Target Reports Q4 2025 Earnings Amid Market Challenges

Target Corp's stock rose by 5.00% as it crossed above the 5-day SMA, despite the broader market decline with the Nasdaq-100 down 1.50% and S&P 500 down 1.39%.

The company reported its Q4 2025 earnings, revealing a GAAP EPS of $2.30, down 4.5% from the previous year, while adjusted EPS increased to $2.44, indicating some resilience in a challenging environment. However, net sales fell by 1.5% year-over-year to $30.5 billion, with comparable sales down 2.5%, reflecting weak consumer demand. The company anticipates approximately 2% net sales growth for FY 2026, showing confidence in future market conditions despite current pressures on profitability and sales performance.

This earnings report highlights the challenges Target faces in maintaining profitability amid declining sales, but the positive adjusted EPS and future growth expectations may bolster investor confidence.

Trade with 70% Backtested Accuracy

Analyst Views on TGT

About TGT

About the author

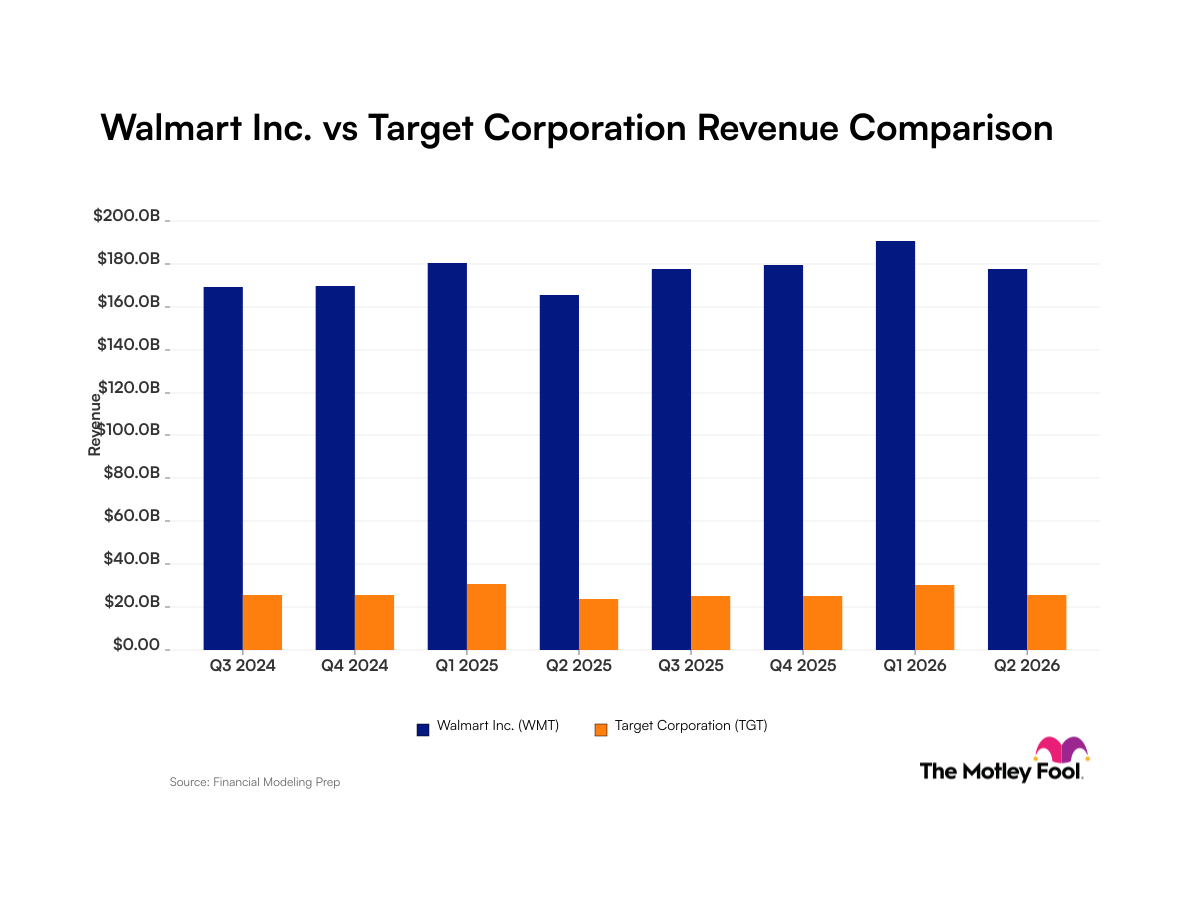

Walmart vs Target: Revenue Comparison

- Walmart's Revenue Stability: In Q1 2026, Walmart reported revenues of $190.7 billion, demonstrating robust performance in the global retail market, maintaining a net income margin of approximately 3%, which indicates sustained profitability despite competitive pressures.

- Target's Revenue Volatility: Target's revenue for Q1 2026 was $30.5 billion, with a similar net income margin of around 3%; however, its performance is subject to seasonal fluctuations, which may affect investor confidence in its long-term growth potential.

- Acquisition and Expansion: Walmart's acquisition of the connected TV advertising platform Vibe.co in June 2026 and the opening of a third owned milk processing facility aim to enhance its e-commerce advertising capabilities and product supply chain, further solidifying its market position.

- Executive Appointment and Partnerships: Target appointed a new Chief Global Supply Chain Officer in mid-2026 and established a multi-season merchandise partnership with Hollister, initiatives designed to improve supply chain efficiency and market responsiveness, despite the challenges posed by revenue volatility.

Walmart vs. Target Revenue Comparison

- Revenue Performance Gap: Walmart demonstrates a stronger revenue position through its massive scale and steady growth, while Target experiences sharp quarter-over-quarter revenue spikes during winter, indicating a smaller and more cyclical revenue base.

- Net Margin Comparison: Both Walmart and Target reported approximately 3% net income margin for the quarter ended April 30, 2026, but Walmart's more consistent revenue growth may widen the revenue gap in the future.

- Strategic Investment Moves: In June 2026, Walmart agreed to acquire the connected TV advertising platform Vibe.co and opened a third owned milk processing facility, reflecting its ongoing commitment to diversifying its business operations.

- Executive Changes and Partnerships: Target appointed a new chief global supply chain officer in mid-2026 and announced a multi-season merchandise partnership with Hollister, aiming to enhance its market competitiveness and supply chain efficiency.

Walmart's Major Price Cuts Spark Competitive Pressure

- Price Cut Implementation: Walmart confirmed broad discounts across its Walmart and Sam's Club stores, including a nearly 15% reduction in ground beef prices, aimed at celebrating the U.S. 250th anniversary, despite persistent inflation, showcasing the company's strategic response to economic pressures.

- Economic Context Impact: The U.S. Consumer Price Index (CPI) rose to 4.2% in May, the highest since April 2023, and Walmart's price cuts not only address consumer concerns over living costs but may also carry significant political weight ahead of the upcoming midterm elections.

- Competitor Response: Walmart's price cuts have put pressure on competitors, with Target's stock sliding over 3%, indicating its limited flexibility in reducing prices on everyday essentials without jeopardizing profitability, highlighting differing financial realities among retailers.

- Market Sentiment Shift: On Stocktwits, retail sentiment around Walmart remained bullish, with message volume surging 1,783% in 24 hours, reflecting investor optimism about the company's future performance, even as its stock has slipped 0.6% year-to-date.

Target Stock Rebounds, Investor Confidence Restored

- Sales Growth Recovery: Target reported a 7% year-over-year net sales growth in Q1 2026, although below Costco's 10%, this performance significantly boosted investor optimism, indicating a gradual recovery in market competitiveness.

- P/E Ratio Advantage: With a P/E ratio of 18, Target is well below Walmart's 40 and Costco's 48, showcasing its relative value in the current market environment, which may attract more value-seeking investors.

- Dividend King Status: Target has raised its dividend for the 55th consecutive year, with a current yield of 3.4%, far exceeding the S&P 500's 1.1%, making it more appealing to income-oriented investors, especially in comparison to its competitors' yields.

- Future Investment Plans: Despite facing a 25% decline in net earnings, Target plans to invest approximately $5 billion over the coming years to improve stores and supply chains, which could lay the groundwork for long-term growth and enhance its market position.

Target Stock Rebounds, Investor Confidence Grows

- Stock Rebound: Target's stock has surged nearly 65% from its 52-week low, reflecting investor confidence in the upgrades under new CEO Michael Fiddelke, although it still trades nearly 50% below its 2021 all-time high, indicating a positive market outlook for its future.

- P/E Ratio Advantage: Despite the price increase, Target's P/E ratio stands at 18, significantly lower than Walmart's and Costco's 40 and 48, respectively, suggesting it remains attractive in the competitive landscape and may draw more value-focused investors.

- Dividend Growth: Target has raised its dividend for the 55th consecutive year, achieving a yield of 3.4%, which is well above the S&P 500's average of 1.1% and its competitors' yields of 0.8% and 0.6%, making it a preferred choice for income-oriented investors.

- Sales Growth Potential: Despite facing three consecutive years of declining sales, Target reported a 7% year-over-year sales growth in Q1 2026, closely matching Walmart's growth, showcasing its potential in improving supply chains and product offerings, which could continue to attract investors moving forward.

UBS's Top Stock Picks for Q3 2026

- Vertiv Stock Surge: Vertiv's stock has surged 92% this year, establishing itself as a favored AI infrastructure play, with UBS analysts noting its strong cash flow return on investment and high asset growth rates, suggesting that its upward value creation trajectory remains intact.

- Nvidia Economic Profit: Although Nvidia's stock is only up 6% in 2026, UBS still regards it as an exemplary wealth compounder, forecasting a doubling of its economic profit by 2027, with analysts' consensus indicating over 50% upside potential from current levels.

- Ralph Lauren Recovery: Ralph Lauren's stock has rallied 13% this year, with UBS highlighting a sharp rebound in cash flow return on investment from pandemic lows, projecting a decade-high of 15%, while the market remains optimistic about its long-term growth potential with a target price suggesting an additional 7% upside.

- Diverse Stock Picks: UBS's list also includes Spotify, Boston Scientific, Target, and Coca-Cola, reflecting confidence in a diversified investment strategy aimed at capitalizing on opportunities arising from market recovery.

Walmart vs Target: Revenue Comparison

- Walmart's Revenue Stability: In Q1 2026, Walmart reported revenues of $190.7 billion, demonstrating robust performance in the global retail market, maintaining a net income margin of approximately 3%, which indicates sustained profitability despite competitive pressures.

- Target's Revenue Volatility: Target's revenue for Q1 2026 was $30.5 billion, with a similar net income margin of around 3%; however, its performance is subject to seasonal fluctuations, which may affect investor confidence in its long-term growth potential.

- Acquisition and Expansion: Walmart's acquisition of the connected TV advertising platform Vibe.co in June 2026 and the opening of a third owned milk processing facility aim to enhance its e-commerce advertising capabilities and product supply chain, further solidifying its market position.

- Executive Appointment and Partnerships: Target appointed a new Chief Global Supply Chain Officer in mid-2026 and established a multi-season merchandise partnership with Hollister, initiatives designed to improve supply chain efficiency and market responsiveness, despite the challenges posed by revenue volatility.

Walmart vs. Target Revenue Comparison

- Revenue Performance Gap: Walmart demonstrates a stronger revenue position through its massive scale and steady growth, while Target experiences sharp quarter-over-quarter revenue spikes during winter, indicating a smaller and more cyclical revenue base.

- Net Margin Comparison: Both Walmart and Target reported approximately 3% net income margin for the quarter ended April 30, 2026, but Walmart's more consistent revenue growth may widen the revenue gap in the future.

- Strategic Investment Moves: In June 2026, Walmart agreed to acquire the connected TV advertising platform Vibe.co and opened a third owned milk processing facility, reflecting its ongoing commitment to diversifying its business operations.

- Executive Changes and Partnerships: Target appointed a new chief global supply chain officer in mid-2026 and announced a multi-season merchandise partnership with Hollister, aiming to enhance its market competitiveness and supply chain efficiency.

Walmart's Major Price Cuts Spark Competitive Pressure

- Price Cut Implementation: Walmart confirmed broad discounts across its Walmart and Sam's Club stores, including a nearly 15% reduction in ground beef prices, aimed at celebrating the U.S. 250th anniversary, despite persistent inflation, showcasing the company's strategic response to economic pressures.

- Economic Context Impact: The U.S. Consumer Price Index (CPI) rose to 4.2% in May, the highest since April 2023, and Walmart's price cuts not only address consumer concerns over living costs but may also carry significant political weight ahead of the upcoming midterm elections.

- Competitor Response: Walmart's price cuts have put pressure on competitors, with Target's stock sliding over 3%, indicating its limited flexibility in reducing prices on everyday essentials without jeopardizing profitability, highlighting differing financial realities among retailers.

- Market Sentiment Shift: On Stocktwits, retail sentiment around Walmart remained bullish, with message volume surging 1,783% in 24 hours, reflecting investor optimism about the company's future performance, even as its stock has slipped 0.6% year-to-date.

Target Stock Rebounds, Investor Confidence Restored

- Sales Growth Recovery: Target reported a 7% year-over-year net sales growth in Q1 2026, although below Costco's 10%, this performance significantly boosted investor optimism, indicating a gradual recovery in market competitiveness.

- P/E Ratio Advantage: With a P/E ratio of 18, Target is well below Walmart's 40 and Costco's 48, showcasing its relative value in the current market environment, which may attract more value-seeking investors.

- Dividend King Status: Target has raised its dividend for the 55th consecutive year, with a current yield of 3.4%, far exceeding the S&P 500's 1.1%, making it more appealing to income-oriented investors, especially in comparison to its competitors' yields.

- Future Investment Plans: Despite facing a 25% decline in net earnings, Target plans to invest approximately $5 billion over the coming years to improve stores and supply chains, which could lay the groundwork for long-term growth and enhance its market position.

Target Stock Rebounds, Investor Confidence Grows

- Stock Rebound: Target's stock has surged nearly 65% from its 52-week low, reflecting investor confidence in the upgrades under new CEO Michael Fiddelke, although it still trades nearly 50% below its 2021 all-time high, indicating a positive market outlook for its future.

- P/E Ratio Advantage: Despite the price increase, Target's P/E ratio stands at 18, significantly lower than Walmart's and Costco's 40 and 48, respectively, suggesting it remains attractive in the competitive landscape and may draw more value-focused investors.

- Dividend Growth: Target has raised its dividend for the 55th consecutive year, achieving a yield of 3.4%, which is well above the S&P 500's average of 1.1% and its competitors' yields of 0.8% and 0.6%, making it a preferred choice for income-oriented investors.

- Sales Growth Potential: Despite facing three consecutive years of declining sales, Target reported a 7% year-over-year sales growth in Q1 2026, closely matching Walmart's growth, showcasing its potential in improving supply chains and product offerings, which could continue to attract investors moving forward.

UBS's Top Stock Picks for Q3 2026

- Vertiv Stock Surge: Vertiv's stock has surged 92% this year, establishing itself as a favored AI infrastructure play, with UBS analysts noting its strong cash flow return on investment and high asset growth rates, suggesting that its upward value creation trajectory remains intact.

- Nvidia Economic Profit: Although Nvidia's stock is only up 6% in 2026, UBS still regards it as an exemplary wealth compounder, forecasting a doubling of its economic profit by 2027, with analysts' consensus indicating over 50% upside potential from current levels.

- Ralph Lauren Recovery: Ralph Lauren's stock has rallied 13% this year, with UBS highlighting a sharp rebound in cash flow return on investment from pandemic lows, projecting a decade-high of 15%, while the market remains optimistic about its long-term growth potential with a target price suggesting an additional 7% upside.

- Diverse Stock Picks: UBS's list also includes Spotify, Boston Scientific, Target, and Coca-Cola, reflecting confidence in a diversified investment strategy aimed at capitalizing on opportunities arising from market recovery.