LATAM Airlines, Kohl's, and Dollar General Rated Buy with Strong Value Metrics

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Jan 12 2026

0mins

Source: NASDAQ.COM

- LATAM Airlines Performance: LATAM Airlines Group holds a Zacks Rank of #1, with the current year earnings consensus estimate rising by 4.2% over the past 60 days, indicating enhanced profitability that is likely to boost investor confidence.

- Kohl's Strong Growth: Kohl's Corporation also carries a Zacks Rank of #1, with the consensus estimate for next year's earnings increasing by 104.4% in the last 60 days, suggesting robust market demand that may attract more investor attention.

- Dollar General's Stability: Dollar General Corporation has a Zacks Rank of #1, with the current year earnings consensus estimate up by 5.4%, and a P/E ratio of 22.26, which is lower than the industry average of 28.60, highlighting its relative value appeal.

- Investment Opportunities: These companies have been handpicked by Zacks experts, expected to gain over 100% in the coming months, presenting excellent investment opportunities, especially given their lower visibility in the market.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy DG?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on DG

Wall Street analysts forecast DG stock price to rise

16 Analyst Rating

9 Buy

7 Hold

0 Sell

Moderate Buy

Current: 126.460

Low

125.00

Averages

147.00

High

170.00

Current: 126.460

Low

125.00

Averages

147.00

High

170.00

About DG

Dollar General Corporation is a discount retailer. The Company offers merchandise, including consumable items, seasonal items, home products and apparel. Its merchandise includes brands from manufacturers, as well as its own private brand selections with prices at discounts to brands. Its consumables category includes paper and cleaning products, packaged food, perishables, snacks, health and beauty, pet, and tobacco products. Its seasonal products include holiday items, toys, batteries, small electronics, greeting cards, stationery, prepaid phones and accessories, gardening supplies, hardware, automotive and home office supplies. Its home products include kitchen supplies, cookware, small appliances, light bulbs, storage containers, frames, candles, craft supplies and kitchen, bed and bath soft goods. The Company’s apparel products include basic items for infants, toddlers, girls, boys, women and men, as well as socks, underwear, disposable diapers, shoes and accessories.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Charles Schwab Named 'Stock to Study' by BetterInvesting

- Investor Interest: Charles Schwab Corp.'s recent report has sparked investor curiosity regarding whether its stock is fairly valued, indicating a rising interest in the company within the market.

- Research Recommendation: BetterInvesting Magazine's Editorial Advisory Committee has named Charles Schwab as the 'Stock to Study' for the June/July 2026 issue, aimed at providing informational and educational support for investors.

- Transparency in Fundamentals: Investors can access key fundamental data such as sales, earnings, pre-tax profit, and return on equity through the National Association of Investors' website, enhancing transparency in investment decision-making.

- Educational Mission: Since its establishment in 1951, BetterInvesting has been dedicated to empowering everyday Americans with investment education, helping over 5 million people improve their financial futures, highlighting its significance in the investment education sector.

See More

Charles Schwab Corp Named 'Stock to Study' by BetterInvesting

- Stock Study Recommendation: Charles Schwab Corp has been designated as the 'Stock to Study' for the June/July 2026 issue of BetterInvesting Magazine, indicating a rising interest among investors that may attract further analysis and investment.

- Transparent Fundamental Data: Investors can access key financial metrics such as sales, earnings, pre-tax profit, and return on equity through a dedicated page by the National Association of Investors, enhancing decision-making transparency and information accessibility.

- Educational Purpose Emphasis: The magazine's committee, composed of several CFAs, emphasizes that the mentioned securities are for educational purposes only, reminding investors to conduct independent analyses before making investment decisions, thereby reducing the risk of misinformation.

- Non-Profit Organization Background: BetterInvesting, established in 1951 as a 501(c)(3) non-profit investment education organization, is dedicated to empowering everyday Americans to improve their financial futures, highlighting its significant role and impact in the investment education sector.

See More

Charles Schwab Named 'Stock to Study' by BetterInvesting

- Investor Interest: Charles Schwab Corp. (NYSE:SCHW) has sparked investor curiosity regarding whether its stock is fairly valued, indicating a heightened market interest in its future performance.

- Educational Resource Provision: BetterInvesting Magazine's Editorial Advisory Committee has designated Charles Schwab as the 'Stock to Study' for the June/July 2026 issue, providing comprehensive fundamental data to assist investors in making informed decisions.

- Comprehensive Report Release: The magazine will feature a detailed report on Charles Schwab in the upcoming issue, covering key financial metrics such as sales, earnings, pre-tax profit, and return on equity, thereby enhancing investors' analytical capabilities.

- Industry Influence: BetterInvesting, a nonprofit investment education organization, has been empowering Americans since 1951, highlighting its significant role and impact in the field of investment education.

See More

Dividend Investors' Safe Strategies Amid Market Challenges

- REIT Performance: Realty Income owns approximately 15,500 single-tenant net-leased properties, with nearly 99% leased, ensuring a steady revenue stream, and has paid monthly dividends since 1994, with an annual payout of about $3.25 per share, yielding 5%, significantly above the S&P 500's 1.1% average.

- Coca-Cola's Transformation: PepsiCo, known as a 'Dividend King' for raising dividends for 54 consecutive years, currently pays a dividend of $5.69 per share with a yield of about 3.6%, and despite health-conscious trends, net revenue grew by 2% in 2025 and nearly 9% in Q1 2026, demonstrating resilience in adversity.

- Brand Integration Challenges: J.M. Smucker, with its portfolio of well-known brands, faces integration challenges from the Hostess Cakes acquisition, with sales not meeting expectations; however, its dividend has increased for 24 straight years, currently at $4.40 per share with a yield of 4.7%, and free cash flow easily covered $348 million in dividend costs for the first three quarters.

- Market Volatility Impact: Although J.M. Smucker's stock has declined over 40% since 2023, its P/E ratio has fallen to 22, still providing a solid investment opportunity for income-seeking investors, indicating the company's strong capability to maintain high-yield dividends.

See More

Realty Income Maintains Steady Dividend Growth

- Consistent Dividend History: Realty Income has paid monthly dividends since 1994, with an annual payout of nearly $3.25 per share and a yield of 5%, significantly above the S&P 500's 1.1%, demonstrating its stability and attractiveness in uncertain markets.

- Strong Cash Flow Support: The company generates $4.25 per share in funds from operations, covering dividend expenses and maintaining a price-to-earnings ratio of 15, indicating that investors can purchase a high-yield stock at a relatively low price, enhancing its appeal.

- Sustainable Growth Potential: Despite market challenges, PepsiCo maintains a 54-year dividend growth streak, with a current payout of $5.69 per share yielding 3.6%, showcasing its resilience underpinned by a diversified product portfolio and stable cash flow.

- Attractive Discount Pricing: J.M. Smucker offers a $4.40 per share dividend with a yield of 4.7%, and despite facing sales pressures, its $672 million in free cash flow easily covers $348 million in dividend expenses, indicating its ongoing capacity for high-yield dividends.

See More

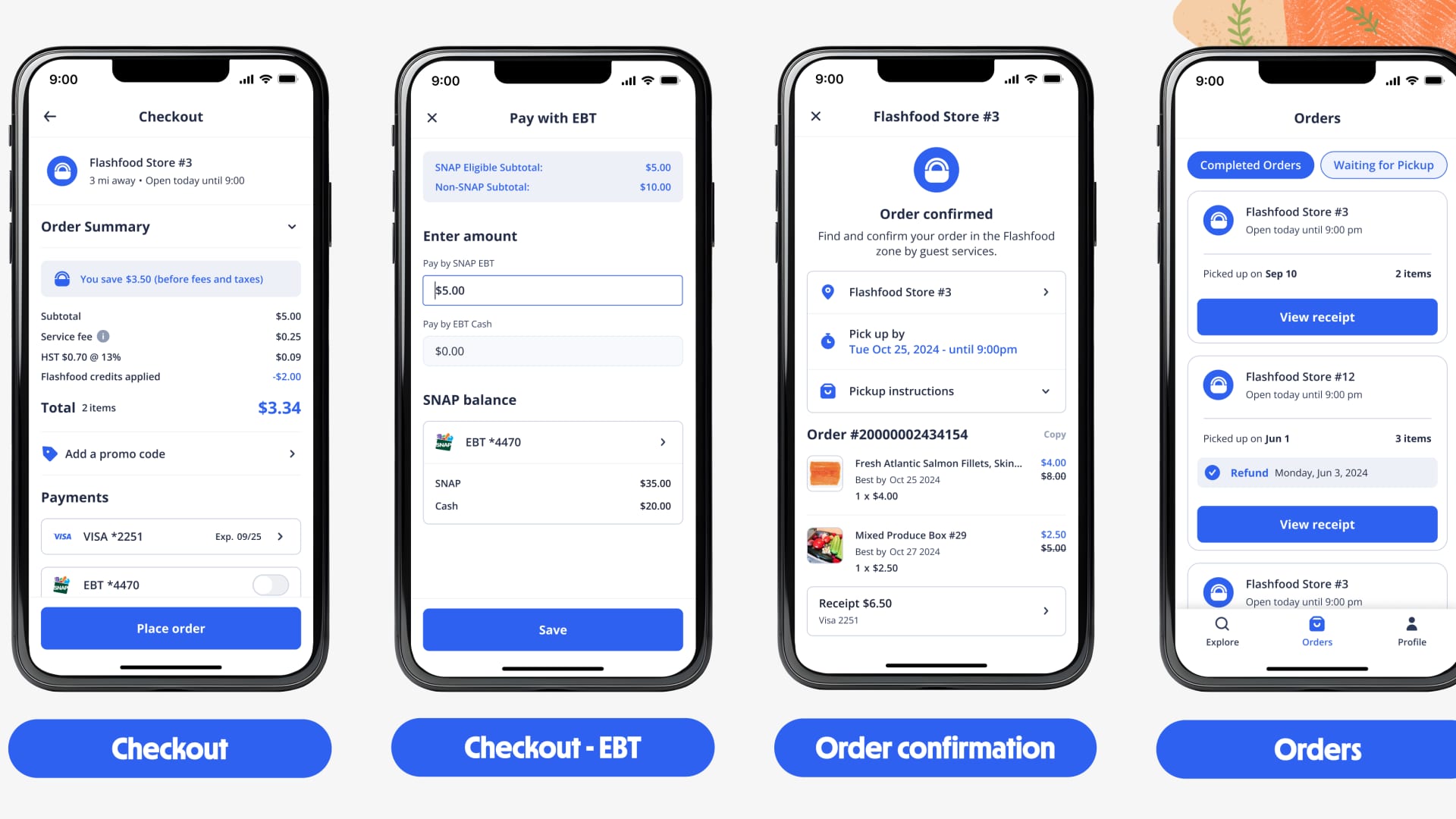

Kroger Leverages AI to Optimize Food Pricing

- AI-Driven Pricing Strategy: Kroger is utilizing AI to adjust pricing on perishable items, aiming to reduce the approximately 30% of food waste that translates to nearly $18.2 billion in losses annually, thereby enhancing profit margins and improving customer experience.

- Intensified Market Competition: With 89% of consumers seeking discounts, Kroger's Flashfood app aids grocers in dynamic pricing, expected to attract more customers and increase average shopping frequency by nearly four additional trips per month, further driving sales growth.

- Inventory Loss Reduction: Flashfood's partners have reduced shrink by an average of 27%, while also increasing customer traffic, indicating that targeted discount strategies can effectively boost sales and minimize food waste.

- Data-Driven Decision Making: Kroger leverages consumer behavior data generated by AI to optimize product pricing and inventory management, enhancing margins on fresh foods and bakery items, showcasing its leadership in data application.

See More

Charles Schwab Named 'Stock to Study' by BetterInvesting

- Investor Interest: Charles Schwab Corp.'s recent report has sparked investor curiosity regarding whether its stock is fairly valued, indicating a rising interest in the company within the market.

- Research Recommendation: BetterInvesting Magazine's Editorial Advisory Committee has named Charles Schwab as the 'Stock to Study' for the June/July 2026 issue, aimed at providing informational and educational support for investors.

- Transparency in Fundamentals: Investors can access key fundamental data such as sales, earnings, pre-tax profit, and return on equity through the National Association of Investors' website, enhancing transparency in investment decision-making.

- Educational Mission: Since its establishment in 1951, BetterInvesting has been dedicated to empowering everyday Americans with investment education, helping over 5 million people improve their financial futures, highlighting its significance in the investment education sector.

See More

Charles Schwab Corp Named 'Stock to Study' by BetterInvesting

- Stock Study Recommendation: Charles Schwab Corp has been designated as the 'Stock to Study' for the June/July 2026 issue of BetterInvesting Magazine, indicating a rising interest among investors that may attract further analysis and investment.

- Transparent Fundamental Data: Investors can access key financial metrics such as sales, earnings, pre-tax profit, and return on equity through a dedicated page by the National Association of Investors, enhancing decision-making transparency and information accessibility.

- Educational Purpose Emphasis: The magazine's committee, composed of several CFAs, emphasizes that the mentioned securities are for educational purposes only, reminding investors to conduct independent analyses before making investment decisions, thereby reducing the risk of misinformation.

- Non-Profit Organization Background: BetterInvesting, established in 1951 as a 501(c)(3) non-profit investment education organization, is dedicated to empowering everyday Americans to improve their financial futures, highlighting its significant role and impact in the investment education sector.

See More

Charles Schwab Named 'Stock to Study' by BetterInvesting

- Investor Interest: Charles Schwab Corp. (NYSE:SCHW) has sparked investor curiosity regarding whether its stock is fairly valued, indicating a heightened market interest in its future performance.

- Educational Resource Provision: BetterInvesting Magazine's Editorial Advisory Committee has designated Charles Schwab as the 'Stock to Study' for the June/July 2026 issue, providing comprehensive fundamental data to assist investors in making informed decisions.

- Comprehensive Report Release: The magazine will feature a detailed report on Charles Schwab in the upcoming issue, covering key financial metrics such as sales, earnings, pre-tax profit, and return on equity, thereby enhancing investors' analytical capabilities.

- Industry Influence: BetterInvesting, a nonprofit investment education organization, has been empowering Americans since 1951, highlighting its significant role and impact in the field of investment education.

See More

Dividend Investors' Safe Strategies Amid Market Challenges

- REIT Performance: Realty Income owns approximately 15,500 single-tenant net-leased properties, with nearly 99% leased, ensuring a steady revenue stream, and has paid monthly dividends since 1994, with an annual payout of about $3.25 per share, yielding 5%, significantly above the S&P 500's 1.1% average.

- Coca-Cola's Transformation: PepsiCo, known as a 'Dividend King' for raising dividends for 54 consecutive years, currently pays a dividend of $5.69 per share with a yield of about 3.6%, and despite health-conscious trends, net revenue grew by 2% in 2025 and nearly 9% in Q1 2026, demonstrating resilience in adversity.

- Brand Integration Challenges: J.M. Smucker, with its portfolio of well-known brands, faces integration challenges from the Hostess Cakes acquisition, with sales not meeting expectations; however, its dividend has increased for 24 straight years, currently at $4.40 per share with a yield of 4.7%, and free cash flow easily covered $348 million in dividend costs for the first three quarters.

- Market Volatility Impact: Although J.M. Smucker's stock has declined over 40% since 2023, its P/E ratio has fallen to 22, still providing a solid investment opportunity for income-seeking investors, indicating the company's strong capability to maintain high-yield dividends.

See More

Realty Income Maintains Steady Dividend Growth

- Consistent Dividend History: Realty Income has paid monthly dividends since 1994, with an annual payout of nearly $3.25 per share and a yield of 5%, significantly above the S&P 500's 1.1%, demonstrating its stability and attractiveness in uncertain markets.

- Strong Cash Flow Support: The company generates $4.25 per share in funds from operations, covering dividend expenses and maintaining a price-to-earnings ratio of 15, indicating that investors can purchase a high-yield stock at a relatively low price, enhancing its appeal.

- Sustainable Growth Potential: Despite market challenges, PepsiCo maintains a 54-year dividend growth streak, with a current payout of $5.69 per share yielding 3.6%, showcasing its resilience underpinned by a diversified product portfolio and stable cash flow.

- Attractive Discount Pricing: J.M. Smucker offers a $4.40 per share dividend with a yield of 4.7%, and despite facing sales pressures, its $672 million in free cash flow easily covers $348 million in dividend expenses, indicating its ongoing capacity for high-yield dividends.

See More

Kroger Leverages AI to Optimize Food Pricing

- AI-Driven Pricing Strategy: Kroger is utilizing AI to adjust pricing on perishable items, aiming to reduce the approximately 30% of food waste that translates to nearly $18.2 billion in losses annually, thereby enhancing profit margins and improving customer experience.

- Intensified Market Competition: With 89% of consumers seeking discounts, Kroger's Flashfood app aids grocers in dynamic pricing, expected to attract more customers and increase average shopping frequency by nearly four additional trips per month, further driving sales growth.

- Inventory Loss Reduction: Flashfood's partners have reduced shrink by an average of 27%, while also increasing customer traffic, indicating that targeted discount strategies can effectively boost sales and minimize food waste.

- Data-Driven Decision Making: Kroger leverages consumer behavior data generated by AI to optimize product pricing and inventory management, enhancing margins on fresh foods and bakery items, showcasing its leadership in data application.

See More