Alphabet's AI Growth May Outpace SpaceX's IPO Impact

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 3 days ago

0mins

Should l Buy GOOGL?

Source: NASDAQ.COM

- SpaceX IPO Impact: The anticipated SpaceX IPO later this year could become one of the largest stock market events ever, and if it achieves a $1.75 trillion market cap, Alphabet stands to gain over $100 billion, significantly enhancing its liquidity.

- AI Technology Edge: Alphabet's generative AI model, Gemini, has become the most widely used AI tool, and its integration with the Google Search platform positions it as the primary means of daily AI interaction, thereby boosting the company's competitive advantage in the AI sector.

- Cloud Computing Growth: Google Cloud's revenue surged 63% year-over-year in Q1, partly due to its sales of custom AI chips, known as TPUs, establishing a strong foothold in both cloud services and chip sales, two of the hottest growth sectors in the economy.

- Capital Restructuring Potential: Should Alphabet sell some of its SpaceX shares post-IPO, it would unlock substantial capital for reinvestment in AI infrastructure, further solidifying its leadership position in the tech industry.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy GOOGL?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on GOOGL

Wall Street analysts forecast GOOGL stock price to fall

33 Analyst Rating

26 Buy

7 Hold

0 Sell

Strong Buy

Current: 388.640

Low

305.00

Averages

374.25

High

400.00

Current: 388.640

Low

305.00

Averages

374.25

High

400.00

About GOOGL

Alphabet Inc. is a holding company. The Company's segments include Google Services, Google Cloud, and Other Bets. The Google Services segment includes products and services such as ads, Android, Chrome, devices, Google Maps, Google Play, Search, and YouTube. The Google Cloud segment includes infrastructure and platform services, collaboration tools, and other services for enterprise customers. Its Other Bets segment is engaged in the sale of healthcare-related services and Internet services. Its Google Cloud provides enterprise-ready cloud services, including Google Cloud Platform and Google Workspace. Google Cloud Platform provides access to solutions such as artificial intelligence (AI) offerings, including its AI infrastructure, Vertex AI platform, and Gemini for Google Cloud; cybersecurity, and data and analytics. Google Workspace includes cloud-based communication and collaboration tools for enterprises, such as Calendar, Gmail, Docs, Drive, and Meet.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Life360 Sees Significant User Growth and Surge in Ad Revenue

- Strong User Growth: Life360's monthly active users reached 97.8 million, marking a 17% year-over-year increase, indicating sustained market demand in the family safety and connection app sector, thereby enhancing the company's competitive position in a crowded market.

- Surge in Paying Users: In Q1 2026, Life360 added 201,000 Paying Circles, bringing the total to 3 million premium accounts, a 27% increase year-over-year, which means that paying user revenue now accounts for 75% of total revenue, showcasing the success of its business model.

- Significant Ad Revenue Growth: The platform generated $19.7 million in ad revenue in Q1, nearly 14% of total revenue, and more than quadrupled year-over-year, indicating that Life360's investment in advertising is starting to pay off, especially after acquiring Nativo to leverage AI for better ad integration.

- Guidance Upgrade: Life360 raised its revenue and adjusted EBITDA guidance for 2026 to a growth forecast of 33% to 40%, despite facing challenges with narrowing margins and declining net income, the robust growth in its core and advertising businesses lays a solid foundation for future development.

See More

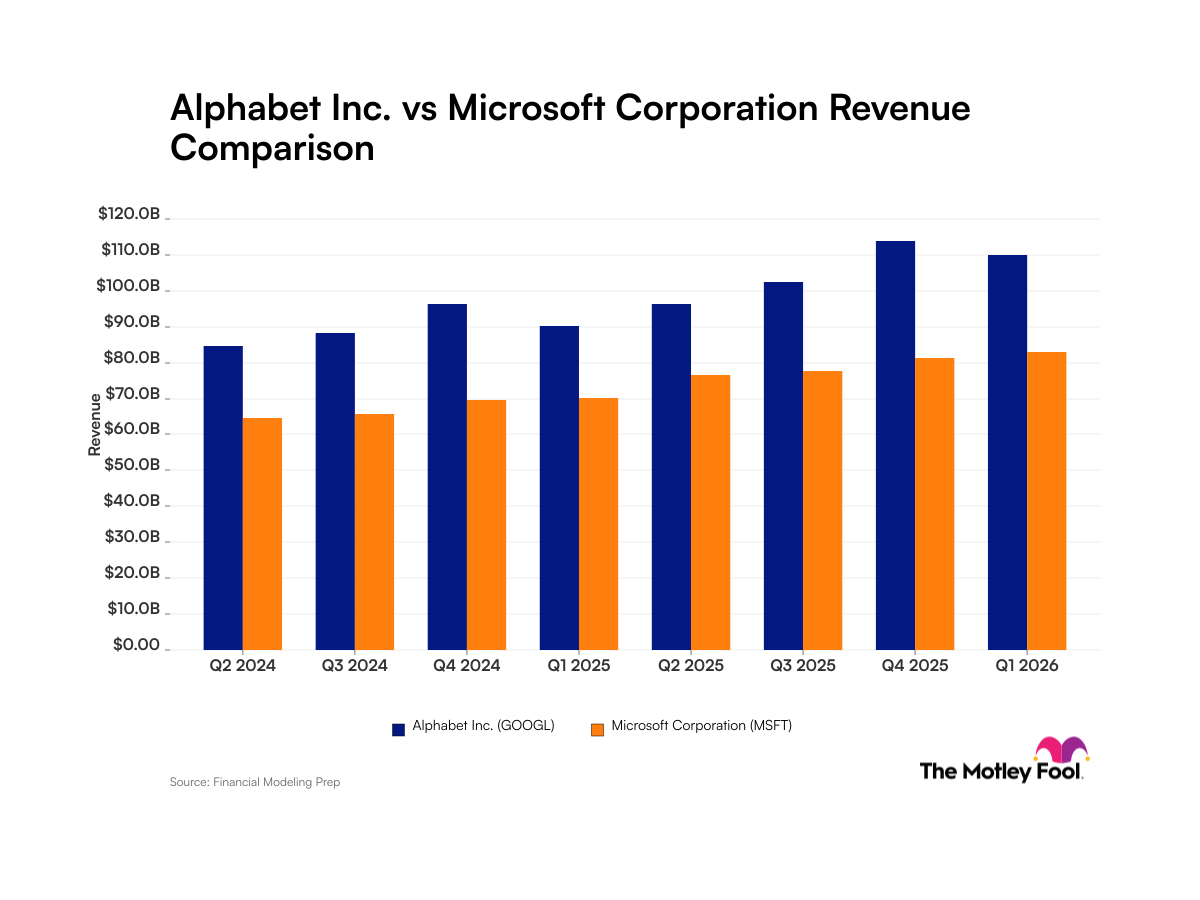

Alphabet and Microsoft Show Consistent Revenue Growth

- Alphabet Revenue Growth: In Q1 2026, Alphabet reported $109.9 billion in revenue, with Google search contributing $60.4 billion, showcasing its dominance in the digital advertising market and reinforcing its competitive edge in the tech industry.

- Microsoft Cloud Progress: Microsoft achieved $82.9 billion in revenue in Q1 2026, with cloud computing operations being crucial for future growth; despite being second in the global cloud sector, it must enhance AI investments to maintain competitiveness.

- AI Investment: Both companies are heavily investing in AI, with Microsoft partnering with OpenAI while Alphabet integrates AI into Google services, indicating that AI will be a significant driver for future business expansion.

- Market Share Comparison: Alphabet's Google search engine holds a 90% market share compared to Microsoft's Bing at 5%, reflecting not only the disparity in advertising revenue but also influencing investor expectations regarding future growth potential.

See More

Alibaba Stock Declines Despite Citi's 'China's Google' Cloud Unit Label

- Stock Price Decline: Despite Citi labeling Alibaba's cloud division as 'China's Google,' the stock has slipped, indicating traders are de-risking ahead of the May 13 earnings report, which could negatively impact short-term market performance.

- AI Growth Potential: The 1:1 CPU-to-GPU ratio in Alibaba's cloud computing is seen as a key driver for AI growth, with this configuration expected to enhance computational efficiency and accelerate AI application development, thereby strengthening the company's competitive position.

- Market Expectation Adjustment: Investors are adopting a cautious stance regarding Alibaba's future performance ahead of the earnings release, likely due to uncertainties in the overall economic environment and concerns about the return on investment in the cloud computing sector, leading to downward pressure on the stock price.

- Intensifying Industry Competition: As Alibaba's cloud business rapidly evolves, competition in the AI and cloud services sectors is intensifying, which may affect the company's market share and profitability, prompting investors to reassess their investment strategies.

See More

Nvidia vs Alphabet: The Race to $10 Trillion Valuation

- Nvidia's Market Leadership: With a market cap of $5.2 trillion, Nvidia is the world's largest company, dominating the AI development space with its data center GPUs, where demand continues to grow rapidly, significantly outpacing supply and indicating strong market demand and future growth potential.

- New Platform Launch: Nvidia is set to launch its Vera Rubin platform in the second half of the year, allowing customers to train AI models with 75% fewer GPUs, which is expected to reduce AI inference costs by 90%, thereby driving wider software adoption and increasing chip demand.

- Google Search Revenue Growth: Google achieved a record $60.4 billion in search revenue in Q1 2023, a 19% year-over-year increase, marking the fourth consecutive quarter of accelerating growth, demonstrating its strong performance and adaptability in the AI era.

- Google TPU Competitiveness: Google unveiled its eighth-generation Tensor Processing Unit, which offers three times the performance for AI training and 80% better performance-per-dollar for inference, showcasing its competitiveness in AI hardware, although its market cap still needs significant growth to catch up with Nvidia.

See More

Wall Street's Growing Divide on Tech Stocks

- Diverging Market Sentiment: Wall Street is sharply divided on tech stocks, with bears arguing that the market is overheating akin to 1999, while bulls see it as a buying opportunity, highlighting a profound disagreement on future market direction.

- Semiconductor Sector Overbought: The Philadelphia Semiconductor Index's overbought condition mirrors only two previous instances in 2000 and 1995, indicating significant adjustment risks ahead, particularly against the backdrop of soaring tech valuations.

- S&P 500 Performance Analysis: Despite the S&P 500 reaching new highs recently, over 60% of its stocks remain below their 50-day and 200-day moving averages, a phenomenon historically associated with market tops, suggesting potential bubble risks in the current environment.

- Investor Caution Signals: Notable investor Michael Burry warns of clear bubble signs in the current market, advising caution towards stocks that have surged dramatically, reflecting concerns about future market trajectories.

See More

ByteDance Challenges EU 'Gatekeeper' Status in Court

- Legal Challenge Context: ByteDance's TikTok was designated a 'gatekeeper' under the EU's Digital Markets Act (DMA) in September 2023, requiring it to adhere to stricter regulatory standards aimed at curbing Big Tech's power.

- Market Impact Analysis: TikTok's lawyer argued that 70%-80% of users engage with multiple platforms, such as Meta's Facebook and Instagram, indicating that users are not locked into TikTok's ecosystem, which may undermine its gatekeeper status.

- Stringent Regulatory Requirements: The DMA imposes onerous criteria for gatekeeper companies, with potential fines reaching up to 10% of annual turnover for violations, posing significant operational challenges for TikTok.

- Future Ruling Implications: The EU Court is expected to rule in the coming months, and this case not only affects TikTok's operational model but also has implications for other companies like Meta contesting their gatekeeper status, potentially reshaping the competitive landscape in Europe.

See More

Life360 Sees Significant User Growth and Surge in Ad Revenue

- Strong User Growth: Life360's monthly active users reached 97.8 million, marking a 17% year-over-year increase, indicating sustained market demand in the family safety and connection app sector, thereby enhancing the company's competitive position in a crowded market.

- Surge in Paying Users: In Q1 2026, Life360 added 201,000 Paying Circles, bringing the total to 3 million premium accounts, a 27% increase year-over-year, which means that paying user revenue now accounts for 75% of total revenue, showcasing the success of its business model.

- Significant Ad Revenue Growth: The platform generated $19.7 million in ad revenue in Q1, nearly 14% of total revenue, and more than quadrupled year-over-year, indicating that Life360's investment in advertising is starting to pay off, especially after acquiring Nativo to leverage AI for better ad integration.

- Guidance Upgrade: Life360 raised its revenue and adjusted EBITDA guidance for 2026 to a growth forecast of 33% to 40%, despite facing challenges with narrowing margins and declining net income, the robust growth in its core and advertising businesses lays a solid foundation for future development.

See More

Alphabet and Microsoft Show Consistent Revenue Growth

- Alphabet Revenue Growth: In Q1 2026, Alphabet reported $109.9 billion in revenue, with Google search contributing $60.4 billion, showcasing its dominance in the digital advertising market and reinforcing its competitive edge in the tech industry.

- Microsoft Cloud Progress: Microsoft achieved $82.9 billion in revenue in Q1 2026, with cloud computing operations being crucial for future growth; despite being second in the global cloud sector, it must enhance AI investments to maintain competitiveness.

- AI Investment: Both companies are heavily investing in AI, with Microsoft partnering with OpenAI while Alphabet integrates AI into Google services, indicating that AI will be a significant driver for future business expansion.

- Market Share Comparison: Alphabet's Google search engine holds a 90% market share compared to Microsoft's Bing at 5%, reflecting not only the disparity in advertising revenue but also influencing investor expectations regarding future growth potential.

See More

Alibaba Stock Declines Despite Citi's 'China's Google' Cloud Unit Label

- Stock Price Decline: Despite Citi labeling Alibaba's cloud division as 'China's Google,' the stock has slipped, indicating traders are de-risking ahead of the May 13 earnings report, which could negatively impact short-term market performance.

- AI Growth Potential: The 1:1 CPU-to-GPU ratio in Alibaba's cloud computing is seen as a key driver for AI growth, with this configuration expected to enhance computational efficiency and accelerate AI application development, thereby strengthening the company's competitive position.

- Market Expectation Adjustment: Investors are adopting a cautious stance regarding Alibaba's future performance ahead of the earnings release, likely due to uncertainties in the overall economic environment and concerns about the return on investment in the cloud computing sector, leading to downward pressure on the stock price.

- Intensifying Industry Competition: As Alibaba's cloud business rapidly evolves, competition in the AI and cloud services sectors is intensifying, which may affect the company's market share and profitability, prompting investors to reassess their investment strategies.

See More

Nvidia vs Alphabet: The Race to $10 Trillion Valuation

- Nvidia's Market Leadership: With a market cap of $5.2 trillion, Nvidia is the world's largest company, dominating the AI development space with its data center GPUs, where demand continues to grow rapidly, significantly outpacing supply and indicating strong market demand and future growth potential.

- New Platform Launch: Nvidia is set to launch its Vera Rubin platform in the second half of the year, allowing customers to train AI models with 75% fewer GPUs, which is expected to reduce AI inference costs by 90%, thereby driving wider software adoption and increasing chip demand.

- Google Search Revenue Growth: Google achieved a record $60.4 billion in search revenue in Q1 2023, a 19% year-over-year increase, marking the fourth consecutive quarter of accelerating growth, demonstrating its strong performance and adaptability in the AI era.

- Google TPU Competitiveness: Google unveiled its eighth-generation Tensor Processing Unit, which offers three times the performance for AI training and 80% better performance-per-dollar for inference, showcasing its competitiveness in AI hardware, although its market cap still needs significant growth to catch up with Nvidia.

See More

Wall Street's Growing Divide on Tech Stocks

- Diverging Market Sentiment: Wall Street is sharply divided on tech stocks, with bears arguing that the market is overheating akin to 1999, while bulls see it as a buying opportunity, highlighting a profound disagreement on future market direction.

- Semiconductor Sector Overbought: The Philadelphia Semiconductor Index's overbought condition mirrors only two previous instances in 2000 and 1995, indicating significant adjustment risks ahead, particularly against the backdrop of soaring tech valuations.

- S&P 500 Performance Analysis: Despite the S&P 500 reaching new highs recently, over 60% of its stocks remain below their 50-day and 200-day moving averages, a phenomenon historically associated with market tops, suggesting potential bubble risks in the current environment.

- Investor Caution Signals: Notable investor Michael Burry warns of clear bubble signs in the current market, advising caution towards stocks that have surged dramatically, reflecting concerns about future market trajectories.

See More

ByteDance Challenges EU 'Gatekeeper' Status in Court

- Legal Challenge Context: ByteDance's TikTok was designated a 'gatekeeper' under the EU's Digital Markets Act (DMA) in September 2023, requiring it to adhere to stricter regulatory standards aimed at curbing Big Tech's power.

- Market Impact Analysis: TikTok's lawyer argued that 70%-80% of users engage with multiple platforms, such as Meta's Facebook and Instagram, indicating that users are not locked into TikTok's ecosystem, which may undermine its gatekeeper status.

- Stringent Regulatory Requirements: The DMA imposes onerous criteria for gatekeeper companies, with potential fines reaching up to 10% of annual turnover for violations, posing significant operational challenges for TikTok.

- Future Ruling Implications: The EU Court is expected to rule in the coming months, and this case not only affects TikTok's operational model but also has implications for other companies like Meta contesting their gatekeeper status, potentially reshaping the competitive landscape in Europe.

See More