Intel Stock Volatility and Future Outlook

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 7 hours ago

0mins

Should l Buy INTC?

Source: Fool

- Stock Performance: Intel's stock has more than doubled in value over the past 12 months, yet it has declined approximately 18% from its 52-week high of $54.60 reached in January, indicating market uncertainty about its future.

- Profitability Challenges: While Intel's foundry business saw a 4% growth, overall revenue fell by 4%, and the foundry segment's operating loss increased to $2.5 billion, highlighting significant challenges in profitability.

- Overvaluation: Currently, Intel's price-to-earnings ratio stands at 85, significantly higher than the S&P 500's average of 22, suggesting that the market has priced in excessive optimism regarding its future growth, posing high risks for investors.

- Market Sentiment and Risks: Despite a strong performance at the beginning of 2026, the optimism surrounding Intel may already be fully reflected in its stock price, prompting investors to carefully consider whether to hold or buy the stock.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy INTC?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on INTC

Wall Street analysts forecast INTC stock price to fall

29 Analyst Rating

5 Buy

19 Hold

5 Sell

Hold

Current: 43.420

Low

20.00

Averages

39.30

High

52.00

Current: 43.420

Low

20.00

Averages

39.30

High

52.00

About INTC

Intel Corporation is a global designer and manufacturer of semiconductor products. The Company operates through three segments: Intel Products, Intel Foundry, and All Other. Its Intel Products segment includes Client Computing Group (CCG), Data Center and AI (DCAI), Network and Edge (NEX). The CCG is bringing together the operating system, system architecture, hardware, and software application integration to enable PC experiences. DCAI delivers workload-optimized solutions to cloud service providers and enterprises, along with silicon devices for communications service providers, network and edge, and HPC customers. NEX helps networks and edge compute systems from fixed-function hardware to general-purpose compute, acceleration, and networking devices running cloud native software on programmable hardware. The Intel Foundry segment comprises technology development, manufacturing and foundry services. All Other segments include Altera, Mobileye, Other.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

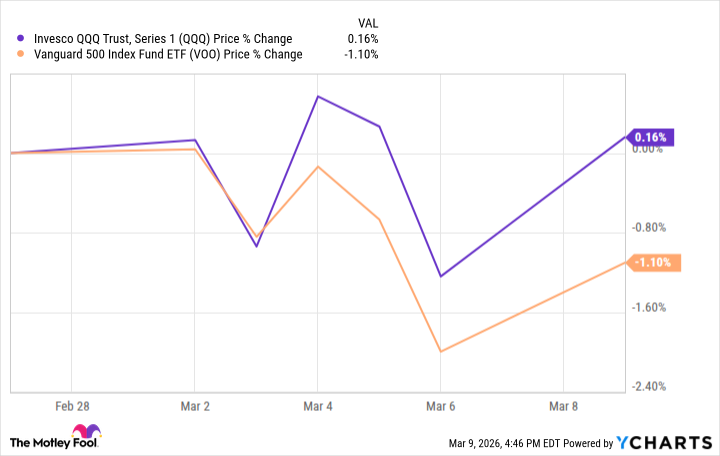

Nasdaq-100 Index Faces Challenges Amid AI Concerns

- Market Stagnation: After three consecutive years of significant gains, the Nasdaq-100 index has stagnated in 2026, primarily due to concerns about the negative impact of artificial intelligence on the global economy and valuation levels, which have shifted it from a market leader to a laggard.

- ETF Performance Comparison: From February 27, the last trading day before the Israel-Iran war began, to March 9, the Invesco QQQ ETF, which tracks the Nasdaq-100, outperformed the Vanguard S&P 500 ETF, indicating short-term resilience in tech stocks, though overall market trends remain to be seen.

- Earnings Growth Expectations: The tech sector is projected to deliver the highest earnings and revenue growth among the S&P 500 sectors in 2026, with a slowdown to a 20% growth rate expected in 2027; however, long-term earnings growth remains a key driver of stock performance.

- Valuation Reasonableness: While U.S. stock valuations are above historical averages, the forward P/E ratio for the S&P 500 information technology sector stands at 24.2, down from 31 a year ago, suggesting that if companies meet current expectations, the Nasdaq-100's valuation may not be excessively high.

See More

Netflix Reports Strong Earnings but Faces High Valuation Risks

- Strong Financial Performance: Netflix's fourth-quarter revenue increased by 17.6% year-over-year to $12.1 billion, demonstrating robust growth momentum in the global market, although the market has already priced in future growth.

- Improving Profitability: The company expects its operating margin to reach 29.5% in 2025, up from 26.7% in 2024, with a further increase to 31.5% in 2026, which will support future earnings growth.

- Surge in Ad Revenue: Netflix's advertising revenue is projected to rise over 150% in 2025 to exceed $1.5 billion, providing a new revenue stream that reduces reliance on subscription price increases and enhances financial stability.

- Valuation Risks Emerge: While the company anticipates an 18% annual growth in earnings per share over the next five years, increasing competition and slowing revenue growth could compress Netflix's price-to-earnings ratio from 38.5 to 20, leading to a price target of $116 and an annualized return of less than 4%.

See More

Analysis of GitLab's 24.8% Stock Plunge

- Significant Stock Drop: GitLab's stock plummeted by 24.8% in February, contrasting with the S&P 500's 0.9% decline, indicating a broader market retreat from software stocks amid concerns over the industry's outlook.

- Earnings Beat but Dim Guidance: Although GitLab reported a Q4 adjusted profit of $0.30 per share and sales of $260.4 million, both exceeding analyst expectations, the company's forward guidance failed to support stock gains, projecting lower sales than anticipated.

- Market Environment Impact: GitLab's stock continued to decline in March due to geopolitical and macroeconomic pressures, particularly the volatility from the U.S.-Israel conflict with Iran and unexpected job losses in February, which heightened market uncertainty.

- Investor Confidence Erosion: With GitLab's guidance falling short of market expectations, investor concerns about the company's near-term growth prospects intensified, leading multiple investment firms to lower their one-year price targets for the stock.

See More

Nvidia Stock Rises as AI Hardware Anticipation Grows

- Stock Price Surge: Nvidia (NVDA) shares rose 2.71% to close at $182.64, reflecting strong investor anticipation for AI hardware announcements at the upcoming GTC 2026 conference, which could drive long-term AI demand.

- Volume Insights: The trading volume reached 6.8 million shares, slightly below the three-month average of 177 million shares, indicating sustained market interest in Nvidia's future products despite a minor dip in short-term trading activity.

- New Product Expectations: The anticipated Rubin platform, expected in the second half of 2026, marks the next phase in Nvidia's AI accelerator architecture, potentially solidifying its lead in high-performance computing and attracting attention from developers and cloud service providers.

- Strategic Investment: Nvidia's multiyear optics partnership with Lumentum includes a multibillion-dollar purchase commitment and a $2 billion investment aimed at securing high-bandwidth interconnects for next-generation AI data centers, demonstrating the company's long-term strategic positioning in AI infrastructure spending.

See More

Intel Stock Volatility and Future Outlook

- Stock Performance: Intel's stock has more than doubled in value over the past 12 months, yet it has declined approximately 18% from its 52-week high of $54.60 reached in January, indicating market uncertainty about its future.

- Profitability Challenges: While Intel's foundry business saw a 4% growth, overall revenue fell by 4%, and the foundry segment's operating loss increased to $2.5 billion, highlighting significant challenges in profitability.

- Overvaluation: Currently, Intel's price-to-earnings ratio stands at 85, significantly higher than the S&P 500's average of 22, suggesting that the market has priced in excessive optimism regarding its future growth, posing high risks for investors.

- Market Sentiment and Risks: Despite a strong performance at the beginning of 2026, the optimism surrounding Intel may already be fully reflected in its stock price, prompting investors to carefully consider whether to hold or buy the stock.

See More

Nvidia Stock Rises as Investors Anticipate GTC Conference Announcements

- Stock Performance: Nvidia's stock closed at $182.65 on Monday, up 2.68%, reflecting investor anticipation for the upcoming GTC 2026 conference, which could significantly influence long-term AI demand.

- Trading Volume Analysis: The company's trading volume reached 174.1 million shares, approximately 1.4% below the three-month average of 176.6 million shares, indicating fluctuating market interest in new product announcements.

- Technological Innovation: Nvidia's Rubin platform, expected to launch in the second half of 2026, represents the next phase in its AI accelerator architecture, potentially solidifying its leadership in high-performance computing.

- Strategic Partnership: The multiyear optics partnership with Lumentum includes a multibillion-dollar purchase commitment and a $2 billion investment, aimed at securing high-bandwidth interconnects for next-generation AI data centers, thereby enhancing future market competitiveness.

See More

Nasdaq-100 Index Faces Challenges Amid AI Concerns

- Market Stagnation: After three consecutive years of significant gains, the Nasdaq-100 index has stagnated in 2026, primarily due to concerns about the negative impact of artificial intelligence on the global economy and valuation levels, which have shifted it from a market leader to a laggard.

- ETF Performance Comparison: From February 27, the last trading day before the Israel-Iran war began, to March 9, the Invesco QQQ ETF, which tracks the Nasdaq-100, outperformed the Vanguard S&P 500 ETF, indicating short-term resilience in tech stocks, though overall market trends remain to be seen.

- Earnings Growth Expectations: The tech sector is projected to deliver the highest earnings and revenue growth among the S&P 500 sectors in 2026, with a slowdown to a 20% growth rate expected in 2027; however, long-term earnings growth remains a key driver of stock performance.

- Valuation Reasonableness: While U.S. stock valuations are above historical averages, the forward P/E ratio for the S&P 500 information technology sector stands at 24.2, down from 31 a year ago, suggesting that if companies meet current expectations, the Nasdaq-100's valuation may not be excessively high.

See More

Netflix Reports Strong Earnings but Faces High Valuation Risks

- Strong Financial Performance: Netflix's fourth-quarter revenue increased by 17.6% year-over-year to $12.1 billion, demonstrating robust growth momentum in the global market, although the market has already priced in future growth.

- Improving Profitability: The company expects its operating margin to reach 29.5% in 2025, up from 26.7% in 2024, with a further increase to 31.5% in 2026, which will support future earnings growth.

- Surge in Ad Revenue: Netflix's advertising revenue is projected to rise over 150% in 2025 to exceed $1.5 billion, providing a new revenue stream that reduces reliance on subscription price increases and enhances financial stability.

- Valuation Risks Emerge: While the company anticipates an 18% annual growth in earnings per share over the next five years, increasing competition and slowing revenue growth could compress Netflix's price-to-earnings ratio from 38.5 to 20, leading to a price target of $116 and an annualized return of less than 4%.

See More

Analysis of GitLab's 24.8% Stock Plunge

- Significant Stock Drop: GitLab's stock plummeted by 24.8% in February, contrasting with the S&P 500's 0.9% decline, indicating a broader market retreat from software stocks amid concerns over the industry's outlook.

- Earnings Beat but Dim Guidance: Although GitLab reported a Q4 adjusted profit of $0.30 per share and sales of $260.4 million, both exceeding analyst expectations, the company's forward guidance failed to support stock gains, projecting lower sales than anticipated.

- Market Environment Impact: GitLab's stock continued to decline in March due to geopolitical and macroeconomic pressures, particularly the volatility from the U.S.-Israel conflict with Iran and unexpected job losses in February, which heightened market uncertainty.

- Investor Confidence Erosion: With GitLab's guidance falling short of market expectations, investor concerns about the company's near-term growth prospects intensified, leading multiple investment firms to lower their one-year price targets for the stock.

See More

Nvidia Stock Rises as AI Hardware Anticipation Grows

- Stock Price Surge: Nvidia (NVDA) shares rose 2.71% to close at $182.64, reflecting strong investor anticipation for AI hardware announcements at the upcoming GTC 2026 conference, which could drive long-term AI demand.

- Volume Insights: The trading volume reached 6.8 million shares, slightly below the three-month average of 177 million shares, indicating sustained market interest in Nvidia's future products despite a minor dip in short-term trading activity.

- New Product Expectations: The anticipated Rubin platform, expected in the second half of 2026, marks the next phase in Nvidia's AI accelerator architecture, potentially solidifying its lead in high-performance computing and attracting attention from developers and cloud service providers.

- Strategic Investment: Nvidia's multiyear optics partnership with Lumentum includes a multibillion-dollar purchase commitment and a $2 billion investment aimed at securing high-bandwidth interconnects for next-generation AI data centers, demonstrating the company's long-term strategic positioning in AI infrastructure spending.

See More

Intel Stock Volatility and Future Outlook

- Stock Performance: Intel's stock has more than doubled in value over the past 12 months, yet it has declined approximately 18% from its 52-week high of $54.60 reached in January, indicating market uncertainty about its future.

- Profitability Challenges: While Intel's foundry business saw a 4% growth, overall revenue fell by 4%, and the foundry segment's operating loss increased to $2.5 billion, highlighting significant challenges in profitability.

- Overvaluation: Currently, Intel's price-to-earnings ratio stands at 85, significantly higher than the S&P 500's average of 22, suggesting that the market has priced in excessive optimism regarding its future growth, posing high risks for investors.

- Market Sentiment and Risks: Despite a strong performance at the beginning of 2026, the optimism surrounding Intel may already be fully reflected in its stock price, prompting investors to carefully consider whether to hold or buy the stock.

See More

Nvidia Stock Rises as Investors Anticipate GTC Conference Announcements

- Stock Performance: Nvidia's stock closed at $182.65 on Monday, up 2.68%, reflecting investor anticipation for the upcoming GTC 2026 conference, which could significantly influence long-term AI demand.

- Trading Volume Analysis: The company's trading volume reached 174.1 million shares, approximately 1.4% below the three-month average of 176.6 million shares, indicating fluctuating market interest in new product announcements.

- Technological Innovation: Nvidia's Rubin platform, expected to launch in the second half of 2026, represents the next phase in its AI accelerator architecture, potentially solidifying its leadership in high-performance computing.

- Strategic Partnership: The multiyear optics partnership with Lumentum includes a multibillion-dollar purchase commitment and a $2 billion investment, aimed at securing high-bandwidth interconnects for next-generation AI data centers, thereby enhancing future market competitiveness.

See More