Sweetgreen Shares Plunge After Disappointing Earnings Report

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Feb 27 2026

0mins

Source: Fool

- Significant Sales Decline: Sweetgreen reported an 11.5% drop in comparable sales, contrasting sharply with a 4.4% increase a year ago, leading to a 3.5% revenue decline to $155.2 million, which fell short of the $158.8 million expected by analysts, indicating ongoing struggles in a competitive fast-casual market.

- Widening Net Loss: The company's net loss widened from $29 million to $49.7 million, resulting in a per-share loss of $0.42, significantly higher than the anticipated $0.25 loss, reflecting substantial challenges during its transition amidst a tough consumer spending environment.

- Management Response: CEO Jonathan Neman stated that the company is urgently advancing the 'Sweet Growth Transformation Plan' to strengthen its core business, while testing wraps priced at $10.95 in select markets, aiming to enhance customer value and competitiveness through new product offerings.

- Bleak Future Outlook: Sweetgreen forecasts a 2%-4% decline in comparable sales for 2026, with expected restaurant-level profit margins between 14.2%-14.7%, below the 15.2% recorded in 2025, although it anticipates adjusted EBITDA improving from an $11 million loss to a profit of $1 million to $6 million, reflecting a conservative approach to new store openings.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy SG?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on SG

Wall Street analysts forecast SG stock price to fall

14 Analyst Rating

3 Buy

10 Hold

1 Sell

Hold

Current: 8.480

Low

5.00

Averages

7.57

High

10.00

Current: 8.480

Low

5.00

Averages

7.57

High

10.00

About SG

Sweetgreen, Inc. is a restaurant and lifestyle brand that serves healthy food at scale. The Company has designed its menu to be customizable and convenient to empower its customers to make healthier choices for both lunch and dinner. The Company's core menu features approximately 13 signature items which are offered year-round in all of its locations, including its new steak plate. In addition to its core menu items, its single most popular item is the custom salad or bowl, which can include combinations from 40-plus ingredients as well as its made-from-scratch dressings. On its Owned Digital Channels, it offers exclusive menu items, including seasonal digital exclusives and collections relevant to each customer. It has a five-channel model that is designed to help its customers to order. The Company's five-channel model includes Pick-Up, Native Delivery, Outpost and Catering, In-Store, and Marketplace. It has approximately 250 restaurants across the country.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

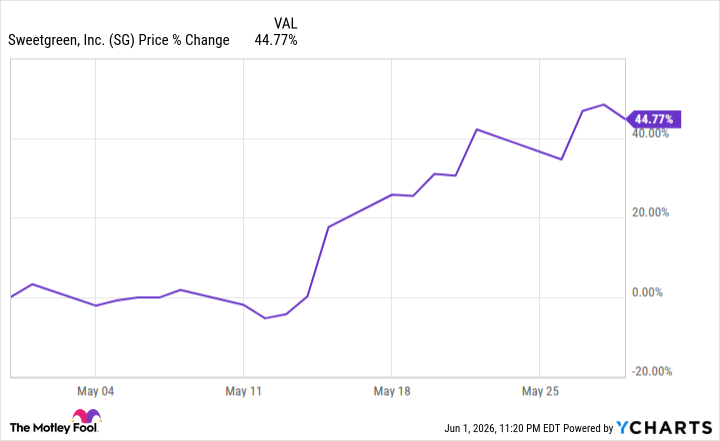

Sweetgreen Stock Surges 45% in May Driven by Wrap Launch and Analyst Upgrade

- Stock Surge: Sweetgreen's stock soared 45% in May, primarily driven by the launch of lower-priced wraps and an analyst upgrade, reflecting market optimism about its future performance.

- Improved Guidance: Despite disappointing first-quarter results, the company expects performance to improve in the second quarter, with comparable sales showing recovery in April, indicating a rebound in market demand.

- Analyst Upgrade: JPMorgan Chase upgraded Sweetgreen to overweight and raised its price target from $8 to $13, reflecting strong market response to the new wraps and potential for free cash flow inflection.

- Executive Appointment: Sweetgreen appointed Cindy Olsen as Chief Strategy Officer to drive the company's transformation, particularly focusing on the strategic rollout of the new wraps, enhancing its competitive position in the market.

See More

Sweetgreen Stock Rebounds with Optimistic Outlook

- Improved Performance Outlook: Sweetgreen's disappointing first-quarter results were overshadowed by guidance indicating expected improvement in the second quarter, with comparable sales showing recovery, which instilled investor confidence and led to a 45% stock price increase.

- New Product Launch: The national rollout of wraps received positive reviews and is priced lower than salads, a strategy that not only attracted more customers but also enhanced brand image, further driving stock price gains.

- Institutional Investor Involvement: Hedge funds like Point72 increased their stakes in Sweetgreen during the first quarter, contributing to a 5% stock rise on May 14 and a subsequent 17% jump, reflecting market confidence in the company's future prospects.

- Executive Appointment: Sweetgreen appointed Cindy Olsen as Chief Strategy Officer to drive the company's transformation, particularly in promoting the new wraps, which could provide new growth momentum for the company.

See More

Sweetgreen Sales Recovery and New Product Launch

- Sales Outlook Improvement: Sweetgreen anticipates an improvement in comparable sales for 2023, with a 12% decline reported in Q1, yet the company expresses optimism for Q2 performance, indicating potential business recovery.

- Positive Product Reception: The national launch of wraps has received favorable feedback and is priced lower than salads, a strategy that not only attracts more customers but also contributed to a 45% stock price increase in April, reflecting market acceptance of the new product.

- Stock Volatility and Investor Confidence: Despite Sweetgreen's stock plummeting over 75% in the past year and a half, it rose 5% on May 14 and another 17% the following day, partly due to hedge funds like Point72 increasing their stakes in Q1, boosting market confidence.

- Executive Appointment and Strategic Shift: Sweetgreen appointed Cindy Olsen as Chief Strategy Officer to drive the company's transformation, particularly in promoting the new wraps, which is expected to bring new growth momentum to the company.

See More

Sweetgreen Stock Rises on Positive Wraps Buzz

- Stock Surge: Sweetgreen's shares rose 9.7% today to $9.98, reflecting market optimism about its newly launched low-priced wraps, despite the absence of major news.

- Product Popularity: Since May 13, Sweetgreen's stock has increased over 50%, primarily due to the national launch of wraps, which may enhance the company's image as consumers recognize their value.

- Management Change: Sweetgreen appointed Cindy Olsen as Chief Strategy Officer yesterday; while the market typically reacts little to such news, this new role could bolster strategic transformation and investor confidence.

- Analyst Rating Upgrade: JPMorgan Chase upgraded Sweetgreen's stock to overweight after meeting with management, citing that the wraps are driving the company's transformation, indicating a positive outlook for future growth.

See More

Starbucks' New CEO Implements Turnaround Strategy

- Personalized Service Enhancement: New CEO Brian Niccol aims to enhance customer experience by writing notes on cups and serving drinks in mugs for in-store customers, thereby reinforcing Starbucks' identity as a 'third place' and boosting customer loyalty and brand image.

- Technology Investment Challenges: The automated inventory management technology that Starbucks invested in has been retired due to frequent miscounts and mislabeling, illustrating that while the intent was positive, the execution fell short, highlighting the need for balance between technology and human service in the restaurant industry.

- Sales Growth Recovery: Under Niccol's 'Back to Starbucks' initiative, comparable sales jumped 6.2% in the most recent quarter, indicating growth across all regions and suggesting that the strategic adjustments are beginning to yield results.

- Human-Centric Business Philosophy: Starbucks' experience underscores that despite the increasing prevalence of technology in the restaurant sector, human-driven service remains crucial for success, with Niccol's strategy emphasizing the importance of enhancing customer service through technology support.

See More

Cava Outpaces Chipotle Growth as Sweetgreen Sales Decline

- Same-Store Sales Growth: Cava leads with a 9.7% same-store sales growth, defying the trend of declining traffic in the restaurant sector, which is expected to enhance its long-term profit potential significantly.

- Profitability Comparison: Cava's restaurant-level operating margin stands at 25.1%, closely trailing Chipotle's 23.7%, indicating that while Chipotle maintains a stronger consolidated margin, Cava's rapid growth positions it favorably for future expansion opportunities.

- Valuation Discrepancy: Cava's price-to-sales ratio of 7.4 significantly exceeds Chipotle's 3.6 and Sweetgreen's 1.6, reflecting investor confidence in Cava's growth potential, making it a more attractive investment despite its higher valuation.

- Market Outlook: With current revenues of $1.3 billion, if Cava can expand to match Chipotle's scale over the next decade, its revenue could soar to $15 billion or more, highlighting its substantial market potential and growth trajectory.

See More

Sweetgreen Stock Surges 45% in May Driven by Wrap Launch and Analyst Upgrade

- Stock Surge: Sweetgreen's stock soared 45% in May, primarily driven by the launch of lower-priced wraps and an analyst upgrade, reflecting market optimism about its future performance.

- Improved Guidance: Despite disappointing first-quarter results, the company expects performance to improve in the second quarter, with comparable sales showing recovery in April, indicating a rebound in market demand.

- Analyst Upgrade: JPMorgan Chase upgraded Sweetgreen to overweight and raised its price target from $8 to $13, reflecting strong market response to the new wraps and potential for free cash flow inflection.

- Executive Appointment: Sweetgreen appointed Cindy Olsen as Chief Strategy Officer to drive the company's transformation, particularly focusing on the strategic rollout of the new wraps, enhancing its competitive position in the market.

See More

Sweetgreen Stock Rebounds with Optimistic Outlook

- Improved Performance Outlook: Sweetgreen's disappointing first-quarter results were overshadowed by guidance indicating expected improvement in the second quarter, with comparable sales showing recovery, which instilled investor confidence and led to a 45% stock price increase.

- New Product Launch: The national rollout of wraps received positive reviews and is priced lower than salads, a strategy that not only attracted more customers but also enhanced brand image, further driving stock price gains.

- Institutional Investor Involvement: Hedge funds like Point72 increased their stakes in Sweetgreen during the first quarter, contributing to a 5% stock rise on May 14 and a subsequent 17% jump, reflecting market confidence in the company's future prospects.

- Executive Appointment: Sweetgreen appointed Cindy Olsen as Chief Strategy Officer to drive the company's transformation, particularly in promoting the new wraps, which could provide new growth momentum for the company.

See More

Sweetgreen Sales Recovery and New Product Launch

- Sales Outlook Improvement: Sweetgreen anticipates an improvement in comparable sales for 2023, with a 12% decline reported in Q1, yet the company expresses optimism for Q2 performance, indicating potential business recovery.

- Positive Product Reception: The national launch of wraps has received favorable feedback and is priced lower than salads, a strategy that not only attracts more customers but also contributed to a 45% stock price increase in April, reflecting market acceptance of the new product.

- Stock Volatility and Investor Confidence: Despite Sweetgreen's stock plummeting over 75% in the past year and a half, it rose 5% on May 14 and another 17% the following day, partly due to hedge funds like Point72 increasing their stakes in Q1, boosting market confidence.

- Executive Appointment and Strategic Shift: Sweetgreen appointed Cindy Olsen as Chief Strategy Officer to drive the company's transformation, particularly in promoting the new wraps, which is expected to bring new growth momentum to the company.

See More

Sweetgreen Stock Rises on Positive Wraps Buzz

- Stock Surge: Sweetgreen's shares rose 9.7% today to $9.98, reflecting market optimism about its newly launched low-priced wraps, despite the absence of major news.

- Product Popularity: Since May 13, Sweetgreen's stock has increased over 50%, primarily due to the national launch of wraps, which may enhance the company's image as consumers recognize their value.

- Management Change: Sweetgreen appointed Cindy Olsen as Chief Strategy Officer yesterday; while the market typically reacts little to such news, this new role could bolster strategic transformation and investor confidence.

- Analyst Rating Upgrade: JPMorgan Chase upgraded Sweetgreen's stock to overweight after meeting with management, citing that the wraps are driving the company's transformation, indicating a positive outlook for future growth.

See More

Starbucks' New CEO Implements Turnaround Strategy

- Personalized Service Enhancement: New CEO Brian Niccol aims to enhance customer experience by writing notes on cups and serving drinks in mugs for in-store customers, thereby reinforcing Starbucks' identity as a 'third place' and boosting customer loyalty and brand image.

- Technology Investment Challenges: The automated inventory management technology that Starbucks invested in has been retired due to frequent miscounts and mislabeling, illustrating that while the intent was positive, the execution fell short, highlighting the need for balance between technology and human service in the restaurant industry.

- Sales Growth Recovery: Under Niccol's 'Back to Starbucks' initiative, comparable sales jumped 6.2% in the most recent quarter, indicating growth across all regions and suggesting that the strategic adjustments are beginning to yield results.

- Human-Centric Business Philosophy: Starbucks' experience underscores that despite the increasing prevalence of technology in the restaurant sector, human-driven service remains crucial for success, with Niccol's strategy emphasizing the importance of enhancing customer service through technology support.

See More

Cava Outpaces Chipotle Growth as Sweetgreen Sales Decline

- Same-Store Sales Growth: Cava leads with a 9.7% same-store sales growth, defying the trend of declining traffic in the restaurant sector, which is expected to enhance its long-term profit potential significantly.

- Profitability Comparison: Cava's restaurant-level operating margin stands at 25.1%, closely trailing Chipotle's 23.7%, indicating that while Chipotle maintains a stronger consolidated margin, Cava's rapid growth positions it favorably for future expansion opportunities.

- Valuation Discrepancy: Cava's price-to-sales ratio of 7.4 significantly exceeds Chipotle's 3.6 and Sweetgreen's 1.6, reflecting investor confidence in Cava's growth potential, making it a more attractive investment despite its higher valuation.

- Market Outlook: With current revenues of $1.3 billion, if Cava can expand to match Chipotle's scale over the next decade, its revenue could soar to $15 billion or more, highlighting its substantial market potential and growth trajectory.

See More