Nvidia Rallies as CEO Huang Joins Trump’s China Delegation

Written by Emily J. Thompson, Senior Investment Analyst

Updated: May 13 2026

0mins

Source: stocktwits

- Nvidia Stock Surge: Nvidia (NVDA) shares rose 1% as CEO Jensen Huang joined President Trump's China delegation, igniting investor optimism ahead of its upcoming earnings report, reflecting strong market sentiment regarding its business prospects in China.

- Wall Street Backing: Susquehanna raised Nvidia's price target from $250 to $275, indicating a potential 25% upside, while Wells Fargo increased its target to $315, suggesting that despite margin and market share concerns, durable AI demand will continue to support the stock.

- Defense Spending Boosts RTX: RTX shares gained as defense spending rises, with Collins Aerospace announcing a $26.5 million expansion of its radar production facility in Florida, expected to create over 100 skilled jobs and enhance its competitive position in the defense sector.

- Broadwind Exceeds Expectations: Broadwind (BWEN) reported Q1 revenue of $34.06 million, surpassing analyst estimates, with total orders reaching $37.4 million, indicating strong demand for AI data centers and natural gas power generation, with the CEO noting the beginning of a super cycle.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy NVDA?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on NVDA

Wall Street analysts forecast NVDA stock price to rise

41 Analyst Rating

39 Buy

1 Hold

1 Sell

Strong Buy

Current: 196.930

Low

200.00

Averages

264.97

High

352.00

Current: 196.930

Low

200.00

Averages

264.97

High

352.00

About NVDA

NVIDIA Corporation is an artificial intelligence (AI) infrastructure company. The Company is engaged in accelerated computing to help solve the challenging computational problems. Its segments include Compute & Networking and Graphics. The Compute & Networking segment includes its Data Center accelerated computing and networking platforms and AI solutions and software, and automotive platforms and autonomous and electric vehicle solutions, including software. The Graphics segment includes GeForce GPUs for gaming and personal computers (PCs), and Quadro/NVIDIA RTX GPUs for enterprise workstation graphics. Its technology stack includes the foundational NVIDIA CUDA development platform that runs on all NVIDIA GPUs, as well as hundreds of domain-specific software libraries, frameworks, algorithms, software development kits (SDKs), and application programming interfaces (APIs). Its platforms address four markets, which include Data Center, Gaming, Professional Visualization, and Automotive.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Nvidia's New Revenue Source: Orbital Data Centers

- Stock Performance: In the first half of 2026, Nvidia's stock price rose only 5%, from $189.84 on January 2 to $200 on June 30, reflecting cautious investor sentiment despite an impressive 859% increase over the past five years.

- Space Market Opportunity: Nvidia is set to become the initial hardware supplier for SpaceX's orbital data centers, which could open new revenue streams for the company amid growing demand for AI computing capabilities.

- AI Computing Module Launch: Nvidia plans to launch the Vera Rubin Space-1 Module, which will perform AI computing directly in space, enhancing real-time decision-making and marking a significant expansion into space technology that could transform future data processing.

- Investor Expectation Adjustment: While Nvidia remains a key player in the AI sector, investors should maintain reasonable expectations for future returns due to the high baseline set by past performance, avoiding excessive hopes for significant stock price increases.

See More

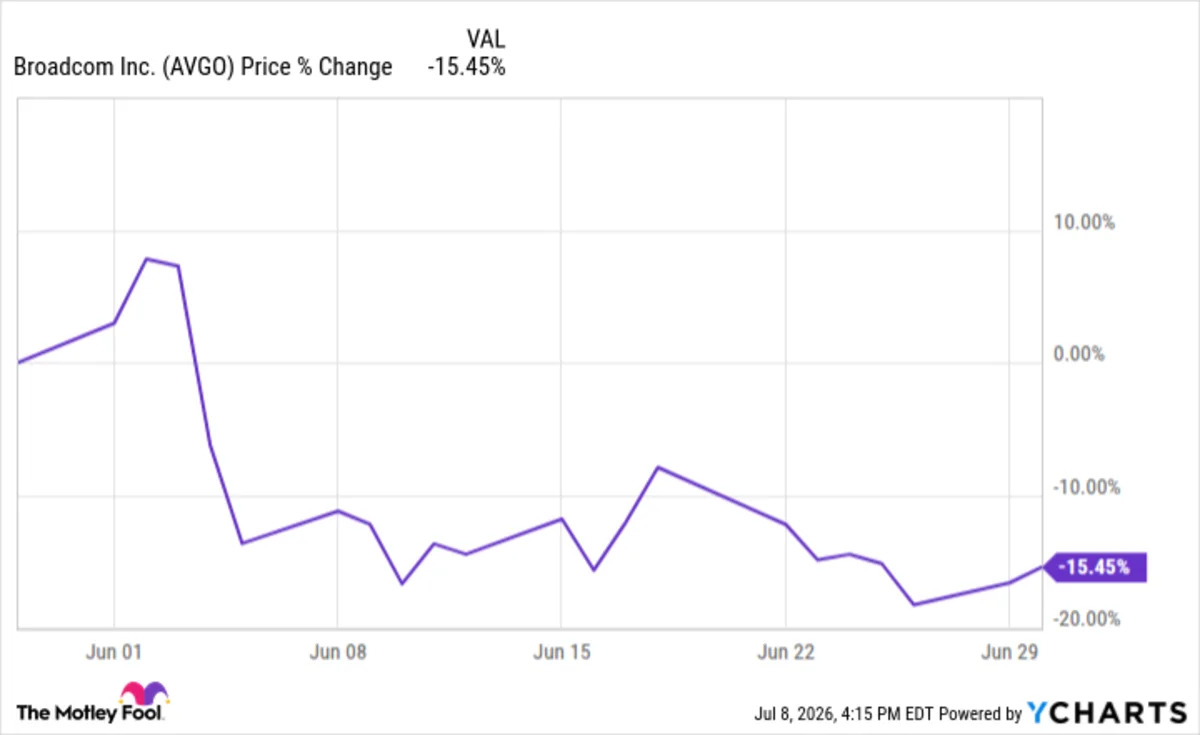

Broadcom Shares Drop 15% in June Amid AI Revenue Concerns

- Earnings Performance: Broadcom reported a 48% revenue increase to $22.2 billion in Q2, with adjusted EPS rising from $1.58 to $2.44, slightly beating expectations; however, concerns arose as AI revenue growth did not meet market forecasts, leading to a stock decline.

- AI Revenue Dynamics: The company's AI-related revenue surged 143% to $10.8 billion, but the forecast for Q3 at $16 billion fell short of the $17 billion expected, indicating market apprehension about future growth prospects.

- Market Reaction: Following the earnings report, Broadcom's stock plummeted 15% due to investor concerns over high valuations and overspending on AI infrastructure, reflecting a diminished confidence in the company's growth trajectory.

- Strategic Partnership: Broadcom signed a $30 billion deal with Apple for chip manufacturing, with Apple investing $1.5 billion to expand a Colorado facility, potentially providing new growth avenues for Broadcom, although the market remains cautious about long-term sustainability.

See More

India's IPO Market Faces Major Risks Amid Geopolitical Tensions

- IPO Plans Under Threat: Trump's decision to end the ceasefire with Iran poses significant risks to India's anticipated $50 billion IPO pipeline, causing a more than 2% market slump and highlighting the increasing impact of geopolitical risks on financial markets.

- Weak Market Performance: IPO activity in India for 2026 has been lackluster compared to the U.S. and Hong Kong, raising only $4 billion in the first half, in stark contrast to the $128 billion and $27 billion raised in those markets, indicating insufficient market absorption for new listings.

- Regulatory Approval Progress: Approximately $22 billion worth of IPOs are seeking regulatory approval, expected to take 2-3 months, while $29 billion worth have already been approved, including major firms like Zepto and Avaada Electro, suggesting potential opportunities still exist in the market.

- Economic Transformation Context: India's economy is transforming with the rise of new manufacturing industries driven by digital technology adoption and tax reforms, and despite unfavorable market conditions, companies are still seeking to list to unlock growth potential, reflecting confidence in future prospects.

See More

Oil Prices Surge Amid Tech Stock Volatility

- Oil Price Surge: Brent crude futures surpassed $80 on Wednesday, primarily driven by U.S. military actions against Iran, with the energy sector being the top performer of the day, up 1.45%, indicating strong market reactions to energy demand.

- Tech Stock Volatility: Nvidia's stock is down 14% from its May high, while AMD, Applied Materials, and Micron Technology have seen declines of 11.5%, 22%, and 24% respectively, reflecting investor caution towards tech stocks that may influence future investment decisions.

- PepsiCo Earnings Preview: PepsiCo is set to report earnings on Thursday, with its stock down about 8% over the past three months and 17% from its 52-week high, which could affect market perceptions of its future growth potential.

- Blue Origin Funding: Jeff Bezos' Blue Origin secured a $4 billion investment from Coatue Management as part of a new $10 billion fundraising round, expected to value the company at $130 billion, showcasing the investment enthusiasm and growth potential in the space industry.

See More

Market Warning Amid AI Boom

- Market Performance Review: The S&P 500 has surged in recent years due to the AI boom, with investors seeing potential for transformative changes in business and daily life, resulting in triple-digit gains for related stocks over the past three years.

- Investor Caution: Despite ongoing growth in AI stocks, geopolitical tensions and rising inflation have prompted investors to shift towards safer sectors like healthcare, leading to a more cautious sentiment towards AI companies, especially following the new Federal Reserve chair's appointment.

- Valuation Warning Signal: The S&P 500 Shiller CAPE ratio recently surpassed 41, a level only seen once in 155 years, mirroring the dot-com bubble, indicating that current stock valuations are extremely high and may face downward pressure.

- Long-Term Investment Outlook: While a decline may be imminent, history shows that holding quality stocks for the long term typically results in investment success, as the S&P 500 has historically recovered and advanced after downturns, suggesting a bright outlook for long-term investors.

See More

Analysis of Nvidia and Broadcom Stock Price Pullback

- Stock Price Pullback: Nvidia's stock has fallen approximately 18.5% and Broadcom's by 24.4%, reflecting market volatility in AI investment sentiment, although both companies remain key investment targets in AI computing infrastructure.

- Future Growth Potential: Broadcom projects AI semiconductor revenue to exceed $100 billion by 2027, with analysts estimating total revenue to reach $172 billion, a 62% increase from this year, indicating strong market demand and growth potential.

- Investment Opportunities: Nvidia anticipates capital expenditures from AI hyperscalers to surpass $1 trillion next year, up from $650 billion in 2026, demonstrating long-term investment confidence in AI technology.

- Valuation Attractiveness: Given the rapid growth of Broadcom and Nvidia, using forward price-to-earnings ratios for valuation is crucial, and current stock prices present a great buying opportunity, especially as AI hyperscalers confirm their spending plans, which could act as a catalyst for stock price increases.

See More

Nvidia's New Revenue Source: Orbital Data Centers

- Stock Performance: In the first half of 2026, Nvidia's stock price rose only 5%, from $189.84 on January 2 to $200 on June 30, reflecting cautious investor sentiment despite an impressive 859% increase over the past five years.

- Space Market Opportunity: Nvidia is set to become the initial hardware supplier for SpaceX's orbital data centers, which could open new revenue streams for the company amid growing demand for AI computing capabilities.

- AI Computing Module Launch: Nvidia plans to launch the Vera Rubin Space-1 Module, which will perform AI computing directly in space, enhancing real-time decision-making and marking a significant expansion into space technology that could transform future data processing.

- Investor Expectation Adjustment: While Nvidia remains a key player in the AI sector, investors should maintain reasonable expectations for future returns due to the high baseline set by past performance, avoiding excessive hopes for significant stock price increases.

See More

Broadcom Shares Drop 15% in June Amid AI Revenue Concerns

- Earnings Performance: Broadcom reported a 48% revenue increase to $22.2 billion in Q2, with adjusted EPS rising from $1.58 to $2.44, slightly beating expectations; however, concerns arose as AI revenue growth did not meet market forecasts, leading to a stock decline.

- AI Revenue Dynamics: The company's AI-related revenue surged 143% to $10.8 billion, but the forecast for Q3 at $16 billion fell short of the $17 billion expected, indicating market apprehension about future growth prospects.

- Market Reaction: Following the earnings report, Broadcom's stock plummeted 15% due to investor concerns over high valuations and overspending on AI infrastructure, reflecting a diminished confidence in the company's growth trajectory.

- Strategic Partnership: Broadcom signed a $30 billion deal with Apple for chip manufacturing, with Apple investing $1.5 billion to expand a Colorado facility, potentially providing new growth avenues for Broadcom, although the market remains cautious about long-term sustainability.

See More

India's IPO Market Faces Major Risks Amid Geopolitical Tensions

- IPO Plans Under Threat: Trump's decision to end the ceasefire with Iran poses significant risks to India's anticipated $50 billion IPO pipeline, causing a more than 2% market slump and highlighting the increasing impact of geopolitical risks on financial markets.

- Weak Market Performance: IPO activity in India for 2026 has been lackluster compared to the U.S. and Hong Kong, raising only $4 billion in the first half, in stark contrast to the $128 billion and $27 billion raised in those markets, indicating insufficient market absorption for new listings.

- Regulatory Approval Progress: Approximately $22 billion worth of IPOs are seeking regulatory approval, expected to take 2-3 months, while $29 billion worth have already been approved, including major firms like Zepto and Avaada Electro, suggesting potential opportunities still exist in the market.

- Economic Transformation Context: India's economy is transforming with the rise of new manufacturing industries driven by digital technology adoption and tax reforms, and despite unfavorable market conditions, companies are still seeking to list to unlock growth potential, reflecting confidence in future prospects.

See More

Oil Prices Surge Amid Tech Stock Volatility

- Oil Price Surge: Brent crude futures surpassed $80 on Wednesday, primarily driven by U.S. military actions against Iran, with the energy sector being the top performer of the day, up 1.45%, indicating strong market reactions to energy demand.

- Tech Stock Volatility: Nvidia's stock is down 14% from its May high, while AMD, Applied Materials, and Micron Technology have seen declines of 11.5%, 22%, and 24% respectively, reflecting investor caution towards tech stocks that may influence future investment decisions.

- PepsiCo Earnings Preview: PepsiCo is set to report earnings on Thursday, with its stock down about 8% over the past three months and 17% from its 52-week high, which could affect market perceptions of its future growth potential.

- Blue Origin Funding: Jeff Bezos' Blue Origin secured a $4 billion investment from Coatue Management as part of a new $10 billion fundraising round, expected to value the company at $130 billion, showcasing the investment enthusiasm and growth potential in the space industry.

See More

Market Warning Amid AI Boom

- Market Performance Review: The S&P 500 has surged in recent years due to the AI boom, with investors seeing potential for transformative changes in business and daily life, resulting in triple-digit gains for related stocks over the past three years.

- Investor Caution: Despite ongoing growth in AI stocks, geopolitical tensions and rising inflation have prompted investors to shift towards safer sectors like healthcare, leading to a more cautious sentiment towards AI companies, especially following the new Federal Reserve chair's appointment.

- Valuation Warning Signal: The S&P 500 Shiller CAPE ratio recently surpassed 41, a level only seen once in 155 years, mirroring the dot-com bubble, indicating that current stock valuations are extremely high and may face downward pressure.

- Long-Term Investment Outlook: While a decline may be imminent, history shows that holding quality stocks for the long term typically results in investment success, as the S&P 500 has historically recovered and advanced after downturns, suggesting a bright outlook for long-term investors.

See More

Analysis of Nvidia and Broadcom Stock Price Pullback

- Stock Price Pullback: Nvidia's stock has fallen approximately 18.5% and Broadcom's by 24.4%, reflecting market volatility in AI investment sentiment, although both companies remain key investment targets in AI computing infrastructure.

- Future Growth Potential: Broadcom projects AI semiconductor revenue to exceed $100 billion by 2027, with analysts estimating total revenue to reach $172 billion, a 62% increase from this year, indicating strong market demand and growth potential.

- Investment Opportunities: Nvidia anticipates capital expenditures from AI hyperscalers to surpass $1 trillion next year, up from $650 billion in 2026, demonstrating long-term investment confidence in AI technology.

- Valuation Attractiveness: Given the rapid growth of Broadcom and Nvidia, using forward price-to-earnings ratios for valuation is crucial, and current stock prices present a great buying opportunity, especially as AI hyperscalers confirm their spending plans, which could act as a catalyst for stock price increases.

See More