Oppenheimer Lowers Target Price for Roblox Corporation to $82 from $130

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 1 hour ago

0mins

Should l Buy RBLX?

Source: moomoo

- Target Price Adjustment: Oppenheimer has reduced the target price for Roblox Corporation from $130 to $82.

- Market Impact: This significant cut reflects changing market conditions and expectations for the company's future performance.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy RBLX?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on RBLX

Wall Street analysts forecast RBLX stock price to rise

22 Analyst Rating

13 Buy

8 Hold

1 Sell

Moderate Buy

Current: 55.260

Low

70.00

Averages

133.89

High

180.00

Current: 55.260

Low

70.00

Averages

133.89

High

180.00

About RBLX

Roblox Corporation operates a platform for connection and communication (Roblox Platform), where every day, people come to create, play, work, learn, and connect with each other in experiences built by its global community of creators. The Company’s platform consists of the Roblox Client, the Roblox Studio, and the Roblox Cloud. Roblox Client is an application that allows users to seamlessly explore 3D immersive experiences. Roblox Studio is the free toolset that allows developers and creators to build, publish, and operate three-dimensional (3D) immersive experiences and other content accessed with the Roblox Client. Roblox Cloud includes the services and infrastructure that power its Platform. The Company operates the Roblox Platform as a live service that allows users to play and socialize with others for free. The Company offers developers and creators the ability to build engaging, immersive experiences and marketplace items that they can easily share with the Roblox community.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Roblox Reports Q1 2026 Earnings with Revised Guidance

- Revenue and Bookings Data: Roblox reported Q1 revenue of $1.4 billion and bookings of $1.7 billion, with strong cash flow metrics of $629 million in operating cash flow and $596 million in free cash flow, yet user growth challenges led to a downward revision of full-year expectations.

- Decline in User Engagement: The global rollout of age checks has impacted user acquisition and engagement, resulting in weaker-than-expected DAUs, with management anticipating continued pressure into Q2 but expecting a return to growth in Q3, highlighting the profound effects of safety measures on user behavior.

- Adjusted Growth Expectations: CFO Naveen Chopra revised full-year revenue growth guidance to 20%-25% and bookings growth to 8%-12%, primarily due to safety-related friction and communication changes, indicating significant short-term challenges for the company.

- Shift in Strategic Priorities: Management emphasized a shift from platform innovation to addressing safety-driven friction, including the rollout of age-based accounts in June and optimizing communication features, aiming to enhance long-term user retention and expand the 18+ user base.

See More

Latest Wall Street Rating Updates

- Apple's Positive Outlook: Bank of America reiterates a buy rating on Apple, forecasting that iPhone revenues will exceed expectations in 2026 due to record upgraders and strong gross margins despite commodity pressures, indicating sustained competitiveness in the smartphone market.

- Roblox Demand Slowdown: Bank of America downgrades Roblox to neutral, citing a significant decline in platform demand; while acknowledging its ability to compress development costs, the uncertainty around the timeline for demand recovery may impact its market performance.

- CoreWeave Growth Potential: Citi reiterates CoreWeave as a buy, raising its price target from $126 to $155, estimating a quarterly growth of 35-40% in AI infrastructure, showcasing strong performance across a diversified customer base.

- Hershey's Positive Outlook: TD Cowen upgrades Hershey to buy, expressing confidence that the company will raise its 2026 guidance and return to volume growth in 2027, reflecting strong recovery potential in the confectionery market.

See More

Oppenheimer Lowers Target Price for Roblox Corporation to $82 from $130

- Target Price Adjustment: Oppenheimer has reduced the target price for Roblox Corporation from $130 to $82.

- Market Impact: This significant cut reflects changing market conditions and expectations for the company's future performance.

See More

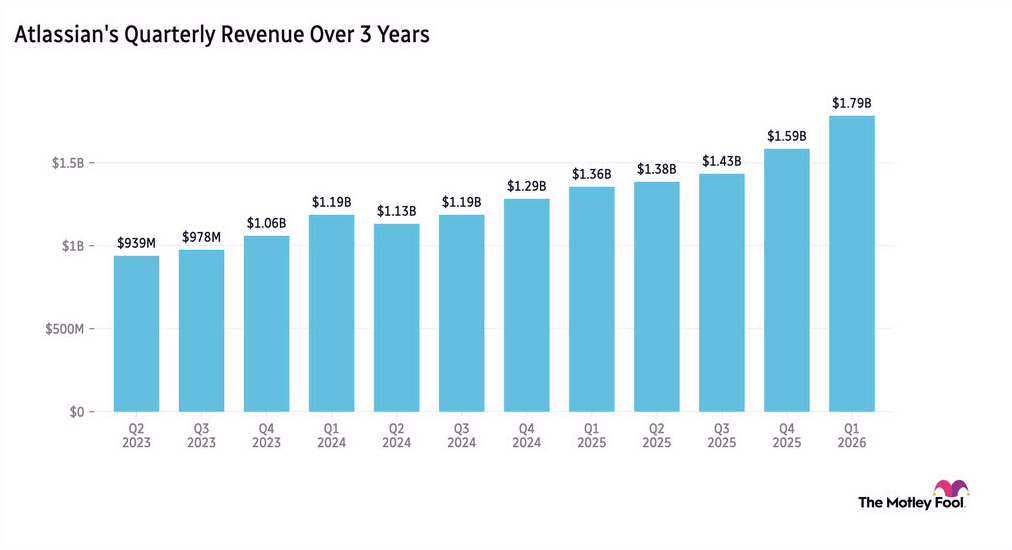

Atlassian Shares Surge 25% on AI-Driven Revenue Growth

- Revenue Surge: Atlassian's third-quarter revenue rose 32% year-over-year, leading to a 25% jump in pre-market trading, and despite restructuring costs impacting profitability, non-GAAP earnings per share soared by 80%, reflecting strong demand for AI services.

- Cloud Transition: CFO James Chuong cautioned that the shift of customers to cloud services would result in a more muted level of data center expansion, with expectations for moderated revenue growth in Q4, which could impact future market performance.

- Product Advantage: Analyst Meilin Quinn noted that while workflows may be taken over by agents, there remains a need for trusted company knowledge and systems, providing Atlassian with a stronger foothold in engineering processes and enhancing its competitive edge.

- Market Reaction: Major stock indexes hit new highs amid continued growth in AI spending, with the S&P 500 closing above 7,200 points for the first time, reflecting strong market confidence in tech stocks and further boosting Atlassian's stock performance.

See More

Apple, Roku, Estée Lauder Beat Earnings Expectations

- Apple's Strong Earnings: Apple reported a fiscal second-quarter earnings of $2.01 per share and revenue of $111.18 billion, surpassing analyst expectations of $1.95 and $109.66 billion, although iPhone sales missed estimates for the third consecutive quarter, indicating increasing market competition pressures.

- Roku's Robust Growth: Roku's first-quarter revenue reached $1.25 billion, exceeding the expected $1.20 billion, with adjusted EBITDA of $148.4 million also above the forecast of $131.3 million, highlighting the company's ongoing growth potential in the streaming market.

- Estée Lauder's Better-Than-Expected Performance: Estée Lauder reported third-quarter earnings of $0.91 per share and revenue of $3.71 billion, both exceeding analyst estimates, despite announcing job cuts as part of its turnaround strategy, reflecting its adaptive measures in a changing market.

- Moderna's Improved Financials: Moderna posted a first-quarter loss of $3.40 per share, better than the anticipated loss of $4.45, with revenues of $389 million surpassing the $236.4 million estimate, indicating its sustained competitiveness in the vaccine market.

See More

Roblox Shares Plunge 24% After Lowering Annual Bookings Forecast

- Bookings Forecast Cut: Roblox has lowered its full-year bookings forecast to $7.33 billion to $7.6 billion from the previous $8.28 billion to $8.55 billion, indicating a pessimistic outlook on future revenues that may erode investor confidence.

- User Growth Constraints: The newly implemented safety measures, including age-based accounts and content monitoring, have restricted user communication and slowed new user acquisition, potentially causing continued short-term friction in user growth over the next few quarters, impacting the platform's long-term development.

- Market Valuation Loss: If current losses persist, Roblox could lose over $9 billion from its market valuation of $39.55 billion, reflecting market concerns about its future growth potential, especially amid increasing competition.

- Increased Competitive Pressure: Analysts have noted that the forecast cut likely reflects competitive pressures from Fortnite and the upcoming release of Take-Two Interactive's Grand Theft Auto VI, which is expected to drive billions in revenue and could further weaken Roblox's bookings growth.

See More

Roblox Reports Q1 2026 Earnings with Revised Guidance

- Revenue and Bookings Data: Roblox reported Q1 revenue of $1.4 billion and bookings of $1.7 billion, with strong cash flow metrics of $629 million in operating cash flow and $596 million in free cash flow, yet user growth challenges led to a downward revision of full-year expectations.

- Decline in User Engagement: The global rollout of age checks has impacted user acquisition and engagement, resulting in weaker-than-expected DAUs, with management anticipating continued pressure into Q2 but expecting a return to growth in Q3, highlighting the profound effects of safety measures on user behavior.

- Adjusted Growth Expectations: CFO Naveen Chopra revised full-year revenue growth guidance to 20%-25% and bookings growth to 8%-12%, primarily due to safety-related friction and communication changes, indicating significant short-term challenges for the company.

- Shift in Strategic Priorities: Management emphasized a shift from platform innovation to addressing safety-driven friction, including the rollout of age-based accounts in June and optimizing communication features, aiming to enhance long-term user retention and expand the 18+ user base.

See More

Latest Wall Street Rating Updates

- Apple's Positive Outlook: Bank of America reiterates a buy rating on Apple, forecasting that iPhone revenues will exceed expectations in 2026 due to record upgraders and strong gross margins despite commodity pressures, indicating sustained competitiveness in the smartphone market.

- Roblox Demand Slowdown: Bank of America downgrades Roblox to neutral, citing a significant decline in platform demand; while acknowledging its ability to compress development costs, the uncertainty around the timeline for demand recovery may impact its market performance.

- CoreWeave Growth Potential: Citi reiterates CoreWeave as a buy, raising its price target from $126 to $155, estimating a quarterly growth of 35-40% in AI infrastructure, showcasing strong performance across a diversified customer base.

- Hershey's Positive Outlook: TD Cowen upgrades Hershey to buy, expressing confidence that the company will raise its 2026 guidance and return to volume growth in 2027, reflecting strong recovery potential in the confectionery market.

See More

Oppenheimer Lowers Target Price for Roblox Corporation to $82 from $130

- Target Price Adjustment: Oppenheimer has reduced the target price for Roblox Corporation from $130 to $82.

- Market Impact: This significant cut reflects changing market conditions and expectations for the company's future performance.

See More

Atlassian Shares Surge 25% on AI-Driven Revenue Growth

- Revenue Surge: Atlassian's third-quarter revenue rose 32% year-over-year, leading to a 25% jump in pre-market trading, and despite restructuring costs impacting profitability, non-GAAP earnings per share soared by 80%, reflecting strong demand for AI services.

- Cloud Transition: CFO James Chuong cautioned that the shift of customers to cloud services would result in a more muted level of data center expansion, with expectations for moderated revenue growth in Q4, which could impact future market performance.

- Product Advantage: Analyst Meilin Quinn noted that while workflows may be taken over by agents, there remains a need for trusted company knowledge and systems, providing Atlassian with a stronger foothold in engineering processes and enhancing its competitive edge.

- Market Reaction: Major stock indexes hit new highs amid continued growth in AI spending, with the S&P 500 closing above 7,200 points for the first time, reflecting strong market confidence in tech stocks and further boosting Atlassian's stock performance.

See More

Apple, Roku, Estée Lauder Beat Earnings Expectations

- Apple's Strong Earnings: Apple reported a fiscal second-quarter earnings of $2.01 per share and revenue of $111.18 billion, surpassing analyst expectations of $1.95 and $109.66 billion, although iPhone sales missed estimates for the third consecutive quarter, indicating increasing market competition pressures.

- Roku's Robust Growth: Roku's first-quarter revenue reached $1.25 billion, exceeding the expected $1.20 billion, with adjusted EBITDA of $148.4 million also above the forecast of $131.3 million, highlighting the company's ongoing growth potential in the streaming market.

- Estée Lauder's Better-Than-Expected Performance: Estée Lauder reported third-quarter earnings of $0.91 per share and revenue of $3.71 billion, both exceeding analyst estimates, despite announcing job cuts as part of its turnaround strategy, reflecting its adaptive measures in a changing market.

- Moderna's Improved Financials: Moderna posted a first-quarter loss of $3.40 per share, better than the anticipated loss of $4.45, with revenues of $389 million surpassing the $236.4 million estimate, indicating its sustained competitiveness in the vaccine market.

See More

Roblox Shares Plunge 24% After Lowering Annual Bookings Forecast

- Bookings Forecast Cut: Roblox has lowered its full-year bookings forecast to $7.33 billion to $7.6 billion from the previous $8.28 billion to $8.55 billion, indicating a pessimistic outlook on future revenues that may erode investor confidence.

- User Growth Constraints: The newly implemented safety measures, including age-based accounts and content monitoring, have restricted user communication and slowed new user acquisition, potentially causing continued short-term friction in user growth over the next few quarters, impacting the platform's long-term development.

- Market Valuation Loss: If current losses persist, Roblox could lose over $9 billion from its market valuation of $39.55 billion, reflecting market concerns about its future growth potential, especially amid increasing competition.

- Increased Competitive Pressure: Analysts have noted that the forecast cut likely reflects competitive pressures from Fortnite and the upcoming release of Take-Two Interactive's Grand Theft Auto VI, which is expected to drive billions in revenue and could further weaken Roblox's bookings growth.

See More