Microsoft Shares Rebound Over 10% Amid Tech Rotation

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 2 hours ago

0mins

Should l Buy MSFT?

Source: seekingalpha

- Price Recovery: Microsoft (MSFT) shares have rebounded over 10% in the past month, currently trading around $412.66, although they remain down approximately 14.6% year-to-date, indicating renewed investor interest in large-cap tech stocks.

- Technical Analysis: Technical traders have noted that after a sharp rally in late April, Microsoft's recent consolidation appears to form a potential bullish flag, suggesting a pause within a broader upward trend.

- Support Levels: The stock continues to trade above its rising 50-day moving average, a key level monitored by institutional investors for assessing intermediate-term momentum, while also holding above a previously established downtrend line, indicating easing selling pressure.

- Market Sentiment: The recent upward movement is supported by ongoing enthusiasm surrounding artificial intelligence infrastructure spending and enterprise software demand, which continues to bolster sentiment across the technology sector.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy MSFT?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on MSFT

Wall Street analysts forecast MSFT stock price to rise

34 Analyst Rating

32 Buy

2 Hold

0 Sell

Strong Buy

Current: 412.660

Low

500.00

Averages

631.36

High

678.00

Current: 412.660

Low

500.00

Averages

631.36

High

678.00

About MSFT

Microsoft Corporation is a technology company. The Company develops and supports software, services, devices, and solutions. The Company’s segments include Productivity and Business Processes, Intelligent Cloud, and More Personal Computing. The Productivity and Business Processes segment consists of products and services in its portfolio of productivity, communication, and information services. This segment primarily comprises: Office Commercial, Office Consumer, LinkedIn, and Dynamics business solutions. The Intelligent Cloud segment consists of server products and cloud services, including Azure and other cloud services, SQL Server, Windows Server, Visual Studio, System Center, and related Client Access Licenses (CALs), and Nuance and GitHub; and Enterprise Services, including enterprise support services, industry solutions and Nuance professional services. The More Personal Computing segment primarily comprises Windows, Devices, Gaming, and search and news advertising.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Microsoft's East Africa Data Center Delayed

- Project Delay Reason: Microsoft's data center construction in Kenya has been delayed due to disagreements with the government over payment guarantees, highlighting the policy challenges the company faces in expanding its cloud computing services.

- Investment Scale: Microsoft, in partnership with UAE-based AI firm G42, plans to invest $1 billion in Kenya to enhance cloud capabilities in East Africa, but the government failed to provide the necessary payment guarantees.

- Negotiation Breakdown: The parties requested the Kenyan government to commit to annual payments for a certain capacity, but talks broke down when the government could not meet Microsoft's demands, potentially impacting Microsoft's market expansion in the region.

- Strategic Implications: This incident underscores the policy risks Microsoft faces in its East African market expansion, which may delay its cloud service growth plans and affect its competitive position in a rapidly growing market.

See More

AI Drives Semiconductor Industry Growth

- Surging Market Demand: McKinsey predicts that by 2030, AI inference will account for over 50% of computing power in data centers, reflecting the urgent demand from enterprises and consumers for AI integration, thereby driving sustained growth in the semiconductor industry.

- Arm's Market Potential: Arm Holdings anticipates over $2 billion in customer demand for its AGI CPU in fiscal years 2027 and 2028, indicating strong competitiveness in the AI inference market and the potential to generate $15 billion in annual revenue over the next five years.

- Technological Innovation and Partnerships: Arm's collaboration with Meta Platforms on the AGI CPU promises to save up to $10 billion in data center capital expenditures while delivering double the computing performance of AMD and Intel's x86 processors, further solidifying its market position.

- Optimistic Financial Outlook: Arm's revenue increased by 23% to $4.92 billion in fiscal 2026, with expectations of reaching $25 billion by fiscal 2031, indicating robust growth potential, and projected earnings per share rising to $9.00, suggesting a 51% upside in stock price.

See More

GameStop's $56B eBay Bid Rejected as Unviable

- Acquisition Proposal Rejected: eBay has officially rejected GameStop's unsolicited $56 billion acquisition bid, labeling it as 'neither credible nor attractive,' with concerns over a significant funding gap and high debt load, which could undermine GameStop's market confidence.

- Financing Challenges Emerge: Despite CEO Ryan Cohen's commitment to provide $20 billion in financing, analysts warn that GameStop's $10 billion market cap makes acquiring a $48 billion giant nearly impossible without extreme equity dilution, highlighting the fragility of its financing capabilities.

- Market Reaction Tepid: Following eBay's rejection, GameStop's stock fell 2.37% in pre-market trading, indicating investor concerns about its acquisition ability, which may impact its future stock performance and market positioning.

- Unclear Strategic Direction: eBay's board reiterated its focus on luxury goods and trading cards, believing this will yield superior shareholder returns, while GameStop's acquisition intentions could distract from its core resources and strategic focus.

See More

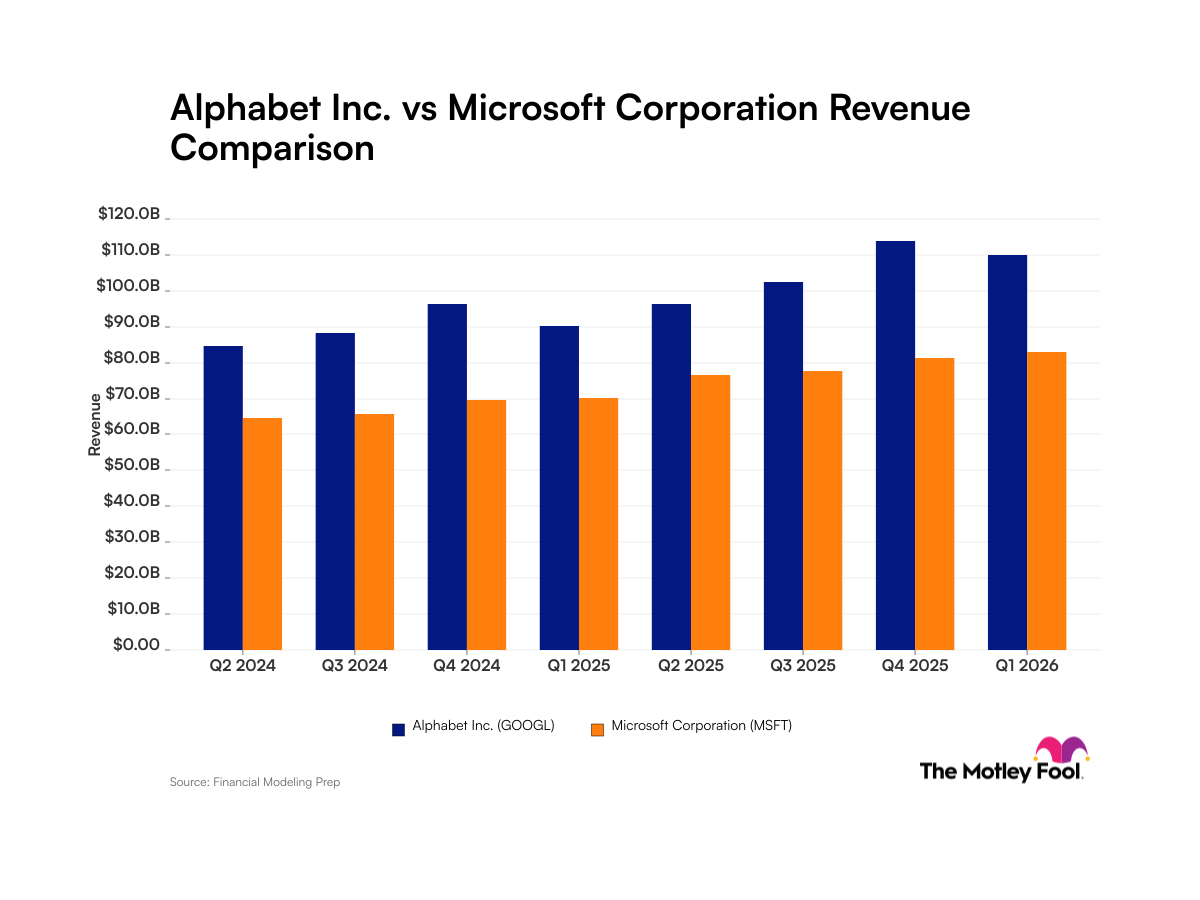

Alphabet and Microsoft Show Consistent Revenue Growth

- Alphabet Revenue Growth: In Q1 2026, Alphabet reported $109.9 billion in revenue, with Google search contributing $60.4 billion, showcasing its dominance in the digital advertising market and reinforcing its competitive edge in the tech industry.

- Microsoft Cloud Progress: Microsoft achieved $82.9 billion in revenue in Q1 2026, with cloud computing operations being crucial for future growth; despite being second in the global cloud sector, it must enhance AI investments to maintain competitiveness.

- AI Investment: Both companies are heavily investing in AI, with Microsoft partnering with OpenAI while Alphabet integrates AI into Google services, indicating that AI will be a significant driver for future business expansion.

- Market Share Comparison: Alphabet's Google search engine holds a 90% market share compared to Microsoft's Bing at 5%, reflecting not only the disparity in advertising revenue but also influencing investor expectations regarding future growth potential.

See More

Microsoft Shares Rebound Over 10% Amid Tech Rotation

- Price Recovery: Microsoft (MSFT) shares have rebounded over 10% in the past month, currently trading around $412.66, although they remain down approximately 14.6% year-to-date, indicating renewed investor interest in large-cap tech stocks.

- Technical Analysis: Technical traders have noted that after a sharp rally in late April, Microsoft's recent consolidation appears to form a potential bullish flag, suggesting a pause within a broader upward trend.

- Support Levels: The stock continues to trade above its rising 50-day moving average, a key level monitored by institutional investors for assessing intermediate-term momentum, while also holding above a previously established downtrend line, indicating easing selling pressure.

- Market Sentiment: The recent upward movement is supported by ongoing enthusiasm surrounding artificial intelligence infrastructure spending and enterprise software demand, which continues to bolster sentiment across the technology sector.

See More

Wall Street's Growing Divide on Tech Stocks

- Diverging Market Sentiment: Wall Street is sharply divided on tech stocks, with bears arguing that the market is overheating akin to 1999, while bulls see it as a buying opportunity, highlighting a profound disagreement on future market direction.

- Semiconductor Sector Overbought: The Philadelphia Semiconductor Index's overbought condition mirrors only two previous instances in 2000 and 1995, indicating significant adjustment risks ahead, particularly against the backdrop of soaring tech valuations.

- S&P 500 Performance Analysis: Despite the S&P 500 reaching new highs recently, over 60% of its stocks remain below their 50-day and 200-day moving averages, a phenomenon historically associated with market tops, suggesting potential bubble risks in the current environment.

- Investor Caution Signals: Notable investor Michael Burry warns of clear bubble signs in the current market, advising caution towards stocks that have surged dramatically, reflecting concerns about future market trajectories.

See More

Microsoft's East Africa Data Center Delayed

- Project Delay Reason: Microsoft's data center construction in Kenya has been delayed due to disagreements with the government over payment guarantees, highlighting the policy challenges the company faces in expanding its cloud computing services.

- Investment Scale: Microsoft, in partnership with UAE-based AI firm G42, plans to invest $1 billion in Kenya to enhance cloud capabilities in East Africa, but the government failed to provide the necessary payment guarantees.

- Negotiation Breakdown: The parties requested the Kenyan government to commit to annual payments for a certain capacity, but talks broke down when the government could not meet Microsoft's demands, potentially impacting Microsoft's market expansion in the region.

- Strategic Implications: This incident underscores the policy risks Microsoft faces in its East African market expansion, which may delay its cloud service growth plans and affect its competitive position in a rapidly growing market.

See More

AI Drives Semiconductor Industry Growth

- Surging Market Demand: McKinsey predicts that by 2030, AI inference will account for over 50% of computing power in data centers, reflecting the urgent demand from enterprises and consumers for AI integration, thereby driving sustained growth in the semiconductor industry.

- Arm's Market Potential: Arm Holdings anticipates over $2 billion in customer demand for its AGI CPU in fiscal years 2027 and 2028, indicating strong competitiveness in the AI inference market and the potential to generate $15 billion in annual revenue over the next five years.

- Technological Innovation and Partnerships: Arm's collaboration with Meta Platforms on the AGI CPU promises to save up to $10 billion in data center capital expenditures while delivering double the computing performance of AMD and Intel's x86 processors, further solidifying its market position.

- Optimistic Financial Outlook: Arm's revenue increased by 23% to $4.92 billion in fiscal 2026, with expectations of reaching $25 billion by fiscal 2031, indicating robust growth potential, and projected earnings per share rising to $9.00, suggesting a 51% upside in stock price.

See More

GameStop's $56B eBay Bid Rejected as Unviable

- Acquisition Proposal Rejected: eBay has officially rejected GameStop's unsolicited $56 billion acquisition bid, labeling it as 'neither credible nor attractive,' with concerns over a significant funding gap and high debt load, which could undermine GameStop's market confidence.

- Financing Challenges Emerge: Despite CEO Ryan Cohen's commitment to provide $20 billion in financing, analysts warn that GameStop's $10 billion market cap makes acquiring a $48 billion giant nearly impossible without extreme equity dilution, highlighting the fragility of its financing capabilities.

- Market Reaction Tepid: Following eBay's rejection, GameStop's stock fell 2.37% in pre-market trading, indicating investor concerns about its acquisition ability, which may impact its future stock performance and market positioning.

- Unclear Strategic Direction: eBay's board reiterated its focus on luxury goods and trading cards, believing this will yield superior shareholder returns, while GameStop's acquisition intentions could distract from its core resources and strategic focus.

See More

Alphabet and Microsoft Show Consistent Revenue Growth

- Alphabet Revenue Growth: In Q1 2026, Alphabet reported $109.9 billion in revenue, with Google search contributing $60.4 billion, showcasing its dominance in the digital advertising market and reinforcing its competitive edge in the tech industry.

- Microsoft Cloud Progress: Microsoft achieved $82.9 billion in revenue in Q1 2026, with cloud computing operations being crucial for future growth; despite being second in the global cloud sector, it must enhance AI investments to maintain competitiveness.

- AI Investment: Both companies are heavily investing in AI, with Microsoft partnering with OpenAI while Alphabet integrates AI into Google services, indicating that AI will be a significant driver for future business expansion.

- Market Share Comparison: Alphabet's Google search engine holds a 90% market share compared to Microsoft's Bing at 5%, reflecting not only the disparity in advertising revenue but also influencing investor expectations regarding future growth potential.

See More

Microsoft Shares Rebound Over 10% Amid Tech Rotation

- Price Recovery: Microsoft (MSFT) shares have rebounded over 10% in the past month, currently trading around $412.66, although they remain down approximately 14.6% year-to-date, indicating renewed investor interest in large-cap tech stocks.

- Technical Analysis: Technical traders have noted that after a sharp rally in late April, Microsoft's recent consolidation appears to form a potential bullish flag, suggesting a pause within a broader upward trend.

- Support Levels: The stock continues to trade above its rising 50-day moving average, a key level monitored by institutional investors for assessing intermediate-term momentum, while also holding above a previously established downtrend line, indicating easing selling pressure.

- Market Sentiment: The recent upward movement is supported by ongoing enthusiasm surrounding artificial intelligence infrastructure spending and enterprise software demand, which continues to bolster sentiment across the technology sector.

See More

Wall Street's Growing Divide on Tech Stocks

- Diverging Market Sentiment: Wall Street is sharply divided on tech stocks, with bears arguing that the market is overheating akin to 1999, while bulls see it as a buying opportunity, highlighting a profound disagreement on future market direction.

- Semiconductor Sector Overbought: The Philadelphia Semiconductor Index's overbought condition mirrors only two previous instances in 2000 and 1995, indicating significant adjustment risks ahead, particularly against the backdrop of soaring tech valuations.

- S&P 500 Performance Analysis: Despite the S&P 500 reaching new highs recently, over 60% of its stocks remain below their 50-day and 200-day moving averages, a phenomenon historically associated with market tops, suggesting potential bubble risks in the current environment.

- Investor Caution Signals: Notable investor Michael Burry warns of clear bubble signs in the current market, advising caution towards stocks that have surged dramatically, reflecting concerns about future market trajectories.

See More