, Intel's current P/E ratio stands at 904, with a forward P/E of 135, prompting investors to closely monitor the upcoming earnings report on April 23 to avoid potential price corrections due to disappointing results.

See More

Wall Street Earnings Season Faces Major Test

- Earnings Season Significance: Wall Street is set for a packed earnings season featuring key companies like Capital One and Boeing, with investors eager to glean insights into the economic impact of the Iran war from these reports.

- Capital One Performance Focus: Capital One is scheduled to report earnings on Tuesday, with market attention on its consumer health metrics and the progress of its acquisitions of Discover and Brex, particularly amid rising economic uncertainties.

- Boeing Earnings Outlook: Boeing is expected to release its earnings report on Wednesday, with market focus on order volumes in both its commercial and defense sectors, as well as free cash flow performance, especially after previous unexpected losses.

- GE Vernova Order Growth: GE Vernova will report alongside Boeing, with first-quarter new orders anticipated to reach $14.4 billion, reflecting a 65% year-over-year increase, indicating strong market performance amid rising electricity demand.

See More

Nvidia Stock Retreats but Optimistic Outlook Persists

- Market Performance Retreat: Nvidia's stock price has retreated nearly 4% over the past six months from its 52-week high in October, despite the company continuing to deliver significant growth each quarter, indicating a potential market skepticism about its future performance.

- Analyst Optimism: With a 12-month median price target of $267.50 from 70 analysts, which is 33% higher than Friday's closing price, Nvidia's market cap could rise to $6.5 trillion if this target is met, reflecting strong confidence in its growth prospects.

- Revenue Growth Potential: Nvidia anticipates generating up to $1 trillion in revenue from its Blackwell and Vera Rubin data center lines in 2026 and 2027, significantly exceeding analysts' revenue expectations for the next two years, indicating robust market demand.

- Valuation vs. Growth Comparison: Trading at a forward P/E ratio of 24, slightly above the S&P 500's 21, Nvidia's expected 74% earnings growth this year far surpasses the S&P 500's 17%, suggesting that Nvidia deserves a premium valuation in the market.

See More