AWS Enters New Era for Defense Contractors with CMMC Implementation

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 2 days ago

0mins

Should l Buy AMZN?

Source: seekingalpha

- CMMC Implementation: AWS is aiding defense contractors in implementing the Cybersecurity Maturity Model Certification 2.0 (CMMC), which is set for full implementation by fiscal year 2028, aiming to enhance cybersecurity standards for businesses working with the U.S. Department of Defense, thereby increasing their market competitiveness.

- Cloud Services Investment: AWS plans a $50 billion investment to expand its artificial intelligence and supercomputing capabilities, expected to add 1.3 GW of compute capacity for U.S. government customers, further solidifying its leadership in the defense cloud services market.

- Major Contract Awarded: In early 2026, AWS secured a $581.3 million contract from the U.S. Air Force to provide cloud services under the Cloud One program, which not only enhances its influence in the defense sector but also paves the way for future contract opportunities.

- AI Capability Collaboration: AWS entered agreements with the Department of Defense as one of eight tech companies to supply AI capabilities, showcasing its technological strength and market potential in the defense sector, which is expected to drive future revenue growth.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy AMZN?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on AMZN

Wall Street analysts forecast AMZN stock price to rise

44 Analyst Rating

41 Buy

3 Hold

0 Sell

Strong Buy

Current: 273.550

Low

175.00

Averages

280.01

High

325.00

Current: 273.550

Low

175.00

Averages

280.01

High

325.00

About AMZN

Amazon.com, Inc. provides a range of products and services to customers. The products offered through its stores include merchandise and content it has purchased for resale and products offered by third-party sellers. The Company’s segments include North America, International and Amazon Web Services (AWS). It serves consumers through its online and physical stores and focuses on selection, price, and convenience. Customers access its offerings through its websites, mobile apps, Alexa, devices, streaming, and physically visiting its stores. It also manufactures and sells electronic devices, including Kindle, Fire tablet, Fire TV, Echo, Ring, Blink, and eero, and develops and produces media content. It serves developers and enterprises of all sizes, including start-ups, government agencies, and academic institutions, through AWS, which offers a set of on-demand technology services, including compute, storage, database, analytics, and machine learning, and other services.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Amazon Accelerates Growth in Key Categories

- Key Category Growth: Amazon has achieved accelerated growth in several key categories, indicating a strong recovery in market demand that is expected to further boost the company's overall revenue.

- Stock Performance: As of May 1, 2026, Amazon's stock price rose by 1.36%, reflecting investor optimism about the company's future growth potential, which may attract more investor interest.

- Market Reaction: This growth trend could enhance Amazon's competitiveness in the e-commerce sector, especially in the face of challenges from other retail giants, further solidifying its market leadership.

- Future Outlook: With the continued growth in key categories, Amazon is poised to capture a larger market share in the coming quarters, thereby driving long-term financial health and shareholder value enhancement.

See More

AMAZON TO INVEST OVER EUR 15 BILLION IN FRANCE, GENERATING 7,000+ PERMANENT JOBS

- Investment Announcement: Amazon has announced plans to invest over €15 billion in France.

- Job Creation: This investment is expected to create more than 7,000 permanent jobs in the country.

See More

AWS Enters New Era for Defense Contractors with CMMC Implementation

- CMMC Implementation: AWS is aiding defense contractors in implementing the Cybersecurity Maturity Model Certification 2.0 (CMMC), which is set for full implementation by fiscal year 2028, aiming to enhance cybersecurity standards for businesses working with the U.S. Department of Defense, thereby increasing their market competitiveness.

- Cloud Services Investment: AWS plans a $50 billion investment to expand its artificial intelligence and supercomputing capabilities, expected to add 1.3 GW of compute capacity for U.S. government customers, further solidifying its leadership in the defense cloud services market.

- Major Contract Awarded: In early 2026, AWS secured a $581.3 million contract from the U.S. Air Force to provide cloud services under the Cloud One program, which not only enhances its influence in the defense sector but also paves the way for future contract opportunities.

- AI Capability Collaboration: AWS entered agreements with the Department of Defense as one of eight tech companies to supply AI capabilities, showcasing its technological strength and market potential in the defense sector, which is expected to drive future revenue growth.

See More

Meta's Investments and Challenges in AI Sector

- Advertising Revenue Surge: Meta's advertising revenue reached $55 billion in Q1, reflecting a 33% year-over-year increase and accounting for nearly 98% of total revenue, indicating the strength of its core advertising business and providing funding for future investments.

- AI Model Launch: The introduction of Meta's new AI model, Muse Spark, claims to outperform common models in several areas, showcasing the company's potential and commitment in the AI sector, although its market adoption remains to be seen.

- Capital Expenditure Plans: Meta expects capital expenditures to range between $125 billion and $145 billion in 2023, primarily for new data centers and AI infrastructure, which has raised skepticism among investors, yet remains conservative compared to other tech giants.

- Vertical Integration Goal: By developing custom AI chips in partnership with Broadcom, Meta aims to reduce reliance on Nvidia and AMD, thereby lowering computing costs and accelerating its vertical integration process, although this requires substantial investment, it will enhance control over its AI ecosystem in the long run.

See More

Meta's Advertising Revenue Sees Significant Growth

- Advertising Revenue Surge: Meta's advertising revenue reached $55 billion in Q1, marking a 33% year-over-year increase and accounting for nearly 98% of total revenue, indicating the strength of its core business that funds other ventures.

- Skepticism Over Capex Plans: Meta expects capital expenditures to range between $125 billion and $145 billion in 2023, primarily for new data centers and AI infrastructure, although this increased forecast still raises skepticism among investors due to past missteps.

- AI Strategic Development: The recent launch of Meta's AI model Muse Spark, which outperforms common models, signifies its growing competitiveness in AI, while partnerships with Broadcom for custom chips aim to reduce reliance on external GPUs and cut computing costs.

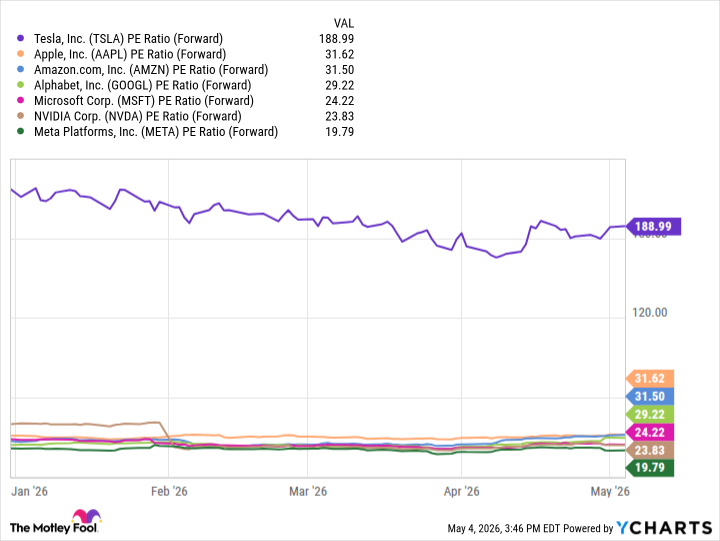

- Market Valuation Shift: Despite a nearly 6% decline in Meta's stock this year, its price-to-earnings ratio stands at 19.8, lower than other

See More

Meta Platforms Stock Slides into Value Territory

- Advertising Revenue Surge: Meta's advertising revenue reached $55 billion in Q1, marking a 33% year-over-year increase and accounting for nearly 98% of total revenue, indicating that its core advertising business remains robust and can fund future investments.

- AI Investment Plans: Meta expects capital expenditures to range between $125 billion and $145 billion in 2023, primarily for new data centers and AI infrastructure, which, despite raising investor skepticism, is crucial for maintaining a competitive edge in the AI race.

- AI Model Launch: The recent release of Meta's AI model, Muse Spark, which outperforms common models in several areas, suggests potential in the AI space, although its adoption remains to be seen, indicating a shift in market perception of Meta's capabilities.

- Vertical Integration Strategy: By developing custom application-specific integrated circuits in partnership with Broadcom, Meta aims to reduce reliance on Nvidia and AMD, thereby lowering computing costs and accelerating its vertical integration within the AI ecosystem.

See More

Amazon Accelerates Growth in Key Categories

- Key Category Growth: Amazon has achieved accelerated growth in several key categories, indicating a strong recovery in market demand that is expected to further boost the company's overall revenue.

- Stock Performance: As of May 1, 2026, Amazon's stock price rose by 1.36%, reflecting investor optimism about the company's future growth potential, which may attract more investor interest.

- Market Reaction: This growth trend could enhance Amazon's competitiveness in the e-commerce sector, especially in the face of challenges from other retail giants, further solidifying its market leadership.

- Future Outlook: With the continued growth in key categories, Amazon is poised to capture a larger market share in the coming quarters, thereby driving long-term financial health and shareholder value enhancement.

See More

AMAZON TO INVEST OVER EUR 15 BILLION IN FRANCE, GENERATING 7,000+ PERMANENT JOBS

- Investment Announcement: Amazon has announced plans to invest over €15 billion in France.

- Job Creation: This investment is expected to create more than 7,000 permanent jobs in the country.

See More

AWS Enters New Era for Defense Contractors with CMMC Implementation

- CMMC Implementation: AWS is aiding defense contractors in implementing the Cybersecurity Maturity Model Certification 2.0 (CMMC), which is set for full implementation by fiscal year 2028, aiming to enhance cybersecurity standards for businesses working with the U.S. Department of Defense, thereby increasing their market competitiveness.

- Cloud Services Investment: AWS plans a $50 billion investment to expand its artificial intelligence and supercomputing capabilities, expected to add 1.3 GW of compute capacity for U.S. government customers, further solidifying its leadership in the defense cloud services market.

- Major Contract Awarded: In early 2026, AWS secured a $581.3 million contract from the U.S. Air Force to provide cloud services under the Cloud One program, which not only enhances its influence in the defense sector but also paves the way for future contract opportunities.

- AI Capability Collaboration: AWS entered agreements with the Department of Defense as one of eight tech companies to supply AI capabilities, showcasing its technological strength and market potential in the defense sector, which is expected to drive future revenue growth.

See More

Meta's Investments and Challenges in AI Sector

- Advertising Revenue Surge: Meta's advertising revenue reached $55 billion in Q1, reflecting a 33% year-over-year increase and accounting for nearly 98% of total revenue, indicating the strength of its core advertising business and providing funding for future investments.

- AI Model Launch: The introduction of Meta's new AI model, Muse Spark, claims to outperform common models in several areas, showcasing the company's potential and commitment in the AI sector, although its market adoption remains to be seen.

- Capital Expenditure Plans: Meta expects capital expenditures to range between $125 billion and $145 billion in 2023, primarily for new data centers and AI infrastructure, which has raised skepticism among investors, yet remains conservative compared to other tech giants.

- Vertical Integration Goal: By developing custom AI chips in partnership with Broadcom, Meta aims to reduce reliance on Nvidia and AMD, thereby lowering computing costs and accelerating its vertical integration process, although this requires substantial investment, it will enhance control over its AI ecosystem in the long run.

See More

Meta's Advertising Revenue Sees Significant Growth

- Advertising Revenue Surge: Meta's advertising revenue reached $55 billion in Q1, marking a 33% year-over-year increase and accounting for nearly 98% of total revenue, indicating the strength of its core business that funds other ventures.

- Skepticism Over Capex Plans: Meta expects capital expenditures to range between $125 billion and $145 billion in 2023, primarily for new data centers and AI infrastructure, although this increased forecast still raises skepticism among investors due to past missteps.

- AI Strategic Development: The recent launch of Meta's AI model Muse Spark, which outperforms common models, signifies its growing competitiveness in AI, while partnerships with Broadcom for custom chips aim to reduce reliance on external GPUs and cut computing costs.

- Market Valuation Shift: Despite a nearly 6% decline in Meta's stock this year, its price-to-earnings ratio stands at 19.8, lower than other

See More

Meta Platforms Stock Slides into Value Territory

- Advertising Revenue Surge: Meta's advertising revenue reached $55 billion in Q1, marking a 33% year-over-year increase and accounting for nearly 98% of total revenue, indicating that its core advertising business remains robust and can fund future investments.

- AI Investment Plans: Meta expects capital expenditures to range between $125 billion and $145 billion in 2023, primarily for new data centers and AI infrastructure, which, despite raising investor skepticism, is crucial for maintaining a competitive edge in the AI race.

- AI Model Launch: The recent release of Meta's AI model, Muse Spark, which outperforms common models in several areas, suggests potential in the AI space, although its adoption remains to be seen, indicating a shift in market perception of Meta's capabilities.

- Vertical Integration Strategy: By developing custom application-specific integrated circuits in partnership with Broadcom, Meta aims to reduce reliance on Nvidia and AMD, thereby lowering computing costs and accelerating its vertical integration within the AI ecosystem.

See More