Potential Successor to Warren Buffett at Berkshire Faces Significant Challenges

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Dec 31 2025

0mins

Source: Barron's

Ted Weschler's Role: Ted Weschler is poised to become Berkshire Hathaway's leading stockpicker.

Investment Success: He transformed an IRA account of approximately $70,000 in the late 1980s into $221 million by 2018.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy CVX?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on CVX

Wall Street analysts forecast CVX stock price to fall

19 Analyst Rating

15 Buy

4 Hold

0 Sell

Strong Buy

Current: 191.100

Low

158.00

Averages

176.95

High

206.00

Current: 191.100

Low

158.00

Averages

176.95

High

206.00

About CVX

Chevron Corporation is an integrated energy company. The Company produces crude oil and natural gas; manufactures transportation fuels, lubricants, petrochemicals and additives; and develops technologies that enhance its business and industry. The Company’s segments include Upstream and Downstream. Upstream operations consist primarily of exploring for, developing, producing and transporting crude oil and natural gas; liquefaction, transportation and regasification associated with LNG; transporting crude oil by major international oil export pipelines; processing, transporting, storage and marketing of natural gas; carbon capture and storage; and a gas-to-liquids plant. Downstream operations consist primarily of the refining of crude oil into petroleum products; marketing crude oil, refined products, and lubricants; manufacturing and marketing of renewable fuels, and transporting of crude oil and refined products by pipeline, marine vessel, motor equipment and rail car.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Trump Warns Iran of Possible Conflict Resurgence

- Oil Price Surge: Trump's social media comments urging Iran to 'get moving' have led to a spike in oil prices overnight, raising concerns about a potential resurgence of conflict that could destabilize global energy markets.

- Market Volatility: Following Trump's remarks, stock futures have fallen, setting Wall Street up for another day of significant losses, highlighting the direct impact of political factors on market sentiment.

- Delta Air Lines Investment: Berkshire Hathaway's announcement of a $2.6 billion stake in Delta Air Lines, making it the company's 14th largest holding, reflects confidence in the airline industry's recovery and may drive Delta's stock price higher.

- Meta Layoff Plans: Meta is expected to lay off about 10% of its workforce this week, amidst widespread layoffs in the tech sector, which could dampen employee morale and underscores the company's urgent need for cost control.

See More

Trump Warns Iran Amid Rising Tensions

- Oil Price Surge: Trump's statement urging Iran to 'get moving' has led to a sharp increase in oil prices overnight, raising concerns that the conflict could reignite, which may impact global energy markets and investor confidence.

- Market Volatility: Following Trump's comments, stock futures fell, setting Wall Street up for potentially significant losses again, despite the S&P 500 managing to achieve its seventh consecutive winning week, indicating market fragility.

- Delta Airlines Stock Rise: Delta Airlines shares rose over 2% before the bell after Berkshire Hathaway revealed a $2.6 billion stake in the carrier, marking a return to the airline sector and potentially boosting market confidence in airline stocks.

- Lululemon's Shareholder Pressure: Lululemon's letter to shareholders criticized founder Chip Wilson's outdated views, which could derail the company's turnaround plan, urging shareholders to support its strategy at the upcoming annual meeting, highlighting the urgency of corporate governance issues.

See More

Nvidia Earnings in Focus as Market Reacts Mutedly

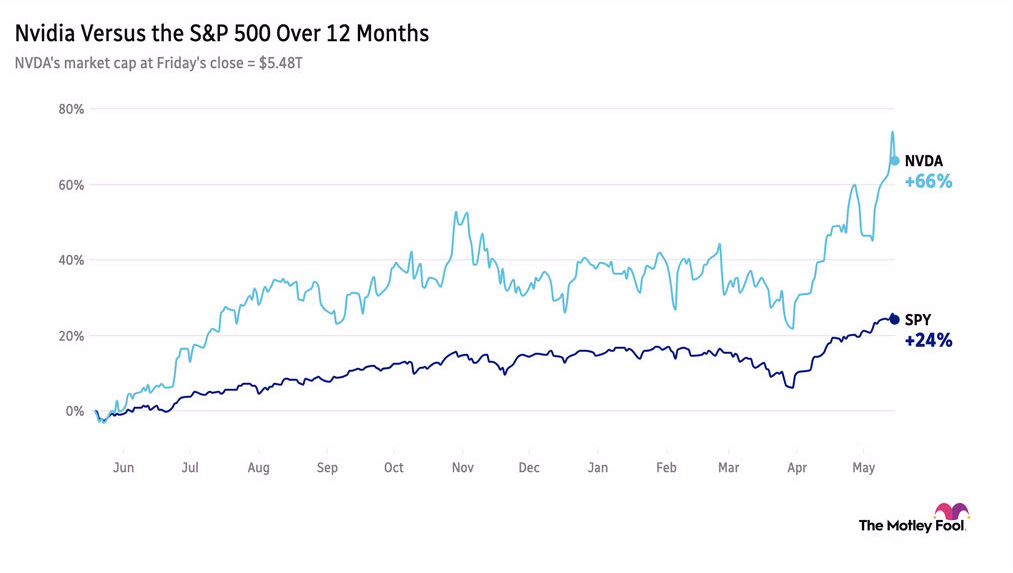

- Nvidia Earnings Expectations: Nvidia is expected to report an 80% year-over-year revenue growth for Q1, with its market cap briefly exceeding $5.7 trillion last week, underscoring its leadership in the AI sector, despite a 4.4% drop in stock price last Friday.

- Market Impact Analysis: Analysts note that Nvidia accounts for 9% of the S&P 500 index and contributed 20% to the index's total returns for 2026, highlighting its significant influence on overall market performance, particularly driven by AI stocks.

- Retail Earnings Outlook: TJX anticipates a 6% year-over-year revenue increase for Q1, while Walmart is expected to maintain strong performance following a 12% EPS growth, indicating continued consumer spending resilience.

- Berkshire Portfolio Adjustments: Berkshire Hathaway, under new CEO Abel, acquired a $2.6 billion stake in Delta Air Lines and reduced investments in banking and healthcare sectors, reflecting a strategy focused on concentrated investments.

See More

Berkshire Hathaway's Portfolio Revamp Triggers Stock Market Fluctuations

- Portfolio Restructuring: Under new CEO Greg Abel, Berkshire Hathaway's latest quarterly filing reveals a purchase of 39.8 million shares in Delta Airlines valued at $2.6 billion, making it the company's 14th largest holding, indicating a renewed confidence in the airline sector.

- Tech Stock Increase: Alphabet, Google's parent company, saw an increase of 58 million shares, up 224%, becoming Berkshire's seventh largest holding, despite a 0.6% drop in early trading, reflecting the market's mixed sentiment towards tech stocks.

- New Investments and Reductions: Berkshire initiated a new stake in Macy's while reducing its Chevron holdings by 35%, selling $8 billion worth of shares, with Macy's stock rising 5% in premarket trading, indicating optimism in retail stocks.

- Complete Exit from Amazon: Berkshire fully exited its investment in Amazon by selling 2.3 million shares in Q1, marking an adaptation to changing consumer behaviors post-pandemic, with Amazon's stock down 0.7% in early trading.

See More

Oil Prices Surge Amid U.S.-China Relations and Middle East Tensions

- Oil Price Surge: Brent crude futures rose about 1.81% and WTI crude futures increased by 2.18%, reflecting heightened market concern over Middle Eastern tensions, particularly following President Trump's strong remarks on Iran, which could influence global oil price trends.

- U.S. Oil Companies Benefit: Following Trump's announcement that China agreed to purchase U.S. crude oil, the United States Oil Fund (USO) rose by 2% and Exxon Mobil (XOM) climbed 0.7%, indicating increased investor confidence in the U.S. oil sector, potentially driving future investments and production.

- Market Sentiment Shift: While retail sentiment on USO remained neutral, sentiment for Exxon Mobil and Chevron leaned bearish, contrasting with the optimistic outlook for Conoco Phillips and Venture Global, highlighting differing market perceptions of various companies.

- U.S.-China Energy Cooperation Outlook: Trump's assertion that U.S. energy production surpasses that of Saudi Arabia and Russia combined underscores America's growing competitiveness in the global energy market, which may also lay the groundwork for future U.S.-China energy collaborations.

See More

Middle East Conflict Drives Oil Prices Up

- Investment Opportunities in Energy Stocks: The geopolitical conflict in the Middle East has led to supply constraints, driving oil prices sharply higher and sparking Wall Street's interest in energy stocks, particularly strong integrated companies like Chevron and ExxonMobil, which have demonstrated resilience throughout the energy cycle.

- Advantages of Integrated Energy Companies: Despite the inherent volatility of the oil and gas sector, integrated energy firms like TotalEnergies mitigate financial risks through diversified operations, with projections indicating that nearly 12% of its business will come from clean energy investments by 2025, showcasing its strategic positioning for future energy transitions.

- Dividend Yield Comparison: Chevron boasts a dividend yield of 3.8%, surpassing Exxon's 2.7%, while TotalEnergies offers a yield of 4.6%; although U.S. investors face French tax implications, its long-term growth potential and clean energy initiatives make it an attractive option.

- Market Outlook: As global demand for clean energy rises, investors should monitor how companies like TotalEnergies leverage profits from carbon fuel operations to build substantial clean energy businesses, positioning themselves favorably in the future energy landscape.

See More

Trump Warns Iran of Possible Conflict Resurgence

- Oil Price Surge: Trump's social media comments urging Iran to 'get moving' have led to a spike in oil prices overnight, raising concerns about a potential resurgence of conflict that could destabilize global energy markets.

- Market Volatility: Following Trump's remarks, stock futures have fallen, setting Wall Street up for another day of significant losses, highlighting the direct impact of political factors on market sentiment.

- Delta Air Lines Investment: Berkshire Hathaway's announcement of a $2.6 billion stake in Delta Air Lines, making it the company's 14th largest holding, reflects confidence in the airline industry's recovery and may drive Delta's stock price higher.

- Meta Layoff Plans: Meta is expected to lay off about 10% of its workforce this week, amidst widespread layoffs in the tech sector, which could dampen employee morale and underscores the company's urgent need for cost control.

See More

Trump Warns Iran Amid Rising Tensions

- Oil Price Surge: Trump's statement urging Iran to 'get moving' has led to a sharp increase in oil prices overnight, raising concerns that the conflict could reignite, which may impact global energy markets and investor confidence.

- Market Volatility: Following Trump's comments, stock futures fell, setting Wall Street up for potentially significant losses again, despite the S&P 500 managing to achieve its seventh consecutive winning week, indicating market fragility.

- Delta Airlines Stock Rise: Delta Airlines shares rose over 2% before the bell after Berkshire Hathaway revealed a $2.6 billion stake in the carrier, marking a return to the airline sector and potentially boosting market confidence in airline stocks.

- Lululemon's Shareholder Pressure: Lululemon's letter to shareholders criticized founder Chip Wilson's outdated views, which could derail the company's turnaround plan, urging shareholders to support its strategy at the upcoming annual meeting, highlighting the urgency of corporate governance issues.

See More

Nvidia Earnings in Focus as Market Reacts Mutedly

- Nvidia Earnings Expectations: Nvidia is expected to report an 80% year-over-year revenue growth for Q1, with its market cap briefly exceeding $5.7 trillion last week, underscoring its leadership in the AI sector, despite a 4.4% drop in stock price last Friday.

- Market Impact Analysis: Analysts note that Nvidia accounts for 9% of the S&P 500 index and contributed 20% to the index's total returns for 2026, highlighting its significant influence on overall market performance, particularly driven by AI stocks.

- Retail Earnings Outlook: TJX anticipates a 6% year-over-year revenue increase for Q1, while Walmart is expected to maintain strong performance following a 12% EPS growth, indicating continued consumer spending resilience.

- Berkshire Portfolio Adjustments: Berkshire Hathaway, under new CEO Abel, acquired a $2.6 billion stake in Delta Air Lines and reduced investments in banking and healthcare sectors, reflecting a strategy focused on concentrated investments.

See More

Berkshire Hathaway's Portfolio Revamp Triggers Stock Market Fluctuations

- Portfolio Restructuring: Under new CEO Greg Abel, Berkshire Hathaway's latest quarterly filing reveals a purchase of 39.8 million shares in Delta Airlines valued at $2.6 billion, making it the company's 14th largest holding, indicating a renewed confidence in the airline sector.

- Tech Stock Increase: Alphabet, Google's parent company, saw an increase of 58 million shares, up 224%, becoming Berkshire's seventh largest holding, despite a 0.6% drop in early trading, reflecting the market's mixed sentiment towards tech stocks.

- New Investments and Reductions: Berkshire initiated a new stake in Macy's while reducing its Chevron holdings by 35%, selling $8 billion worth of shares, with Macy's stock rising 5% in premarket trading, indicating optimism in retail stocks.

- Complete Exit from Amazon: Berkshire fully exited its investment in Amazon by selling 2.3 million shares in Q1, marking an adaptation to changing consumer behaviors post-pandemic, with Amazon's stock down 0.7% in early trading.

See More

Oil Prices Surge Amid U.S.-China Relations and Middle East Tensions

- Oil Price Surge: Brent crude futures rose about 1.81% and WTI crude futures increased by 2.18%, reflecting heightened market concern over Middle Eastern tensions, particularly following President Trump's strong remarks on Iran, which could influence global oil price trends.

- U.S. Oil Companies Benefit: Following Trump's announcement that China agreed to purchase U.S. crude oil, the United States Oil Fund (USO) rose by 2% and Exxon Mobil (XOM) climbed 0.7%, indicating increased investor confidence in the U.S. oil sector, potentially driving future investments and production.

- Market Sentiment Shift: While retail sentiment on USO remained neutral, sentiment for Exxon Mobil and Chevron leaned bearish, contrasting with the optimistic outlook for Conoco Phillips and Venture Global, highlighting differing market perceptions of various companies.

- U.S.-China Energy Cooperation Outlook: Trump's assertion that U.S. energy production surpasses that of Saudi Arabia and Russia combined underscores America's growing competitiveness in the global energy market, which may also lay the groundwork for future U.S.-China energy collaborations.

See More

Middle East Conflict Drives Oil Prices Up

- Investment Opportunities in Energy Stocks: The geopolitical conflict in the Middle East has led to supply constraints, driving oil prices sharply higher and sparking Wall Street's interest in energy stocks, particularly strong integrated companies like Chevron and ExxonMobil, which have demonstrated resilience throughout the energy cycle.

- Advantages of Integrated Energy Companies: Despite the inherent volatility of the oil and gas sector, integrated energy firms like TotalEnergies mitigate financial risks through diversified operations, with projections indicating that nearly 12% of its business will come from clean energy investments by 2025, showcasing its strategic positioning for future energy transitions.

- Dividend Yield Comparison: Chevron boasts a dividend yield of 3.8%, surpassing Exxon's 2.7%, while TotalEnergies offers a yield of 4.6%; although U.S. investors face French tax implications, its long-term growth potential and clean energy initiatives make it an attractive option.

- Market Outlook: As global demand for clean energy rises, investors should monitor how companies like TotalEnergies leverage profits from carbon fuel operations to build substantial clean energy businesses, positioning themselves favorably in the future energy landscape.

See More