Lam Research Corp. (LRCX) Receives Bullish Upgrades with Price Targets Up to $260

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Jan 15 2026

0mins

Should l Buy LRCX?

Source: Benzinga

- Analyst Upgrades: RBC Capital initiated coverage on Lam Research with an Outperform rating and a $260 price target, while Wells Fargo upgraded its rating to Overweight, raising its target from $145 to $250, indicating a significant increase in market confidence regarding the stock's outlook.

- Optimistic Earnings Forecast: Investors are looking forward to the earnings conference call on January 28, 2026, with EPS expected to reach $1.17, a 29% increase year-over-year, and revenue projected at $5.23 billion, a 19% increase, further solidifying positive sentiment around Lam Research.

- Strong Stock Performance: Lam Research shares are currently priced at $221.28, trading 17.2% above the 20-day simple moving average and having increased 186.99% over the past 12 months, demonstrating robust short-term and long-term strength as it approaches its 52-week high.

- Significant ETF Exposure: Lam Research holds substantial weight in several semiconductor ETFs, such as First Trust Nasdaq Semiconductor ETF (5.46%) and Invesco Semiconductors ETF (5.24%), indicating that any significant inflows or outflows in these funds will likely impact the stock's trading dynamics.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy LRCX?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on LRCX

Wall Street analysts forecast LRCX stock price to fall

22 Analyst Rating

18 Buy

4 Hold

0 Sell

Strong Buy

Current: 219.400

Low

142.00

Averages

192.50

High

265.00

Current: 219.400

Low

142.00

Averages

192.50

High

265.00

About LRCX

Lam Research Corporation is a global supplier of wafer fabrication equipment and services to the semiconductor industry. The Company designs, manufactures, markets, refurbishes, and services semiconductor processing equipment used in the fabrication of integrated circuits. Its products and services are designed to help its customers build devices that are used in a variety of electronic products, including mobile phones, personal computers, servers, wearables, automotive vehicles, and data storage devices. Its product families include ALTUS, SABRE, SPEED, Striker, VECTOR, Flex, Vantex, Kiyo, Versys Metal, Syndion, Coronus, and DV-Prime, Da Vinci, EOS, and SP Series. Its customer base includes semiconductor memory, foundries, and integrated device manufacturers that make products such as non-volatile memory, dynamic random-access memory, and logic devices. It offers services in areas, such as nanoscale applications enablement, chemistry, plasma and fluidics, and others.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

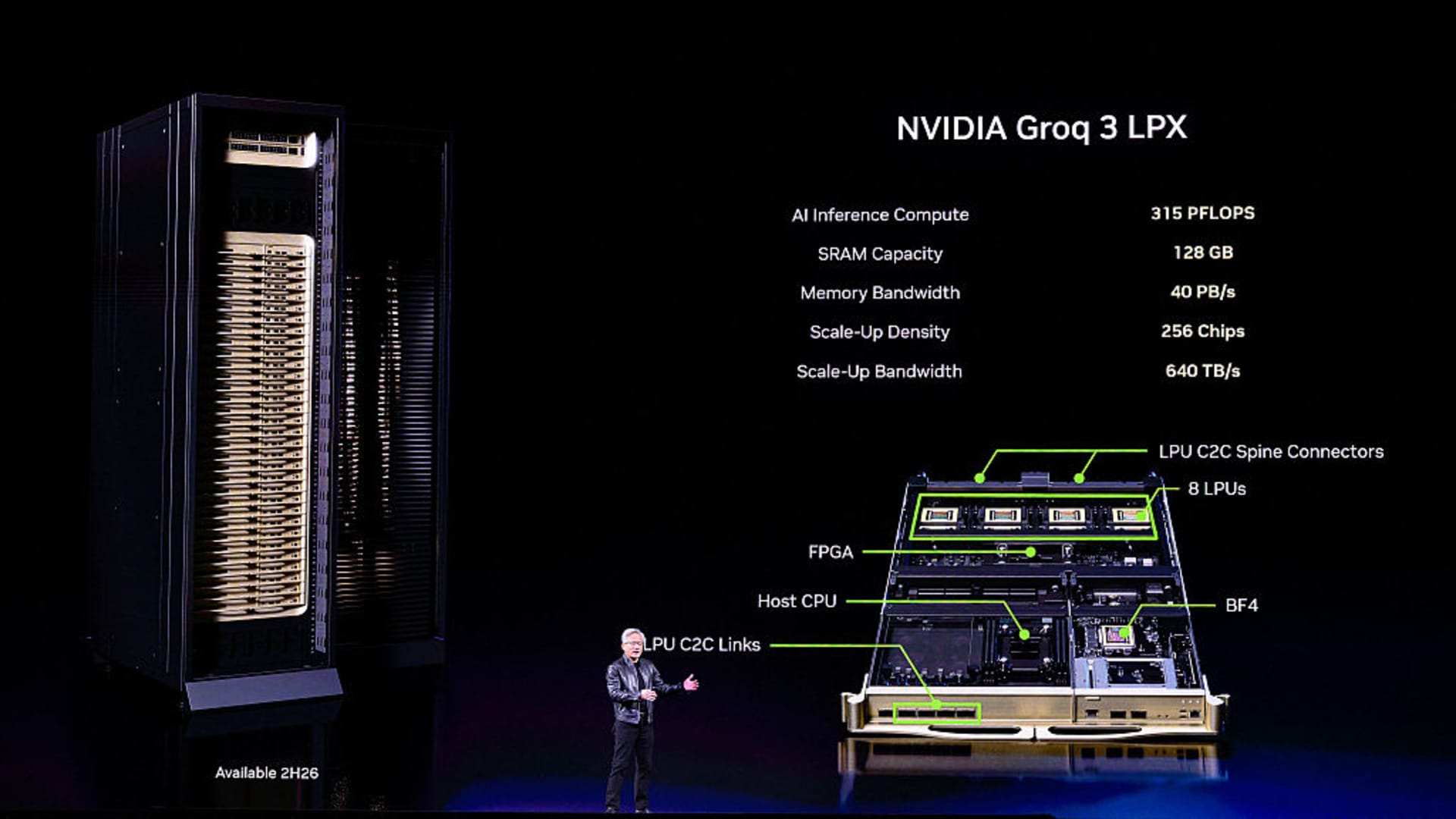

Nvidia Unveils New Inference Chip and Revenue Outlook

- New Inference Chip Launch: Nvidia unveiled its LPX inference chip, built on a $20 billion technology licensing deal with AI startup Groq, aimed at enhancing performance for low-latency inference tasks, and is set to launch alongside the Vera Rubin chip series, solidifying its market position in inference computing.

- Production and Market Strategy: The LPX chip is currently in volume production at third-party manufacturer Samsung and will be offered in server racks containing 256 LPX processors, with Nvidia planning to enhance overall data center performance by integrating LPX with Vera Rubin servers to meet diverse workload demands.

- Revenue Outlook Update: Nvidia expects orders for its Blackwell and Vera Rubin chips to reach $1 trillion by 2027, a significant increase from the $500 billion previously mentioned, reflecting strong confidence in future demand and potentially leading to upward revisions in market expectations for its 2027 data center revenue.

- Market Reaction and Analysis: Following Jensen Huang's announcement of the $1 trillion order outlook, Nvidia's stock briefly rose to $188.88 before closing at $183.22, with analysts suggesting that this news will bolster investor confidence in the sustainability of future AI spending, particularly in an active capital market environment.

See More

US Stocks Rise as Oil Prices Drop, Boosting Market Sentiment

- Oil Price Drop Fuels Market Rally: The S&P 500 rose 1.01%, the Dow Jones increased by 0.83%, and the Nasdaq 100 climbed 1.13% as crude oil prices fell over 5% due to hopes of tanker passage through the Strait of Hormuz, reflecting positive market sentiment towards lower energy costs.

- Mixed Economic Data: February manufacturing production in the US rose 0.2% month-over-month, surpassing expectations of 0.1%, and January's figure was revised up to 0.8%, indicating a recovery in manufacturing; however, the Empire State manufacturing index fell 7.3 points to -0.2, highlighting economic uncertainty.

- China's Economic Indicators Impact Global Outlook: China's February industrial production grew 6.3% year-on-year, exceeding expectations of 5.3%, while retail sales rose 2.8%, above the 2.5% forecast; however, the unemployment rate increased to 5.3%, indicating labor market pressures that could challenge global economic recovery.

- Airline and Cruise Stocks Surge: With falling oil prices, airline and cruise line stocks rallied, with Norwegian Cruise Line up over 5% and United Airlines up over 4%, suggesting optimistic market expectations for improved profitability due to lower fuel costs.

See More

US Stocks Surge as Crude Prices Drop Sharply

- Crude Price Drop Fuels Market Rally: The successful passage of several oil tankers through the Strait of Hormuz has led to a more than 4% drop in crude prices, directly contributing to a 1.04% rise in the S&P 500, a 0.94% increase in the Dow Jones, and a 1.12% gain in the Nasdaq 100, indicating a positive market response to lower oil prices.

- Mixed Economic Data: February manufacturing production in the US rose by 0.2% month-over-month, surpassing expectations of 0.1%, while January's production was revised up to 0.8%, showcasing manufacturing resilience; however, the February Empire manufacturing survey fell to -0.2, below the expected 3.9, reflecting economic recovery uncertainties.

- Positive Chinese Economic Indicators: China's February industrial production increased by 6.3% year-over-year, exceeding expectations of 5.3%, and retail sales rose by 2.8%, also above the anticipated 2.5%, despite a rise in the unemployment rate to 5.3%, highlighting the complexities of economic recovery.

- Airline and Cruise Stocks Surge: With falling oil prices, airline and cruise line stocks are rising, with Norwegian Cruise Line up over 5% and Royal Caribbean up more than 4%, indicating optimistic market sentiment regarding future earnings prospects.

See More

US Stocks Rise as Oil Prices Decline

- Oil Price Decline Boosts Markets: The successful passage of oil tankers through the Strait of Hormuz has led to a more than 3% drop in crude prices, directly contributing to a 1.23% rise in the S&P 500, a 1.06% increase in the Dow Jones, and a 1.30% gain in the Nasdaq 100, reflecting market optimism about supply recovery.

- Mixed Economic Data: February manufacturing production in the US rose by 0.2% month-over-month, surpassing expectations of 0.1%, and January was revised up to 0.8%, yet the February Empire manufacturing survey showed a decline of 7.3 points to -0.2, indicating challenges in economic recovery.

- Positive Chinese Economic Indicators: China's February industrial production increased by 6.3% year-on-year, exceeding expectations of 5.3%, and retail sales rose by 2.8%, also above the 2.5% forecast, although the unemployment rate climbed to 5.3%, indicating labor market pressures.

- Shifts in Rate Expectations: The market is pricing in only a 1% chance of a 25 basis point rate cut by the Federal Reserve at the upcoming policy meeting, while expectations for a rate hike by the European Central Bank are also decreasing, reflecting investor caution regarding future monetary policy.

See More

SOXL ETF 52-Week Price Analysis

- Price Range Analysis: SOXL ETF's 52-week low is $7.225 per share and high is $72.36, with the latest trade at $54.83, indicating significant volatility over the past year that reflects market interest and investor sentiment in the semiconductor sector.

- Technical Analysis Tool: Comparing the latest share price to the 200-day moving average provides investors with valuable insights for technical analysis, helping them assess market trends and potential buy or sell opportunities to optimize investment decisions.

- ETF Unit Trading Mechanism: ETFs trade similarly to stocks, where investors buy and sell 'units' that can be created or destroyed based on investor demand, offering flexibility that allows ETFs to better adapt to market changes.

- Inflows and Outflows Monitoring: Weekly monitoring of changes in shares outstanding for ETFs highlights those experiencing notable inflows or outflows, where inflows necessitate purchasing underlying assets, while outflows may lead to selling, thus impacting the performance of individual stocks within the ETF.

See More

Nvidia Shares Rise Ahead of Developer Conference

- Stock Price Increase: Nvidia's shares rose approximately 2% ahead of its developer conference, reflecting investor confidence in the sustainability of AI spending, with expectations that the event will unveil insights into next-generation processors and the technology roadmap.

- Market Share Concerns: Analysts highlight that Nvidia's market share in the semiconductor sector is under pressure from competitors like AMD with custom AI chips, and the GTC conference could help alleviate investor concerns regarding long-term market share.

- Long-Term Target Expectations: While market estimates for Nvidia's 2027 earnings hover around $13 per share, analysts believe that clearer long-term targets could help reignite the stock, especially as rivals have provided multi-year outlooks.

- Capital Return Potential: Nvidia reported over $60 billion in cash in its latest quarterly report, with projected free cash flows of $180 billion and $240 billion for 2026 and 2027, respectively, and an updated buyback strategy could further boost the stock price.

See More

Nvidia Unveils New Inference Chip and Revenue Outlook

- New Inference Chip Launch: Nvidia unveiled its LPX inference chip, built on a $20 billion technology licensing deal with AI startup Groq, aimed at enhancing performance for low-latency inference tasks, and is set to launch alongside the Vera Rubin chip series, solidifying its market position in inference computing.

- Production and Market Strategy: The LPX chip is currently in volume production at third-party manufacturer Samsung and will be offered in server racks containing 256 LPX processors, with Nvidia planning to enhance overall data center performance by integrating LPX with Vera Rubin servers to meet diverse workload demands.

- Revenue Outlook Update: Nvidia expects orders for its Blackwell and Vera Rubin chips to reach $1 trillion by 2027, a significant increase from the $500 billion previously mentioned, reflecting strong confidence in future demand and potentially leading to upward revisions in market expectations for its 2027 data center revenue.

- Market Reaction and Analysis: Following Jensen Huang's announcement of the $1 trillion order outlook, Nvidia's stock briefly rose to $188.88 before closing at $183.22, with analysts suggesting that this news will bolster investor confidence in the sustainability of future AI spending, particularly in an active capital market environment.

See More

US Stocks Rise as Oil Prices Drop, Boosting Market Sentiment

- Oil Price Drop Fuels Market Rally: The S&P 500 rose 1.01%, the Dow Jones increased by 0.83%, and the Nasdaq 100 climbed 1.13% as crude oil prices fell over 5% due to hopes of tanker passage through the Strait of Hormuz, reflecting positive market sentiment towards lower energy costs.

- Mixed Economic Data: February manufacturing production in the US rose 0.2% month-over-month, surpassing expectations of 0.1%, and January's figure was revised up to 0.8%, indicating a recovery in manufacturing; however, the Empire State manufacturing index fell 7.3 points to -0.2, highlighting economic uncertainty.

- China's Economic Indicators Impact Global Outlook: China's February industrial production grew 6.3% year-on-year, exceeding expectations of 5.3%, while retail sales rose 2.8%, above the 2.5% forecast; however, the unemployment rate increased to 5.3%, indicating labor market pressures that could challenge global economic recovery.

- Airline and Cruise Stocks Surge: With falling oil prices, airline and cruise line stocks rallied, with Norwegian Cruise Line up over 5% and United Airlines up over 4%, suggesting optimistic market expectations for improved profitability due to lower fuel costs.

See More

US Stocks Surge as Crude Prices Drop Sharply

- Crude Price Drop Fuels Market Rally: The successful passage of several oil tankers through the Strait of Hormuz has led to a more than 4% drop in crude prices, directly contributing to a 1.04% rise in the S&P 500, a 0.94% increase in the Dow Jones, and a 1.12% gain in the Nasdaq 100, indicating a positive market response to lower oil prices.

- Mixed Economic Data: February manufacturing production in the US rose by 0.2% month-over-month, surpassing expectations of 0.1%, while January's production was revised up to 0.8%, showcasing manufacturing resilience; however, the February Empire manufacturing survey fell to -0.2, below the expected 3.9, reflecting economic recovery uncertainties.

- Positive Chinese Economic Indicators: China's February industrial production increased by 6.3% year-over-year, exceeding expectations of 5.3%, and retail sales rose by 2.8%, also above the anticipated 2.5%, despite a rise in the unemployment rate to 5.3%, highlighting the complexities of economic recovery.

- Airline and Cruise Stocks Surge: With falling oil prices, airline and cruise line stocks are rising, with Norwegian Cruise Line up over 5% and Royal Caribbean up more than 4%, indicating optimistic market sentiment regarding future earnings prospects.

See More

US Stocks Rise as Oil Prices Decline

- Oil Price Decline Boosts Markets: The successful passage of oil tankers through the Strait of Hormuz has led to a more than 3% drop in crude prices, directly contributing to a 1.23% rise in the S&P 500, a 1.06% increase in the Dow Jones, and a 1.30% gain in the Nasdaq 100, reflecting market optimism about supply recovery.

- Mixed Economic Data: February manufacturing production in the US rose by 0.2% month-over-month, surpassing expectations of 0.1%, and January was revised up to 0.8%, yet the February Empire manufacturing survey showed a decline of 7.3 points to -0.2, indicating challenges in economic recovery.

- Positive Chinese Economic Indicators: China's February industrial production increased by 6.3% year-on-year, exceeding expectations of 5.3%, and retail sales rose by 2.8%, also above the 2.5% forecast, although the unemployment rate climbed to 5.3%, indicating labor market pressures.

- Shifts in Rate Expectations: The market is pricing in only a 1% chance of a 25 basis point rate cut by the Federal Reserve at the upcoming policy meeting, while expectations for a rate hike by the European Central Bank are also decreasing, reflecting investor caution regarding future monetary policy.

See More

SOXL ETF 52-Week Price Analysis

- Price Range Analysis: SOXL ETF's 52-week low is $7.225 per share and high is $72.36, with the latest trade at $54.83, indicating significant volatility over the past year that reflects market interest and investor sentiment in the semiconductor sector.

- Technical Analysis Tool: Comparing the latest share price to the 200-day moving average provides investors with valuable insights for technical analysis, helping them assess market trends and potential buy or sell opportunities to optimize investment decisions.

- ETF Unit Trading Mechanism: ETFs trade similarly to stocks, where investors buy and sell 'units' that can be created or destroyed based on investor demand, offering flexibility that allows ETFs to better adapt to market changes.

- Inflows and Outflows Monitoring: Weekly monitoring of changes in shares outstanding for ETFs highlights those experiencing notable inflows or outflows, where inflows necessitate purchasing underlying assets, while outflows may lead to selling, thus impacting the performance of individual stocks within the ETF.

See More

Nvidia Shares Rise Ahead of Developer Conference

- Stock Price Increase: Nvidia's shares rose approximately 2% ahead of its developer conference, reflecting investor confidence in the sustainability of AI spending, with expectations that the event will unveil insights into next-generation processors and the technology roadmap.

- Market Share Concerns: Analysts highlight that Nvidia's market share in the semiconductor sector is under pressure from competitors like AMD with custom AI chips, and the GTC conference could help alleviate investor concerns regarding long-term market share.

- Long-Term Target Expectations: While market estimates for Nvidia's 2027 earnings hover around $13 per share, analysts believe that clearer long-term targets could help reignite the stock, especially as rivals have provided multi-year outlooks.

- Capital Return Potential: Nvidia reported over $60 billion in cash in its latest quarterly report, with projected free cash flows of $180 billion and $240 billion for 2026 and 2027, respectively, and an updated buyback strategy could further boost the stock price.

See More