National PTA Ends Partnership with Meta Amid Child Safety Concerns

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Feb 20 2026

0mins

Should l Buy META?

Source: Newsfilter

- Partnership Termination: The National PTA has announced it will not renew its partnership with Meta, reflecting significant concerns over the social media giant's ongoing legal challenges regarding child safety, particularly in lawsuits in California and New Mexico accusing Meta of misleading the public about app safety.

- Funding Discontinuation: PTA President Yvonne Johnson stated that the organization will not seek renewal funding from Meta for the PTA Connected initiative aimed at educating parents and teachers about digital safety tools, which could hinder access to essential resources and exacerbate public distrust in Meta.

- Public Scrutiny Intensifies: The decision comes amid increasing negative media coverage of Meta's impact on child safety, particularly following Zuckerberg's testimony, which has heightened public awareness of the potential harms of its products on children.

- Call to End Other Partnerships: The advocacy group ParentsSOS has urged the National PTA to terminate its partnerships with other tech companies, emphasizing concerns over design flaws that jeopardize children's mental health and safety, indicating a broader distrust of Big Tech in relation to child welfare.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy META?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on META

Wall Street analysts forecast META stock price to rise

44 Analyst Rating

37 Buy

6 Hold

1 Sell

Strong Buy

Current: 616.810

Low

655.15

Averages

824.71

High

1117

Current: 616.810

Low

655.15

Averages

824.71

High

1117

About META

Meta Platforms, Inc. is building human connections, powered by artificial intelligence and immersive technologies. The Company's products enable people to connect and share with friends and family through mobile devices, personal computers, virtual reality (VR) and mixed reality (MR) headsets, augmented reality (AR), and wearables. It also helps people discover and learn about what is going on in the world around them, enabling people to share their experiences, ideas, photos, videos, and other content with audiences ranging from their closest family members and friends to the public at large. The Company's segments include Family of Apps (FoA) and Reality Labs (RL). FoA segment includes Facebook, Instagram, Messenger, WhatsApp and Threads. RL segment includes its virtual, augmented, and mixed reality related consumer hardware, software and content. Its product offerings in VR include its Meta Quest devices, as well as software and content available through the Meta Horizon Store.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Meta's Profits and Cash Flow Soar

- Profit Surge: Meta's profits saw a significant increase in Q1 2026, indicating strong performance in the digital advertising market, which is expected to further drive stock price growth.

- Strong Cash Flow: The company's cash flow continues to rise, demonstrating a notable improvement in operational efficiency and profitability, providing ample funding for future investments and expansions.

- Positive Market Reaction: On May 3, 2026, Meta's stock price rose during trading, reflecting increased investor confidence in the company's financial health.

- Optimistic Strategic Outlook: With the growth in profits and cash flow, Meta is poised to increase investments in new technologies and market expansion, thereby solidifying its leadership position in the tech industry.

See More

Amazon Stock Surges 27.3% in April Amid Strong Earnings and AI Deal

- Stock Surge: Amazon's share price skyrocketed by 27.3% in April, significantly outperforming the S&P 500's 10.4% and the Nasdaq Composite's 15.3%, reflecting a strong return of investor interest in tech stocks amid a bullish market backdrop.

- Earnings Beat: The company reported Q1 earnings of $2.78 per share and revenue of $181.52 billion, both surpassing Wall Street estimates, showcasing robust performance in advertising and cloud services, which solidifies its market leadership.

- AI Partnership Opportunity: Amazon secured a deal with Meta Platforms, which will integrate “tens of millions of AWS Gravitron cores” into its computing portfolio, indicating a new revenue stream for Amazon and suggesting that custom AI chips could drive long-term growth for the company.

- Market Optimism: Despite ongoing geopolitical risks, Amazon has continued to rise approximately 3% in May, supported by strong job data and optimistic market sentiment regarding macroeconomic conditions, demonstrating sustained investor confidence in tech stocks.

See More

Meta Reports 33% Revenue Growth, AI Investments Pay Off

- Significant Revenue Growth: Meta's quarterly revenue rose by 33% year-over-year, with operating profit increasing by 30%, indicating substantial progress in ad performance and user engagement, which boosts investor confidence in future growth.

- Improved Ad Performance: Ad impressions increased by 19% and the average ad price rose by 12%, demonstrating not only Meta's efficiency in ad placements but also advertisers' recognition of the value, driving overall revenue growth.

- AI Technology Integration: By embedding AI across platforms like Facebook, Instagram, and WhatsApp, Meta has enhanced content recommendations and ad targeting, leading to increased user engagement and ad effectiveness, creating a positive feedback loop.

- Ecosystem Advantage: With 3.6 billion daily active users, Meta can test and refine its AI systems in real-time, and as the user base grows, the intelligence of the AI improves, providing the company with a unique edge in the AI race.

See More

Market Update: Stocks Set for Higher Open Amid Positive Economic Signals

- Positive Employment Report: The April employment report in the U.S. exceeded expectations, albeit not overly strong, leading to optimism for a higher open in the stock market, which may boost investor risk appetite and confidence in economic recovery.

- CoreWeave's Weak Forecast: CoreWeave's second-quarter revenue forecast fell short of expectations, causing its stock to drop over 7%, highlighting the competitive pressures in the AI compute market as operating expenses rise faster than revenue growth.

- Nike Downgrade: Wells Fargo downgraded Nike from buy to hold, reducing the price target from $55 to $45 due to increased competition in the athletic apparel market and slower-than-expected turnaround progress, which could impact future performance.

- Cloudflare Layoff Announcement: Cloudflare announced layoffs of 1,100 employees, or 20% of its workforce, and expects to incur significant charges as it transitions to an AI-first model, with implementation expected to be largely completed by the third quarter, potentially affecting operational efficiency in the short term.

See More

The Truth Behind AI-Induced Layoffs

- Layoff Surge: Year-to-date, employers have disclosed a total of 300,749 job cuts, down 50% from the same period in 2025, indicating the complexity and uncertainty of economic recovery.

- Tech Sector Impact: Major layoffs at companies like Oracle, which cut 30,000 jobs, and Block, which slashed 40% of its workforce, highlight the pain points in the tech industry amid the AI transition.

- Industry Shift and Hiring: Despite severe layoffs in tech, sectors such as healthcare, manufacturing, and infrastructure are actively hiring, suggesting an economic restructuring to adapt to new technologies.

- Future Outlook: Economists note that the impact of AI will unfold over a five-year horizon, with some jobs being eliminated but new opportunities created, necessitating attention to the upcoming jobs report.

See More

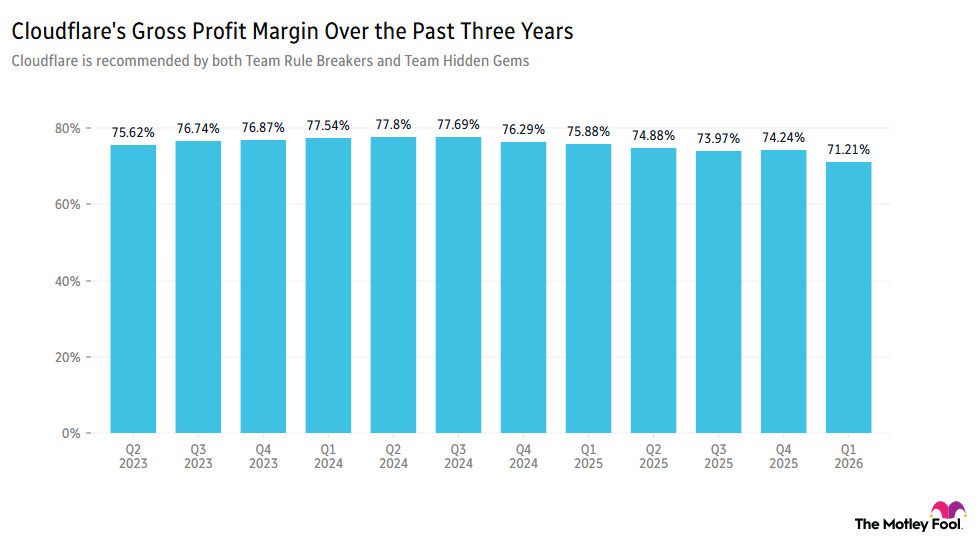

Cloudflare's AI Reform Triggers Stock Plunge

- Significant Stock Drop: Cloudflare's stock plummeted over 18% ahead of the market open as investors perceived the company's late entry into AI as a major concern, despite management's assertion of it being the 'biggest tailwind we've ever seen,' compounded by a 4.67% year-over-year decline in gross profit margins that undermined market confidence.

- Layoff Implementation: The company announced a layoff of 1,100 employees, representing 20% of its current workforce, with management stating in an internal email the need to 'be intentional in how we architect our company for the agentic AI era,' which could impact operational efficiency and employee morale.

- Strong Revenue Growth: Despite the drop in gross margins, Cloudflare reported a 34% year-over-year revenue increase and raised its outlook for fiscal year 2026 revenue and earnings, indicating that investments in AI may yield returns in the future.

- Outstanding Market Performance: Since November 2022, Cloudflare's stock has outperformed the S&P 500 by 285%, suggesting that despite current challenges, investors remain optimistic about the company's long-term potential.

See More

Meta's Profits and Cash Flow Soar

- Profit Surge: Meta's profits saw a significant increase in Q1 2026, indicating strong performance in the digital advertising market, which is expected to further drive stock price growth.

- Strong Cash Flow: The company's cash flow continues to rise, demonstrating a notable improvement in operational efficiency and profitability, providing ample funding for future investments and expansions.

- Positive Market Reaction: On May 3, 2026, Meta's stock price rose during trading, reflecting increased investor confidence in the company's financial health.

- Optimistic Strategic Outlook: With the growth in profits and cash flow, Meta is poised to increase investments in new technologies and market expansion, thereby solidifying its leadership position in the tech industry.

See More

Amazon Stock Surges 27.3% in April Amid Strong Earnings and AI Deal

- Stock Surge: Amazon's share price skyrocketed by 27.3% in April, significantly outperforming the S&P 500's 10.4% and the Nasdaq Composite's 15.3%, reflecting a strong return of investor interest in tech stocks amid a bullish market backdrop.

- Earnings Beat: The company reported Q1 earnings of $2.78 per share and revenue of $181.52 billion, both surpassing Wall Street estimates, showcasing robust performance in advertising and cloud services, which solidifies its market leadership.

- AI Partnership Opportunity: Amazon secured a deal with Meta Platforms, which will integrate “tens of millions of AWS Gravitron cores” into its computing portfolio, indicating a new revenue stream for Amazon and suggesting that custom AI chips could drive long-term growth for the company.

- Market Optimism: Despite ongoing geopolitical risks, Amazon has continued to rise approximately 3% in May, supported by strong job data and optimistic market sentiment regarding macroeconomic conditions, demonstrating sustained investor confidence in tech stocks.

See More

Meta Reports 33% Revenue Growth, AI Investments Pay Off

- Significant Revenue Growth: Meta's quarterly revenue rose by 33% year-over-year, with operating profit increasing by 30%, indicating substantial progress in ad performance and user engagement, which boosts investor confidence in future growth.

- Improved Ad Performance: Ad impressions increased by 19% and the average ad price rose by 12%, demonstrating not only Meta's efficiency in ad placements but also advertisers' recognition of the value, driving overall revenue growth.

- AI Technology Integration: By embedding AI across platforms like Facebook, Instagram, and WhatsApp, Meta has enhanced content recommendations and ad targeting, leading to increased user engagement and ad effectiveness, creating a positive feedback loop.

- Ecosystem Advantage: With 3.6 billion daily active users, Meta can test and refine its AI systems in real-time, and as the user base grows, the intelligence of the AI improves, providing the company with a unique edge in the AI race.

See More

Market Update: Stocks Set for Higher Open Amid Positive Economic Signals

- Positive Employment Report: The April employment report in the U.S. exceeded expectations, albeit not overly strong, leading to optimism for a higher open in the stock market, which may boost investor risk appetite and confidence in economic recovery.

- CoreWeave's Weak Forecast: CoreWeave's second-quarter revenue forecast fell short of expectations, causing its stock to drop over 7%, highlighting the competitive pressures in the AI compute market as operating expenses rise faster than revenue growth.

- Nike Downgrade: Wells Fargo downgraded Nike from buy to hold, reducing the price target from $55 to $45 due to increased competition in the athletic apparel market and slower-than-expected turnaround progress, which could impact future performance.

- Cloudflare Layoff Announcement: Cloudflare announced layoffs of 1,100 employees, or 20% of its workforce, and expects to incur significant charges as it transitions to an AI-first model, with implementation expected to be largely completed by the third quarter, potentially affecting operational efficiency in the short term.

See More

The Truth Behind AI-Induced Layoffs

- Layoff Surge: Year-to-date, employers have disclosed a total of 300,749 job cuts, down 50% from the same period in 2025, indicating the complexity and uncertainty of economic recovery.

- Tech Sector Impact: Major layoffs at companies like Oracle, which cut 30,000 jobs, and Block, which slashed 40% of its workforce, highlight the pain points in the tech industry amid the AI transition.

- Industry Shift and Hiring: Despite severe layoffs in tech, sectors such as healthcare, manufacturing, and infrastructure are actively hiring, suggesting an economic restructuring to adapt to new technologies.

- Future Outlook: Economists note that the impact of AI will unfold over a five-year horizon, with some jobs being eliminated but new opportunities created, necessitating attention to the upcoming jobs report.

See More

Cloudflare's AI Reform Triggers Stock Plunge

- Significant Stock Drop: Cloudflare's stock plummeted over 18% ahead of the market open as investors perceived the company's late entry into AI as a major concern, despite management's assertion of it being the 'biggest tailwind we've ever seen,' compounded by a 4.67% year-over-year decline in gross profit margins that undermined market confidence.

- Layoff Implementation: The company announced a layoff of 1,100 employees, representing 20% of its current workforce, with management stating in an internal email the need to 'be intentional in how we architect our company for the agentic AI era,' which could impact operational efficiency and employee morale.

- Strong Revenue Growth: Despite the drop in gross margins, Cloudflare reported a 34% year-over-year revenue increase and raised its outlook for fiscal year 2026 revenue and earnings, indicating that investments in AI may yield returns in the future.

- Outstanding Market Performance: Since November 2022, Cloudflare's stock has outperformed the S&P 500 by 285%, suggesting that despite current challenges, investors remain optimistic about the company's long-term potential.

See More