Netflix Executives Offload Nearly $40 Million in Shares

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Mar 04 2026

0mins

Source: seekingalpha

- Executive Sell-off: Netflix director Reed Hastings sold 410,550 shares this week for a total of $39.89 million, with prices ranging from $96.05 to $97.59, indicating a strategic response to market fluctuations while reflecting confidence in the company's performance.

- Options Exercise: On the same day, Hastings exercised options to purchase 410,550 shares at $9.667 each, totaling $3.97 million, suggesting he remains optimistic about Netflix's long-term prospects despite the recent sell-off.

- CFO Divestment: CFO Adam Neumann also sold $8.25 million worth of shares, further illustrating the executives' asset allocation strategies during a period of rising stock prices, potentially to realize some gains.

- Compliance with Trading Plan: Both executives' transactions were executed under a Rule 10b5-1 trading plan, which allows key shareholders to pre-schedule sales to mitigate insider trading concerns, thereby ensuring market transparency and compliance.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy NFLX?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on NFLX

Wall Street analysts forecast NFLX stock price to rise

38 Analyst Rating

27 Buy

10 Hold

1 Sell

Moderate Buy

Current: 88.090

Low

92.00

Averages

114.18

High

150.00

Current: 88.090

Low

92.00

Averages

114.18

High

150.00

About NFLX

Netflix, Inc. is a provider of entertainment services. The Company acquires, licenses and produces content, including original programming. It provides paid memberships in over 190 countries offering television (TV) series, films and games across a variety of genres and languages. It allows members to play, pause and resume watching as much as they want, anytime, anywhere, and can change their plans at any time. The Company offers members the ability to receive streaming content through a host of Internet-connected devices, including TVs, digital video players, TV set-top boxes and mobile devices. It is engaged in scaling its streaming service, such as introducing games and advertising on its service, as well as offering live programming. It is developing technology and utilizing third-party cloud computing, technology and other services. The Company is also engaged in scaling its own studio operations to produce original content.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Netflix to Live Stream The Breakfast Club Podcast Starting June 1

- First Live Program: Netflix will begin live streaming Charlamagne Tha God’s The Breakfast Club podcast on June 1, marking the streaming giant's first daily live program, which is expected to attract a significant number of new users and enhance user engagement.

- Innovative Content: The podcast will feature three hours of uninterrupted programming, with regular commercial breaks replaced by exclusive bonus segments and extended interviews, aimed at improving user experience and increasing viewer retention.

- Large Audience Base: Since the beginning of the year, The Breakfast Club has aired on a delayed basis under a programming agreement with iHeartMedia, boasting approximately 6.6 million weekly terrestrial listeners and over 1 billion downloads, demonstrating its substantial market influence.

- Strategic Partnership Continuation: iHeartMedia recently extended its contract with Charlamagne Tha God for another five years, further solidifying their partnership and providing Netflix with a stable content source, thereby enhancing its competitive edge in the podcasting space.

See More

Analysis of Netflix and Booking Stock Splits and Future Prospects

- Netflix Stock Split: Netflix executed a 10-for-1 stock split on November 17, with shares currently trading around $88, reflecting a 25% decline over the past year due to disappointing financial guidance that sharply impacted stock prices, necessitating investor vigilance regarding future market performance.

- Market Potential: Despite challenges, Netflix's penetration in the U.S. streaming market is still below 50%, and the company plans to enhance market share by venturing into live sports and long-form video podcasts, thereby boosting user engagement and revenue growth.

- Booking Stock Split: Booking Holdings conducted a 25-for-1 stock split on April 6, adjusting shares from above $4,000, and while facing potential disruptions from AI, the company sees significant growth opportunities, particularly in the fast-growing Asian travel market.

- Competitive Advantage: Booking Holdings benefits from strong network effects and a diversified service ecosystem that attracts more travelers to its platform, and despite a 25% drop in stock price over the past year, its market position and future growth opportunities still make it an attractive investment.

See More

Analysis of Netflix and Booking Stock Splits

- Netflix Stock Split: Netflix executed a 10-for-1 stock split on November 17, yet this move failed to prevent a 25% decline in its stock price over the past year, currently trading around $88, reflecting investor disappointment following weak financial guidance.

- Market Potential: Despite challenges, Netflix still has a massive addressable market in the U.S. streaming industry, which commands less than 50% of television viewing time, and it aims to capture market share by expanding into live sports and long-form video podcasts.

- Booking Stock Split: Booking Holdings conducted a 25-for-1 stock split on April 6, which was well-received despite CEO Glenn Fogel's previous reluctance to attract investors deterred by high share prices, as shares were trading above $4,000.

- Competitive Edge: Booking Holdings possesses a strong competitive advantage in the global travel market, particularly in Asia, and despite a 25% drop in stock price, the company is leveraging AI tools to enhance service quality, indicating solid performance potential over the next decade.

See More

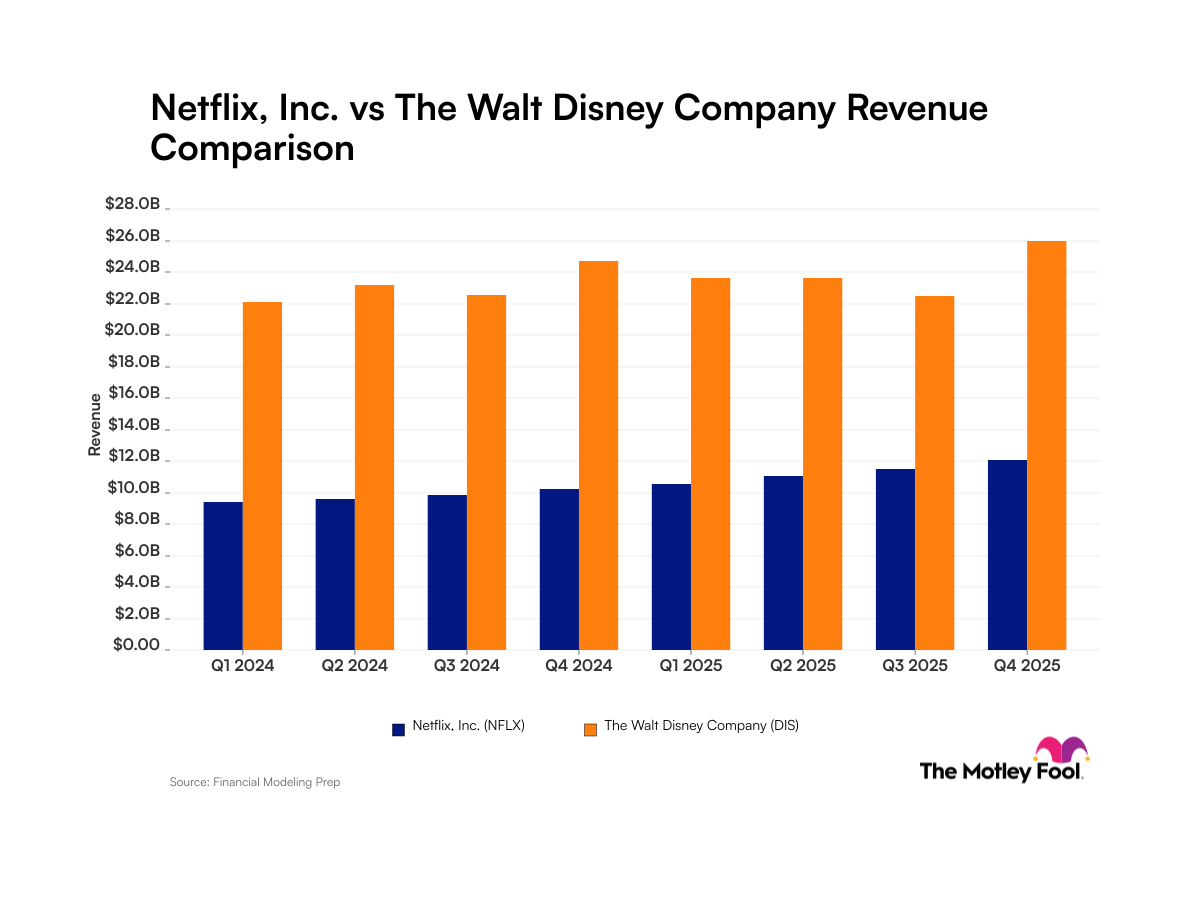

Comparison of Netflix and Disney Financial Reports

- Netflix Revenue Growth: In Q1 2026, Netflix reported revenue of $12.2 billion, marking a 16% year-over-year increase, while its earnings per share surged from $0.66 to $1.23, demonstrating strong performance and financial stability in the streaming market.

- Disney's Financial Challenges: Disney's revenue for Q2 2026 reached $25.2 billion, up 7% year-over-year, but its earnings per share fell 30% to $1.27, and free cash flow decreased by 1% to $4.9 billion, indicating vulnerabilities in its financial health.

- Market Competition Dynamics: While Disney's diversified business includes theme parks and cruise ships, its sales growth is more volatile compared to Netflix's pure streaming model, highlighting significant differences in market positioning and business strategies between the two companies.

- Impact of New CEO: The appointment of Josh D'Amaro as Disney's new CEO signifies a transition for the company, suggesting that investors should view Disney as a different type of company compared to Netflix to better understand its future growth potential.

See More

Rising AI Costs Impact IPO Valuations for OpenAI and Anthropic

- AI Cost Pressure: Companies like Meta, Shopify, Spotify, and Pinterest have reported rising AI and inference costs as a drag on margins, with Shopify noting that economies of scale were partially offset by increased LLM costs, highlighting the profitability challenges faced across the industry.

- Intensifying Market Competition: As Chinese labs offer competitive models at lower prices, the IPO valuations for OpenAI and Anthropic, projected to exceed $800 billion, face pressure, as the assumptions regarding market share and pricing power are increasingly challenged.

- Shifts in Enterprise Budgets: A survey by CloudZero indicates that by 2025, over 45% of companies will spend more than $100,000 monthly on AI, a significant increase from the previous year, demonstrating a growing commitment to AI investments among enterprises.

- Accelerated Technological Transformation: The CEO of Databricks noted that enterprises are adopting an

See More

Can Netflix Evolve into a Trillion-Dollar Company?

- Shift in Profit Model: Netflix is gradually transitioning to a profitability model by consistently raising subscription prices, having done so almost every year for the past decade, which not only boosts revenue from existing users but also lays the groundwork for future profit growth.

- Advertising Revenue Potential: With over 250 million active users on its ad-supported plans, Netflix's advertising business could become a significant second revenue stream, fundamentally altering the long-term profitability equation.

- Operating Margin Improvement: Currently boasting an operating margin above 30%, Netflix is expected to enhance this further as its advertising business scales, and if it can continue to grow revenue while expanding margins, earnings growth could outpace revenue growth.

- New Business Opportunities: Netflix has potential growth avenues in live programming, gaming, and physical experiences, and while these do not need to be massive successes, even one meaningful initiative could provide additional growth momentum for the company.

See More

Netflix to Live Stream The Breakfast Club Podcast Starting June 1

- First Live Program: Netflix will begin live streaming Charlamagne Tha God’s The Breakfast Club podcast on June 1, marking the streaming giant's first daily live program, which is expected to attract a significant number of new users and enhance user engagement.

- Innovative Content: The podcast will feature three hours of uninterrupted programming, with regular commercial breaks replaced by exclusive bonus segments and extended interviews, aimed at improving user experience and increasing viewer retention.

- Large Audience Base: Since the beginning of the year, The Breakfast Club has aired on a delayed basis under a programming agreement with iHeartMedia, boasting approximately 6.6 million weekly terrestrial listeners and over 1 billion downloads, demonstrating its substantial market influence.

- Strategic Partnership Continuation: iHeartMedia recently extended its contract with Charlamagne Tha God for another five years, further solidifying their partnership and providing Netflix with a stable content source, thereby enhancing its competitive edge in the podcasting space.

See More

Analysis of Netflix and Booking Stock Splits and Future Prospects

- Netflix Stock Split: Netflix executed a 10-for-1 stock split on November 17, with shares currently trading around $88, reflecting a 25% decline over the past year due to disappointing financial guidance that sharply impacted stock prices, necessitating investor vigilance regarding future market performance.

- Market Potential: Despite challenges, Netflix's penetration in the U.S. streaming market is still below 50%, and the company plans to enhance market share by venturing into live sports and long-form video podcasts, thereby boosting user engagement and revenue growth.

- Booking Stock Split: Booking Holdings conducted a 25-for-1 stock split on April 6, adjusting shares from above $4,000, and while facing potential disruptions from AI, the company sees significant growth opportunities, particularly in the fast-growing Asian travel market.

- Competitive Advantage: Booking Holdings benefits from strong network effects and a diversified service ecosystem that attracts more travelers to its platform, and despite a 25% drop in stock price over the past year, its market position and future growth opportunities still make it an attractive investment.

See More

Analysis of Netflix and Booking Stock Splits

- Netflix Stock Split: Netflix executed a 10-for-1 stock split on November 17, yet this move failed to prevent a 25% decline in its stock price over the past year, currently trading around $88, reflecting investor disappointment following weak financial guidance.

- Market Potential: Despite challenges, Netflix still has a massive addressable market in the U.S. streaming industry, which commands less than 50% of television viewing time, and it aims to capture market share by expanding into live sports and long-form video podcasts.

- Booking Stock Split: Booking Holdings conducted a 25-for-1 stock split on April 6, which was well-received despite CEO Glenn Fogel's previous reluctance to attract investors deterred by high share prices, as shares were trading above $4,000.

- Competitive Edge: Booking Holdings possesses a strong competitive advantage in the global travel market, particularly in Asia, and despite a 25% drop in stock price, the company is leveraging AI tools to enhance service quality, indicating solid performance potential over the next decade.

See More

Comparison of Netflix and Disney Financial Reports

- Netflix Revenue Growth: In Q1 2026, Netflix reported revenue of $12.2 billion, marking a 16% year-over-year increase, while its earnings per share surged from $0.66 to $1.23, demonstrating strong performance and financial stability in the streaming market.

- Disney's Financial Challenges: Disney's revenue for Q2 2026 reached $25.2 billion, up 7% year-over-year, but its earnings per share fell 30% to $1.27, and free cash flow decreased by 1% to $4.9 billion, indicating vulnerabilities in its financial health.

- Market Competition Dynamics: While Disney's diversified business includes theme parks and cruise ships, its sales growth is more volatile compared to Netflix's pure streaming model, highlighting significant differences in market positioning and business strategies between the two companies.

- Impact of New CEO: The appointment of Josh D'Amaro as Disney's new CEO signifies a transition for the company, suggesting that investors should view Disney as a different type of company compared to Netflix to better understand its future growth potential.

See More

Rising AI Costs Impact IPO Valuations for OpenAI and Anthropic

- AI Cost Pressure: Companies like Meta, Shopify, Spotify, and Pinterest have reported rising AI and inference costs as a drag on margins, with Shopify noting that economies of scale were partially offset by increased LLM costs, highlighting the profitability challenges faced across the industry.

- Intensifying Market Competition: As Chinese labs offer competitive models at lower prices, the IPO valuations for OpenAI and Anthropic, projected to exceed $800 billion, face pressure, as the assumptions regarding market share and pricing power are increasingly challenged.

- Shifts in Enterprise Budgets: A survey by CloudZero indicates that by 2025, over 45% of companies will spend more than $100,000 monthly on AI, a significant increase from the previous year, demonstrating a growing commitment to AI investments among enterprises.

- Accelerated Technological Transformation: The CEO of Databricks noted that enterprises are adopting an

See More

Can Netflix Evolve into a Trillion-Dollar Company?

- Shift in Profit Model: Netflix is gradually transitioning to a profitability model by consistently raising subscription prices, having done so almost every year for the past decade, which not only boosts revenue from existing users but also lays the groundwork for future profit growth.

- Advertising Revenue Potential: With over 250 million active users on its ad-supported plans, Netflix's advertising business could become a significant second revenue stream, fundamentally altering the long-term profitability equation.

- Operating Margin Improvement: Currently boasting an operating margin above 30%, Netflix is expected to enhance this further as its advertising business scales, and if it can continue to grow revenue while expanding margins, earnings growth could outpace revenue growth.

- New Business Opportunities: Netflix has potential growth avenues in live programming, gaming, and physical experiences, and while these do not need to be massive successes, even one meaningful initiative could provide additional growth momentum for the company.

See More