Chewy Scheduled to Announce Q4 Earnings on March 25

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 1 hour ago

0mins

Should l Buy CHWY?

Source: seekingalpha

- Earnings Announcement: Chewy (CHWY) is set to release its Q4 earnings on March 25 before the market opens, with consensus EPS estimate at $0.28 and revenue expected to reach $3.26 billion, reflecting a 0.3% year-over-year growth.

- Historical Performance: Over the past two years, Chewy has exceeded EPS estimates 63% of the time and has beaten revenue estimates 100% of the time, indicating a strong track record of financial performance and reliability.

- Estimate Adjustments: In the last three months, EPS estimates have seen two upward revisions and two downward revisions, while revenue estimates have experienced two upward revisions with no downward adjustments, suggesting fluctuating market confidence in Chewy's future performance.

- Market Analyst Insights: Although Chewy's fundamentals are improving, analysts caution that it may not be the right time to buy, advising investors to monitor the sustainability of its growth drivers before making investment decisions.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy CHWY?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on CHWY

Wall Street analysts forecast CHWY stock price to rise

20 Analyst Rating

17 Buy

3 Hold

0 Sell

Strong Buy

Current: 23.590

Low

42.00

Averages

47.06

High

52.00

Current: 23.590

Low

42.00

Averages

47.06

High

52.00

About CHWY

Chewy, Inc. is an e-commerce business geared toward pet products and services. The Company’s products consist of pet food and treats, pet supplies and pet medications, other pet-health products, and pet services. It serves its customers through its retail websites, and its mobile applications and focuses on delivering customer service, competitive prices, convenience, including Chewy’s Autoship subscription program, and a range of pet food, treats and supplies, and pet healthcare products and services. It partners with approximately 3,200 of the brands in the pet industry, and it creates and offers its own private brands. It owns a number of trademark registrations and applications in the United States and in foreign jurisdictions. These trademarks include American Journey, Blue Box Event, Careplus, Chewy, Chewy.com, Chewy Vet Care, Dr. Lyon’s, Frisco, Goody Box, Onguard, PetMD, PracticeHub, Tiny Tiger, True Acre Farms, Tylee’s, Vibeful, and The Zoo.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Chewy Reports Earnings Growth and Customer Loyalty Expansion

- Customer Loyalty Highlighted: Over 80% of Chewy's sales come from recurring customers, indicating the success of its Autoship service, which significantly enhances visibility on future sales and boosts investor confidence in long-term growth.

- Revenue Diversification Strategy: By expanding into veterinary clinics in the U.S., Chewy not only diversifies its revenue streams but also attracts new customers who have yet to try its e-commerce platform, further driving overall business growth.

- Profitability Milestone Achieved: Chewy has reached profitability in recent years, and despite its stock price dropping nearly 30% this year, the company's consistent revenue growth and successful market expansion lay a solid foundation for potential stock price recovery, demonstrating its long-term investment value.

- Attractive Valuation for Investors: Chewy's stock is currently trading at 15 times forward earnings estimates, a significant drop from over 30 times a year ago, making this reasonable valuation potentially a once-in-a-lifetime buying opportunity, especially given the company's strong fundamentals.

See More

Chewy's Stock Down 30% Yet Outlook Remains Positive

- Profitability Milestone: Chewy has achieved profitability despite a nearly 30% drop in stock price this year, indicating sustained growth in its e-commerce business in both the U.S. and Canada, showcasing its market expansion potential and profitability.

- Revenue Diversification: By adding veterinary clinics in the U.S., Chewy not only diversifies its revenue streams but also attracts new customers who have yet to try its e-commerce platform, thereby enhancing its competitive edge in the market.

- Customer Loyalty: With over 80% of sales coming from recurring customers, Chewy's Autoship service effectively boosts customer retention, ensuring visibility and stability in sales for the upcoming quarters.

- Reasonable Valuation: Although Chewy's stock performance has not reflected its fundamentals, the current 15x forward earnings ratio is reasonable compared to over 30x a year ago, suggesting that this may be an excellent buying opportunity.

See More

Chewy Scheduled to Announce Q4 Earnings on March 25

- Earnings Announcement: Chewy (CHWY) is set to release its Q4 earnings on March 25 before the market opens, with consensus EPS estimate at $0.28 and revenue expected to reach $3.26 billion, reflecting a 0.3% year-over-year growth.

- Historical Performance: Over the past two years, Chewy has exceeded EPS estimates 63% of the time and has beaten revenue estimates 100% of the time, indicating a strong track record of financial performance and reliability.

- Estimate Adjustments: In the last three months, EPS estimates have seen two upward revisions and two downward revisions, while revenue estimates have experienced two upward revisions with no downward adjustments, suggesting fluctuating market confidence in Chewy's future performance.

- Market Analyst Insights: Although Chewy's fundamentals are improving, analysts caution that it may not be the right time to buy, advising investors to monitor the sustainability of its growth drivers before making investment decisions.

See More

Chewy Set to Report Earnings; Investors Eye Key Metrics

- Customer Growth Trends: Chewy experienced a 43% year-over-year increase in active customers during fiscal 2020, but growth has slowed post-pandemic, with rates of 8%, 1%, and 2% from 2021 to 2023, indicating intensified market competition and changing consumer behaviors.

- Sales Performance: While Chewy's total net sales surged by 47% in fiscal 2020, the growth rate has declined annually, dropping to just 6% in fiscal 2024, reflecting the impact of inflation and macroeconomic pressures on non-essential pet product sales.

- Subscription Stability: In Q3 2025, Chewy's Autoship customers accounted for 83.9% of total net sales, up from 79.2% in fiscal 2024, indicating positive progress in customer retention and repeat purchase rates.

- Future Outlook: Analysts project Chewy's revenue to grow by 6% and 7% in 2025 and 2026, respectively, with adjusted EBITDA increasing by 25% and 24%, showcasing the company's potential in expanding its service ecosystem, even as its high-growth phase may be over.

See More

Chewy Shows Signs of Stock Stabilization

- Customer Growth Trends: Chewy experienced a 43% increase in active customers during fiscal 2020, but post-pandemic growth has declined, with a -2% rate in fiscal 2023, reflecting intensified market competition and changing consumer behaviors.

- Sales Stability: Despite inflation and competition from Amazon, Chewy has stabilized its business by locking in more Autoship subscription customers, with 83.9% of net sales in Q3 2025 coming from Autoship customers, indicating a shift towards a more resilient business model.

- Optimistic Financial Outlook: Analysts project Chewy's revenue and adjusted EBITDA to grow by 6% and 25% respectively in 2025, highlighting the company's potential in expanding its service ecosystem, even as overall growth rates slow down.

- Attractive Valuation: With an enterprise value of $8.9 billion, Chewy's valuation stands at just 9 times next year's adjusted EBITDA, suggesting that its stock is undervalued in the market, potentially offering a good buying opportunity for investors.

See More

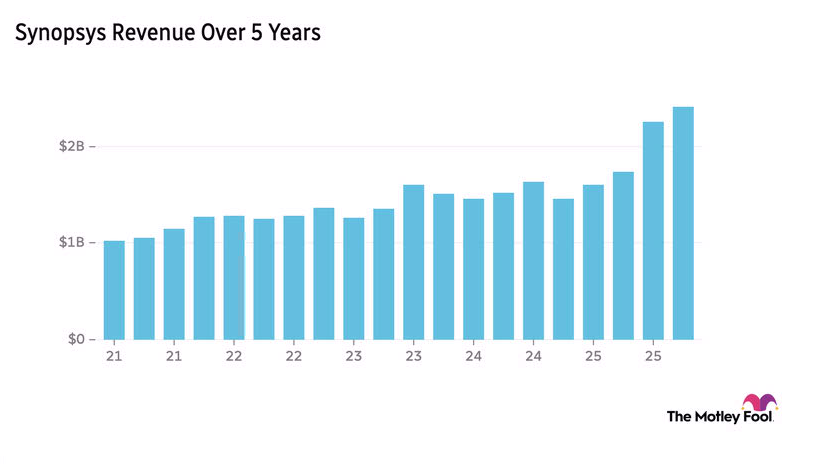

Elliott Builds Major Stake in Synopsys to Enhance Profitability

- Investor Stake Increase: Elliott Investment Management has built a multibillion-dollar stake in chip design software company Synopsys, aiming to enhance its software and services profitability, which is expected to positively impact the company's future financial performance.

- Positive Market Reaction: Following the news of Elliott's stake increase, Synopsys's stock rose by 2.5% in early trading, indicating optimistic market sentiment regarding its growth potential and likely attracting more investor interest.

- Strong Industry Demand: Nvidia CEO Jensen Huang stated at the Synopsys Converge 2026 conference that the number of Synopsys tool users is set to soar, reflecting the ongoing demand for efficient tools in the chip design industry and further solidifying Synopsys's market position.

- AI's Profound Impact: Analysts noted that while AI will change workflows, the demand for subscriptions to Synopsys and Cadence will remain robust, with expectations that user engagement will significantly rise as AI features expand, thereby driving revenue growth for the company.

See More

Chewy Reports Earnings Growth and Customer Loyalty Expansion

- Customer Loyalty Highlighted: Over 80% of Chewy's sales come from recurring customers, indicating the success of its Autoship service, which significantly enhances visibility on future sales and boosts investor confidence in long-term growth.

- Revenue Diversification Strategy: By expanding into veterinary clinics in the U.S., Chewy not only diversifies its revenue streams but also attracts new customers who have yet to try its e-commerce platform, further driving overall business growth.

- Profitability Milestone Achieved: Chewy has reached profitability in recent years, and despite its stock price dropping nearly 30% this year, the company's consistent revenue growth and successful market expansion lay a solid foundation for potential stock price recovery, demonstrating its long-term investment value.

- Attractive Valuation for Investors: Chewy's stock is currently trading at 15 times forward earnings estimates, a significant drop from over 30 times a year ago, making this reasonable valuation potentially a once-in-a-lifetime buying opportunity, especially given the company's strong fundamentals.

See More

Chewy's Stock Down 30% Yet Outlook Remains Positive

- Profitability Milestone: Chewy has achieved profitability despite a nearly 30% drop in stock price this year, indicating sustained growth in its e-commerce business in both the U.S. and Canada, showcasing its market expansion potential and profitability.

- Revenue Diversification: By adding veterinary clinics in the U.S., Chewy not only diversifies its revenue streams but also attracts new customers who have yet to try its e-commerce platform, thereby enhancing its competitive edge in the market.

- Customer Loyalty: With over 80% of sales coming from recurring customers, Chewy's Autoship service effectively boosts customer retention, ensuring visibility and stability in sales for the upcoming quarters.

- Reasonable Valuation: Although Chewy's stock performance has not reflected its fundamentals, the current 15x forward earnings ratio is reasonable compared to over 30x a year ago, suggesting that this may be an excellent buying opportunity.

See More

Chewy Scheduled to Announce Q4 Earnings on March 25

- Earnings Announcement: Chewy (CHWY) is set to release its Q4 earnings on March 25 before the market opens, with consensus EPS estimate at $0.28 and revenue expected to reach $3.26 billion, reflecting a 0.3% year-over-year growth.

- Historical Performance: Over the past two years, Chewy has exceeded EPS estimates 63% of the time and has beaten revenue estimates 100% of the time, indicating a strong track record of financial performance and reliability.

- Estimate Adjustments: In the last three months, EPS estimates have seen two upward revisions and two downward revisions, while revenue estimates have experienced two upward revisions with no downward adjustments, suggesting fluctuating market confidence in Chewy's future performance.

- Market Analyst Insights: Although Chewy's fundamentals are improving, analysts caution that it may not be the right time to buy, advising investors to monitor the sustainability of its growth drivers before making investment decisions.

See More

Chewy Set to Report Earnings; Investors Eye Key Metrics

- Customer Growth Trends: Chewy experienced a 43% year-over-year increase in active customers during fiscal 2020, but growth has slowed post-pandemic, with rates of 8%, 1%, and 2% from 2021 to 2023, indicating intensified market competition and changing consumer behaviors.

- Sales Performance: While Chewy's total net sales surged by 47% in fiscal 2020, the growth rate has declined annually, dropping to just 6% in fiscal 2024, reflecting the impact of inflation and macroeconomic pressures on non-essential pet product sales.

- Subscription Stability: In Q3 2025, Chewy's Autoship customers accounted for 83.9% of total net sales, up from 79.2% in fiscal 2024, indicating positive progress in customer retention and repeat purchase rates.

- Future Outlook: Analysts project Chewy's revenue to grow by 6% and 7% in 2025 and 2026, respectively, with adjusted EBITDA increasing by 25% and 24%, showcasing the company's potential in expanding its service ecosystem, even as its high-growth phase may be over.

See More

Chewy Shows Signs of Stock Stabilization

- Customer Growth Trends: Chewy experienced a 43% increase in active customers during fiscal 2020, but post-pandemic growth has declined, with a -2% rate in fiscal 2023, reflecting intensified market competition and changing consumer behaviors.

- Sales Stability: Despite inflation and competition from Amazon, Chewy has stabilized its business by locking in more Autoship subscription customers, with 83.9% of net sales in Q3 2025 coming from Autoship customers, indicating a shift towards a more resilient business model.

- Optimistic Financial Outlook: Analysts project Chewy's revenue and adjusted EBITDA to grow by 6% and 25% respectively in 2025, highlighting the company's potential in expanding its service ecosystem, even as overall growth rates slow down.

- Attractive Valuation: With an enterprise value of $8.9 billion, Chewy's valuation stands at just 9 times next year's adjusted EBITDA, suggesting that its stock is undervalued in the market, potentially offering a good buying opportunity for investors.

See More

Elliott Builds Major Stake in Synopsys to Enhance Profitability

- Investor Stake Increase: Elliott Investment Management has built a multibillion-dollar stake in chip design software company Synopsys, aiming to enhance its software and services profitability, which is expected to positively impact the company's future financial performance.

- Positive Market Reaction: Following the news of Elliott's stake increase, Synopsys's stock rose by 2.5% in early trading, indicating optimistic market sentiment regarding its growth potential and likely attracting more investor interest.

- Strong Industry Demand: Nvidia CEO Jensen Huang stated at the Synopsys Converge 2026 conference that the number of Synopsys tool users is set to soar, reflecting the ongoing demand for efficient tools in the chip design industry and further solidifying Synopsys's market position.

- AI's Profound Impact: Analysts noted that while AI will change workflows, the demand for subscriptions to Synopsys and Cadence will remain robust, with expectations that user engagement will significantly rise as AI features expand, thereby driving revenue growth for the company.

See More