Union Pacific Q1 Earnings Beat Expectations

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 1 hour ago

0mins

Should l Buy UNP?

Source: seekingalpha

- Earnings Performance: Union Pacific reported a Q1 non-GAAP EPS of $2.93, beating expectations by $0.07, indicating robust profitability despite slightly missing overall revenue targets.

- Slow Revenue Growth: The Q1 revenue of $6.22 billion grew 3.2% year-over-year but fell short of expectations, primarily due to a 1% decrease in carloads and lower other revenue, reflecting soft market demand.

- Operational Efficiency Improvement: The operating ratio stood at 60.5%, with an adjusted operating ratio of 59.9%, demonstrating ongoing enhancements in cost control and operational efficiency, further solidifying its industry-leading position.

- Optimistic Future Outlook: The company affirmed its 2026 outlook, expecting to meet customer demand with strong service despite a muted economic forecast, and aims for a mid-single-digit EPS growth to achieve a high-single to low-double digit CAGR by 2027, showcasing confidence in future performance.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy UNP?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on UNP

Wall Street analysts forecast UNP stock price to rise

15 Analyst Rating

9 Buy

6 Hold

0 Sell

Moderate Buy

Current: 251.250

Low

245.00

Averages

265.27

High

289.00

Current: 251.250

Low

245.00

Averages

265.27

High

289.00

About UNP

Union Pacific Corporation, through its principal operating company, Union Pacific Railroad Company, connects over 23 states in the western two-thirds of the country by rail, providing a critical link in the global supply chain. It maintains coordinated schedules with other rail carriers to move freight to and from the Atlantic Coast, the Pacific Coast, the Southeast, the Southwest, Canada, and Mexico. The railroad’s diversified business mix includes bulk, industrial, and premium. Its Bulk shipments consist of grain and grain products, fertilizer, food and refrigerated, and coal and renewables. The Industrial shipments consist of several categories, including construction, industrial chemicals, plastics, forest products, specialized products (primarily waste, salt, and roofing), metals and ores, petroleum, liquid petroleum gases (LPG), soda ash, and sand. Its Premium shipments include finished automobiles, automotive parts, and merchandise in intermodal containers.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Union Pacific Set to Announce Q1 Earnings on April 23

- Earnings Announcement: Union Pacific is set to release its Q1 2023 earnings report on April 23 before the market opens, with Wall Street expecting an EPS of $2.86 and revenue of $6.23 billion, reflecting a 3.3% year-over-year increase.

- Performance Review: In Q4 2022, Union Pacific reported mixed results, missing both revenue and EPS estimates while beating operating ratio expectations, indicating ongoing operational challenges.

- Future Guidance: The company anticipates mid-single-digit EPS growth for FY26; however, it faces near-term headwinds from soaring fuel costs and delayed surcharge offsets, raising concerns among analysts.

- Market Reaction: Since the beginning of the year, Union Pacific shares have risen nearly 10%, outperforming the S&P 500's 3% increase, reflecting market confidence in its future performance, despite analysts maintaining a neutral rating.

See More

Union Pacific Reports 6.3% Profit Increase in Q1

- Profit Growth: Union Pacific's Q1 earnings per share increased from $2.70 to $2.87, reflecting a 6.3% rise, driven by strong core pricing performance despite higher operating costs.

- Effective Pricing Strategy: The company's successful core pricing strategy has effectively offset rising operating costs, demonstrating its pricing power and competitive advantage in the market, thereby enhancing financial stability.

- Operating Cost Challenges: Despite the profit increase, the company faces ongoing challenges from rising operating costs, which may impact future profit margins and prompt management to implement more effective cost control measures.

- Optimistic Market Outlook: With economic recovery and increasing transportation demand, Union Pacific's performance growth provides a solid foundation for future investments and expansion, expected to further enhance market share and profitability.

See More

Union Pacific Corporation Reports Strong Q1 2026 Earnings Highlights

- Net Income Growth: Union Pacific Corporation reported a net income of $1.7 billion for Q1 2026, translating to $2.87 per diluted share, reflecting a 5% increase compared to Q1 2025, showcasing the company's robust performance and enhanced profitability in the market.

- Operating Ratio Improvement: The reported operating ratio stood at 60.5%, an improvement of 20 basis points year-over-year, while the adjusted operating ratio was 59.9%, improving by 80 basis points, indicating significant progress in cost control and operational efficiency.

- Freight Revenue Increase: Freight revenue rose by 4% to $5.893 billion, primarily driven by core pricing gains and increased fuel surcharge revenue, despite a 1% decline in carloads, demonstrating the company's ability to optimize its business mix for revenue growth.

- Productivity Enhancements: Freight car velocity averaged 235 daily miles, a 9% increase from last year, while average terminal dwell time decreased to 19.7 hours, an 11% improvement, enhancing service efficiency and laying a solid foundation for future business growth.

See More

Union Pacific Q1 Earnings Beat Expectations

- Earnings Performance: Union Pacific reported a Q1 non-GAAP EPS of $2.93, beating expectations by $0.07, indicating robust profitability despite slightly missing overall revenue targets.

- Slow Revenue Growth: The Q1 revenue of $6.22 billion grew 3.2% year-over-year but fell short of expectations, primarily due to a 1% decrease in carloads and lower other revenue, reflecting soft market demand.

- Operational Efficiency Improvement: The operating ratio stood at 60.5%, with an adjusted operating ratio of 59.9%, demonstrating ongoing enhancements in cost control and operational efficiency, further solidifying its industry-leading position.

- Optimistic Future Outlook: The company affirmed its 2026 outlook, expecting to meet customer demand with strong service despite a muted economic forecast, and aims for a mid-single-digit EPS growth to achieve a high-single to low-double digit CAGR by 2027, showcasing confidence in future performance.

See More

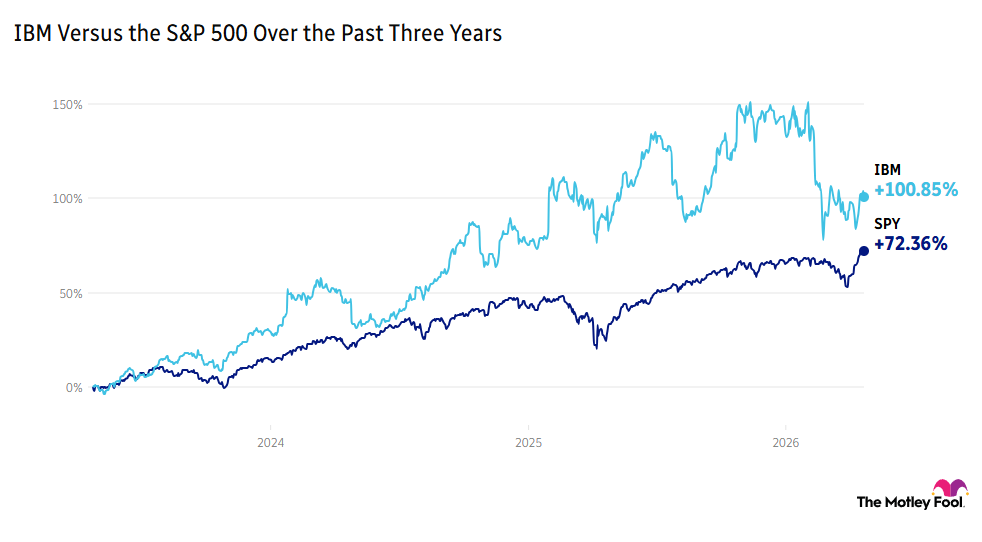

IBM Shares Drop Amid Inflation and Geopolitical Concerns

- Strong Earnings but Cautious Outlook: IBM's quarterly results exceeded revenue and earnings expectations; however, the stock fell over 7% pre-market due to cautious full-year guidance, with CEO Arvind Krishna attributing this to broader geopolitical uncertainties, indicating market concerns about future performance.

- Inflation's Impact on Client Spending: Krishna highlighted that inflation could lead to reduced consumer spending at clients like Walmart, indirectly affecting IBM's business activity, reflecting the potential threats economic conditions pose to tech companies.

- Dual Impact of AI Tools: IBM's consulting business faces threats from more sophisticated AI tools, although TMF's CIO Andy Cross noted that mainframes remain essential infrastructure for complex computing systems, suggesting that AI's impact on the industry is multifaceted.

- Long-term Performance vs. Market Comparison: While IBM has risen 85% over the past five years, outperforming the S&P 500's 70% increase, the stock is down 15% this year, including its worst single-day drop in over 25 years, indicating that advancements in AI may be fundamentally altering the investment case.

See More

Union Pacific Railroad's Positive Outlook Amid Merger Speculation

- Strong Sector Performance: Over the past three years, the Industrial Select Sector SPDR ETF has achieved total returns of 80.33%, surpassing the S&P 500, indicating robust sector performance despite a low dividend yield of 1.18%, which is below the market average.

- Attractive High Dividend: Union Pacific Railroad (UNP) boasts a dividend yield of 2.18%, making it a high-yield stock relative to the industrial sector and broader market, thus attracting income-focused investors.

- Merger Potential: The merger with rival Norfolk Southern could yield an additional $2.75 billion in EBITDA, with projected free cash flow surging from $7.3 billion to $12 billion by 2029, highlighting the strategic value of the merger.

- Robust Dividend History: Union Pacific has paid dividends for 126 consecutive years and has increased its payout for 19 years, demonstrating stability and appeal in a capital-intensive industry, especially in the context of a potential merger.

See More

Union Pacific Set to Announce Q1 Earnings on April 23

- Earnings Announcement: Union Pacific is set to release its Q1 2023 earnings report on April 23 before the market opens, with Wall Street expecting an EPS of $2.86 and revenue of $6.23 billion, reflecting a 3.3% year-over-year increase.

- Performance Review: In Q4 2022, Union Pacific reported mixed results, missing both revenue and EPS estimates while beating operating ratio expectations, indicating ongoing operational challenges.

- Future Guidance: The company anticipates mid-single-digit EPS growth for FY26; however, it faces near-term headwinds from soaring fuel costs and delayed surcharge offsets, raising concerns among analysts.

- Market Reaction: Since the beginning of the year, Union Pacific shares have risen nearly 10%, outperforming the S&P 500's 3% increase, reflecting market confidence in its future performance, despite analysts maintaining a neutral rating.

See More

Union Pacific Reports 6.3% Profit Increase in Q1

- Profit Growth: Union Pacific's Q1 earnings per share increased from $2.70 to $2.87, reflecting a 6.3% rise, driven by strong core pricing performance despite higher operating costs.

- Effective Pricing Strategy: The company's successful core pricing strategy has effectively offset rising operating costs, demonstrating its pricing power and competitive advantage in the market, thereby enhancing financial stability.

- Operating Cost Challenges: Despite the profit increase, the company faces ongoing challenges from rising operating costs, which may impact future profit margins and prompt management to implement more effective cost control measures.

- Optimistic Market Outlook: With economic recovery and increasing transportation demand, Union Pacific's performance growth provides a solid foundation for future investments and expansion, expected to further enhance market share and profitability.

See More

Union Pacific Corporation Reports Strong Q1 2026 Earnings Highlights

- Net Income Growth: Union Pacific Corporation reported a net income of $1.7 billion for Q1 2026, translating to $2.87 per diluted share, reflecting a 5% increase compared to Q1 2025, showcasing the company's robust performance and enhanced profitability in the market.

- Operating Ratio Improvement: The reported operating ratio stood at 60.5%, an improvement of 20 basis points year-over-year, while the adjusted operating ratio was 59.9%, improving by 80 basis points, indicating significant progress in cost control and operational efficiency.

- Freight Revenue Increase: Freight revenue rose by 4% to $5.893 billion, primarily driven by core pricing gains and increased fuel surcharge revenue, despite a 1% decline in carloads, demonstrating the company's ability to optimize its business mix for revenue growth.

- Productivity Enhancements: Freight car velocity averaged 235 daily miles, a 9% increase from last year, while average terminal dwell time decreased to 19.7 hours, an 11% improvement, enhancing service efficiency and laying a solid foundation for future business growth.

See More

Union Pacific Q1 Earnings Beat Expectations

- Earnings Performance: Union Pacific reported a Q1 non-GAAP EPS of $2.93, beating expectations by $0.07, indicating robust profitability despite slightly missing overall revenue targets.

- Slow Revenue Growth: The Q1 revenue of $6.22 billion grew 3.2% year-over-year but fell short of expectations, primarily due to a 1% decrease in carloads and lower other revenue, reflecting soft market demand.

- Operational Efficiency Improvement: The operating ratio stood at 60.5%, with an adjusted operating ratio of 59.9%, demonstrating ongoing enhancements in cost control and operational efficiency, further solidifying its industry-leading position.

- Optimistic Future Outlook: The company affirmed its 2026 outlook, expecting to meet customer demand with strong service despite a muted economic forecast, and aims for a mid-single-digit EPS growth to achieve a high-single to low-double digit CAGR by 2027, showcasing confidence in future performance.

See More

IBM Shares Drop Amid Inflation and Geopolitical Concerns

- Strong Earnings but Cautious Outlook: IBM's quarterly results exceeded revenue and earnings expectations; however, the stock fell over 7% pre-market due to cautious full-year guidance, with CEO Arvind Krishna attributing this to broader geopolitical uncertainties, indicating market concerns about future performance.

- Inflation's Impact on Client Spending: Krishna highlighted that inflation could lead to reduced consumer spending at clients like Walmart, indirectly affecting IBM's business activity, reflecting the potential threats economic conditions pose to tech companies.

- Dual Impact of AI Tools: IBM's consulting business faces threats from more sophisticated AI tools, although TMF's CIO Andy Cross noted that mainframes remain essential infrastructure for complex computing systems, suggesting that AI's impact on the industry is multifaceted.

- Long-term Performance vs. Market Comparison: While IBM has risen 85% over the past five years, outperforming the S&P 500's 70% increase, the stock is down 15% this year, including its worst single-day drop in over 25 years, indicating that advancements in AI may be fundamentally altering the investment case.

See More

Union Pacific Railroad's Positive Outlook Amid Merger Speculation

- Strong Sector Performance: Over the past three years, the Industrial Select Sector SPDR ETF has achieved total returns of 80.33%, surpassing the S&P 500, indicating robust sector performance despite a low dividend yield of 1.18%, which is below the market average.

- Attractive High Dividend: Union Pacific Railroad (UNP) boasts a dividend yield of 2.18%, making it a high-yield stock relative to the industrial sector and broader market, thus attracting income-focused investors.

- Merger Potential: The merger with rival Norfolk Southern could yield an additional $2.75 billion in EBITDA, with projected free cash flow surging from $7.3 billion to $12 billion by 2029, highlighting the strategic value of the merger.

- Robust Dividend History: Union Pacific has paid dividends for 126 consecutive years and has increased its payout for 19 years, demonstrating stability and appeal in a capital-intensive industry, especially in the context of a potential merger.

See More