BKNG Shares Drop to Lowest Point in Over 16 Months as Brokerages Highlight AI-Related Concerns

Stock Performance: Booking Holdings (BKNG) shares have dropped over 8%, reaching their lowest levels since September 2024, despite better-than-expected fourth-quarter results, due to concerns about potential AI disruption.

Revenue Growth: The company reported a 16% increase in fourth-quarter revenue to $6.3 billion, surpassing Street estimates, and projected low double-digit revenue growth for fiscal 2026.

Stock Split Announcement: Booking's board approved a 25-for-1 stock split, effective April 2, which will adjust trading on a split-adjusted basis starting April 6.

Analyst Ratings: Analysts have reduced price targets for Booking, with Cantor Fitzgerald lowering it to $4,495 and Barclays to $5,500, while maintaining neutral or overweight ratings, reflecting concerns about AI developments impacting stock valuation.

Trade with 70% Backtested Accuracy

Analyst Views on BKNG

About BKNG

About the author

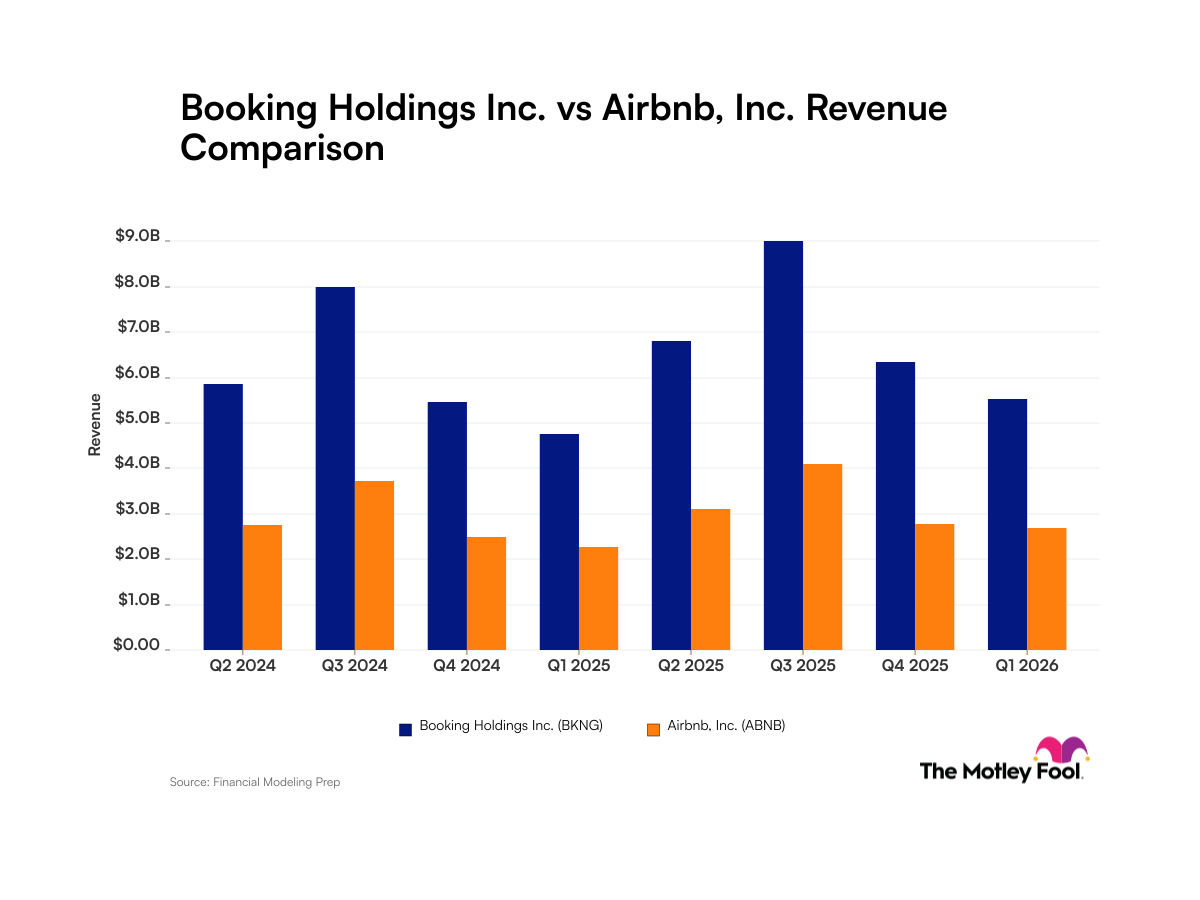

Quarterly Revenue Analysis for Booking and Airbnb

- Quarterly Revenue Performance: Booking reported $5.5 billion in revenue for Q1 2026, reflecting a 16% year-over-year growth, while Airbnb's revenue for the same period was $2.7 billion, showing an 18% increase, indicating both companies are actively expanding in the market.

- Competitive Market Dynamics: Although Booking's revenue significantly exceeds that of Airbnb, the latter's faster growth rate suggests that its efforts to diversify into hotels and additional services may pose a competitive threat to Booking's market share.

- Seasonal Sales Fluctuations: The third quarter typically serves as a peak sales period for both companies, with significant sales boosts during the summer travel season, highlighting the seasonal nature of travel demand.

- Future Outlook and Challenges: Booking forecasts a revenue increase of 4% to 6% year-over-year for Q2, a stark decline from its 16% growth in Q1, primarily due to the impact of conflicts with Iran, which may negatively affect its future performance.

Financial Comparison Between Booking and Airbnb

- Revenue Scale Comparison: Booking consistently generates significantly higher total revenue than Airbnb across all reporting periods, with Booking reporting $5.5 billion in sales for Q1 2026 compared to Airbnb's $2.7 billion, indicating Booking's dominant market position.

- Quarterly Revenue Fluctuations: Both companies experience revenue declines in Q1 but see substantial increases in Q3 due to the summer travel season, with Booking's growth rate at 16% and Airbnb's at 18%, suggesting Airbnb's market expansion strategies are effective.

- Market Challenges and Outlook: Booking's stock fell to a 52-week low of $150.14 on May 20 due to conflicts with Iran, forecasting only a 4% to 6% year-over-year revenue increase for Q2, which is a stark contrast to its Q1 growth, reflecting external pressures on its business.

- Investor Considerations: Despite Booking's larger revenue scale, analysts note it was not included in the “best stocks” list, prompting investors to carefully evaluate its future growth potential, especially in a competitive market landscape.

OpenTable Expands with New Toronto Office Lease

- New Office Opening: OpenTable has signed a multi-year lease at Allied's 134 Peter Street in Downtown Toronto, securing over 24,000 square feet of premium office space, marking a significant milestone in its commitment to the Canadian market and international expansion.

- Team Expansion Plans: The new office is expected to accommodate over 200 employees, with OpenTable actively hiring across engineering, product, marketing, and more to support global product innovation and local operations.

- Tech Talent Utilization: By establishing a new office in Toronto, OpenTable can tap into the city's world-class tech talent pool, thereby driving global product innovation and further solidifying its position in the Canadian restaurant industry.

- Confidence in the Industry: OpenTable's expansion in Toronto is seen as a strong show of confidence in the Canadian restaurant sector, supporting local economies and communities while enhancing service for restaurant operators and diners.

Analysis of Netflix and Booking Stock Splits and Future Prospects

- Netflix Stock Split: Netflix executed a 10-for-1 stock split on November 17, with shares currently trading around $88, reflecting a 25% decline over the past year due to disappointing financial guidance that sharply impacted stock prices, necessitating investor vigilance regarding future market performance.

- Market Potential: Despite challenges, Netflix's penetration in the U.S. streaming market is still below 50%, and the company plans to enhance market share by venturing into live sports and long-form video podcasts, thereby boosting user engagement and revenue growth.

- Booking Stock Split: Booking Holdings conducted a 25-for-1 stock split on April 6, adjusting shares from above $4,000, and while facing potential disruptions from AI, the company sees significant growth opportunities, particularly in the fast-growing Asian travel market.

- Competitive Advantage: Booking Holdings benefits from strong network effects and a diversified service ecosystem that attracts more travelers to its platform, and despite a 25% drop in stock price over the past year, its market position and future growth opportunities still make it an attractive investment.

Analysis of Netflix and Booking Stock Splits

- Netflix Stock Split: Netflix executed a 10-for-1 stock split on November 17, yet this move failed to prevent a 25% decline in its stock price over the past year, currently trading around $88, reflecting investor disappointment following weak financial guidance.

- Market Potential: Despite challenges, Netflix still has a massive addressable market in the U.S. streaming industry, which commands less than 50% of television viewing time, and it aims to capture market share by expanding into live sports and long-form video podcasts.

- Booking Stock Split: Booking Holdings conducted a 25-for-1 stock split on April 6, which was well-received despite CEO Glenn Fogel's previous reluctance to attract investors deterred by high share prices, as shares were trading above $4,000.

- Competitive Edge: Booking Holdings possesses a strong competitive advantage in the global travel market, particularly in Asia, and despite a 25% drop in stock price, the company is leveraging AI tools to enhance service quality, indicating solid performance potential over the next decade.

KAYAK's Summer Travel Report Reveals Key Trends

- Flight Search Growth: KAYAK data indicates a 4% year-over-year increase in flight searches this summer, with domestic travel searches rising by 7%, demonstrating that consumers are eager to travel and seek value despite fluctuating airfare prices.

- Trending Destinations: Santiago de los Caballeros (+29%) and Santo Domingo (+24%) in the Dominican Republic are among the fastest-growing international destinations, while Valparaiso, Florida (+27%) and Asheville, North Carolina (+24%) lead domestic searches, reflecting travelers' preference for closer trips.

- Cost-Saving Opportunities: KAYAK's data reveals that travelers can save up to 9% on domestic flights and approximately 42% on international flights by booking now and traveling between mid-August and early September, highlighting the significant impact of travel timing on budgets.

- Smart Travel Tools: KAYAK offers tools like the Trip Calculator and Price Alerts to help users monitor real-time airfare changes, ensuring they find the best flights within their budget, thereby enhancing traveler confidence and satisfaction.

Quarterly Revenue Analysis for Booking and Airbnb

- Quarterly Revenue Performance: Booking reported $5.5 billion in revenue for Q1 2026, reflecting a 16% year-over-year growth, while Airbnb's revenue for the same period was $2.7 billion, showing an 18% increase, indicating both companies are actively expanding in the market.

- Competitive Market Dynamics: Although Booking's revenue significantly exceeds that of Airbnb, the latter's faster growth rate suggests that its efforts to diversify into hotels and additional services may pose a competitive threat to Booking's market share.

- Seasonal Sales Fluctuations: The third quarter typically serves as a peak sales period for both companies, with significant sales boosts during the summer travel season, highlighting the seasonal nature of travel demand.

- Future Outlook and Challenges: Booking forecasts a revenue increase of 4% to 6% year-over-year for Q2, a stark decline from its 16% growth in Q1, primarily due to the impact of conflicts with Iran, which may negatively affect its future performance.

Financial Comparison Between Booking and Airbnb

- Revenue Scale Comparison: Booking consistently generates significantly higher total revenue than Airbnb across all reporting periods, with Booking reporting $5.5 billion in sales for Q1 2026 compared to Airbnb's $2.7 billion, indicating Booking's dominant market position.

- Quarterly Revenue Fluctuations: Both companies experience revenue declines in Q1 but see substantial increases in Q3 due to the summer travel season, with Booking's growth rate at 16% and Airbnb's at 18%, suggesting Airbnb's market expansion strategies are effective.

- Market Challenges and Outlook: Booking's stock fell to a 52-week low of $150.14 on May 20 due to conflicts with Iran, forecasting only a 4% to 6% year-over-year revenue increase for Q2, which is a stark contrast to its Q1 growth, reflecting external pressures on its business.

- Investor Considerations: Despite Booking's larger revenue scale, analysts note it was not included in the “best stocks” list, prompting investors to carefully evaluate its future growth potential, especially in a competitive market landscape.

OpenTable Expands with New Toronto Office Lease

- New Office Opening: OpenTable has signed a multi-year lease at Allied's 134 Peter Street in Downtown Toronto, securing over 24,000 square feet of premium office space, marking a significant milestone in its commitment to the Canadian market and international expansion.

- Team Expansion Plans: The new office is expected to accommodate over 200 employees, with OpenTable actively hiring across engineering, product, marketing, and more to support global product innovation and local operations.

- Tech Talent Utilization: By establishing a new office in Toronto, OpenTable can tap into the city's world-class tech talent pool, thereby driving global product innovation and further solidifying its position in the Canadian restaurant industry.

- Confidence in the Industry: OpenTable's expansion in Toronto is seen as a strong show of confidence in the Canadian restaurant sector, supporting local economies and communities while enhancing service for restaurant operators and diners.

Analysis of Netflix and Booking Stock Splits and Future Prospects

- Netflix Stock Split: Netflix executed a 10-for-1 stock split on November 17, with shares currently trading around $88, reflecting a 25% decline over the past year due to disappointing financial guidance that sharply impacted stock prices, necessitating investor vigilance regarding future market performance.

- Market Potential: Despite challenges, Netflix's penetration in the U.S. streaming market is still below 50%, and the company plans to enhance market share by venturing into live sports and long-form video podcasts, thereby boosting user engagement and revenue growth.

- Booking Stock Split: Booking Holdings conducted a 25-for-1 stock split on April 6, adjusting shares from above $4,000, and while facing potential disruptions from AI, the company sees significant growth opportunities, particularly in the fast-growing Asian travel market.

- Competitive Advantage: Booking Holdings benefits from strong network effects and a diversified service ecosystem that attracts more travelers to its platform, and despite a 25% drop in stock price over the past year, its market position and future growth opportunities still make it an attractive investment.

Analysis of Netflix and Booking Stock Splits

- Netflix Stock Split: Netflix executed a 10-for-1 stock split on November 17, yet this move failed to prevent a 25% decline in its stock price over the past year, currently trading around $88, reflecting investor disappointment following weak financial guidance.

- Market Potential: Despite challenges, Netflix still has a massive addressable market in the U.S. streaming industry, which commands less than 50% of television viewing time, and it aims to capture market share by expanding into live sports and long-form video podcasts.

- Booking Stock Split: Booking Holdings conducted a 25-for-1 stock split on April 6, which was well-received despite CEO Glenn Fogel's previous reluctance to attract investors deterred by high share prices, as shares were trading above $4,000.

- Competitive Edge: Booking Holdings possesses a strong competitive advantage in the global travel market, particularly in Asia, and despite a 25% drop in stock price, the company is leveraging AI tools to enhance service quality, indicating solid performance potential over the next decade.

KAYAK's Summer Travel Report Reveals Key Trends

- Flight Search Growth: KAYAK data indicates a 4% year-over-year increase in flight searches this summer, with domestic travel searches rising by 7%, demonstrating that consumers are eager to travel and seek value despite fluctuating airfare prices.

- Trending Destinations: Santiago de los Caballeros (+29%) and Santo Domingo (+24%) in the Dominican Republic are among the fastest-growing international destinations, while Valparaiso, Florida (+27%) and Asheville, North Carolina (+24%) lead domestic searches, reflecting travelers' preference for closer trips.

- Cost-Saving Opportunities: KAYAK's data reveals that travelers can save up to 9% on domestic flights and approximately 42% on international flights by booking now and traveling between mid-August and early September, highlighting the significant impact of travel timing on budgets.

- Smart Travel Tools: KAYAK offers tools like the Trip Calculator and Price Alerts to help users monitor real-time airfare changes, ensuring they find the best flights within their budget, thereby enhancing traveler confidence and satisfaction.