Philips Reports Strong Q1 2026 Performance with 6% Order Growth

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 44 minutes ago

0mins

Should l Buy PHG?

Source: Newsfilter

- Significant Order Growth: In Q1 2026, Philips achieved a 6% increase in comparable order intake, primarily driven by strong performance in North America and the International Region, demonstrating the company's ability to sustain growth amid an uncertain macro environment.

- Steady Sales Increase: Group sales reached EUR 3.9 billion, reflecting a 4% year-over-year growth, with all business segments contributing positively, particularly Personal Health, indicating an enhanced competitive position in the market.

- Improved Profitability: The adjusted EBITA margin increased by 40 basis points to 9.0%, mainly due to higher sales and improved underlying gross margins, despite pressures from tariffs and cost inflation, showcasing effective cost management strategies.

- Innovation-Driven Growth: Philips continues to lead in MedTech, securing FDA approvals for AI-powered innovations like SmartHeart and DeviceGuide, which further solidify its competitive edge in health technology and drive strong customer demand.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy PHG?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on PHG

About PHG

Koninklijke Philips NV is a Netherlands-based health technology company. The Company's segments include Personal Health businesses, Diagnosis & Treatment businesses, Connected Care businesses and Other. The Personal Health businesses segment is engaged in the health continuum, delivering integrated, connected solutions that support healthier lifestyles and those living with chronic disease as well as oral healthcare and mother and child care support. The Diagnosis & Treatment businesses segment delivers precision medicine and treatment, and therapy. The Connected Care businesses segment provides consumers, care givers and clinicians with digital solutions that facilitate care by enabling precision medicine and population health management. The Other segment comprises such items, as innovation, emerging businesses, royalties, among others.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Philips to Announce Q1 Earnings on May 6

- Earnings Announcement: Philips (PHG) is set to announce its Q1 2023 earnings on May 6 before the market opens, with consensus EPS estimated at $0.19 and revenue projected at $4.55 billion, indicating the company's financial stability.

- Historical Performance: Over the past two years, Philips has consistently beaten EPS and revenue estimates 100% of the time, reflecting its strong profitability and boosting investor confidence in its future performance.

- Investor Day Event: Philips will also hold an Analyst/Investor Day to showcase its strategic direction and future growth potential, which is expected to attract more investor interest and enhance market perception of its stock.

- Board Restructuring Plan: The company plans to reshuffle its board and reappoint the CEO at the 2026 AGM, aiming to strengthen corporate governance and improve decision-making efficiency, thereby laying a solid foundation for future business development.

See More

Philips Reiterates 2026 Outlook Amid Q1 Results

- Financial Performance: Philips reported a Q1 non-GAAP EPS of €0.16 and revenue of €3.9 billion, reflecting a 4.9% year-over-year decline, indicating pressure from market competition and broader economic challenges.

- Order Growth: Despite the revenue drop, comparable order intake grew by 6%, suggesting strong market demand in specific areas, which could lay the groundwork for future sales recovery.

- Operational Efficiency: Income from operations rose to €241 million, with adjusted EBITA margin increasing by 40 basis points to 9.0%, indicating positive progress in cost control and efficiency improvements that enhance profitability.

- Future Outlook: Philips reiterated its full-year 2026 outlook, projecting comparable sales growth of 3%-4.5%, adjusted EBITA margin of 12.5%-13.0%, and free cash flow between €1.3 billion and €1.5 billion, demonstrating confidence in future growth prospects.

See More

Philips Reports Strong Q1 2026 Performance with 6% Order Growth

- Significant Order Growth: In Q1 2026, Philips achieved a 6% increase in comparable order intake, primarily driven by strong performance in North America and the International Region, demonstrating the company's ability to sustain growth amid an uncertain macro environment.

- Steady Sales Increase: Group sales reached EUR 3.9 billion, reflecting a 4% year-over-year growth, with all business segments contributing positively, particularly Personal Health, indicating an enhanced competitive position in the market.

- Improved Profitability: The adjusted EBITA margin increased by 40 basis points to 9.0%, mainly due to higher sales and improved underlying gross margins, despite pressures from tariffs and cost inflation, showcasing effective cost management strategies.

- Innovation-Driven Growth: Philips continues to lead in MedTech, securing FDA approvals for AI-powered innovations like SmartHeart and DeviceGuide, which further solidify its competitive edge in health technology and drive strong customer demand.

See More

Global Sleep Apnea Devices Market Growth Forecast

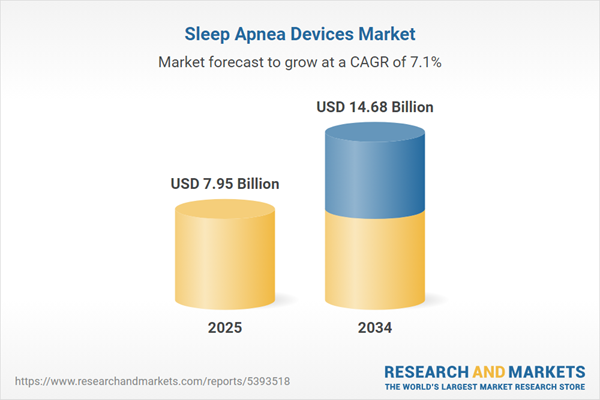

- Market Size Growth: The global sleep apnea devices market is projected to expand from USD 7.95 billion in 2025 to USD 14.68 billion by 2034, growing at a CAGR of 7.05%, reflecting increased awareness of sleep disorders and technological advancements.

- Expanding Patient Base: Approximately 1 billion individuals globally are affected by sleep apnea, with 936 million suffering from obstructive sleep apnea, and over 30 million in the U.S., indicating significant market demand potential.

- Technological Innovation Drive: Recent advancements have made sleep apnea devices smaller, quieter, and more portable, while the introduction of smart devices enhances treatment effectiveness and patient comfort, propelling market growth.

- Homecare Trend: The increasing preference for home-based healthcare solutions has significantly boosted demand for sleep apnea devices, particularly as insurance coverage expands, making home testing devices like NightOwl more appealing.

See More

Philips Rembra Platform Receives FDA Clearance

- FDA Clearance: Philips' Rembra CT, Rembra RT, and Areta RT systems have received 510(k) clearance from the U.S. FDA, marking a significant advancement in high-throughput imaging and cancer treatment planning, expected to enhance efficiency and quality in healthcare services.

- High-Throughput Imaging Capability: The Rembra CT system supports up to 270 exams per day, designed for emergency, critical care, and interventional settings, enabling clinicians to make timely decisions in critical moments, thus improving the coherence of patient care.

- Precision Treatment Planning: Rembra RT and Areta RT systems feature an 85 cm extended field of view and next-generation 4DCT imaging capabilities, allowing for more accurate tumor targeting while protecting healthy tissue, thereby enhancing the personalization and precision of cancer treatment and reducing variability in the treatment process.

- Integrated Healthcare Workflows: The Rembra platform aims to enhance the efficiency and confidence of healthcare providers by integrating diagnostic and therapeutic solutions, further solidifying Philips' market position in the CT field to meet the growing demand for imaging.

See More

Philips Receives FDA Clearance for First AI-Powered Spectral CT

- FDA Clearance: Philips' Spectral CT Verida system has received FDA 510(k) clearance, becoming the world's first AI-powered spectral CT scanner for clinical use, marking a significant advancement in medical imaging technology.

- Enhanced Imaging Efficiency: The system can reconstruct up to 145 images per second, reducing full-body exam times to under 30 seconds and supporting up to 270 exams per day, significantly improving workflow efficiency in high-volume departments.

- Broad Clinical Applications: The Verida system is cleared for head, whole-body, cardiac, and vascular CT imaging, and is also indicated for oncology treatment planning, providing simultaneous conventional and spectral results to enhance tissue characterization capabilities.

- Personalized Adjustments: The updated computing infrastructure allows clinicians to adjust image de-noising levels based on personal preferences, ensuring customization without compromising spectral output, further enhancing the accuracy of clinical decision-making.

See More

Philips to Announce Q1 Earnings on May 6

- Earnings Announcement: Philips (PHG) is set to announce its Q1 2023 earnings on May 6 before the market opens, with consensus EPS estimated at $0.19 and revenue projected at $4.55 billion, indicating the company's financial stability.

- Historical Performance: Over the past two years, Philips has consistently beaten EPS and revenue estimates 100% of the time, reflecting its strong profitability and boosting investor confidence in its future performance.

- Investor Day Event: Philips will also hold an Analyst/Investor Day to showcase its strategic direction and future growth potential, which is expected to attract more investor interest and enhance market perception of its stock.

- Board Restructuring Plan: The company plans to reshuffle its board and reappoint the CEO at the 2026 AGM, aiming to strengthen corporate governance and improve decision-making efficiency, thereby laying a solid foundation for future business development.

See More

Philips Reiterates 2026 Outlook Amid Q1 Results

- Financial Performance: Philips reported a Q1 non-GAAP EPS of €0.16 and revenue of €3.9 billion, reflecting a 4.9% year-over-year decline, indicating pressure from market competition and broader economic challenges.

- Order Growth: Despite the revenue drop, comparable order intake grew by 6%, suggesting strong market demand in specific areas, which could lay the groundwork for future sales recovery.

- Operational Efficiency: Income from operations rose to €241 million, with adjusted EBITA margin increasing by 40 basis points to 9.0%, indicating positive progress in cost control and efficiency improvements that enhance profitability.

- Future Outlook: Philips reiterated its full-year 2026 outlook, projecting comparable sales growth of 3%-4.5%, adjusted EBITA margin of 12.5%-13.0%, and free cash flow between €1.3 billion and €1.5 billion, demonstrating confidence in future growth prospects.

See More

Philips Reports Strong Q1 2026 Performance with 6% Order Growth

- Significant Order Growth: In Q1 2026, Philips achieved a 6% increase in comparable order intake, primarily driven by strong performance in North America and the International Region, demonstrating the company's ability to sustain growth amid an uncertain macro environment.

- Steady Sales Increase: Group sales reached EUR 3.9 billion, reflecting a 4% year-over-year growth, with all business segments contributing positively, particularly Personal Health, indicating an enhanced competitive position in the market.

- Improved Profitability: The adjusted EBITA margin increased by 40 basis points to 9.0%, mainly due to higher sales and improved underlying gross margins, despite pressures from tariffs and cost inflation, showcasing effective cost management strategies.

- Innovation-Driven Growth: Philips continues to lead in MedTech, securing FDA approvals for AI-powered innovations like SmartHeart and DeviceGuide, which further solidify its competitive edge in health technology and drive strong customer demand.

See More

Global Sleep Apnea Devices Market Growth Forecast

- Market Size Growth: The global sleep apnea devices market is projected to expand from USD 7.95 billion in 2025 to USD 14.68 billion by 2034, growing at a CAGR of 7.05%, reflecting increased awareness of sleep disorders and technological advancements.

- Expanding Patient Base: Approximately 1 billion individuals globally are affected by sleep apnea, with 936 million suffering from obstructive sleep apnea, and over 30 million in the U.S., indicating significant market demand potential.

- Technological Innovation Drive: Recent advancements have made sleep apnea devices smaller, quieter, and more portable, while the introduction of smart devices enhances treatment effectiveness and patient comfort, propelling market growth.

- Homecare Trend: The increasing preference for home-based healthcare solutions has significantly boosted demand for sleep apnea devices, particularly as insurance coverage expands, making home testing devices like NightOwl more appealing.

See More

Philips Rembra Platform Receives FDA Clearance

- FDA Clearance: Philips' Rembra CT, Rembra RT, and Areta RT systems have received 510(k) clearance from the U.S. FDA, marking a significant advancement in high-throughput imaging and cancer treatment planning, expected to enhance efficiency and quality in healthcare services.

- High-Throughput Imaging Capability: The Rembra CT system supports up to 270 exams per day, designed for emergency, critical care, and interventional settings, enabling clinicians to make timely decisions in critical moments, thus improving the coherence of patient care.

- Precision Treatment Planning: Rembra RT and Areta RT systems feature an 85 cm extended field of view and next-generation 4DCT imaging capabilities, allowing for more accurate tumor targeting while protecting healthy tissue, thereby enhancing the personalization and precision of cancer treatment and reducing variability in the treatment process.

- Integrated Healthcare Workflows: The Rembra platform aims to enhance the efficiency and confidence of healthcare providers by integrating diagnostic and therapeutic solutions, further solidifying Philips' market position in the CT field to meet the growing demand for imaging.

See More

Philips Receives FDA Clearance for First AI-Powered Spectral CT

- FDA Clearance: Philips' Spectral CT Verida system has received FDA 510(k) clearance, becoming the world's first AI-powered spectral CT scanner for clinical use, marking a significant advancement in medical imaging technology.

- Enhanced Imaging Efficiency: The system can reconstruct up to 145 images per second, reducing full-body exam times to under 30 seconds and supporting up to 270 exams per day, significantly improving workflow efficiency in high-volume departments.

- Broad Clinical Applications: The Verida system is cleared for head, whole-body, cardiac, and vascular CT imaging, and is also indicated for oncology treatment planning, providing simultaneous conventional and spectral results to enhance tissue characterization capabilities.

- Personalized Adjustments: The updated computing infrastructure allows clinicians to adjust image de-noising levels based on personal preferences, ensuring customization without compromising spectral output, further enhancing the accuracy of clinical decision-making.

See More