Chevron Q1 Earnings Beat Expectations Despite Revenue Miss

- Earnings Beat: Chevron reported a Q1 non-GAAP EPS of $1.41, exceeding expectations by $0.44, indicating strong profitability despite the revenue shortfall.

- Slight Revenue Growth: The company generated $48.61 billion in revenue for the quarter, reflecting a 2.1% year-over-year increase, yet falling short of the anticipated $49.09 billion, highlighting market challenges.

- Production Increase: Worldwide and U.S. production rose by 15% and 24%, respectively, demonstrating significant progress in output enhancement, which is expected to contribute positively to future revenue.

- Increased Shareholder Returns: Chevron returned $6.0 billion to shareholders during the quarter, including $2.5 billion in share repurchases and $3.5 billion in dividends, underscoring the company's commitment to shareholder value.

Trade with 70% Backtested Accuracy

Analyst Views on CVX

About CVX

About the author

CHEVRON: Q2 Downtime and Turnarounds, Including Effects of Cyclone Narelle in Australia and MEAST Conflict, Anticipated to Range from 100,000 to 150,000 BOEPD

Chevron's Q2 Performance: Chevron reported a turnaround in its Q2 performance, indicating a recovery in its operations and financial results.

Impact of Cyclone Narelle: The company faced challenges due to Cyclone Narelle, which affected its operations in Australia, particularly in the eastern conflict region.

Expected Workforce Reduction: Chevron anticipates a workforce reduction, estimating that between 100 to 150 employees may be impacted by the ongoing changes.

Broader Industry Implications: The developments at Chevron reflect broader trends in the energy sector, where companies are adjusting to environmental challenges and operational disruptions.

CHEVRON ANNOUNCES FIRST QUARTER 2026 FINANCIAL RESULTS

Financial Performance: Chevron reported its first-quarter 2026 results, showcasing significant financial metrics and performance indicators.

Revenue and Earnings: The company highlighted its revenue and earnings figures, reflecting the impact of market conditions and operational efficiency.

Operational Highlights: Chevron provided insights into its operational achievements and strategic initiatives during the quarter.

Future Outlook: The report included projections and expectations for future performance, considering ongoing market trends and company strategies.

Chevron Reports Strong EPS Beat Amid Revenue Miss

- Earnings Highlights: Chevron's non-GAAP EPS of $1.41 exceeded expectations by $0.44, showcasing strong profitability despite a revenue miss of $48.61 billion, which fell short of the $49.09 billion forecast, indicating challenges in the market environment.

- Market Environment Impact: The ongoing turmoil in the Middle East is expected to lead to double-digit profit declines for both Chevron and Exxon in Q1, highlighting the geopolitical risks that pressure profitability in the oil sector and may influence future investment decisions.

- Growth Drivers: Despite the revenue miss, Chevron's growth drivers remain aligned with its valuation and technicals, suggesting that the company still possesses solid growth potential under current market conditions, which may attract long-term investor interest.

- Technical Analysis: Analysts indicate that Chevron's current stock price does not fully capture its earnings power and market potential, suggesting possible upside in the future, prompting investors to monitor technical indicators for optimal entry points.

Chevron Q1 Performance Analysis Amid Global Energy Crisis

- Production Growth: Chevron's total oil equivalent production reached 3.858 million barrels per day in Q1, a 15% increase year-over-year, demonstrating the company's resilience amid the global energy crisis, particularly with a 24% rise in U.S. production.

- Financial Performance: Although Q1 revenue was $48.61 billion, missing the $52.7 billion estimate, the adjusted earnings per share stood at $1.41, surpassing the $0.97 forecast, indicating strong profitability.

- Middle East Risk Management: CEO Mike Wirth highlighted that Chevron's exposure to the Middle East is less than 5%, allowing the company to remain largely unaffected by the ongoing U.S.-Iran conflict, thus ensuring stability in its global supply chain.

- Market Sentiment Shift: Retail sentiment towards CVX shifted from 'bearish' to 'bullish' in the last 24 hours, reflecting investor confidence in the company's future performance, with CVX stock rising 27% year-to-date.

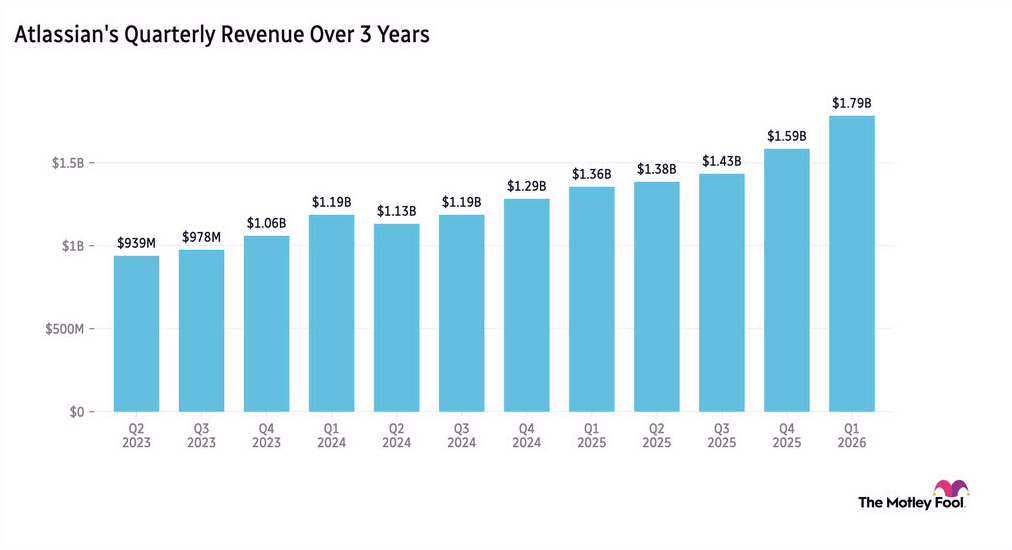

Atlassian Shares Surge 25% on AI-Driven Revenue Growth

- Revenue Surge: Atlassian's third-quarter revenue rose 32% year-over-year, leading to a 25% jump in pre-market trading, and despite restructuring costs impacting profitability, non-GAAP earnings per share soared by 80%, reflecting strong demand for AI services.

- Cloud Transition: CFO James Chuong cautioned that the shift of customers to cloud services would result in a more muted level of data center expansion, with expectations for moderated revenue growth in Q4, which could impact future market performance.

- Product Advantage: Analyst Meilin Quinn noted that while workflows may be taken over by agents, there remains a need for trusted company knowledge and systems, providing Atlassian with a stronger foothold in engineering processes and enhancing its competitive edge.

- Market Reaction: Major stock indexes hit new highs amid continued growth in AI spending, with the S&P 500 closing above 7,200 points for the first time, reflecting strong market confidence in tech stocks and further boosting Atlassian's stock performance.

Exxon Mobil Beats Q1 Earnings Estimates Despite Lowest Profit in Five Years

- Adjusted Earnings Beat: Exxon Mobil reported adjusted earnings of $1.16 per share for Q1, surpassing the consensus estimate of $1.00, despite unadjusted profits dropping to a five-year low due to war-related disruptions, showcasing the company's resilience in adversity.

- Significant Net Income Decline: The net income for the first quarter was $4.2 billion, down from $7.7 billion in the same period of 2025, reflecting the negative impact of Middle Eastern tensions on production and shipping, although the company experienced growth in other regions.

- Cash Flow and Shareholder Returns: Free cash flow for Q1 was $2.7 billion, a significant drop from $8.8 billion year-over-year, while the company paid $4.3 billion in dividends and repurchased $4.9 billion in shares during the quarter, demonstrating a continued commitment to shareholder returns.

- Significant Middle East Impact: Approximately 20% of Exxon's oil and gas production is sourced from the Middle East, with production down 6% due to war disruptions, and the company's liquefied natural gas assets in the region were also attacked, making the timeline for repairs a key focus for analysts moving forward.

CHEVRON: Q2 Downtime and Turnarounds, Including Effects of Cyclone Narelle in Australia and MEAST Conflict, Anticipated to Range from 100,000 to 150,000 BOEPD

Chevron's Q2 Performance: Chevron reported a turnaround in its Q2 performance, indicating a recovery in its operations and financial results.

Impact of Cyclone Narelle: The company faced challenges due to Cyclone Narelle, which affected its operations in Australia, particularly in the eastern conflict region.

Expected Workforce Reduction: Chevron anticipates a workforce reduction, estimating that between 100 to 150 employees may be impacted by the ongoing changes.

Broader Industry Implications: The developments at Chevron reflect broader trends in the energy sector, where companies are adjusting to environmental challenges and operational disruptions.

CHEVRON ANNOUNCES FIRST QUARTER 2026 FINANCIAL RESULTS

Financial Performance: Chevron reported its first-quarter 2026 results, showcasing significant financial metrics and performance indicators.

Revenue and Earnings: The company highlighted its revenue and earnings figures, reflecting the impact of market conditions and operational efficiency.

Operational Highlights: Chevron provided insights into its operational achievements and strategic initiatives during the quarter.

Future Outlook: The report included projections and expectations for future performance, considering ongoing market trends and company strategies.

Chevron Reports Strong EPS Beat Amid Revenue Miss

- Earnings Highlights: Chevron's non-GAAP EPS of $1.41 exceeded expectations by $0.44, showcasing strong profitability despite a revenue miss of $48.61 billion, which fell short of the $49.09 billion forecast, indicating challenges in the market environment.

- Market Environment Impact: The ongoing turmoil in the Middle East is expected to lead to double-digit profit declines for both Chevron and Exxon in Q1, highlighting the geopolitical risks that pressure profitability in the oil sector and may influence future investment decisions.

- Growth Drivers: Despite the revenue miss, Chevron's growth drivers remain aligned with its valuation and technicals, suggesting that the company still possesses solid growth potential under current market conditions, which may attract long-term investor interest.

- Technical Analysis: Analysts indicate that Chevron's current stock price does not fully capture its earnings power and market potential, suggesting possible upside in the future, prompting investors to monitor technical indicators for optimal entry points.

Chevron Q1 Performance Analysis Amid Global Energy Crisis

- Production Growth: Chevron's total oil equivalent production reached 3.858 million barrels per day in Q1, a 15% increase year-over-year, demonstrating the company's resilience amid the global energy crisis, particularly with a 24% rise in U.S. production.

- Financial Performance: Although Q1 revenue was $48.61 billion, missing the $52.7 billion estimate, the adjusted earnings per share stood at $1.41, surpassing the $0.97 forecast, indicating strong profitability.

- Middle East Risk Management: CEO Mike Wirth highlighted that Chevron's exposure to the Middle East is less than 5%, allowing the company to remain largely unaffected by the ongoing U.S.-Iran conflict, thus ensuring stability in its global supply chain.

- Market Sentiment Shift: Retail sentiment towards CVX shifted from 'bearish' to 'bullish' in the last 24 hours, reflecting investor confidence in the company's future performance, with CVX stock rising 27% year-to-date.

Atlassian Shares Surge 25% on AI-Driven Revenue Growth

- Revenue Surge: Atlassian's third-quarter revenue rose 32% year-over-year, leading to a 25% jump in pre-market trading, and despite restructuring costs impacting profitability, non-GAAP earnings per share soared by 80%, reflecting strong demand for AI services.

- Cloud Transition: CFO James Chuong cautioned that the shift of customers to cloud services would result in a more muted level of data center expansion, with expectations for moderated revenue growth in Q4, which could impact future market performance.

- Product Advantage: Analyst Meilin Quinn noted that while workflows may be taken over by agents, there remains a need for trusted company knowledge and systems, providing Atlassian with a stronger foothold in engineering processes and enhancing its competitive edge.

- Market Reaction: Major stock indexes hit new highs amid continued growth in AI spending, with the S&P 500 closing above 7,200 points for the first time, reflecting strong market confidence in tech stocks and further boosting Atlassian's stock performance.

Exxon Mobil Beats Q1 Earnings Estimates Despite Lowest Profit in Five Years

- Adjusted Earnings Beat: Exxon Mobil reported adjusted earnings of $1.16 per share for Q1, surpassing the consensus estimate of $1.00, despite unadjusted profits dropping to a five-year low due to war-related disruptions, showcasing the company's resilience in adversity.

- Significant Net Income Decline: The net income for the first quarter was $4.2 billion, down from $7.7 billion in the same period of 2025, reflecting the negative impact of Middle Eastern tensions on production and shipping, although the company experienced growth in other regions.

- Cash Flow and Shareholder Returns: Free cash flow for Q1 was $2.7 billion, a significant drop from $8.8 billion year-over-year, while the company paid $4.3 billion in dividends and repurchased $4.9 billion in shares during the quarter, demonstrating a continued commitment to shareholder returns.

- Significant Middle East Impact: Approximately 20% of Exxon's oil and gas production is sourced from the Middle East, with production down 6% due to war disruptions, and the company's liquefied natural gas assets in the region were also attacked, making the timeline for repairs a key focus for analysts moving forward.