Hasbro Provides Strong Q1 Guidance Update, Shares Surge

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Apr 23 2026

0mins

Should l Buy HAS?

Source: seekingalpha

- Q1 Revenue Growth: Hasbro anticipates Q1 revenue between $970 million and $985 million, reflecting a 9% to 11% year-over-year increase, significantly exceeding the consensus estimate of $909 million, driven by robust performance in the MAGIC: THE GATHERING segment, which boosts investor confidence.

- Full-Year Outlook Reaffirmed: The company reiterated its full-year 2026 outlook, projecting 3% to 5% constant-currency revenue growth, a 24% to 25% adjusted operating margin, and adjusted EBITDA of $1.40 billion to $1.45 billion, indicating strong confidence and stability in future growth.

- Cybersecurity Incident Update: Hasbro provided an update on the previously disclosed unauthorized network access incident, stating that it appears contained; while it did not impact Q1 financial results, it did slow the preparation and filing of quarterly results, demonstrating the company's transparency in addressing cybersecurity challenges.

- Product Shipment Plans On Track: Despite some processing and shipping delays, Hasbro confirmed that MAGIC: THE GATHERING shipments and release cadence remain on schedule for Q2, with expectations to make up for delayed consumer product shipments in the second half of the year, showcasing the resilience of its supply chain.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy HAS?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on HAS

Wall Street analysts forecast HAS stock price to rise

9 Analyst Rating

7 Buy

1 Hold

1 Sell

Moderate Buy

Current: 95.250

Low

90.00

Averages

95.71

High

100.00

Current: 95.250

Low

90.00

Averages

95.71

High

100.00

About HAS

Hasbro, Inc. is a game, intellectual property (IP) and toy company. The Company delivers play experiences to kids, families, and fans around the world, through physical and digital games, video games, and toys, among others. Its Consumer Products segment engages in the sourcing, marketing and sales of toy and game products around the world. Its Wizards of the Coast and Digital Gaming segment engages in the promotion of the Company's brands through the development of trading cards, role-playing and digital game experiences based on Hasbro and Wizards of the Coast games. Its Entertainment segment engages in the development and production of Hasbro-branded entertainment content, including film, television, children’s programming, digital content and live entertainment focused on Hasbro-owned properties. Its portfolio of brands includes MAGIC: THE GATHERING, DUNGEONS & DRAGONS, MONOPOLY, HASBRO GAMES, NERF, TRANSFORMERS, PLAY-DOH and PEPPA PIG, as well as premier partner brands.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

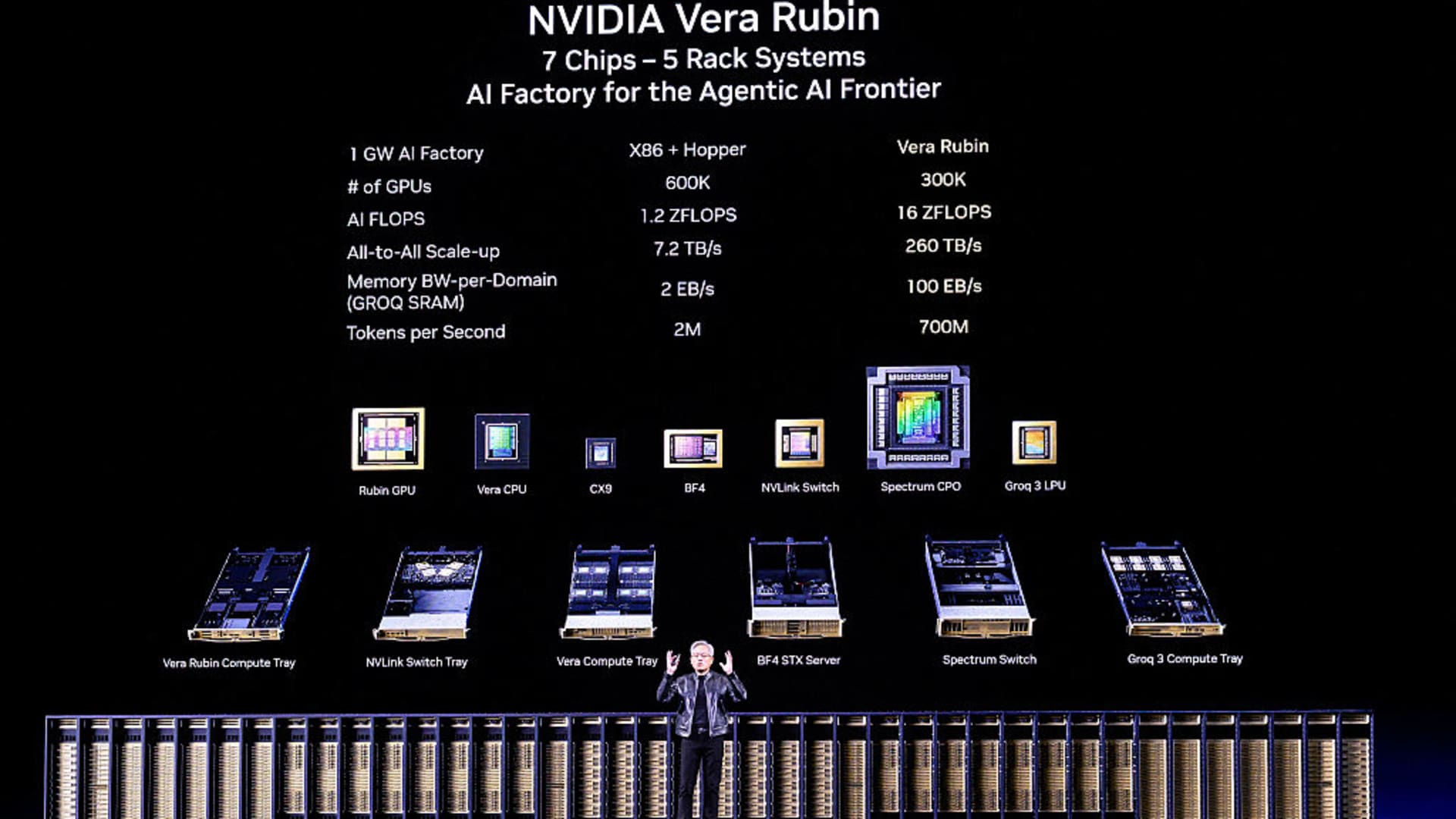

Nvidia Earnings Week Approaches, Market Anticipates Key Insights

- Nvidia Earnings Expectations: Nvidia is set to report its Q1 earnings on Wednesday, with revenue anticipated at $78.67 billion and EPS of $1.76, as analysts look for results that exceed expectations to boost stock prices and alleviate concerns about a slowing investment cycle.

- Home Depot Performance Outlook: Home Depot is expected to see only 0.8% same-store sales growth in Q1, as rising mortgage rates and a challenging economic backdrop lead analysts to predict its full-year guidance will remain flat to 2%, reflecting low market expectations for its performance.

- TJX Companies Performance: TJX anticipates a 4.1% same-store sales growth in Q1, benefiting from consumer demand for quality merchandise at affordable prices, although rising freight costs may impact margins; nonetheless, the company is viewed as a solid long-term investment.

- Google Developer Conference: Google will host its annual developer conference on Tuesday and Wednesday, with analysts warning that a lack of a

See More

Ross Stores and TJX Companies Earnings Outlook

- Earnings Reporting Outlook: Ross Stores and TJX Companies are set to report quarterly results on Wednesday and Thursday, respectively, with analysts expecting both to showcase strong earnings momentum, particularly against a backdrop of overall positive retail performance.

- Upward Earnings Revisions: According to FactSet data, both companies have seen their earnings estimates revised up by over 10% in the past three to six months, indicating increased market confidence in their future performance, which could drive stock price increases.

- Divergent Stock Performance: While TJX Companies has seen a 4% decline in 2026, Ross Stores has experienced an 18% increase, reflecting differing market expectations and shifts in investor sentiment towards the two stocks.

- Analyst Rating Support: Deutsche Bank reiterated its buy ratings on both stocks ahead of their earnings reports, with analyst Krisztina Katai noting that Ross Stores' same-store sales momentum continues to exceed expectations, while TJX's business model is well-positioned to maintain competitive advantages.

See More

Can the AI Rally Sustain Amid Inflation Fears?

- Market Performance Review: The S&P 500 has surged approximately 19% since its March low, surpassing 7,500 for the first time this week, reflecting a revival in enthusiasm for artificial intelligence, yet the absence of cyclical sectors raises concerns.

- Internal and External Pressures: Despite a 3% rise in the S&P 500 this month, it remains nearly flat on an equal-weight basis, with the financial sector being the worst performer year-to-date, down over 6%, indicating potential impacts of high inflation on the economy.

- Nvidia Earnings Outlook: Nvidia is set to report earnings, with high expectations that CEO Jensen Huang will once again deliver a beat, although its market cap nearing $6 trillion marks a historic high, its valuation appears relatively attractive compared to peers.

- Retail Market Dynamics: Retailers like Walmart and Target are about to release earnings, and the low consumer sentiment may affect sales performance, particularly for lower-income consumers under pressure from rising oil prices, with Walmart's low-price strategy potentially giving it a competitive edge.

See More

Mattel Responds to Activist Investor's Sale Proposal

- Ongoing Shareholder Communication: Mattel (MAT) emphasized its commitment to ongoing communication with shareholders, valuing their perspectives and appreciating Southeastern Asset Management's continued engagement, indicating the company's attentiveness to shareholder opinions.

- Commitment to Strategic Review: The Mattel board and management team are dedicated to regularly reviewing the company's strategy, performance, and opportunities to enhance long-term value, demonstrating a proactive approach to shareholder interests and future growth.

- Positive Analyst Outlook: Jefferies analyst Kylie Cohu noted that while Mattel faces pressure from activist investors, no immediate changes are expected, suggesting that activism may cap downside risks and revive optionality, maintaining a Buy rating on Mattel.

- Slight Stock Increase: Shares of Mattel (MAT) rose 1.3% in premarket trading, despite a 24% decline year-to-date, reflecting cautious optimism in the market regarding the company's future potential.

See More

Investor Calls for Mattel to Explore Buyout Options

- Investor Push for Privatization: Southeastern Asset Management, holding about 4% or $170 million of Mattel's stock, has urged CEO Ynon Kreiz to consider taking the company private or a buyout by Hasbro in light of weak demand.

- Poor Financial Performance: Mattel reported a larger adjusted operating loss of $70 million for the three months ending in March, up from $8 million a year ago, despite exceeding quarterly sales expectations, highlighting challenges in its transformation efforts.

- Potential for Industry Consolidation: Southeastern emphasized that synergies between Mattel and Hasbro could be significant, arguing that Hasbro's superior execution in digital growth gives it a competitive edge, making a merger more necessary.

- Focus on Strategic Execution: Mattel stated it will continue to focus on its IP-driven strategy, even as it faces challenges from supply chain bottlenecks and declining demand for traditional toys, with the board regularly reviewing strategic opportunities to enhance long-term value.

See More

Grindr Nominates New Board Members for 2026

- Board Member Nominations: Grindr has announced the nomination of Rob Solomon, Lisa Gersh, and Fadi Hanna for election at the Annual Meeting of Shareholders on June 2, 2026, aiming to enhance the Board's strategic and governance capabilities to support the company's next phase of growth.

- Rob Solomon's Background: As CEO of H55, Solomon has extensive experience in electric aviation and previously led GoFundMe and Groupon, overseeing billions in donations and demonstrating exceptional operational and growth capabilities.

- Lisa Gersh's Contributions: Gersh brings deep expertise in consumer brands and media, having served as CEO for several high-profile companies and as a board member at Hasbro, focusing on brand innovation and consumer engagement to drive business transformation.

- Fadi Hanna's Risk Management: As Chief Risk Officer at Bloomberg, Hanna oversees global risk management and previously served as Managing Director of Compliance at J.P. Morgan, providing critical risk oversight and governance support for Grindr's Board.

See More

Nvidia Earnings Week Approaches, Market Anticipates Key Insights

- Nvidia Earnings Expectations: Nvidia is set to report its Q1 earnings on Wednesday, with revenue anticipated at $78.67 billion and EPS of $1.76, as analysts look for results that exceed expectations to boost stock prices and alleviate concerns about a slowing investment cycle.

- Home Depot Performance Outlook: Home Depot is expected to see only 0.8% same-store sales growth in Q1, as rising mortgage rates and a challenging economic backdrop lead analysts to predict its full-year guidance will remain flat to 2%, reflecting low market expectations for its performance.

- TJX Companies Performance: TJX anticipates a 4.1% same-store sales growth in Q1, benefiting from consumer demand for quality merchandise at affordable prices, although rising freight costs may impact margins; nonetheless, the company is viewed as a solid long-term investment.

- Google Developer Conference: Google will host its annual developer conference on Tuesday and Wednesday, with analysts warning that a lack of a

See More

Ross Stores and TJX Companies Earnings Outlook

- Earnings Reporting Outlook: Ross Stores and TJX Companies are set to report quarterly results on Wednesday and Thursday, respectively, with analysts expecting both to showcase strong earnings momentum, particularly against a backdrop of overall positive retail performance.

- Upward Earnings Revisions: According to FactSet data, both companies have seen their earnings estimates revised up by over 10% in the past three to six months, indicating increased market confidence in their future performance, which could drive stock price increases.

- Divergent Stock Performance: While TJX Companies has seen a 4% decline in 2026, Ross Stores has experienced an 18% increase, reflecting differing market expectations and shifts in investor sentiment towards the two stocks.

- Analyst Rating Support: Deutsche Bank reiterated its buy ratings on both stocks ahead of their earnings reports, with analyst Krisztina Katai noting that Ross Stores' same-store sales momentum continues to exceed expectations, while TJX's business model is well-positioned to maintain competitive advantages.

See More

Can the AI Rally Sustain Amid Inflation Fears?

- Market Performance Review: The S&P 500 has surged approximately 19% since its March low, surpassing 7,500 for the first time this week, reflecting a revival in enthusiasm for artificial intelligence, yet the absence of cyclical sectors raises concerns.

- Internal and External Pressures: Despite a 3% rise in the S&P 500 this month, it remains nearly flat on an equal-weight basis, with the financial sector being the worst performer year-to-date, down over 6%, indicating potential impacts of high inflation on the economy.

- Nvidia Earnings Outlook: Nvidia is set to report earnings, with high expectations that CEO Jensen Huang will once again deliver a beat, although its market cap nearing $6 trillion marks a historic high, its valuation appears relatively attractive compared to peers.

- Retail Market Dynamics: Retailers like Walmart and Target are about to release earnings, and the low consumer sentiment may affect sales performance, particularly for lower-income consumers under pressure from rising oil prices, with Walmart's low-price strategy potentially giving it a competitive edge.

See More

Mattel Responds to Activist Investor's Sale Proposal

- Ongoing Shareholder Communication: Mattel (MAT) emphasized its commitment to ongoing communication with shareholders, valuing their perspectives and appreciating Southeastern Asset Management's continued engagement, indicating the company's attentiveness to shareholder opinions.

- Commitment to Strategic Review: The Mattel board and management team are dedicated to regularly reviewing the company's strategy, performance, and opportunities to enhance long-term value, demonstrating a proactive approach to shareholder interests and future growth.

- Positive Analyst Outlook: Jefferies analyst Kylie Cohu noted that while Mattel faces pressure from activist investors, no immediate changes are expected, suggesting that activism may cap downside risks and revive optionality, maintaining a Buy rating on Mattel.

- Slight Stock Increase: Shares of Mattel (MAT) rose 1.3% in premarket trading, despite a 24% decline year-to-date, reflecting cautious optimism in the market regarding the company's future potential.

See More

Investor Calls for Mattel to Explore Buyout Options

- Investor Push for Privatization: Southeastern Asset Management, holding about 4% or $170 million of Mattel's stock, has urged CEO Ynon Kreiz to consider taking the company private or a buyout by Hasbro in light of weak demand.

- Poor Financial Performance: Mattel reported a larger adjusted operating loss of $70 million for the three months ending in March, up from $8 million a year ago, despite exceeding quarterly sales expectations, highlighting challenges in its transformation efforts.

- Potential for Industry Consolidation: Southeastern emphasized that synergies between Mattel and Hasbro could be significant, arguing that Hasbro's superior execution in digital growth gives it a competitive edge, making a merger more necessary.

- Focus on Strategic Execution: Mattel stated it will continue to focus on its IP-driven strategy, even as it faces challenges from supply chain bottlenecks and declining demand for traditional toys, with the board regularly reviewing strategic opportunities to enhance long-term value.

See More

Grindr Nominates New Board Members for 2026

- Board Member Nominations: Grindr has announced the nomination of Rob Solomon, Lisa Gersh, and Fadi Hanna for election at the Annual Meeting of Shareholders on June 2, 2026, aiming to enhance the Board's strategic and governance capabilities to support the company's next phase of growth.

- Rob Solomon's Background: As CEO of H55, Solomon has extensive experience in electric aviation and previously led GoFundMe and Groupon, overseeing billions in donations and demonstrating exceptional operational and growth capabilities.

- Lisa Gersh's Contributions: Gersh brings deep expertise in consumer brands and media, having served as CEO for several high-profile companies and as a board member at Hasbro, focusing on brand innovation and consumer engagement to drive business transformation.

- Fadi Hanna's Risk Management: As Chief Risk Officer at Bloomberg, Hanna oversees global risk management and previously served as Managing Director of Compliance at J.P. Morgan, providing critical risk oversight and governance support for Grindr's Board.

See More