Salesforce vs Adobe Revenue Comparison Analysis

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 1 hour ago

0mins

Should l Buy ADBE?

Source: NASDAQ.COM

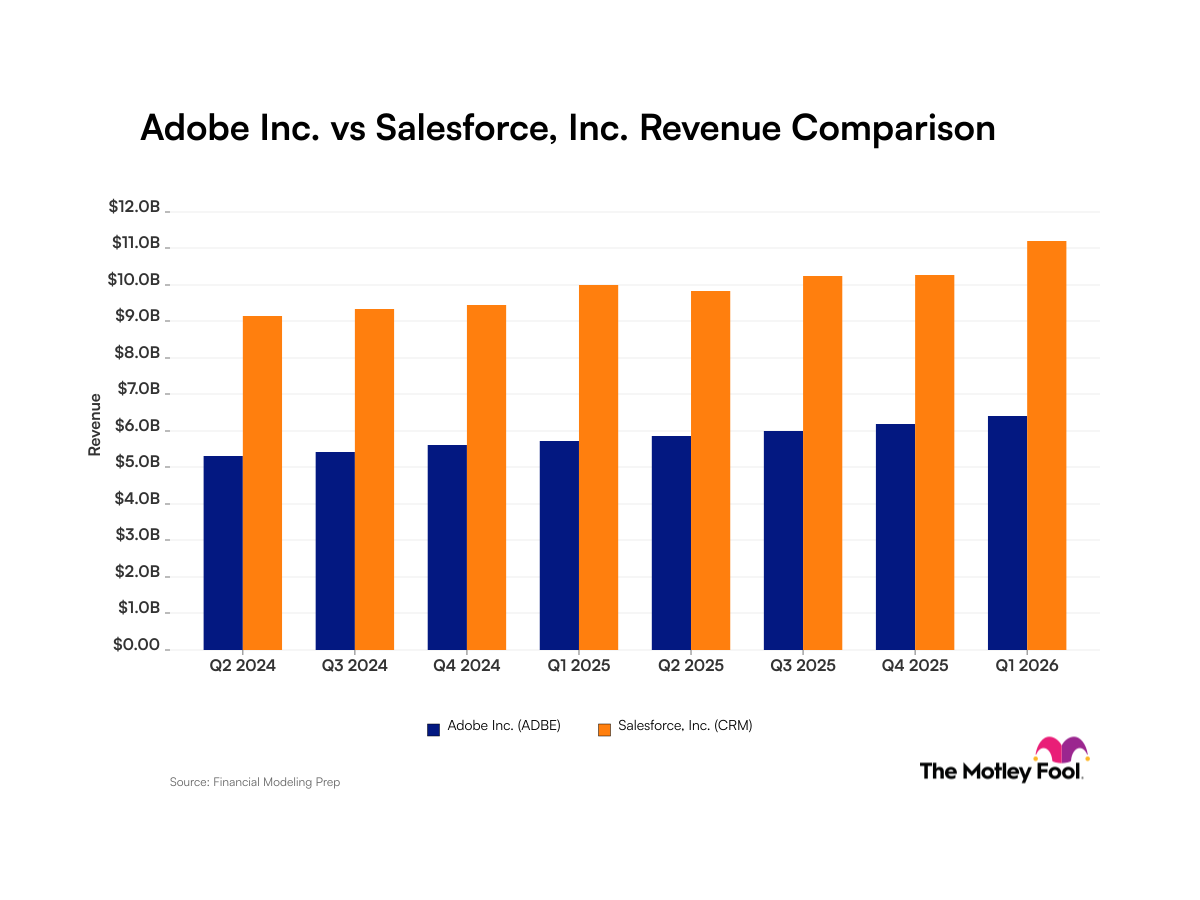

- Revenue Growth Trend: Salesforce has maintained continuous quarter-over-quarter revenue growth over the past eight quarters, despite one slight decline, while Adobe has shown similar growth, indicating a competitive landscape between the two companies.

- Net Income Margin Comparison: Adobe reported approximately 30% net income margin for the quarter ended February 27, 2026, while Salesforce posted about 17% for the quarter ended January 31, 2026, reflecting differences in profitability between the two firms.

- Market Performance Review: Both Adobe and Salesforce have seen their stock prices decline by about 34% over the past year, which correlates with a bearish market sentiment towards the software-as-a-service (SaaS) model, highlighting challenges faced by the industry.

- Valuation Opportunities: Adobe's price-to-sales (P/S) ratio has dropped to 4.2x, its lowest in over a decade, while Salesforce's P/S ratio stands at 4.1x, close to its lowest since the 2008/2009 financial crisis, potentially presenting buying opportunities for value investors.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy ADBE?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on ADBE

Wall Street analysts forecast ADBE stock price to rise

26 Analyst Rating

13 Buy

11 Hold

2 Sell

Moderate Buy

Current: 246.100

Low

270.00

Averages

431.08

High

660.00

Current: 246.100

Low

270.00

Averages

431.08

High

660.00

About ADBE

Adobe Inc. is a global technology company. The Company's products, services and solutions are used around the world to imagine, create, manage, deliver, measure, optimize and engage with content across surfaces and fuel digital experiences. Its segments include Digital Media, Digital Experience, and Publishing and Advertising. The Digital Media segment is centered around Adobe Creative Cloud and Adobe Document Cloud, which include Adobe Express, Adobe Firefly, Photoshop and other products, offering a variety of tools for creative professionals, communicators and other consumers. The Digital Experience segment provides an integrated platform and set of products, services and solutions through Adobe Experience Cloud. The Publishing and Advertising segment contains legacy products and services. In addition, its Adobe GenStudio solution allows businesses to simplify their content supply chain process with generative artificial intelligence (AI) capabilities and intelligent automation.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Adobe and Salesforce Show Consistent Revenue Growth

- Revenue Growth Performance: Adobe reported a revenue of $6.4 billion for Q1 2026 with a net income margin of approximately 30%, indicating strong performance in its software subscription model across digital media and experience sectors, thereby enhancing its market competitiveness.

- Salesforce Financial Status: Salesforce achieved a revenue of $11.2 billion in Q1 2026 with a net income margin of about 17%, further solidifying its position in the market through the provision of cloud-based customer relationship management software and enterprise analytics tools.

- Market Reaction Analysis: Despite both Adobe and Salesforce stocks declining by approximately 34% over the past year, both companies continue to demonstrate stable revenue growth, showcasing resilience in the software-as-a-service (SaaS) sector.

- Valuation Opportunities: Adobe's price-to-sales (P/S) ratio has dropped to 4.2x, the lowest in over a decade, while Salesforce's P/S ratio stands at 4.1x, indicating that growth-oriented investors may find value potential in these stocks under the current market conditions.

See More

Salesforce vs Adobe Revenue Comparison Analysis

- Revenue Growth Trend: Salesforce has maintained continuous quarter-over-quarter revenue growth over the past eight quarters, despite one slight decline, while Adobe has shown similar growth, indicating a competitive landscape between the two companies.

- Net Income Margin Comparison: Adobe reported approximately 30% net income margin for the quarter ended February 27, 2026, while Salesforce posted about 17% for the quarter ended January 31, 2026, reflecting differences in profitability between the two firms.

- Market Performance Review: Both Adobe and Salesforce have seen their stock prices decline by about 34% over the past year, which correlates with a bearish market sentiment towards the software-as-a-service (SaaS) model, highlighting challenges faced by the industry.

- Valuation Opportunities: Adobe's price-to-sales (P/S) ratio has dropped to 4.2x, its lowest in over a decade, while Salesforce's P/S ratio stands at 4.1x, close to its lowest since the 2008/2009 financial crisis, potentially presenting buying opportunities for value investors.

See More

Stagwell Reports Record Q1 Earnings and New Business Growth

- Record New Business: Stagwell achieved a record $141 million in net new business in Q1, bringing the last 12 months total to $486 million, which is approximately $80 million ahead of the same period last year, indicating successful advancements in large-scale projects and an expanding client base.

- AI Product Traction: The company's efforts in AI and enterprise products have gained early traction, with $12 million booked towards a $25 million first-year sales goal, reflecting rising market demand in the digital transformation sector.

- Improved Financials: Revenue rose 8% to $704 million in Q1, with adjusted EBITDA increasing about 9% to $90 million, and net leverage improved to 3.11x, demonstrating effective cost control and cash flow management.

- Strategic Investment and Outlook: Stagwell reiterated its full-year net revenue growth target of 8% to 12%, expecting double-digit growth in the second half driven by large creative contracts and a political cycle, showcasing the company's confidence in future market opportunities.

See More

Adobe Announces $25 Billion Stock Buyback Plan Amid AI Concerns

- Stock Buyback Plan: On April 21, Adobe announced a stock buyback plan of up to $25 billion, set to run through April 30, 2030, aimed at boosting investor confidence; however, the market reaction was tepid, with stock prices showing little movement post-announcement.

- Steady Financial Performance: Despite challenges posed by AI technology, Adobe's revenue has steadily increased from $21.5 billion in 2024 to $23.7 billion in 2025, with net income rising from $5.5 billion to $7.1 billion, demonstrating resilience in its fundamentals.

- Leadership Transition Risks: Adobe is undergoing a leadership transition as CEO Shantanu Narayen steps down after 18 years, leaving the new CEO to navigate the complexities of AI integration and develop a clear strategy, which is crucial for the company's future direction.

- Attractive Valuation Amid Challenges: Although Adobe's forward price-to-earnings ratio stands at 10.4, indicating attractiveness, the multitude of challenges it faces suggests that investors should be cautious, as a turnaround may take considerable time and is unlikely to yield immediate results.

See More

Adobe Announces $25 Billion Stock Buyback Plan Amid Challenges

- Stock Buyback Plan: Adobe's board has authorized a stock buyback plan of up to $25 billion, set to run through April 30, 2030, aimed at boosting investor confidence, yet it failed to significantly impact the stock price.

- Steady Financial Performance: Despite facing challenges, Adobe's revenue rose from $21.5 billion in 2024 to $23.7 billion in 2025, with net income increasing from $5.5 billion to $7.1 billion, demonstrating resilience in its fundamentals.

- Leadership Transition: CEO Shantanu Narayen will step down once a successor is found, placing the new leader in a challenging position to effectively integrate AI technology and develop a clear strategy to navigate market changes.

- Lackluster Market Reaction: Although Adobe's forward price-to-earnings ratio stands at an attractive 10.4, the stock's performance remains weak due to multiple challenges, prompting investors to carefully assess their investment decisions.

See More

Apple's CEO Tim Cook to Retire Amid AI Challenges and Opportunities

- Cook's Leadership Legacy: Apple's CEO Tim Cook announced his retirement later this year, marking the end of nearly 15 years of leadership during which Apple's market cap soared from $600 billion to nearly $3 trillion, highlighting his contributions to stability and sustained growth.

- Opportunities in the AI Era: With the rise of artificial intelligence, Apple faces new challenges, particularly in hardware innovation, as Cook's successor Ternus will need to maintain the competitiveness of core products while exploring new AI-driven markets.

- Intel's Resurgence: Intel reported strong earnings in 2026, with stock hitting an all-time high due to surging demand for CPUs, underscoring the company's pivotal role in AI infrastructure development and its potential to benefit from the growing need for high-performance computing.

- SaaS Market Turmoil: ServiceNow's earnings triggered market panic, leading to a widespread decline in related stocks, despite its report showing solid growth potential, reflecting investors' heightened sensitivity to AI impacts, which may result in short-term market volatility.

See More

Adobe and Salesforce Show Consistent Revenue Growth

- Revenue Growth Performance: Adobe reported a revenue of $6.4 billion for Q1 2026 with a net income margin of approximately 30%, indicating strong performance in its software subscription model across digital media and experience sectors, thereby enhancing its market competitiveness.

- Salesforce Financial Status: Salesforce achieved a revenue of $11.2 billion in Q1 2026 with a net income margin of about 17%, further solidifying its position in the market through the provision of cloud-based customer relationship management software and enterprise analytics tools.

- Market Reaction Analysis: Despite both Adobe and Salesforce stocks declining by approximately 34% over the past year, both companies continue to demonstrate stable revenue growth, showcasing resilience in the software-as-a-service (SaaS) sector.

- Valuation Opportunities: Adobe's price-to-sales (P/S) ratio has dropped to 4.2x, the lowest in over a decade, while Salesforce's P/S ratio stands at 4.1x, indicating that growth-oriented investors may find value potential in these stocks under the current market conditions.

See More

Salesforce vs Adobe Revenue Comparison Analysis

- Revenue Growth Trend: Salesforce has maintained continuous quarter-over-quarter revenue growth over the past eight quarters, despite one slight decline, while Adobe has shown similar growth, indicating a competitive landscape between the two companies.

- Net Income Margin Comparison: Adobe reported approximately 30% net income margin for the quarter ended February 27, 2026, while Salesforce posted about 17% for the quarter ended January 31, 2026, reflecting differences in profitability between the two firms.

- Market Performance Review: Both Adobe and Salesforce have seen their stock prices decline by about 34% over the past year, which correlates with a bearish market sentiment towards the software-as-a-service (SaaS) model, highlighting challenges faced by the industry.

- Valuation Opportunities: Adobe's price-to-sales (P/S) ratio has dropped to 4.2x, its lowest in over a decade, while Salesforce's P/S ratio stands at 4.1x, close to its lowest since the 2008/2009 financial crisis, potentially presenting buying opportunities for value investors.

See More

Stagwell Reports Record Q1 Earnings and New Business Growth

- Record New Business: Stagwell achieved a record $141 million in net new business in Q1, bringing the last 12 months total to $486 million, which is approximately $80 million ahead of the same period last year, indicating successful advancements in large-scale projects and an expanding client base.

- AI Product Traction: The company's efforts in AI and enterprise products have gained early traction, with $12 million booked towards a $25 million first-year sales goal, reflecting rising market demand in the digital transformation sector.

- Improved Financials: Revenue rose 8% to $704 million in Q1, with adjusted EBITDA increasing about 9% to $90 million, and net leverage improved to 3.11x, demonstrating effective cost control and cash flow management.

- Strategic Investment and Outlook: Stagwell reiterated its full-year net revenue growth target of 8% to 12%, expecting double-digit growth in the second half driven by large creative contracts and a political cycle, showcasing the company's confidence in future market opportunities.

See More

Adobe Announces $25 Billion Stock Buyback Plan Amid AI Concerns

- Stock Buyback Plan: On April 21, Adobe announced a stock buyback plan of up to $25 billion, set to run through April 30, 2030, aimed at boosting investor confidence; however, the market reaction was tepid, with stock prices showing little movement post-announcement.

- Steady Financial Performance: Despite challenges posed by AI technology, Adobe's revenue has steadily increased from $21.5 billion in 2024 to $23.7 billion in 2025, with net income rising from $5.5 billion to $7.1 billion, demonstrating resilience in its fundamentals.

- Leadership Transition Risks: Adobe is undergoing a leadership transition as CEO Shantanu Narayen steps down after 18 years, leaving the new CEO to navigate the complexities of AI integration and develop a clear strategy, which is crucial for the company's future direction.

- Attractive Valuation Amid Challenges: Although Adobe's forward price-to-earnings ratio stands at 10.4, indicating attractiveness, the multitude of challenges it faces suggests that investors should be cautious, as a turnaround may take considerable time and is unlikely to yield immediate results.

See More

Adobe Announces $25 Billion Stock Buyback Plan Amid Challenges

- Stock Buyback Plan: Adobe's board has authorized a stock buyback plan of up to $25 billion, set to run through April 30, 2030, aimed at boosting investor confidence, yet it failed to significantly impact the stock price.

- Steady Financial Performance: Despite facing challenges, Adobe's revenue rose from $21.5 billion in 2024 to $23.7 billion in 2025, with net income increasing from $5.5 billion to $7.1 billion, demonstrating resilience in its fundamentals.

- Leadership Transition: CEO Shantanu Narayen will step down once a successor is found, placing the new leader in a challenging position to effectively integrate AI technology and develop a clear strategy to navigate market changes.

- Lackluster Market Reaction: Although Adobe's forward price-to-earnings ratio stands at an attractive 10.4, the stock's performance remains weak due to multiple challenges, prompting investors to carefully assess their investment decisions.

See More

Apple's CEO Tim Cook to Retire Amid AI Challenges and Opportunities

- Cook's Leadership Legacy: Apple's CEO Tim Cook announced his retirement later this year, marking the end of nearly 15 years of leadership during which Apple's market cap soared from $600 billion to nearly $3 trillion, highlighting his contributions to stability and sustained growth.

- Opportunities in the AI Era: With the rise of artificial intelligence, Apple faces new challenges, particularly in hardware innovation, as Cook's successor Ternus will need to maintain the competitiveness of core products while exploring new AI-driven markets.

- Intel's Resurgence: Intel reported strong earnings in 2026, with stock hitting an all-time high due to surging demand for CPUs, underscoring the company's pivotal role in AI infrastructure development and its potential to benefit from the growing need for high-performance computing.

- SaaS Market Turmoil: ServiceNow's earnings triggered market panic, leading to a widespread decline in related stocks, despite its report showing solid growth potential, reflecting investors' heightened sensitivity to AI impacts, which may result in short-term market volatility.

See More