Orla Mining Reports Record $133 Million Free Cash Flow for 2025

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Mar 19 2026

0mins

Should l Buy ORLA?

Source: Yahoo Finance

- Record Cash Flow: Orla Mining achieved a record free cash flow of $133 million in 2025, supporting its self-funded growth model and demonstrating strong financial performance and sustainability in the gold mining sector.

- Production Exceeds Expectations: The total gold production for 2025 reached 300,620 ounces, surpassing guidance, indicating the company's success in resource development and production efficiency, further solidifying its market position.

- Effective Cost Control: The all-in sustaining cost (AISC) for Q4 was $1,536 per ounce, with an annual AISC of $1,458, both within guidance, showcasing the company's excellence in cost management and operational efficiency.

- Ongoing Project Investment: The company reported exploration and project expenditures of $43.9 million in Q4, with $31.6 million capitalized, reflecting Orla's continued investment in future growth and confidence in resource potential.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy ORLA?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on ORLA

Wall Street analysts forecast ORLA stock price to rise

5 Analyst Rating

5 Buy

0 Hold

0 Sell

Strong Buy

Current: 16.430

Low

15.14

Averages

18.60

High

23.07

Current: 16.430

Low

15.14

Averages

18.60

High

23.07

About ORLA

Orla Mining Ltd. is a Canada-based company, which focuses on acquiring, developing, and operating mineral properties. The Company’s segments include the Camino Rojo Mine, the Nevada projects, the Cerro Quema project, and Musselwhite Mine. Camino Rojo, in Zacatecas State, Mexico, is an operating gold and silver open-pit and heap leach mine. The property covers over 139,000 hectares and contains a large oxide and sulfide mineral resource. Musselwhite Mine, in Northwestern Ontario, Canada, is an underground gold mine that produces close to six million ounces of gold. Musselwhite Gold Mine is located on the shore of Opapimiskan Lake in Northwestern Ontario. The Company’s South Railroad Project is located along the Pinon mountain range, approximately 24 kilometers south-southeast of Carlin, Nevada, in the railroad mining district. South Railroad is part of the Company’s South Carlin Complex, a prospective 25,000-hectare land package.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

ORLA Ranks High Among Analysts in Metals Sector

- Analyst Ranking Methodology: The ranking of the Metals Channel Global Mining Titans Index was formed by averaging analyst opinions from major brokerages, indicating a growing interest in ORLA, which, despite its lower rank, suggests potential for upside.

- Market Performance Comparison: ORLA is currently trading up about 5.5%, outperforming peers like Newmont Corp (up about 3%) and Barrick Mining Corp (up about 2.9%), highlighting its relative strength in the precious metals sector and potentially attracting more investor interest.

- Diverse Investor Interpretations: Although ORLA ranks low among analysts, investors can interpret this as an opportunity for upside, indicating a divergence in market sentiment that may benefit bullish investors looking for contrarian plays.

- Price History Analysis: A three-month price history chart comparing ORLA with NEM and B is provided, further illustrating ORLA's performance trends in the precious metals market, aiding investors in making more informed decisions.

See More

Orla Mining on Track for 2026 Gold Production Guidance

- Stable Gold Production: Orla Mining confirmed its 2026 gold production guidance of 340,000 to 360,000 ounces, with Q1 total production reaching 81,206 ounces and sales slightly higher at 81,540 ounces, indicating a stable performance in the gold market.

- Musselwhite Mine Performance: At the Musselwhite mine, 333,495 tonnes of ore were mined and 332,822 tonnes processed in Q1, with a mill head grade of 6.29 g/t gold and a recovery rate of 95.91%, resulting in gold production of 62,985 ounces.

- Strong Cash Position: As of March 31, 2026, Orla's cash and debt stood at $427.3 million and $331.3 million, respectively, yielding a net cash position of $96.0 million, reflecting the company's financial robustness that supports future investments and expansions.

- Strategic Growth Outlook: CEO Jason Simpson noted that 2026 is a catalyst-rich year, and the strong start suggests the company is poised for further growth and development in the coming months.

See More

Orla Mining Expands Musselwhite Mine Potential with New Discoveries

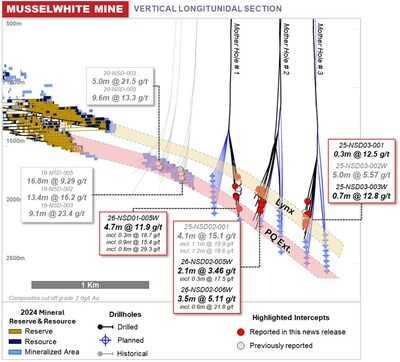

- Mine Potential Expansion: Orla Mining's directional drilling at the Musselwhite Mine has uncovered new high-grade gold mineralization, indicating that the Lynx and PQ zones extend over two kilometers, significantly enhancing resource potential and possibly extending the mine's lifespan.

- Underground Drilling Results: Ongoing underground drilling continues to return strong gold intercepts, including 11.5 meters at 11.0 g/t Au, reinforcing confidence in resource growth and reserve replacement, indicating a more robust resource base for the mine.

- Near-Mine Surface Drilling: Near-mine surface drilling at Camp Bay has identified new shallow mineralization, with notable results of 37.4 meters at 1.84 g/t Au, highlighting satellite discovery potential near existing infrastructure, which could support future resource growth.

- Regional Data Compilation: Orla is advancing a regional data compilation initiative across its 65,000-hectare Musselwhite land package to identify high-priority drill targets, aiming to unlock belt-scale potential and support long-term resource development strategies.

See More

Orla Mining Reports Strong Q4 2025 Earnings

- Gold Production Surge: Orla Mining Ltd achieved nearly 76,000 ounces of gold production in Q4 2025, more than doubling its output from the previous year, demonstrating the success of its Musselwhite mine acquisition and solidifying its market position.

- Strong Financial Performance: The company reported revenues of $378 million and net income of $79 million in Q4 2025, with adjusted earnings per share at $0.42, alongside robust cash flow from operating activities of $165 million, showcasing strong profitability and cash flow management.

- Optimistic Future Guidance: Orla anticipates gold production between 340,000 to 360,000 ounces in 2026, with all-in sustaining costs projected at $1,550 to $1,750 per ounce, reflecting confidence in future growth and clear strategic planning.

- Environmental Approval Progress: The company received environmental impact statement approval for the Camino Rojo project, facilitating further development, although it faces high mining costs and significant capital expenditure plans, indicating a commitment to sustainable development.

See More

Orla Mining Q4 Earnings Exceed Expectations

- Earnings Beat: Orla Mining reported a Q4 non-GAAP EPS of $0.42, surpassing expectations by $0.08, which indicates a significant improvement in profitability and boosts investor confidence.

- Revenue Surge: The company achieved Q4 revenue of $378.5 million, reflecting a staggering 307.9% year-over-year increase and exceeding forecasts by $90.5 million, showcasing its strong performance in gold production and sustained market demand.

- Record Production: Orla Mining's quarterly production reached an all-time high, further solidifying its position as a de-risked gold producer, which is likely to attract increased investor interest.

- Dividend Scorecard: The dividend scorecard for Orla Mining indicates stable cash flow and profitability, potentially supporting future shareholder returns and enhancing the company's appeal among investors.

See More

Orla Mining Reports Record $133 Million Free Cash Flow for 2025

- Record Cash Flow: Orla Mining achieved a record free cash flow of $133 million in 2025, supporting its self-funded growth model and demonstrating strong financial performance and sustainability in the gold mining sector.

- Production Exceeds Expectations: The total gold production for 2025 reached 300,620 ounces, surpassing guidance, indicating the company's success in resource development and production efficiency, further solidifying its market position.

- Effective Cost Control: The all-in sustaining cost (AISC) for Q4 was $1,536 per ounce, with an annual AISC of $1,458, both within guidance, showcasing the company's excellence in cost management and operational efficiency.

- Ongoing Project Investment: The company reported exploration and project expenditures of $43.9 million in Q4, with $31.6 million capitalized, reflecting Orla's continued investment in future growth and confidence in resource potential.

See More

ORLA Ranks High Among Analysts in Metals Sector

- Analyst Ranking Methodology: The ranking of the Metals Channel Global Mining Titans Index was formed by averaging analyst opinions from major brokerages, indicating a growing interest in ORLA, which, despite its lower rank, suggests potential for upside.

- Market Performance Comparison: ORLA is currently trading up about 5.5%, outperforming peers like Newmont Corp (up about 3%) and Barrick Mining Corp (up about 2.9%), highlighting its relative strength in the precious metals sector and potentially attracting more investor interest.

- Diverse Investor Interpretations: Although ORLA ranks low among analysts, investors can interpret this as an opportunity for upside, indicating a divergence in market sentiment that may benefit bullish investors looking for contrarian plays.

- Price History Analysis: A three-month price history chart comparing ORLA with NEM and B is provided, further illustrating ORLA's performance trends in the precious metals market, aiding investors in making more informed decisions.

See More

Orla Mining on Track for 2026 Gold Production Guidance

- Stable Gold Production: Orla Mining confirmed its 2026 gold production guidance of 340,000 to 360,000 ounces, with Q1 total production reaching 81,206 ounces and sales slightly higher at 81,540 ounces, indicating a stable performance in the gold market.

- Musselwhite Mine Performance: At the Musselwhite mine, 333,495 tonnes of ore were mined and 332,822 tonnes processed in Q1, with a mill head grade of 6.29 g/t gold and a recovery rate of 95.91%, resulting in gold production of 62,985 ounces.

- Strong Cash Position: As of March 31, 2026, Orla's cash and debt stood at $427.3 million and $331.3 million, respectively, yielding a net cash position of $96.0 million, reflecting the company's financial robustness that supports future investments and expansions.

- Strategic Growth Outlook: CEO Jason Simpson noted that 2026 is a catalyst-rich year, and the strong start suggests the company is poised for further growth and development in the coming months.

See More

Orla Mining Expands Musselwhite Mine Potential with New Discoveries

- Mine Potential Expansion: Orla Mining's directional drilling at the Musselwhite Mine has uncovered new high-grade gold mineralization, indicating that the Lynx and PQ zones extend over two kilometers, significantly enhancing resource potential and possibly extending the mine's lifespan.

- Underground Drilling Results: Ongoing underground drilling continues to return strong gold intercepts, including 11.5 meters at 11.0 g/t Au, reinforcing confidence in resource growth and reserve replacement, indicating a more robust resource base for the mine.

- Near-Mine Surface Drilling: Near-mine surface drilling at Camp Bay has identified new shallow mineralization, with notable results of 37.4 meters at 1.84 g/t Au, highlighting satellite discovery potential near existing infrastructure, which could support future resource growth.

- Regional Data Compilation: Orla is advancing a regional data compilation initiative across its 65,000-hectare Musselwhite land package to identify high-priority drill targets, aiming to unlock belt-scale potential and support long-term resource development strategies.

See More

Orla Mining Reports Strong Q4 2025 Earnings

- Gold Production Surge: Orla Mining Ltd achieved nearly 76,000 ounces of gold production in Q4 2025, more than doubling its output from the previous year, demonstrating the success of its Musselwhite mine acquisition and solidifying its market position.

- Strong Financial Performance: The company reported revenues of $378 million and net income of $79 million in Q4 2025, with adjusted earnings per share at $0.42, alongside robust cash flow from operating activities of $165 million, showcasing strong profitability and cash flow management.

- Optimistic Future Guidance: Orla anticipates gold production between 340,000 to 360,000 ounces in 2026, with all-in sustaining costs projected at $1,550 to $1,750 per ounce, reflecting confidence in future growth and clear strategic planning.

- Environmental Approval Progress: The company received environmental impact statement approval for the Camino Rojo project, facilitating further development, although it faces high mining costs and significant capital expenditure plans, indicating a commitment to sustainable development.

See More

Orla Mining Q4 Earnings Exceed Expectations

- Earnings Beat: Orla Mining reported a Q4 non-GAAP EPS of $0.42, surpassing expectations by $0.08, which indicates a significant improvement in profitability and boosts investor confidence.

- Revenue Surge: The company achieved Q4 revenue of $378.5 million, reflecting a staggering 307.9% year-over-year increase and exceeding forecasts by $90.5 million, showcasing its strong performance in gold production and sustained market demand.

- Record Production: Orla Mining's quarterly production reached an all-time high, further solidifying its position as a de-risked gold producer, which is likely to attract increased investor interest.

- Dividend Scorecard: The dividend scorecard for Orla Mining indicates stable cash flow and profitability, potentially supporting future shareholder returns and enhancing the company's appeal among investors.

See More

Orla Mining Reports Record $133 Million Free Cash Flow for 2025

- Record Cash Flow: Orla Mining achieved a record free cash flow of $133 million in 2025, supporting its self-funded growth model and demonstrating strong financial performance and sustainability in the gold mining sector.

- Production Exceeds Expectations: The total gold production for 2025 reached 300,620 ounces, surpassing guidance, indicating the company's success in resource development and production efficiency, further solidifying its market position.

- Effective Cost Control: The all-in sustaining cost (AISC) for Q4 was $1,536 per ounce, with an annual AISC of $1,458, both within guidance, showcasing the company's excellence in cost management and operational efficiency.

- Ongoing Project Investment: The company reported exploration and project expenditures of $43.9 million in Q4, with $31.6 million capitalized, reflecting Orla's continued investment in future growth and confidence in resource potential.

See More