Nucor's Q4 Guidance Misses The Mark, Hit By Steel Slowdown; Stock Slides

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Dec 17 2024

0mins

Source: Benzinga

Earnings Guidance: Nucor Corporation's fourth-quarter earnings per share (EPS) guidance is projected at $0.55 – $0.65, significantly lower than the consensus estimate of $0.86, primarily due to decreased volumes and lower average selling prices in the steel mills segment.

Share Repurchases and Financial Performance: The company has repurchased approximately 2.1 million shares in the fourth quarter, totaling 13.1 million shares for the year, while returning over $2.73 billion to shareholders through repurchases and dividends.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy NUE?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on NUE

Wall Street analysts forecast NUE stock price to fall

10 Analyst Rating

8 Buy

2 Hold

0 Sell

Strong Buy

Current: 219.020

Low

168.00

Averages

179.00

High

200.00

Current: 219.020

Low

168.00

Averages

179.00

High

200.00

About NUE

Nucor Corporation is a manufacturer of steel and steel products, with operating facilities in the United States, Canada and Mexico. The Company also produces and procures ferrous and non-ferrous materials primarily for use in its steel manufacturing business. Its segments include steel mills, steel products and raw materials. Its products include carbon and alloy steel in bars, beams, sheet and plate; hollow structural section tubing; electrical conduit; steel racking; steel piling; steel joists and joist girders; steel deck; fabricated concrete reinforcing steel; cold finished steel; precision castings; steel fasteners; metal building systems; insulated metal panels; overhead doors; steel grating; wire and wire mesh; and utility structures. The Company, through The David J. Joseph Company and its affiliates, also brokers ferrous and nonferrous metals, pig iron and hot briquetted iron / direct reduced iron; supplies ferro-alloys; and processes ferrous and nonferrous scrap.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Three Reliable Dividend Stocks to Hold

- Medical Device Leader: Medtronic boasts a 49-year dividend growth history with a current yield of 3.5%, and despite market fluctuations, its latest report indicates the highest annual revenue growth in a decade, reflecting effective restructuring efforts to enhance profitability.

- Real Estate Investment Trust: Realty Income offers a 5.2% dividend yield and has increased dividends for 31 consecutive years; as the largest net lease REIT, its portfolio spans North America and Europe, maintaining over 96% occupancy during economic downturns, showcasing its stability and reliability.

- Steel Industry Leader: Nucor, recognized as a Dividend King with over 50 consecutive annual hikes, currently has a low yield of 0.9%, yet its modern electric arc steel mills and strong employee relations enable it to perform well amid cyclical fluctuations, making it a solid long-term hold.

- Long-Term Investment Strategy: The author emphasizes a commitment to holding these quality stocks through market volatility, believing that Medtronic, Realty Income, and Nucor are proven successful companies that will continue to grow, making them worthy of attention for long-term investors.

See More

Anticipating a Deep Bear Market Ahead

- Healthcare Giant: Medtronic has maintained a dividend increase streak for 49 years, with a current yield of 3.5%, and despite market downturns, it recently reported its highest annual revenue growth in a decade, indicating a successful restructuring and potential for stable dividend growth even in a bear market.

- Real Estate Investment Trust: Realty Income offers a 5.2% dividend yield and has increased its dividend for 31 consecutive years; while not at historical highs, its absolute yield remains attractive, and its occupancy rate never dropped below 96% during the Great Recession, showcasing its reliability amid market fluctuations.

- Steel Industry Leader: Nucor, known for over 50 consecutive years of dividend increases, currently has a low yield of 0.9%, but has only reported one loss in the last four decades, demonstrating resilience in a cyclical industry, making it a potential quality pick for investors during a bear market.

- Long-Term Holding Strategy: The author intends to hold Medtronic, Realty Income, and Nucor through market volatility, believing that these companies' management capabilities and historical performance will enable continued growth in future market conditions, reflecting the value of long-term investing.

See More

Nucor Upgraded to Overweight by KeyBanc with $274 Target

- Rating Upgrade: KeyBanc upgraded Nucor from Sector Weight to Overweight with a $274 price target, reflecting confidence in the company's future performance despite a more than 10% drop in shares over the past six trading days.

- Earnings Guidance: Nucor guided for Q2 earnings between $4.50 and $4.60 per share, exceeding the FactSet analyst consensus of $4.21 and significantly higher than Q1's $3.23 and last year's Q2 EPS of $2.60, indicating ongoing improvement in profitability.

- Market Outlook: KeyBanc analyst expects Nucor's actual Q2 results to surpass company guidance, citing management's historical conservatism, while forecasting that steel prices will continue to rise at least through August, positively impacting the company's performance.

- Shipment Growth: Nucor's steel mill shipments are projected to increase nearly 10% year-over-year by 2026, suggesting that the company will benefit from strong steel pricing in the upcoming quarters, particularly in the seasonally strong fourth quarter.

See More

Latest Wall Street Rating Updates

- Citi Upgrade: Citi upgraded Macerich from Neutral to Buy, raising the target price from $24 to $28, indicating strong balance sheet strength that is expected to drive stock price appreciation.

- Citizens Initiation: Citizens initiated coverage on Bitdeer Holdings and Mara Holdings, stating that these bitcoin miners have significant potential to outperform the market by repurposing existing power capacity for high-performance computing.

- Mizuho's Biotech Outlook: Mizuho initiated coverage of Sol-Gel Technologies with an Outperform rating and a $285 price target, suggesting that the biotech firm is well-positioned for future growth in a competitive landscape.

- Goldman on Twilio: Goldman Sachs initiated coverage of Twilio with a Buy rating and a 12-month price target of $300, highlighting expected margin upside that reflects strong confidence in the company's financial prospects.

See More

NU E Power Announces Non-Brokered Private Placement of Up to $3 Million

- Funding Size: NU E Power Corp. intends to issue up to 20,000,000 units at a price of $0.15 per unit, aiming for total gross proceeds of up to $3 million to support its renewable energy projects.

- Subscription Terms: Each unit consists of one common share and half a warrant, with warrants allowing the purchase of additional shares at $0.25 for three years; if the share price meets certain conditions, the company may accelerate the warrants' expiry.

- Use of Proceeds: The net proceeds will be allocated for working capital, advancing existing projects like Lethbridge 2, 3, and Hanna, as well as acquiring new projects, demonstrating the company's commitment to the renewable energy sector.

- Compliance and Regional Focus: The offering will rely on prospectus exemptions under national regulations and is expected to occur across multiple provinces, with all securities subject to a four-month statutory hold period to ensure compliance with Canadian securities laws.

See More

Market Dynamics and Corporate Mergers Overview

- Muted Market Start: The new trading week begins with the S&P 500 indicated flat while the tech-heavy Nasdaq shows slight gains, and WTI crude oil is trading around $76.50 per barrel, reflecting cautious market sentiment regarding economic outlook.

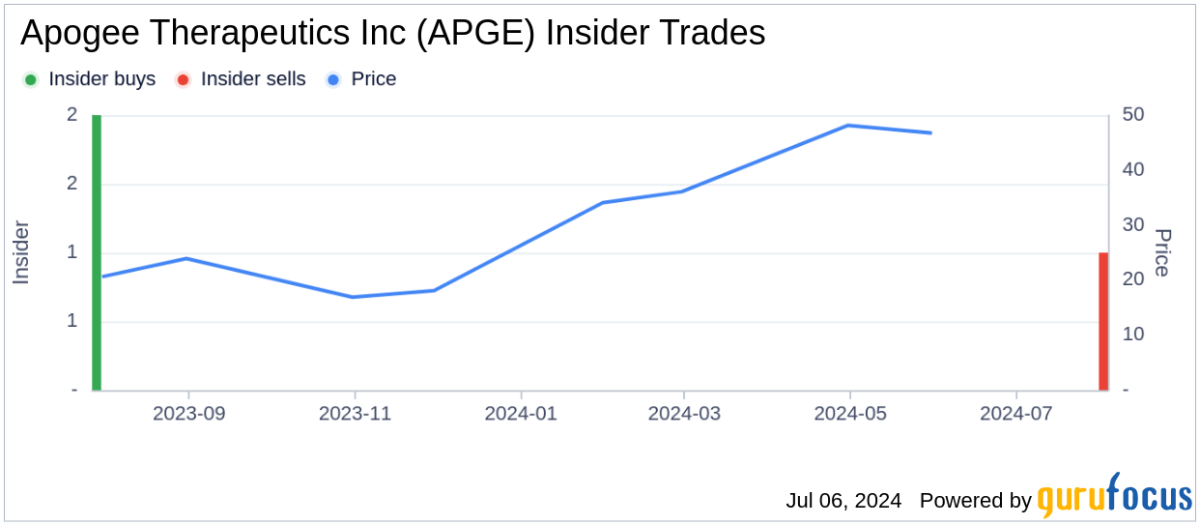

- Abbvie Acquires Apogee: Abbvie is acquiring Apogee Therapeutics for $10.9 billion to strengthen its immunology portfolio, particularly competing with Johnson & Johnson's Tremfya through its top drug Skyrizi, which is expected to enhance Abbvie's competitive edge in the biopharmaceutical market.

- CRH Acquires Arcosa: CRH is acquiring Arcosa for $8.5 billion, stating that the acquisition is highly complementary amid growing demand for energy and utility infrastructure, which is expected to further solidify CRH's position in the construction materials market.

- Estee Lauder Buy Rating Reinstated: Goldman Sachs has reinstated a buy rating for Estee Lauder with a price target of $100, as analysts believe the market is underestimating the company's growth momentum, especially after it walked away from merger talks with Spanish beauty peer Puig.

See More

Three Reliable Dividend Stocks to Hold

- Medical Device Leader: Medtronic boasts a 49-year dividend growth history with a current yield of 3.5%, and despite market fluctuations, its latest report indicates the highest annual revenue growth in a decade, reflecting effective restructuring efforts to enhance profitability.

- Real Estate Investment Trust: Realty Income offers a 5.2% dividend yield and has increased dividends for 31 consecutive years; as the largest net lease REIT, its portfolio spans North America and Europe, maintaining over 96% occupancy during economic downturns, showcasing its stability and reliability.

- Steel Industry Leader: Nucor, recognized as a Dividend King with over 50 consecutive annual hikes, currently has a low yield of 0.9%, yet its modern electric arc steel mills and strong employee relations enable it to perform well amid cyclical fluctuations, making it a solid long-term hold.

- Long-Term Investment Strategy: The author emphasizes a commitment to holding these quality stocks through market volatility, believing that Medtronic, Realty Income, and Nucor are proven successful companies that will continue to grow, making them worthy of attention for long-term investors.

See More

Anticipating a Deep Bear Market Ahead

- Healthcare Giant: Medtronic has maintained a dividend increase streak for 49 years, with a current yield of 3.5%, and despite market downturns, it recently reported its highest annual revenue growth in a decade, indicating a successful restructuring and potential for stable dividend growth even in a bear market.

- Real Estate Investment Trust: Realty Income offers a 5.2% dividend yield and has increased its dividend for 31 consecutive years; while not at historical highs, its absolute yield remains attractive, and its occupancy rate never dropped below 96% during the Great Recession, showcasing its reliability amid market fluctuations.

- Steel Industry Leader: Nucor, known for over 50 consecutive years of dividend increases, currently has a low yield of 0.9%, but has only reported one loss in the last four decades, demonstrating resilience in a cyclical industry, making it a potential quality pick for investors during a bear market.

- Long-Term Holding Strategy: The author intends to hold Medtronic, Realty Income, and Nucor through market volatility, believing that these companies' management capabilities and historical performance will enable continued growth in future market conditions, reflecting the value of long-term investing.

See More

Nucor Upgraded to Overweight by KeyBanc with $274 Target

- Rating Upgrade: KeyBanc upgraded Nucor from Sector Weight to Overweight with a $274 price target, reflecting confidence in the company's future performance despite a more than 10% drop in shares over the past six trading days.

- Earnings Guidance: Nucor guided for Q2 earnings between $4.50 and $4.60 per share, exceeding the FactSet analyst consensus of $4.21 and significantly higher than Q1's $3.23 and last year's Q2 EPS of $2.60, indicating ongoing improvement in profitability.

- Market Outlook: KeyBanc analyst expects Nucor's actual Q2 results to surpass company guidance, citing management's historical conservatism, while forecasting that steel prices will continue to rise at least through August, positively impacting the company's performance.

- Shipment Growth: Nucor's steel mill shipments are projected to increase nearly 10% year-over-year by 2026, suggesting that the company will benefit from strong steel pricing in the upcoming quarters, particularly in the seasonally strong fourth quarter.

See More

Latest Wall Street Rating Updates

- Citi Upgrade: Citi upgraded Macerich from Neutral to Buy, raising the target price from $24 to $28, indicating strong balance sheet strength that is expected to drive stock price appreciation.

- Citizens Initiation: Citizens initiated coverage on Bitdeer Holdings and Mara Holdings, stating that these bitcoin miners have significant potential to outperform the market by repurposing existing power capacity for high-performance computing.

- Mizuho's Biotech Outlook: Mizuho initiated coverage of Sol-Gel Technologies with an Outperform rating and a $285 price target, suggesting that the biotech firm is well-positioned for future growth in a competitive landscape.

- Goldman on Twilio: Goldman Sachs initiated coverage of Twilio with a Buy rating and a 12-month price target of $300, highlighting expected margin upside that reflects strong confidence in the company's financial prospects.

See More

NU E Power Announces Non-Brokered Private Placement of Up to $3 Million

- Funding Size: NU E Power Corp. intends to issue up to 20,000,000 units at a price of $0.15 per unit, aiming for total gross proceeds of up to $3 million to support its renewable energy projects.

- Subscription Terms: Each unit consists of one common share and half a warrant, with warrants allowing the purchase of additional shares at $0.25 for three years; if the share price meets certain conditions, the company may accelerate the warrants' expiry.

- Use of Proceeds: The net proceeds will be allocated for working capital, advancing existing projects like Lethbridge 2, 3, and Hanna, as well as acquiring new projects, demonstrating the company's commitment to the renewable energy sector.

- Compliance and Regional Focus: The offering will rely on prospectus exemptions under national regulations and is expected to occur across multiple provinces, with all securities subject to a four-month statutory hold period to ensure compliance with Canadian securities laws.

See More

Market Dynamics and Corporate Mergers Overview

- Muted Market Start: The new trading week begins with the S&P 500 indicated flat while the tech-heavy Nasdaq shows slight gains, and WTI crude oil is trading around $76.50 per barrel, reflecting cautious market sentiment regarding economic outlook.

- Abbvie Acquires Apogee: Abbvie is acquiring Apogee Therapeutics for $10.9 billion to strengthen its immunology portfolio, particularly competing with Johnson & Johnson's Tremfya through its top drug Skyrizi, which is expected to enhance Abbvie's competitive edge in the biopharmaceutical market.

- CRH Acquires Arcosa: CRH is acquiring Arcosa for $8.5 billion, stating that the acquisition is highly complementary amid growing demand for energy and utility infrastructure, which is expected to further solidify CRH's position in the construction materials market.

- Estee Lauder Buy Rating Reinstated: Goldman Sachs has reinstated a buy rating for Estee Lauder with a price target of $100, as analysts believe the market is underestimating the company's growth momentum, especially after it walked away from merger talks with Spanish beauty peer Puig.

See More