Nomura Holdings and Mizuho Financial Stocks Overbought with RSI Values of 86.1 and 84.8

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Jan 16 2026

0mins

Source: Benzinga

- Overbought Warning: As of January 16, 2026, Nomura Holdings has an RSI of 86.1, indicating its stock price has risen approximately 15% over the past month, with a 52-week high of $9.47, suggesting potential short-term pullback risks.

- Price Performance: Nomura closed at $9.39 on Thursday, up 1.4% from the previous trading day, but the high RSI value may signal caution for investors.

- Mizuho Financial Update: Mizuho Financial's RSI stands at 84.8, also reflecting a 15% increase over the past month, with a 52-week high of $8.59, indicating strong market performance but also potential overbought risks.

- Community Investment: On January 5, Mizuho announced $1 million in grants through the Mizuho USA Foundation to support young adults in gaining technology skills and career pathways, enhancing its brand image and community engagement.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy MFG?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on MFG

Wall Street analysts forecast MFG stock price to rise

1 Analyst Rating

1 Buy

0 Hold

0 Sell

Moderate Buy

Current: 9.590

Low

38.88

Averages

38.88

High

38.88

Current: 9.590

Low

38.88

Averages

38.88

High

38.88

About MFG

Mizuho Financial Group Inc is a Japan-based company mainly engaged in the banking, trust banking, securities, and other financial services. The Company operates through five business segments: Retail & Business Corporations Company (RBC), Corporate & Investment Banking Company (CIBC), Global Corporate & Investment Banking Company (GCIBC), Global Markets Company (GMC), and Asset Management Company (AMC). The CIBC segment operates for clients of large corporate corporations, financial corporations and public corporations in Japan. The GCIBC segment operates for clients of overseas-affiliated Japanese companies and non-Japanese companies. The GMC segment is engaged in investment business in interest rates, equity, among others. The AMC segment is engaged in the development and provision of products that meet the asset management needs of clients from individuals to institutional investors.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

S&P Global Spins Off Mobility Business into Standalone Company

- Spinoff Announcement: S&P Global is spinning off its Mobility business into a standalone entity named Mobility Global, which will begin trading on the NYSE under the ticker MBGL on July 1, allowing S&P to concentrate more resources on its core operations and enhance its competitive edge in the market.

- Shareholder Benefits: As part of the spinoff, shareholders will receive one share of Mobility Global common stock for each share of S&P Global common stock held as of the close on June 15, with the distribution expected to be effective on July 1, thereby increasing shareholder value and engagement.

- Financial Performance: The Mobility segment generated $454 million in revenue last quarter, reflecting an 8% year-over-year increase, and while it remains the smallest business unit, its operating profit grew by 9%, indicating potential for growth post-spinoff.

- Market Outlook: Analysts are bullish on the spinoff, with 93% rating S&P Global stock as a buy and projecting a 28% upside over the next 12 months, showcasing strong market confidence in S&P Global's future growth trajectory despite an 18% decline in stock price this year.

See More

S&P Global Spins Off Mobility Business

- Mobility Spin-Off: S&P Global will spin off its Mobility business into a standalone company, Mobility Global, effective July 1, marking a strategic shift that is expected to enhance resource allocation efficiency towards its core businesses.

- Shareholder Distribution: Shareholders will receive one share of Mobility Global common stock for each share of S&P Global common stock held as of the close on June 15, which is anticipated to enhance shareholder returns.

- Analyst Optimism: With 93% of analysts rating S&P Global stock as a buy and a median price target of $543, indicating a potential 28% upside over the next 12 months, this reflects strong market confidence in the company's growth prospects post-spin-off.

- Strong Financial Performance: Although the Mobility segment generated only $454 million in revenue last quarter, its operating profit grew by 9%, demonstrating S&P Global's robust performance in its core businesses and its ongoing ability to increase dividends, further solidifying its market leadership.

See More

Arm Holdings Stock Soars 210%, Price Target Raised to $360

- Stock Surge: Driven by rampant enthusiasm for AI stocks, Arm Holdings has seen its stock price soar over 210% since the beginning of 2026, with a 13% increase today, reflecting strong market demand and investor confidence.

- Price Target Increase: Mizuho raised its price target for Arm stock from $290 to $360, based on expectations of strong demand for dynamic random access memory (DRAM) that is anticipated to persist through 2027, further propelling growth in the semiconductor sector.

- Market Potential: Mizuho also highlighted that the total addressable market for high bandwidth memory is expanding, which provides a favorable outlook for Arm's future, indicating that the company will continue to strengthen its competitive position in the semiconductor industry.

- Valuation Considerations: Despite Mizuho's bullish outlook on Arm stock, its current price-to-earnings ratio stands at a steep 356 times, leading investors to consider investing in AI ETFs that include Arm stock to mitigate risk while gaining market exposure.

See More

Arm Stock Soars 210% in 2026 Amid AI Enthusiasm

- Stock Surge: Arm Holdings' stock has soared over 210% since the beginning of 2026, reflecting strong market enthusiasm for AI stocks and boosting overall semiconductor sector performance.

- Price Target Increase: Mizuho raised its price target on Arm stock from $290 to $360, based on expectations of strong demand for dynamic random access memory (DRAM), which is projected to grow through 2027.

- Valuation Warning: Despite Mizuho's bullish outlook, Arm's current price-to-earnings ratio stands at 356, leading investors to consider AI ETFs that include Arm stock to mitigate risk.

- Market Performance Comparison: With Arm's latest closing price at $302.71, the new target implies a 19% upside, and reaching $360 would set a new all-time high, indicating strong market confidence in its future growth.

See More

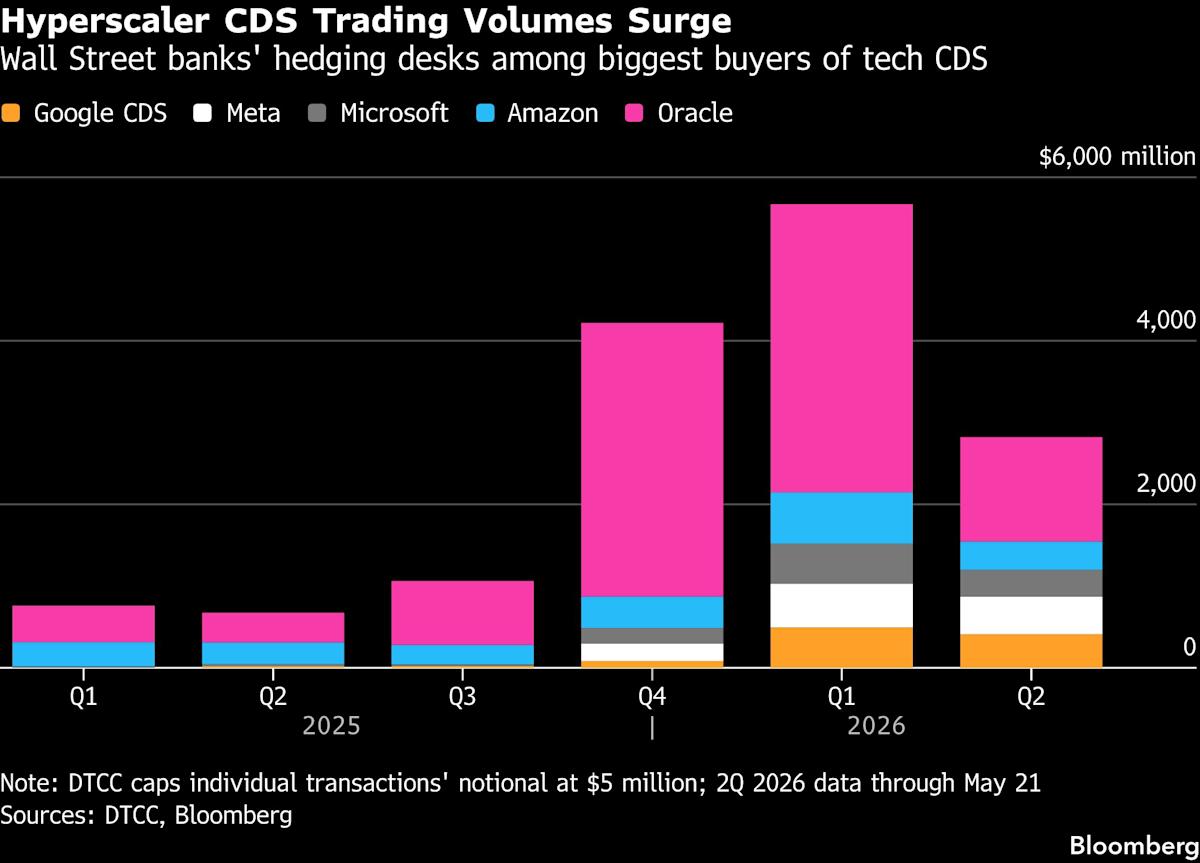

Wall Street Banks Increase Credit Derivative Trading with Hyperscalers

- Surge in Derivative Demand: As hyperscalers like Meta and Alphabet raise over $250 billion for AI, Wall Street banks are experiencing a significant increase in credit derivative trading volumes, driving market activity and rising trading costs.

- Hedging Needs Rise: Banks are purchasing credit derivatives to mitigate risk exposure to single companies, allowing them to increase lending and derivative trading without breaching credit limits, thereby enhancing overall profitability.

- Hedge Fund Profit Opportunities: With credit derivatives for hyperscalers priced unusually high relative to their credit ratings, Andrew Weinberg of Saba Capital Management notes that now is an optimal time to sell high-rated credit default swaps, anticipating substantial returns.

- Market Structure Shift: As borrowing demands from hyperscalers continue to rise, banks' credit valuation adjustment (CVA) desks are actively engaging in trades, leading to record growth in CDS trading volumes, reflecting a dual demand for confidence and risk management in the market.

See More

Pokémon Card Market Experiences Renaissance

- Price Surge: According to an index by Collectors, Pokémon card prices have skyrocketed by 1,350% since 2020, significantly outpacing traditional asset classes, attracting high-net-worth individuals and cryptocurrency investors, indicating robust market demand and investment potential.

- Market Hype: In 2023, The Pokémon Company continues to release new card sets, particularly special 30th-anniversary products, driving excitement and attracting a wave of young collectors and investors, creating a new collecting frenzy.

- Increased Speculation: Due to the scarcity of cards, many scalpers quickly buy up new releases and resell them at inflated prices, leading to market volatility and panic among consumers who feel compelled to purchase quickly to avoid missing out, further driving up prices.

- Collectors vs. Speculators: Despite the influx of speculators, many genuine collectors are still pursuing complete card sets, providing stability to the market and demonstrating the enduring appeal of collecting culture.

See More

S&P Global Spins Off Mobility Business into Standalone Company

- Spinoff Announcement: S&P Global is spinning off its Mobility business into a standalone entity named Mobility Global, which will begin trading on the NYSE under the ticker MBGL on July 1, allowing S&P to concentrate more resources on its core operations and enhance its competitive edge in the market.

- Shareholder Benefits: As part of the spinoff, shareholders will receive one share of Mobility Global common stock for each share of S&P Global common stock held as of the close on June 15, with the distribution expected to be effective on July 1, thereby increasing shareholder value and engagement.

- Financial Performance: The Mobility segment generated $454 million in revenue last quarter, reflecting an 8% year-over-year increase, and while it remains the smallest business unit, its operating profit grew by 9%, indicating potential for growth post-spinoff.

- Market Outlook: Analysts are bullish on the spinoff, with 93% rating S&P Global stock as a buy and projecting a 28% upside over the next 12 months, showcasing strong market confidence in S&P Global's future growth trajectory despite an 18% decline in stock price this year.

See More

S&P Global Spins Off Mobility Business

- Mobility Spin-Off: S&P Global will spin off its Mobility business into a standalone company, Mobility Global, effective July 1, marking a strategic shift that is expected to enhance resource allocation efficiency towards its core businesses.

- Shareholder Distribution: Shareholders will receive one share of Mobility Global common stock for each share of S&P Global common stock held as of the close on June 15, which is anticipated to enhance shareholder returns.

- Analyst Optimism: With 93% of analysts rating S&P Global stock as a buy and a median price target of $543, indicating a potential 28% upside over the next 12 months, this reflects strong market confidence in the company's growth prospects post-spin-off.

- Strong Financial Performance: Although the Mobility segment generated only $454 million in revenue last quarter, its operating profit grew by 9%, demonstrating S&P Global's robust performance in its core businesses and its ongoing ability to increase dividends, further solidifying its market leadership.

See More

Arm Holdings Stock Soars 210%, Price Target Raised to $360

- Stock Surge: Driven by rampant enthusiasm for AI stocks, Arm Holdings has seen its stock price soar over 210% since the beginning of 2026, with a 13% increase today, reflecting strong market demand and investor confidence.

- Price Target Increase: Mizuho raised its price target for Arm stock from $290 to $360, based on expectations of strong demand for dynamic random access memory (DRAM) that is anticipated to persist through 2027, further propelling growth in the semiconductor sector.

- Market Potential: Mizuho also highlighted that the total addressable market for high bandwidth memory is expanding, which provides a favorable outlook for Arm's future, indicating that the company will continue to strengthen its competitive position in the semiconductor industry.

- Valuation Considerations: Despite Mizuho's bullish outlook on Arm stock, its current price-to-earnings ratio stands at a steep 356 times, leading investors to consider investing in AI ETFs that include Arm stock to mitigate risk while gaining market exposure.

See More

Arm Stock Soars 210% in 2026 Amid AI Enthusiasm

- Stock Surge: Arm Holdings' stock has soared over 210% since the beginning of 2026, reflecting strong market enthusiasm for AI stocks and boosting overall semiconductor sector performance.

- Price Target Increase: Mizuho raised its price target on Arm stock from $290 to $360, based on expectations of strong demand for dynamic random access memory (DRAM), which is projected to grow through 2027.

- Valuation Warning: Despite Mizuho's bullish outlook, Arm's current price-to-earnings ratio stands at 356, leading investors to consider AI ETFs that include Arm stock to mitigate risk.

- Market Performance Comparison: With Arm's latest closing price at $302.71, the new target implies a 19% upside, and reaching $360 would set a new all-time high, indicating strong market confidence in its future growth.

See More

Wall Street Banks Increase Credit Derivative Trading with Hyperscalers

- Surge in Derivative Demand: As hyperscalers like Meta and Alphabet raise over $250 billion for AI, Wall Street banks are experiencing a significant increase in credit derivative trading volumes, driving market activity and rising trading costs.

- Hedging Needs Rise: Banks are purchasing credit derivatives to mitigate risk exposure to single companies, allowing them to increase lending and derivative trading without breaching credit limits, thereby enhancing overall profitability.

- Hedge Fund Profit Opportunities: With credit derivatives for hyperscalers priced unusually high relative to their credit ratings, Andrew Weinberg of Saba Capital Management notes that now is an optimal time to sell high-rated credit default swaps, anticipating substantial returns.

- Market Structure Shift: As borrowing demands from hyperscalers continue to rise, banks' credit valuation adjustment (CVA) desks are actively engaging in trades, leading to record growth in CDS trading volumes, reflecting a dual demand for confidence and risk management in the market.

See More

Pokémon Card Market Experiences Renaissance

- Price Surge: According to an index by Collectors, Pokémon card prices have skyrocketed by 1,350% since 2020, significantly outpacing traditional asset classes, attracting high-net-worth individuals and cryptocurrency investors, indicating robust market demand and investment potential.

- Market Hype: In 2023, The Pokémon Company continues to release new card sets, particularly special 30th-anniversary products, driving excitement and attracting a wave of young collectors and investors, creating a new collecting frenzy.

- Increased Speculation: Due to the scarcity of cards, many scalpers quickly buy up new releases and resell them at inflated prices, leading to market volatility and panic among consumers who feel compelled to purchase quickly to avoid missing out, further driving up prices.

- Collectors vs. Speculators: Despite the influx of speculators, many genuine collectors are still pursuing complete card sets, providing stability to the market and demonstrating the enduring appeal of collecting culture.

See More