PulteGroup announces $800 million bond offering to optimize capital structure

PulteGroup's stock price increased by 3.01% and reached a 52-week high following the announcement of an $800 million senior unsecured notes offering.

The offering includes $400 million of 4.250% notes due in 2031 and $400 million of 4.900% notes due in 2036, aimed at repaying existing senior notes and reducing financial costs. This move demonstrates the company's strong capital market financing capabilities and has garnered positive market sentiment, reflecting confidence in PulteGroup's financial health.

The successful bond offering is expected to enhance PulteGroup's capital structure, allowing the company to manage its debt more effectively and potentially invest in growth opportunities, further solidifying its position in the housing market.

Trade with 70% Backtested Accuracy

Analyst Views on PHM

About PHM

About the author

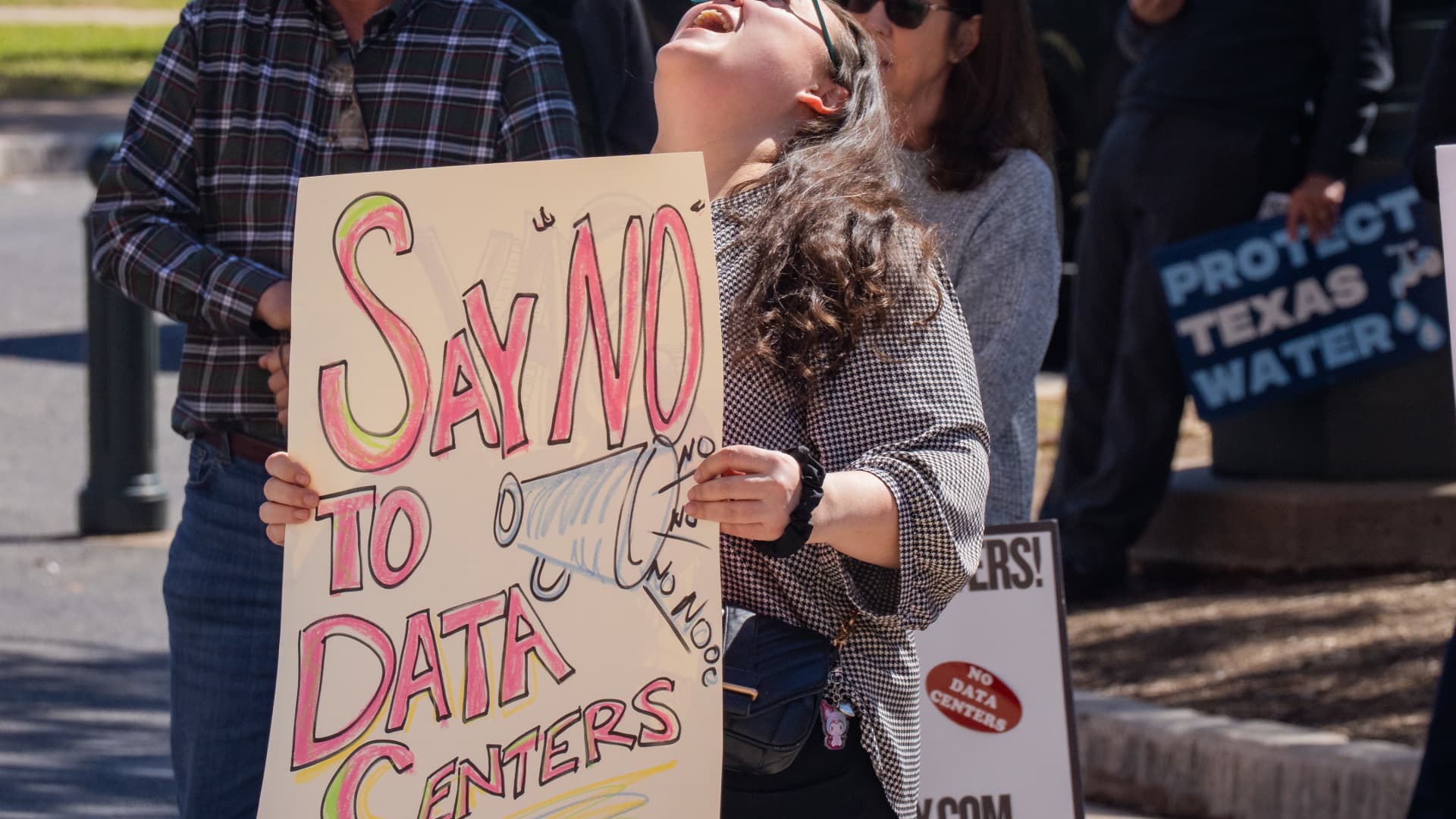

The Rise and Challenges of Home Data Centers

- Legislative Developments: Maine's legislature passed a data center ban, though it failed to override the governor's veto, indicating rising public discontent with data centers, as 14 states consider similar legislation reflecting concerns over big tech's influence.

- Massive Investment Trends: U.S. tech companies are projected to spend up to $1 trillion annually on AI by 2027, with global data center spending expected to reach $7 trillion by 2030, illustrating a significant influx of capital despite public opposition.

- Home Data Center Model: PulteGroup is collaborating with Nvidia and startup Span to test the installation of small data center nodes on new homes' exterior walls, although the scalability and regulatory approval of this model remain uncertain, its potential for energy efficiency and cost savings is noteworthy.

- Technical and Security Challenges: Home data centers face significant technical limitations regarding power density, connectivity, and security, as they may work for specific workloads, but high-density AI training and real-time tasks present major challenges, with experts highlighting concerns over reliability and security in residential settings.

US Stocks Close: Tech Stocks Show Strong Performance

- Uber Earnings Preview: Uber's CEO Dara Khosrowshahi will discuss quarterly results on the morning show, with the stock down 3% over the past three months, yet market anticipation for the earnings report could boost investor confidence and influence future stock performance.

- Disney Earnings Forecast: Disney is set to release its earnings in the morning, with a 4.3% decline in stock price over the past three months and a 19% drop from the June 30 high, prompting investor interest in how the company plans to navigate market challenges to regain growth.

- AMD Stock Recovery: Following a strong first-quarter performance that exceeded analyst expectations, AMD's stock rose 13%, driven by robust data center growth, and has surged 300% over the past year, highlighting the company's strong position in the semiconductor industry.

- Rockwell Automation Strong Growth: Rockwell Automation reported earnings that beat expectations, with shares rising nearly 9%, and a 72% increase over the past year, reflecting the company's successful strategy in data center and warehouse automation sectors.

Span Introduces New Home Data Center Model

- Home Data Center Innovation: Span, in collaboration with Nvidia, has launched XFRA units, small data centers that can be installed on residential walls, leveraging unused local grid power, which is expected to significantly reduce household electricity costs and enhance energy efficiency.

- Rapid Installation Advantage: Span claims that its XFRA units can be installed six times faster and at five times lower cost than traditional 100-megawatt data centers, making it easier for homeowners and small businesses to access efficient computing infrastructure.

- Smart Electrical Panel Integration: The Span system includes smart electrical panels, XFRA units, and home backup batteries, effectively utilizing existing power resources, allowing homeowners to receive compensation through flat-rate electricity and Wi-Fi, thereby enhancing economic benefits for users.

- Market Potential Assessment: PulteGroup is testing the capabilities and economics of XFRA nodes, and if the technology proves viable, it could alleviate local infrastructure burdens while providing homeowners with innovative technology and potential income sources.

Middle East Tensions Weigh on Stock Market Performance

- Market Decline: The S&P 500 index fell by 0.41%, the Dow Jones Industrial Average dropped by 1.13%, and the Nasdaq 100 index decreased by 0.21%, reflecting investor concerns over escalating tensions in the Middle East, which dampened market sentiment.

- Oil Price Surge: WTI crude oil prices surged over 4% following exchanges of fire between the US and Iran in the Strait of Hormuz, raising inflation expectations and pushing bond yields higher, with the 10-year T-note yield reaching a five-week high of 4.46%.

- Strong Economic Data: US March factory orders rose by 1.5% month-over-month, exceeding expectations of 0.6%, marking the largest increase in four months, indicating economic resilience that could provide support to the stock market.

- Earnings Optimism: As of Monday, 82% of the 322 S&P 500 companies that reported Q1 earnings exceeded estimates, with projected earnings growth of 12% year-over-year for Q1, although excluding the technology sector, the growth is only 3%, highlighting performance disparities across sectors.

Analysis of Investment Opportunities in Mid-Cap Stocks

- Ralph Lauren Performance Decline: With a market cap of $21.71 billion, Ralph Lauren's constant currency growth has fallen short over the past two years, indicating a need for investment in product improvements that could impact its future competitiveness in the fashion industry.

- PulteGroup Revenue Growth Struggles: PulteGroup, valued at $23.31 billion, has experienced only 1.2% annual revenue growth over the last two years, coupled with a concerning 7.7% annual decline in earnings per share, suggesting that increasing competition is eroding its profitability.

- SoFi Strong Growth Potential: SoFi, with a market cap of $20.53 billion, has achieved an impressive 33.4% annual revenue growth over the past two years, and its earnings per share surged by 396%, reflecting its robust performance and increasing market share in the digital financial services sector.

- Intensifying Market Competition: Mid-cap stocks are facing fierce competition from both industry giants and agile small players, and while they hold significant potential, investors must carefully assess the financial health and market adaptability of these companies.

US Housing Market Faces Continued Stagnation Amid High Mortgage Rates

- Stagnant Home Sales: Since the pandemic, existing home sales in the US have averaged around 4 million annually, significantly lower than the pre-pandemic level of 5.5 million, with insufficient inventory pushing prices up and indicating weak market demand.

- Rising Mortgage Rates: The 30-year fixed mortgage rate has reached 6.45%, the highest since April, and with inflation pressures, further increases are likely, which could suppress home-buying interest and exacerbate market stagnation.

- Declining Builder Stocks: Homebuilder stocks, which initially benefited from market opportunities, have slumped since late 2024, with significant revenue declines reported by D.R. Horton and NVR, highlighting the ongoing weakness in the housing market.

- Uncertain Market Outlook: Despite a housing shortage, the recovery in home sales and construction activity remains distant due to high rates and a weak labor market, suggesting that significant growth is unlikely in the near term.

The Rise and Challenges of Home Data Centers

- Legislative Developments: Maine's legislature passed a data center ban, though it failed to override the governor's veto, indicating rising public discontent with data centers, as 14 states consider similar legislation reflecting concerns over big tech's influence.

- Massive Investment Trends: U.S. tech companies are projected to spend up to $1 trillion annually on AI by 2027, with global data center spending expected to reach $7 trillion by 2030, illustrating a significant influx of capital despite public opposition.

- Home Data Center Model: PulteGroup is collaborating with Nvidia and startup Span to test the installation of small data center nodes on new homes' exterior walls, although the scalability and regulatory approval of this model remain uncertain, its potential for energy efficiency and cost savings is noteworthy.

- Technical and Security Challenges: Home data centers face significant technical limitations regarding power density, connectivity, and security, as they may work for specific workloads, but high-density AI training and real-time tasks present major challenges, with experts highlighting concerns over reliability and security in residential settings.

US Stocks Close: Tech Stocks Show Strong Performance

- Uber Earnings Preview: Uber's CEO Dara Khosrowshahi will discuss quarterly results on the morning show, with the stock down 3% over the past three months, yet market anticipation for the earnings report could boost investor confidence and influence future stock performance.

- Disney Earnings Forecast: Disney is set to release its earnings in the morning, with a 4.3% decline in stock price over the past three months and a 19% drop from the June 30 high, prompting investor interest in how the company plans to navigate market challenges to regain growth.

- AMD Stock Recovery: Following a strong first-quarter performance that exceeded analyst expectations, AMD's stock rose 13%, driven by robust data center growth, and has surged 300% over the past year, highlighting the company's strong position in the semiconductor industry.

- Rockwell Automation Strong Growth: Rockwell Automation reported earnings that beat expectations, with shares rising nearly 9%, and a 72% increase over the past year, reflecting the company's successful strategy in data center and warehouse automation sectors.

Span Introduces New Home Data Center Model

- Home Data Center Innovation: Span, in collaboration with Nvidia, has launched XFRA units, small data centers that can be installed on residential walls, leveraging unused local grid power, which is expected to significantly reduce household electricity costs and enhance energy efficiency.

- Rapid Installation Advantage: Span claims that its XFRA units can be installed six times faster and at five times lower cost than traditional 100-megawatt data centers, making it easier for homeowners and small businesses to access efficient computing infrastructure.

- Smart Electrical Panel Integration: The Span system includes smart electrical panels, XFRA units, and home backup batteries, effectively utilizing existing power resources, allowing homeowners to receive compensation through flat-rate electricity and Wi-Fi, thereby enhancing economic benefits for users.

- Market Potential Assessment: PulteGroup is testing the capabilities and economics of XFRA nodes, and if the technology proves viable, it could alleviate local infrastructure burdens while providing homeowners with innovative technology and potential income sources.

Middle East Tensions Weigh on Stock Market Performance

- Market Decline: The S&P 500 index fell by 0.41%, the Dow Jones Industrial Average dropped by 1.13%, and the Nasdaq 100 index decreased by 0.21%, reflecting investor concerns over escalating tensions in the Middle East, which dampened market sentiment.

- Oil Price Surge: WTI crude oil prices surged over 4% following exchanges of fire between the US and Iran in the Strait of Hormuz, raising inflation expectations and pushing bond yields higher, with the 10-year T-note yield reaching a five-week high of 4.46%.

- Strong Economic Data: US March factory orders rose by 1.5% month-over-month, exceeding expectations of 0.6%, marking the largest increase in four months, indicating economic resilience that could provide support to the stock market.

- Earnings Optimism: As of Monday, 82% of the 322 S&P 500 companies that reported Q1 earnings exceeded estimates, with projected earnings growth of 12% year-over-year for Q1, although excluding the technology sector, the growth is only 3%, highlighting performance disparities across sectors.

Analysis of Investment Opportunities in Mid-Cap Stocks

- Ralph Lauren Performance Decline: With a market cap of $21.71 billion, Ralph Lauren's constant currency growth has fallen short over the past two years, indicating a need for investment in product improvements that could impact its future competitiveness in the fashion industry.

- PulteGroup Revenue Growth Struggles: PulteGroup, valued at $23.31 billion, has experienced only 1.2% annual revenue growth over the last two years, coupled with a concerning 7.7% annual decline in earnings per share, suggesting that increasing competition is eroding its profitability.

- SoFi Strong Growth Potential: SoFi, with a market cap of $20.53 billion, has achieved an impressive 33.4% annual revenue growth over the past two years, and its earnings per share surged by 396%, reflecting its robust performance and increasing market share in the digital financial services sector.

- Intensifying Market Competition: Mid-cap stocks are facing fierce competition from both industry giants and agile small players, and while they hold significant potential, investors must carefully assess the financial health and market adaptability of these companies.

US Housing Market Faces Continued Stagnation Amid High Mortgage Rates

- Stagnant Home Sales: Since the pandemic, existing home sales in the US have averaged around 4 million annually, significantly lower than the pre-pandemic level of 5.5 million, with insufficient inventory pushing prices up and indicating weak market demand.

- Rising Mortgage Rates: The 30-year fixed mortgage rate has reached 6.45%, the highest since April, and with inflation pressures, further increases are likely, which could suppress home-buying interest and exacerbate market stagnation.

- Declining Builder Stocks: Homebuilder stocks, which initially benefited from market opportunities, have slumped since late 2024, with significant revenue declines reported by D.R. Horton and NVR, highlighting the ongoing weakness in the housing market.

- Uncertain Market Outlook: Despite a housing shortage, the recovery in home sales and construction activity remains distant due to high rates and a weak labor market, suggesting that significant growth is unlikely in the near term.