Meta and AI Investment Trends Analysis

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Apr 10 2026

0mins

Should l Buy INTC?

Source: NASDAQ.COM

- Strong AI Investment Demand: Anthropic's annual revenue is approximately $30 billion, while OpenAI approaches $25 billion, indicating accelerated enterprise and platform-level AI adoption, with Meta paying about $1.6 billion annually for Anthropic access, underscoring AI's critical role in its product ecosystem.

- Significant Capital Expenditure Increase: Meta has raised its capital expenditure guidance to $115–$135 billion, making it one of the largest capex programs globally, reflecting a sustained commitment to AI and infrastructure investment, which is expected to drive future growth for the company.

- Semiconductor Sector Recovery: Nvidia and Broadcom's stock prices are rebounding as geopolitical pressures ease, with Broadcom trading at a forward P/E of 31x and projected EPS growth of 49%, while Nvidia is at 23x forward P/E with profit growth expected at 39%, demonstrating ongoing market confidence in computing demand.

- Rising Energy Demand: The significant power requirements of large AI data centers are driving investments in renewable energy and distributed generation, with Bloom Energy expected to see a 60% sales growth over the next two years, highlighting its leadership in next-generation energy infrastructure technology.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy INTC?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on INTC

Wall Street analysts forecast INTC stock price to fall

29 Analyst Rating

5 Buy

19 Hold

5 Sell

Hold

Current: 68.500

Low

20.00

Averages

39.30

High

52.00

Current: 68.500

Low

20.00

Averages

39.30

High

52.00

About INTC

Intel Corporation is a global designer and manufacturer of semiconductor products. The Company operates through three segments: Intel Products, Intel Foundry, and All Other. Its Intel Products segment includes Client Computing Group (CCG), Data Center and AI (DCAI), Network and Edge (NEX). The CCG is bringing together the operating system, system architecture, hardware, and software application integration to enable PC experiences. DCAI delivers workload-optimized solutions to cloud service providers and enterprises, along with silicon devices for communications service providers, network and edge, and HPC customers. NEX helps networks and edge compute systems from fixed-function hardware to general-purpose compute, acceleration, and networking devices running cloud native software on programmable hardware. The Intel Foundry segment comprises technology development, manufacturing and foundry services. All Other segments include Altera, Mobileye, Other.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Intel's First Quarter Earnings Outlook is Optimistic

- Strong Earnings Expectations: Intel is expected to report $12.3 billion in revenue for its first quarter earnings on April 23, reflecting analysts' confidence in its profitability and the market's optimistic outlook for future growth.

- Terafab Project Boost: Intel's involvement in the multi-billion-dollar Terafab project enhances its competitiveness in high-end chip production, with the initiative featuring two dedicated production lines that will allow new chip iterations to be manufactured and tested in under a week.

- Analyst Rating Upgrade: Northland analyst Gus Richard raised Intel's price target from $54 to $92 while maintaining an 'Outperform' rating, indicating market recognition of its crucial role in the global artificial intelligence infrastructure buildout.

- Retail Sentiment Extremely Bullish: According to Stocktwits, retail sentiment around Intel remains in 'extremely bullish' territory, with the stock gaining over 89% year-to-date, showcasing strong investor confidence in the company's future prospects.

See More

Ethereum's Outperformance Over Bitcoin Explained

- Ethereum Price Movement: Over the past 12 months, Ethereum has gained 48% while Bitcoin has fallen about 11%, indicating Ethereum's relative strength in the market, which may attract more investor attention.

- Blockchain Upgrade Frequency: Ethereum undergoes two significant upgrades annually, with recent updates like Pectra and Fusaka significantly enhancing data processing capabilities, resulting in gas fees that are 83% lower than a year ago, thereby strengthening its competitive edge in decentralized finance.

- Increased Capital Inflow: The total value locked (TVL) in Ethereum's DeFi protocols has risen from $45 billion to $56 billion over the past year, indicating that more capital is flowing into the Ethereum ecosystem, which will drive the development of new applications and value creation.

- Optimistic Future Outlook: As Ethereum's technical capabilities continue to improve, its price is expected to rebound, narrowing the gap with Bitcoin and further solidifying its leadership position in the cryptocurrency market.

See More

Lockheed Martin vs. Howmet Aerospace: Which Stock is the Better Buy?

- Howmet Aerospace Growth: Howmet reported a record revenue of $8.3 billion in 2025, an 11% increase, with EPS rising 32% to $3.71, indicating strong demand for its critical components in the aerospace and defense sectors, particularly for the F-35 program.

- Optimistic Future Projections: The company forecasts 2026 revenue between $9 billion and $9.2 billion, reflecting a 9.6% increase at the midpoint, alongside an 18% rise in adjusted EPS, which will provide sufficient free cash flow to continue boosting dividends, showcasing resilience in uncertain market conditions.

- Lockheed Martin Stability: Lockheed achieved $75 billion in revenue for 2025, with EPS down 23% to $21.49 due to non-recurring charges; however, its $194 billion backlog ensures stable future cash flows, highlighting its critical role in the growing defense budget.

- Dividend Performance Comparison: Lockheed has increased its dividend for 23 consecutive years, with a recent 5% boost to $3.45 per share, yielding around 2.2%, while Howmet's shorter dividend history and lower yield suggest Lockheed offers more attractive returns for investors.

See More

Chewy: A No-Brainer Growth Stock to Buy Now

- Autoship Program Growth: Chewy's Autoship service accounted for 84% of sales in Q4, up from 80.6% a year ago, which not only locks in customers but also reduces inventory management costs, thereby enhancing the company's profitability.

- Strong Advertising Business: Chewy Ads is experiencing growth driven by first-party data and a highly engaged audience, with CEO Sumit Singh noting that a significant portion of ad-attributed purchases comes from Autoship orders, providing advertisers with high returns on investment and further boosting the company's overall operating margin.

- Healthcare Business Expansion: As of early April, Chewy had 18 Vet Care clinics and recently added 29 more through the acquisition of Modern Animal, with the healthcare business operating at a higher margin, providing a new avenue to attract customers while tightly integrating with its online pharmacy to enhance customer retention.

- Improving Profitability: Chewy's adjusted EBITDA margin was 5.7% last year, up from 4.8% the previous year, with management expecting continued expansion this year and a long-term goal of reaching a 10% EBITDA margin, indicating a potential 75% growth in EBITDA even without revenue growth.

See More

Market Dynamics: The Tug-of-War Between Bonds and Oil Prices

- Bond Market Stability: The slight decline in bond yields indicates a stable market outlook, which helps support the stock market, particularly amid oil price fluctuations, thereby reducing investor panic.

- Tech Stock Recovery: The so-called 'Magnificent Seven' tech companies, including Alphabet and Amazon, are beginning to reap benefits from their previous high expenditures, enhancing market confidence in their future profitability, which could drive further market gains.

- Rise of the AI Economy: The emergence of AI agents is expected to significantly reduce hiring and operational costs for enterprises, driving demand for chips like Nvidia's, which will further boost growth for related companies.

- Improved Investor Sentiment: Despite ongoing market uncertainties, the combination of low bond yields and strong performance from tech stocks fosters an optimistic outlook among investors, potentially attracting more capital into the stock market.

See More

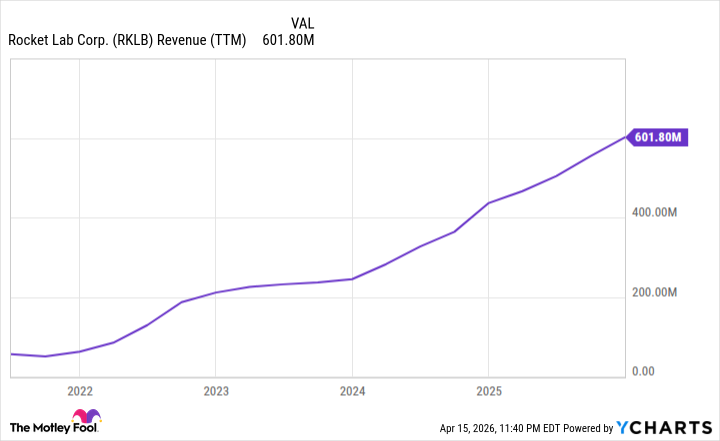

Rocket Lab Stock Up Nearly 250%: A Buy-and-Hold Space Investment?

- Significant Revenue Growth: Rocket Lab achieved record revenue of $602 million in 2025, marking a 38% year-over-year increase, while its backlog surged by 73% to nearly $1.9 billion, indicating strong demand and growth potential in the aerospace market.

- Success Rate and Contracts: The company executed 21 missions last year with a 100% success rate, which helped secure an $816 million contract from the Space Development Agency, further solidifying its leadership position in the aerospace sector.

- Competitive New Rocket: The upcoming Neutron medium-lift rocket will enable Rocket Lab to compete directly with SpaceX's Falcon 9 at a launch price of approximately $15 million less, expected to significantly enhance the company's market share and profitability.

- Investment Risks and Opportunities: Although the stock is trading at about 66 times sales and the company reported a nearly $200 million loss in 2025, the improving margins and potential success of Neutron present substantial growth opportunities, especially in light of SpaceX's IPO plans.

See More

Intel's First Quarter Earnings Outlook is Optimistic

- Strong Earnings Expectations: Intel is expected to report $12.3 billion in revenue for its first quarter earnings on April 23, reflecting analysts' confidence in its profitability and the market's optimistic outlook for future growth.

- Terafab Project Boost: Intel's involvement in the multi-billion-dollar Terafab project enhances its competitiveness in high-end chip production, with the initiative featuring two dedicated production lines that will allow new chip iterations to be manufactured and tested in under a week.

- Analyst Rating Upgrade: Northland analyst Gus Richard raised Intel's price target from $54 to $92 while maintaining an 'Outperform' rating, indicating market recognition of its crucial role in the global artificial intelligence infrastructure buildout.

- Retail Sentiment Extremely Bullish: According to Stocktwits, retail sentiment around Intel remains in 'extremely bullish' territory, with the stock gaining over 89% year-to-date, showcasing strong investor confidence in the company's future prospects.

See More

Ethereum's Outperformance Over Bitcoin Explained

- Ethereum Price Movement: Over the past 12 months, Ethereum has gained 48% while Bitcoin has fallen about 11%, indicating Ethereum's relative strength in the market, which may attract more investor attention.

- Blockchain Upgrade Frequency: Ethereum undergoes two significant upgrades annually, with recent updates like Pectra and Fusaka significantly enhancing data processing capabilities, resulting in gas fees that are 83% lower than a year ago, thereby strengthening its competitive edge in decentralized finance.

- Increased Capital Inflow: The total value locked (TVL) in Ethereum's DeFi protocols has risen from $45 billion to $56 billion over the past year, indicating that more capital is flowing into the Ethereum ecosystem, which will drive the development of new applications and value creation.

- Optimistic Future Outlook: As Ethereum's technical capabilities continue to improve, its price is expected to rebound, narrowing the gap with Bitcoin and further solidifying its leadership position in the cryptocurrency market.

See More

Lockheed Martin vs. Howmet Aerospace: Which Stock is the Better Buy?

- Howmet Aerospace Growth: Howmet reported a record revenue of $8.3 billion in 2025, an 11% increase, with EPS rising 32% to $3.71, indicating strong demand for its critical components in the aerospace and defense sectors, particularly for the F-35 program.

- Optimistic Future Projections: The company forecasts 2026 revenue between $9 billion and $9.2 billion, reflecting a 9.6% increase at the midpoint, alongside an 18% rise in adjusted EPS, which will provide sufficient free cash flow to continue boosting dividends, showcasing resilience in uncertain market conditions.

- Lockheed Martin Stability: Lockheed achieved $75 billion in revenue for 2025, with EPS down 23% to $21.49 due to non-recurring charges; however, its $194 billion backlog ensures stable future cash flows, highlighting its critical role in the growing defense budget.

- Dividend Performance Comparison: Lockheed has increased its dividend for 23 consecutive years, with a recent 5% boost to $3.45 per share, yielding around 2.2%, while Howmet's shorter dividend history and lower yield suggest Lockheed offers more attractive returns for investors.

See More

Chewy: A No-Brainer Growth Stock to Buy Now

- Autoship Program Growth: Chewy's Autoship service accounted for 84% of sales in Q4, up from 80.6% a year ago, which not only locks in customers but also reduces inventory management costs, thereby enhancing the company's profitability.

- Strong Advertising Business: Chewy Ads is experiencing growth driven by first-party data and a highly engaged audience, with CEO Sumit Singh noting that a significant portion of ad-attributed purchases comes from Autoship orders, providing advertisers with high returns on investment and further boosting the company's overall operating margin.

- Healthcare Business Expansion: As of early April, Chewy had 18 Vet Care clinics and recently added 29 more through the acquisition of Modern Animal, with the healthcare business operating at a higher margin, providing a new avenue to attract customers while tightly integrating with its online pharmacy to enhance customer retention.

- Improving Profitability: Chewy's adjusted EBITDA margin was 5.7% last year, up from 4.8% the previous year, with management expecting continued expansion this year and a long-term goal of reaching a 10% EBITDA margin, indicating a potential 75% growth in EBITDA even without revenue growth.

See More

Market Dynamics: The Tug-of-War Between Bonds and Oil Prices

- Bond Market Stability: The slight decline in bond yields indicates a stable market outlook, which helps support the stock market, particularly amid oil price fluctuations, thereby reducing investor panic.

- Tech Stock Recovery: The so-called 'Magnificent Seven' tech companies, including Alphabet and Amazon, are beginning to reap benefits from their previous high expenditures, enhancing market confidence in their future profitability, which could drive further market gains.

- Rise of the AI Economy: The emergence of AI agents is expected to significantly reduce hiring and operational costs for enterprises, driving demand for chips like Nvidia's, which will further boost growth for related companies.

- Improved Investor Sentiment: Despite ongoing market uncertainties, the combination of low bond yields and strong performance from tech stocks fosters an optimistic outlook among investors, potentially attracting more capital into the stock market.

See More

Rocket Lab Stock Up Nearly 250%: A Buy-and-Hold Space Investment?

- Significant Revenue Growth: Rocket Lab achieved record revenue of $602 million in 2025, marking a 38% year-over-year increase, while its backlog surged by 73% to nearly $1.9 billion, indicating strong demand and growth potential in the aerospace market.

- Success Rate and Contracts: The company executed 21 missions last year with a 100% success rate, which helped secure an $816 million contract from the Space Development Agency, further solidifying its leadership position in the aerospace sector.

- Competitive New Rocket: The upcoming Neutron medium-lift rocket will enable Rocket Lab to compete directly with SpaceX's Falcon 9 at a launch price of approximately $15 million less, expected to significantly enhance the company's market share and profitability.

- Investment Risks and Opportunities: Although the stock is trading at about 66 times sales and the company reported a nearly $200 million loss in 2025, the improving margins and potential success of Neutron present substantial growth opportunities, especially in light of SpaceX's IPO plans.

See More