Big Wall Street Investors Bought Into Bitcoin ETFs in Q2

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Aug 15 2024

0mins

Source: investopedia.com

Institutional Investment in Bitcoin ETFs: Major financial institutions like Goldman Sachs and Morgan Stanley significantly increased their investments in spot bitcoin ETFs during the second quarter, with Goldman holding over $400 million across multiple funds and Morgan Stanley adding new positions worth approximately $189 million.

BlackRock's IBIT Dominance: BlackRock's iShares Bitcoin Trust ETF (IBIT) emerged as a leading choice among investors, receiving substantial inflows from firms such as Goldman Sachs and the State of Wisconsin Investment Board, while other firms like JPMorgan reduced their bitcoin ETF holdings.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy GS?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on GS

Wall Street analysts forecast GS stock price to fall

12 Analyst Rating

5 Buy

7 Hold

0 Sell

Moderate Buy

Current: 1055.290

Low

604.00

Averages

951.45

High

1100

Current: 1055.290

Low

604.00

Averages

951.45

High

1100

About GS

The Goldman Sachs Group, Inc. is a global financial institution that delivers a range of financial services to a large and diversified client base that includes corporations, financial institutions, governments and individuals. Its segments include Global Banking & Markets, Asset & Wealth Management and Platform Solutions. The Global Banking & Markets segment offers a range of services, including financing, advisory services, risk distribution, and hedging for its institutional and corporate clients. It facilitates client transactions and makes markets in fixed income, equity, currency and commodity products. The Asset & Wealth Management segment manages assets and offers investment products across all asset classes to a diverse set of clients. It also provides investing and wealth advisory solutions. The Platform Solutions segment includes consumer platforms, such as partnerships offering credit cards and point-of-sale financing, and transaction banking and other platform businesses.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Declining CD Rates: Opportunities for Competitive Returns

- Current Rate Overview: As of July 8, 2026, the best short-term CD rates range from 4% to 4.5% APY, with Marcus by Goldman Sachs offering a competitive 4.10% APY on its 14-month CD, indicating a strong market despite overall declining rates compared to traditional savings accounts.

- Historical Rate Review: Since the 2000s, CD rates have seen significant fluctuations, dropping to around 1% APY for one-year CDs in 2009 due to economic slowdowns and Federal Reserve rate cuts, which diminished investor confidence in long-term deposits.

- Impact of Economic Policies: Following the COVID-19 pandemic, the Fed raised rates 11 times, boosting CD rates; although rate cuts began in September 2024, current rates remain above historical averages, suggesting potential for economic recovery.

- Factors in Choosing CDs: When selecting a CD with a high APY, it is essential to consider the duration for which funds will be locked, the type of financial institution, and account terms to ensure the investment aligns with personal financial goals while avoiding penalties for early withdrawal.

See More

Nscale Secures $900 Million Credit Facility to Boost AI Infrastructure

- Significant Financing: Nscale has secured a $900 million revolving credit facility aimed at strengthening its balance sheet and accelerating the construction of AI data centers, highlighting robust demand for AI infrastructure.

- Global Expansion Plans: This financing will support Nscale's capital deployment across the U.S., Europe, and APAC, further solidifying its position in the global AI infrastructure market.

- Increased Institutional Confidence: Nscale CEO Josh Payne stated that this financing reflects investor confidence in the company's platform and team, while enhancing its flexibility to build infrastructure for major tech companies at greater speed.

- Accelerated Strategic Partnerships: The financing follows Nscale's collaboration with Microsoft on a data center in Portugal, indicating that the company is leveraging funds to support broader AI infrastructure expansion to meet ongoing market demand for advanced GPU capabilities.

See More

Goldman Sachs Maintains Hold Rating

- Rating Maintenance: Goldman Sachs (GS) currently holds an average rating of Hold, indicating a cautious market sentiment regarding its future performance, despite its competitive position in the financial services sector.

- Price Target Analysis: The average price target for Goldman Sachs is $1,035.70, which may reflect investor expectations regarding its future profitability, showcasing confidence in the stability of its stock price.

- Market Environment: The Hold rating in the current economic climate suggests that investors remain optimistic about Goldman Sachs' long-term growth potential, particularly amid fluctuations in interest rates and inflation.

- Investor Strategy: The rating and price target provide investors with a reference point to make informed investment decisions in a complex market environment, especially given the increasing volatility in the financial sector.

See More

Wall Street's Major Banks Bullish on SpaceX's Future

- Analysts' Optimistic Outlook: Deutsche Bank analysts describe SpaceX as 'the apex of civilizational ambition,' indicating strong confidence in the company's future role in shaping history and technological advancement.

- Market Capitalization: With a market cap of $2.1 trillion and a closing price of $160.42 per share on Monday, SpaceX's performance post-IPO reflects market approval, although MoffettNathanson remains pessimistic about its value over the next 12 months.

- Technological Innovation Potential: Analysts at Raymond James assert that the successful deployment of Starship will industrialize orbital transportation, potentially reducing launch costs to hundreds of dollars per kilogram, thereby advancing the broader space economy.

- Diversified Business Strategy: SpaceX's integration strategy across its three business segments—Space, Connectivity, and Artificial Intelligence—is expected to enhance its competitive edge in future markets, particularly as Starlink's user base has reached 12 million, becoming a significant revenue driver.

See More

Market Dynamics and Company News Overview

- Mixed Market Performance: Dow futures are up 130 points while Nasdaq is set for a sharp decline due to chip stock sell-offs, and S&P futures are modestly lower, indicating a complex market sentiment that could impact investor confidence.

- SpaceX Joins Nasdaq 100: SpaceX officially enters the Nasdaq 100 index, expected to attract billions in passive flows, with at least 18 buy ratings from analysts, reflecting strong market confidence in its future growth potential following its IPO.

- Samsung Stock Pullback: Samsung Electronics shares fell 7% in South Korea despite a staggering 1,800% increase in second-quarter operating profit and doubled sales, indicating potential profit-taking by investors concerned about the sustainability of its AI spending boom.

- Walmart's Price Reduction Strategy: Walmart has lowered prices on beef and other summer grilling essentials, which, combined with falling gas prices, helps alleviate inflationary pressures; despite an 18% drop in shares since mid-May, this move is seen as an investment opportunity that could attract more consumers.

See More

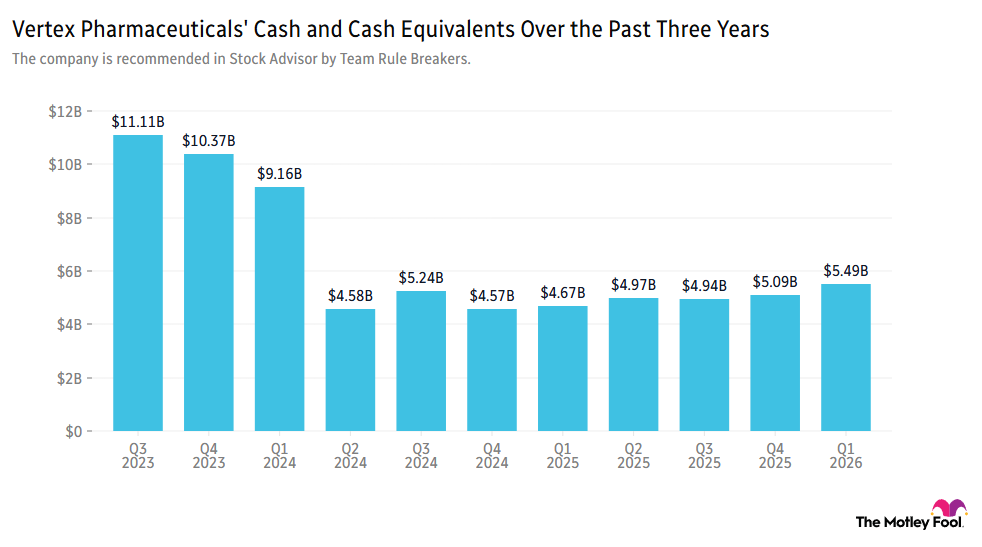

Vertex Acquires Crinetics for $10 Billion to Expand Rare Disease Portfolio

- Acquisition of Crinetics: Vertex Pharmaceuticals is acquiring Crinetics Pharmaceuticals for $10 billion, aiming to expand its business into endocrine diseases, with the potential to add up to $5 billion in annual revenue over the long term, although the market reacted negatively in the short term, pushing the stock down about 2%.

- Strategic Fit: Vertex CEO Reshma Kewalramani praised the acquisition as an excellent strategic fit, as Crinetics focuses on serious diseases in specialty markets with significant unmet needs, and it is expected to contribute revenue immediately through the ongoing launch of the Palsonify medicine.

- Revenue Growth Potential: The growing demand for therapeutics in endocrine diseases provides Vertex with a clear runway for double-digit revenue growth in the coming years, with Crinetics in the portfolio further solidifying its market position.

- Strong Market Performance: Since February 2022, Vertex's stock has outperformed the S&P 500 by 45%, demonstrating strong investor appeal, particularly in the current market environment.

See More

Declining CD Rates: Opportunities for Competitive Returns

- Current Rate Overview: As of July 8, 2026, the best short-term CD rates range from 4% to 4.5% APY, with Marcus by Goldman Sachs offering a competitive 4.10% APY on its 14-month CD, indicating a strong market despite overall declining rates compared to traditional savings accounts.

- Historical Rate Review: Since the 2000s, CD rates have seen significant fluctuations, dropping to around 1% APY for one-year CDs in 2009 due to economic slowdowns and Federal Reserve rate cuts, which diminished investor confidence in long-term deposits.

- Impact of Economic Policies: Following the COVID-19 pandemic, the Fed raised rates 11 times, boosting CD rates; although rate cuts began in September 2024, current rates remain above historical averages, suggesting potential for economic recovery.

- Factors in Choosing CDs: When selecting a CD with a high APY, it is essential to consider the duration for which funds will be locked, the type of financial institution, and account terms to ensure the investment aligns with personal financial goals while avoiding penalties for early withdrawal.

See More

Nscale Secures $900 Million Credit Facility to Boost AI Infrastructure

- Significant Financing: Nscale has secured a $900 million revolving credit facility aimed at strengthening its balance sheet and accelerating the construction of AI data centers, highlighting robust demand for AI infrastructure.

- Global Expansion Plans: This financing will support Nscale's capital deployment across the U.S., Europe, and APAC, further solidifying its position in the global AI infrastructure market.

- Increased Institutional Confidence: Nscale CEO Josh Payne stated that this financing reflects investor confidence in the company's platform and team, while enhancing its flexibility to build infrastructure for major tech companies at greater speed.

- Accelerated Strategic Partnerships: The financing follows Nscale's collaboration with Microsoft on a data center in Portugal, indicating that the company is leveraging funds to support broader AI infrastructure expansion to meet ongoing market demand for advanced GPU capabilities.

See More

Goldman Sachs Maintains Hold Rating

- Rating Maintenance: Goldman Sachs (GS) currently holds an average rating of Hold, indicating a cautious market sentiment regarding its future performance, despite its competitive position in the financial services sector.

- Price Target Analysis: The average price target for Goldman Sachs is $1,035.70, which may reflect investor expectations regarding its future profitability, showcasing confidence in the stability of its stock price.

- Market Environment: The Hold rating in the current economic climate suggests that investors remain optimistic about Goldman Sachs' long-term growth potential, particularly amid fluctuations in interest rates and inflation.

- Investor Strategy: The rating and price target provide investors with a reference point to make informed investment decisions in a complex market environment, especially given the increasing volatility in the financial sector.

See More

Wall Street's Major Banks Bullish on SpaceX's Future

- Analysts' Optimistic Outlook: Deutsche Bank analysts describe SpaceX as 'the apex of civilizational ambition,' indicating strong confidence in the company's future role in shaping history and technological advancement.

- Market Capitalization: With a market cap of $2.1 trillion and a closing price of $160.42 per share on Monday, SpaceX's performance post-IPO reflects market approval, although MoffettNathanson remains pessimistic about its value over the next 12 months.

- Technological Innovation Potential: Analysts at Raymond James assert that the successful deployment of Starship will industrialize orbital transportation, potentially reducing launch costs to hundreds of dollars per kilogram, thereby advancing the broader space economy.

- Diversified Business Strategy: SpaceX's integration strategy across its three business segments—Space, Connectivity, and Artificial Intelligence—is expected to enhance its competitive edge in future markets, particularly as Starlink's user base has reached 12 million, becoming a significant revenue driver.

See More

Market Dynamics and Company News Overview

- Mixed Market Performance: Dow futures are up 130 points while Nasdaq is set for a sharp decline due to chip stock sell-offs, and S&P futures are modestly lower, indicating a complex market sentiment that could impact investor confidence.

- SpaceX Joins Nasdaq 100: SpaceX officially enters the Nasdaq 100 index, expected to attract billions in passive flows, with at least 18 buy ratings from analysts, reflecting strong market confidence in its future growth potential following its IPO.

- Samsung Stock Pullback: Samsung Electronics shares fell 7% in South Korea despite a staggering 1,800% increase in second-quarter operating profit and doubled sales, indicating potential profit-taking by investors concerned about the sustainability of its AI spending boom.

- Walmart's Price Reduction Strategy: Walmart has lowered prices on beef and other summer grilling essentials, which, combined with falling gas prices, helps alleviate inflationary pressures; despite an 18% drop in shares since mid-May, this move is seen as an investment opportunity that could attract more consumers.

See More

Vertex Acquires Crinetics for $10 Billion to Expand Rare Disease Portfolio

- Acquisition of Crinetics: Vertex Pharmaceuticals is acquiring Crinetics Pharmaceuticals for $10 billion, aiming to expand its business into endocrine diseases, with the potential to add up to $5 billion in annual revenue over the long term, although the market reacted negatively in the short term, pushing the stock down about 2%.

- Strategic Fit: Vertex CEO Reshma Kewalramani praised the acquisition as an excellent strategic fit, as Crinetics focuses on serious diseases in specialty markets with significant unmet needs, and it is expected to contribute revenue immediately through the ongoing launch of the Palsonify medicine.

- Revenue Growth Potential: The growing demand for therapeutics in endocrine diseases provides Vertex with a clear runway for double-digit revenue growth in the coming years, with Crinetics in the portfolio further solidifying its market position.

- Strong Market Performance: Since February 2022, Vertex's stock has outperformed the S&P 500 by 45%, demonstrating strong investor appeal, particularly in the current market environment.

See More