Walmart Board Under Investigation for Fiduciary Breaches

Walmart's stock has hit a 20-day low, reflecting investor concerns amid broader market declines, with the Nasdaq-100 down 0.48% and the S&P 500 down 0.59%.

The core catalyst for this decline is the investigation into Walmart's Board of Directors for potential breaches of fiduciary duties related to oversight failures concerning deceptive pay practices for Spark drivers. This investigation raises significant concerns about corporate governance and could negatively impact shareholder interests and market performance.

As one of the largest retail corporations globally, Walmart's governance issues may lead to diminished investor confidence, necessitating enhanced internal controls and transparency to restore trust and stabilize its market position.

Trade with 70% Backtested Accuracy

Analyst Views on WMT

About WMT

About the author

Walmart Lowers Prices Amid Competitive Pressure

- Pricing Strategy: Walmart has lowered prices on various grocery and seasonal items at both Walmart and Sam's Club, including a nearly 15% reduction in ground beef prices, addressing consumer concerns over high prices amid a 4.2% inflation rate in the U.S.

- Analyst Support: BofA analyst Christopher Nardone stated that the price cuts will be funded through existing financial guidance and tariff refunds, indicating the company's willingness to compete aggressively in the highly competitive grocery market while maintaining margins.

- Market Reaction: Despite Walmart's stock facing a fourth consecutive week of losses, both BofA and Mizuho have maintained their 'Outperform' ratings, with Mizuho setting a price target of $137, suggesting a 24% upside, reflecting confidence in the effectiveness of the pricing strategy.

- Cost Pressure Relief: Walmart expects to receive over $2 billion in tariff refunds, and the decline in diesel prices has eased cost pressures, with the full-year fuel impact now estimated to be between $700 million and $800 million, further supporting the sustainability of its price-cutting strategy.

India's IPO Market Faces Major Risks Amid Geopolitical Tensions

- IPO Plans Under Threat: Trump's decision to end the ceasefire with Iran poses significant risks to India's anticipated $50 billion IPO pipeline, causing a more than 2% market slump and highlighting the increasing impact of geopolitical risks on financial markets.

- Weak Market Performance: IPO activity in India for 2026 has been lackluster compared to the U.S. and Hong Kong, raising only $4 billion in the first half, in stark contrast to the $128 billion and $27 billion raised in those markets, indicating insufficient market absorption for new listings.

- Regulatory Approval Progress: Approximately $22 billion worth of IPOs are seeking regulatory approval, expected to take 2-3 months, while $29 billion worth have already been approved, including major firms like Zepto and Avaada Electro, suggesting potential opportunities still exist in the market.

- Economic Transformation Context: India's economy is transforming with the rise of new manufacturing industries driven by digital technology adoption and tax reforms, and despite unfavorable market conditions, companies are still seeking to list to unlock growth potential, reflecting confidence in future prospects.

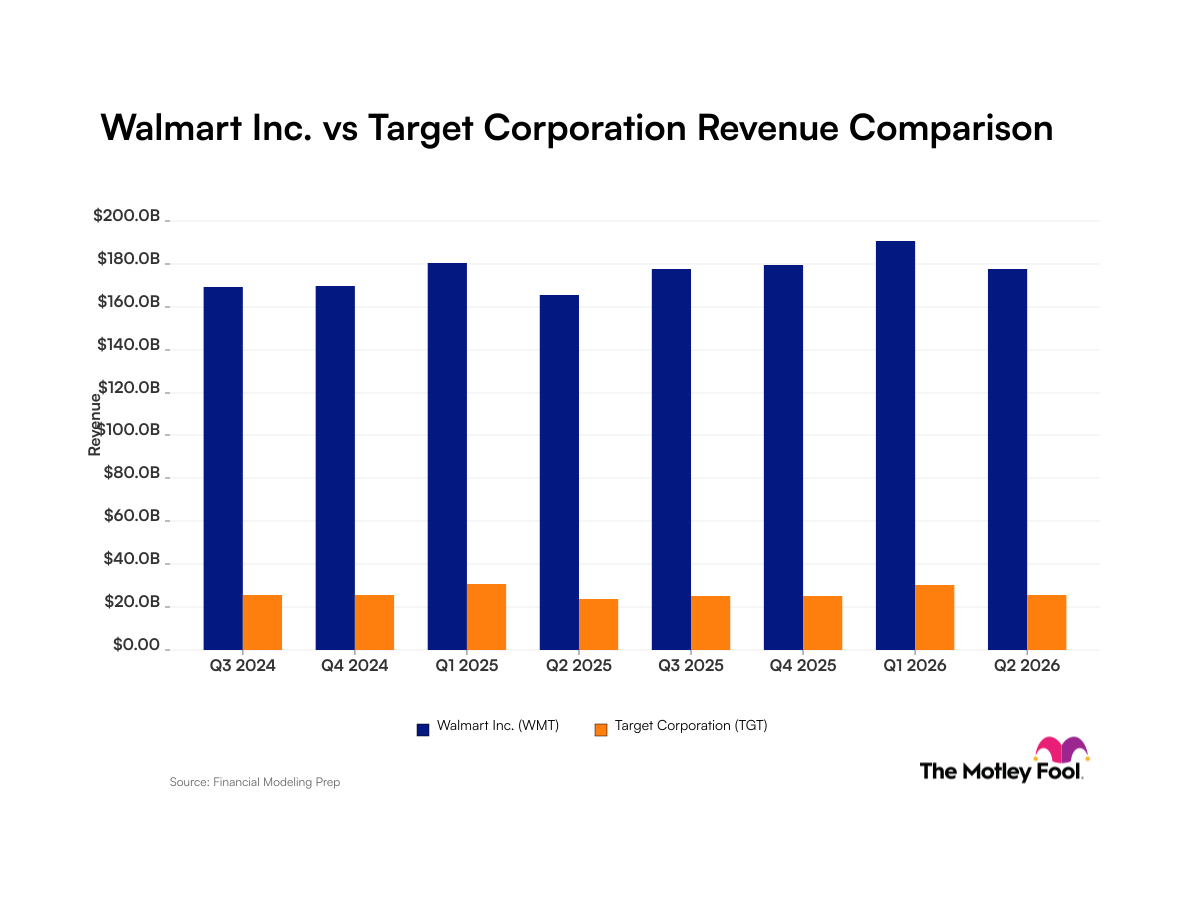

Walmart vs Target: Revenue Comparison

- Walmart's Revenue Stability: In Q1 2026, Walmart reported revenues of $190.7 billion, demonstrating robust performance in the global retail market, maintaining a net income margin of approximately 3%, which indicates sustained profitability despite competitive pressures.

- Target's Revenue Volatility: Target's revenue for Q1 2026 was $30.5 billion, with a similar net income margin of around 3%; however, its performance is subject to seasonal fluctuations, which may affect investor confidence in its long-term growth potential.

- Acquisition and Expansion: Walmart's acquisition of the connected TV advertising platform Vibe.co in June 2026 and the opening of a third owned milk processing facility aim to enhance its e-commerce advertising capabilities and product supply chain, further solidifying its market position.

- Executive Appointment and Partnerships: Target appointed a new Chief Global Supply Chain Officer in mid-2026 and established a multi-season merchandise partnership with Hollister, initiatives designed to improve supply chain efficiency and market responsiveness, despite the challenges posed by revenue volatility.

Walmart vs. Target Revenue Comparison

- Revenue Performance Gap: Walmart demonstrates a stronger revenue position through its massive scale and steady growth, while Target experiences sharp quarter-over-quarter revenue spikes during winter, indicating a smaller and more cyclical revenue base.

- Net Margin Comparison: Both Walmart and Target reported approximately 3% net income margin for the quarter ended April 30, 2026, but Walmart's more consistent revenue growth may widen the revenue gap in the future.

- Strategic Investment Moves: In June 2026, Walmart agreed to acquire the connected TV advertising platform Vibe.co and opened a third owned milk processing facility, reflecting its ongoing commitment to diversifying its business operations.

- Executive Changes and Partnerships: Target appointed a new chief global supply chain officer in mid-2026 and announced a multi-season merchandise partnership with Hollister, aiming to enhance its market competitiveness and supply chain efficiency.

Investment Outlook for Amazon, Walmart, and Costco

- Amazon's Growth Potential: Amazon's AWS cloud computing division boasts an annual revenue run rate of $150 billion, and with its e-commerce business and revamped cost structure, earnings are expected to strengthen further in the coming quarters, showcasing robust growth potential.

- Costco's Membership Model: Costco's renewal rates exceed 90% in its largest markets, the U.S. and Canada, providing visibility for future earnings, while its high-margin membership fees significantly contribute to profit growth, positioning the company for long-term success.

- Walmart's Market Advantage: Walmart's low-price strategy and advancements in digital sales led to a 26% increase in global e-commerce sales and a 17% rise in membership fee revenue in the latest quarter, ensuring stable revenue and growth potential amid competition.

- Investment Choice Analysis: While Amazon, Walmart, and Costco each have their strengths, Amazon is viewed as the best investment choice for the second half due to its lower valuation and superior revenue growth potential, particularly as it remains competitive even during economic slowdowns.

Investment Outlook for Amazon, Walmart, and Costco

- Amazon's Earnings Potential: Amazon's AWS cloud computing division boasts an annual revenue run rate of $150 billion, and with the company's restructuring of its cost structure, earnings are expected to strengthen further in the coming quarters, boosting investor confidence.

- Costco's Membership Model: Costco's renewal rates exceed 90% in its largest markets of the U.S. and Canada, with high-margin membership fees providing a stable revenue source that ensures sustainable long-term profit growth.

- Walmart's Market Advantage: With global e-commerce sales rising 26% and membership fee revenue increasing by 17%, Walmart's advertising business also achieved 37% growth, showcasing its strong market competitiveness and revenue stability.

- Emerging Investment Opportunities: Despite recent stock price pullbacks for all three companies, their long-term prospects remain robust, particularly with Amazon trading at a relatively lower valuation, making it an ideal choice for investors in the second half of 2026.

Walmart Lowers Prices Amid Competitive Pressure

- Pricing Strategy: Walmart has lowered prices on various grocery and seasonal items at both Walmart and Sam's Club, including a nearly 15% reduction in ground beef prices, addressing consumer concerns over high prices amid a 4.2% inflation rate in the U.S.

- Analyst Support: BofA analyst Christopher Nardone stated that the price cuts will be funded through existing financial guidance and tariff refunds, indicating the company's willingness to compete aggressively in the highly competitive grocery market while maintaining margins.

- Market Reaction: Despite Walmart's stock facing a fourth consecutive week of losses, both BofA and Mizuho have maintained their 'Outperform' ratings, with Mizuho setting a price target of $137, suggesting a 24% upside, reflecting confidence in the effectiveness of the pricing strategy.

- Cost Pressure Relief: Walmart expects to receive over $2 billion in tariff refunds, and the decline in diesel prices has eased cost pressures, with the full-year fuel impact now estimated to be between $700 million and $800 million, further supporting the sustainability of its price-cutting strategy.

India's IPO Market Faces Major Risks Amid Geopolitical Tensions

- IPO Plans Under Threat: Trump's decision to end the ceasefire with Iran poses significant risks to India's anticipated $50 billion IPO pipeline, causing a more than 2% market slump and highlighting the increasing impact of geopolitical risks on financial markets.

- Weak Market Performance: IPO activity in India for 2026 has been lackluster compared to the U.S. and Hong Kong, raising only $4 billion in the first half, in stark contrast to the $128 billion and $27 billion raised in those markets, indicating insufficient market absorption for new listings.

- Regulatory Approval Progress: Approximately $22 billion worth of IPOs are seeking regulatory approval, expected to take 2-3 months, while $29 billion worth have already been approved, including major firms like Zepto and Avaada Electro, suggesting potential opportunities still exist in the market.

- Economic Transformation Context: India's economy is transforming with the rise of new manufacturing industries driven by digital technology adoption and tax reforms, and despite unfavorable market conditions, companies are still seeking to list to unlock growth potential, reflecting confidence in future prospects.

Walmart vs Target: Revenue Comparison

- Walmart's Revenue Stability: In Q1 2026, Walmart reported revenues of $190.7 billion, demonstrating robust performance in the global retail market, maintaining a net income margin of approximately 3%, which indicates sustained profitability despite competitive pressures.

- Target's Revenue Volatility: Target's revenue for Q1 2026 was $30.5 billion, with a similar net income margin of around 3%; however, its performance is subject to seasonal fluctuations, which may affect investor confidence in its long-term growth potential.

- Acquisition and Expansion: Walmart's acquisition of the connected TV advertising platform Vibe.co in June 2026 and the opening of a third owned milk processing facility aim to enhance its e-commerce advertising capabilities and product supply chain, further solidifying its market position.

- Executive Appointment and Partnerships: Target appointed a new Chief Global Supply Chain Officer in mid-2026 and established a multi-season merchandise partnership with Hollister, initiatives designed to improve supply chain efficiency and market responsiveness, despite the challenges posed by revenue volatility.

Walmart vs. Target Revenue Comparison

- Revenue Performance Gap: Walmart demonstrates a stronger revenue position through its massive scale and steady growth, while Target experiences sharp quarter-over-quarter revenue spikes during winter, indicating a smaller and more cyclical revenue base.

- Net Margin Comparison: Both Walmart and Target reported approximately 3% net income margin for the quarter ended April 30, 2026, but Walmart's more consistent revenue growth may widen the revenue gap in the future.

- Strategic Investment Moves: In June 2026, Walmart agreed to acquire the connected TV advertising platform Vibe.co and opened a third owned milk processing facility, reflecting its ongoing commitment to diversifying its business operations.

- Executive Changes and Partnerships: Target appointed a new chief global supply chain officer in mid-2026 and announced a multi-season merchandise partnership with Hollister, aiming to enhance its market competitiveness and supply chain efficiency.

Investment Outlook for Amazon, Walmart, and Costco

- Amazon's Growth Potential: Amazon's AWS cloud computing division boasts an annual revenue run rate of $150 billion, and with its e-commerce business and revamped cost structure, earnings are expected to strengthen further in the coming quarters, showcasing robust growth potential.

- Costco's Membership Model: Costco's renewal rates exceed 90% in its largest markets, the U.S. and Canada, providing visibility for future earnings, while its high-margin membership fees significantly contribute to profit growth, positioning the company for long-term success.

- Walmart's Market Advantage: Walmart's low-price strategy and advancements in digital sales led to a 26% increase in global e-commerce sales and a 17% rise in membership fee revenue in the latest quarter, ensuring stable revenue and growth potential amid competition.

- Investment Choice Analysis: While Amazon, Walmart, and Costco each have their strengths, Amazon is viewed as the best investment choice for the second half due to its lower valuation and superior revenue growth potential, particularly as it remains competitive even during economic slowdowns.

Investment Outlook for Amazon, Walmart, and Costco

- Amazon's Earnings Potential: Amazon's AWS cloud computing division boasts an annual revenue run rate of $150 billion, and with the company's restructuring of its cost structure, earnings are expected to strengthen further in the coming quarters, boosting investor confidence.

- Costco's Membership Model: Costco's renewal rates exceed 90% in its largest markets of the U.S. and Canada, with high-margin membership fees providing a stable revenue source that ensures sustainable long-term profit growth.

- Walmart's Market Advantage: With global e-commerce sales rising 26% and membership fee revenue increasing by 17%, Walmart's advertising business also achieved 37% growth, showcasing its strong market competitiveness and revenue stability.

- Emerging Investment Opportunities: Despite recent stock price pullbacks for all three companies, their long-term prospects remain robust, particularly with Amazon trading at a relatively lower valuation, making it an ideal choice for investors in the second half of 2026.