Kimbell Royalty Partners Set to Announce Q4 Earnings

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Feb 25 2026

0mins

Should l Buy KRP?

Source: seekingalpha

- Earnings Announcement Schedule: Kimbell Royalty Partners is set to announce its Q4 earnings on February 26 before market open, with consensus EPS estimate at $0.14 and revenue expected to reach $77.09 million, reflecting a 15.5% year-over-year growth.

- Earnings Forecast Changes: Over the past three months, EPS estimates have seen one upward revision and one downward adjustment, while revenue estimates have experienced no upward revisions and three downward adjustments, indicating market caution regarding the company's future performance.

- Credit Facility Extension: Kimbell Royalty Partners has extended its $625 million credit facility to 2030, a move that not only enhances the company's liquidity but also provides greater financial flexibility for future investments and operations.

- Dividend Stability: Despite market challenges, Kimbell Royalty Partners' dividends are expected to remain relatively stable through 2026, reflecting the company's ongoing commitment to shareholder returns and financial discipline.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy KRP?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

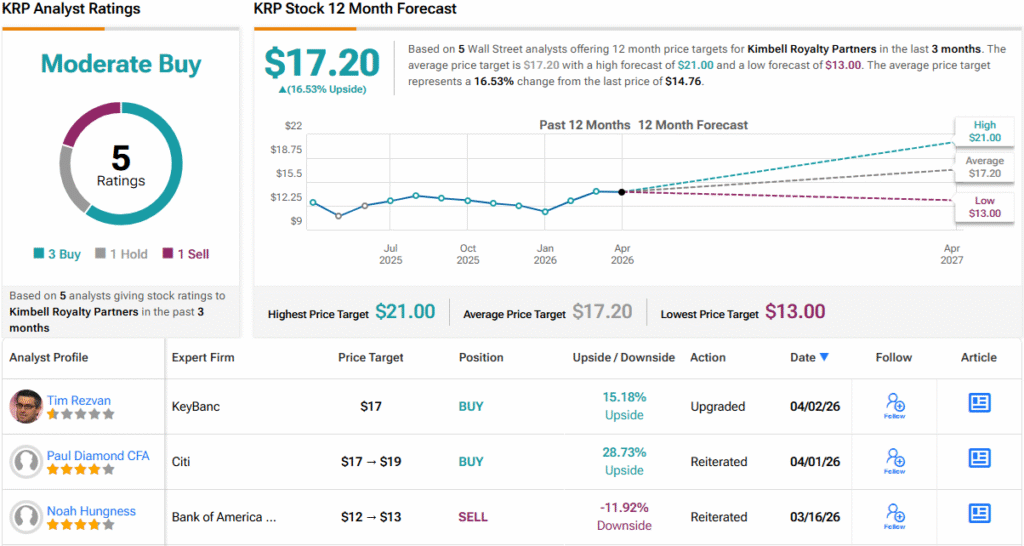

Analyst Views on KRP

Wall Street analysts forecast KRP stock price to rise

6 Analyst Rating

2 Buy

3 Hold

1 Sell

Hold

Current: 14.080

Low

12.00

Averages

17.00

High

24.00

Current: 14.080

Low

12.00

Averages

17.00

High

24.00

About KRP

Kimbell Royalty Partners, LP is an oil and gas mineral and royalty company. It owns mineral and royalty interests in over 17 million gross acres in 28 states and in onshore basins in the continental United States, including ownership in more than 130,000 gross wells with over 51,000 wells in the Permian Basin. Its properties include the Permian Basin, Mid-Continent, Appalachian, Eagle Ford, Bakken, Terryville/Cotton Valley/Haynesville, and DJ Basin/Rockies/Niobrara. The Permian Basin extends from southeastern New Mexico into West Texas. The Mid-Continent is an area containing fields in Arkansas, Kansas, Louisiana, New Mexico, Oklahoma, Nebraska and Texas and including the Granite Wash, Cleveland, and Mississippi Lime formations. The Appalachian Basin covers most of Pennsylvania, eastern Ohio, West Virginia, western Maryland, eastern Kentucky, central Tennessee, Western Virginia, northwestern Georgia, and northern Alabama. The Eagle Ford shale formation stretches across south Texas.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

High-Yield Dividend Stocks Attract Investor Attention

- Kimbell Royalty Partners Performance: Kimbell Royalty Partners reported a run-rate daily production of 25,627 Boe/d in Q4 2025, generating $76 million in oil, natural gas, and liquids revenue, with total revenue of $82.5 million reflecting over 23% year-over-year growth, exceeding forecasts by $5.36 million, indicating strong performance in the energy sector.

- Cash Distribution and Dividends: By the end of Q4 2025, Kimbell had $46.84 million available for distribution, supporting a dividend of $0.37 per share, which annualizes to $1.48, yielding 10%, providing investors with a reliable income stream amidst market volatility.

- One Liberty Properties Strategy: One Liberty Properties acquired 13 industrial properties for $188 million in 2025, reflecting its strategic shift towards an industrial-heavy portfolio, which is expected to drive earnings growth and enhance market competitiveness.

- Dividends and Market Expectations: One Liberty's quarterly dividend is set at $0.45 per share, annualizing to $1.80, with a forward yield of 8.2%, and combined with analysts' buy ratings, suggests a potential total return of 33% over the next year.

See More

Kimbell Royalty Partners Upgraded to Overweight by KeyBanc

- Stock Price Surge: Kimbell Royalty Partners (KRP) rose 3.7% in Thursday's trading, reflecting market optimism following KeyBanc's upgrade from Sector Weight to Overweight with a $17 price target, indicating strong future performance expectations.

- Increased Yield Forecast: KeyBanc analyst Tim Rezvan now projects a near-term yield of 13.5% for KRP units, significantly up from the previous 10.5%, driven by revised oil and gas price forecasts amid ongoing Middle East disruptions affecting global crude and refined products.

- Acquisition Strategy Shift: KRP management expressed equal interest in assets in the Eagle Ford, Mid-Con, and Haynesville regions, demonstrating a pragmatic approach to seeking deals outside the competitive Permian Basin, which may lead to higher M&A accretion.

- Market Environment Impact: Rezvan noted that the oil price rally should alleviate concerns about declining activity in the Lower 48, while a stronger oil price outlook may attract sellers for bolt-on acquisitions, further strengthening KRP's market position.

See More

Kimbell Royalty Partners to Release Q1 2026 Financial Results

- Earnings Release Schedule: Kimbell Royalty Partners is set to announce its Q1 2026 financial results on May 7, 2026, before market open, alongside its quarterly distribution, reflecting the company's commitment to transparency and shareholder returns.

- Conference Call Details: The company will host a conference call at 10:00 a.m. Central (11:00 a.m. Eastern) on the same day, providing a live webcast to enhance investor communication and market engagement.

- Replay Availability: A replay of the conference call will be accessible until May 14, allowing investors who missed the live event to dial 201-612-7415 with conference ID 13759315# to catch up on critical information.

- Company Overview: Kimbell Royalty Partners holds mineral and royalty interests in over 133,000 gross wells across 28 states, covering more than 17 million gross acres, showcasing its significant presence and influence in the oil and gas sector.

See More

Kimbell Royalty Partners to Release Q1 2026 Financial Results

- Earnings Release Schedule: Kimbell Royalty Partners is set to announce its Q1 2026 financial results on May 7, 2026, before market opening, alongside its quarterly distribution, which is expected to positively influence investor confidence.

- Conference Call Details: The company will host a conference call at 10:00 a.m. Central (11:00 a.m. Eastern) on the same day, with investors able to join by dialing 201-389-0869, and a replay available until May 14, enhancing information transparency.

- Webcast Access: Investors can participate in the live webcast via Kimbell's Investor Relations website, requiring a login at least 10 minutes in advance to ensure smooth access, thereby improving engagement with stakeholders.

- Company Background: Kimbell Royalty Partners holds mineral and royalty interests in over 133,000 gross wells across 28 states, covering more than 17 million gross acres, underscoring its significant position and market influence in the oil and gas sector.

See More

Analysis of Investment Opportunities in Energy Infrastructure

- Energy Transition Potential: Energy Transfer (ET) has a market cap of $65 billion with a quarterly distribution of $0.335 per unit, yielding approximately 7.2%; despite missing EPS estimates, its revenue grew 29.6% year-over-year, indicating strong potential in the energy transition.

- Stable Distribution Growth: MPLX (MPLX) offers a quarterly distribution of $1.0765 per unit, yielding around 7.4%, with a 13.78% increase in net income for 2025 and a consistent 12.5% distribution hike for two consecutive years, showcasing its stable cash flow and distribution policy.

- No Capital Expenditure Risk: Kimbell Royalty Partners (KRP) leads with a quarterly distribution of $0.37 per unit and a yield of 10.7%, benefiting from a royalty model that eliminates capital expenditure risk, while its net income surged 713.27% in 2025, demonstrating strong profitability.

- Market Competitive Advantage: All three MLPs offer yields significantly above market averages, with Energy Transfer enhancing scale through data center growth strategies, MPLX standing out for consistent execution and clear distribution growth trajectory, and Kimbell maintaining a unique position with high yields and tax advantages.

See More

Analysis of Three Key MLP Energy Partnerships

- Energy Transition Potential: Energy Transfer, with a market cap of $65 billion, offers a quarterly distribution of $0.335 per unit, implying a yield of approximately 7.2%; despite missing EPS estimates, its natural gas supply agreements and expansion plans indicate strong growth potential.

- Stable Distribution Growth: MPLX's quarterly distribution stands at $1.0765 per unit, yielding around 7.4%, and has raised its distribution by 12.5% for the second consecutive year, with a 13.78% increase in full-year net income, showcasing robust capital return performance.

- No Capital Expenditure Risk: Kimbell Royalty Partners provides a quarterly distribution of $0.37 per unit, yielding 10.7%, and its unique royalty model entirely eliminates capital expenditure risk, with a staggering 713.27% surge in net income for 2025, reflecting strong profitability.

- Market Appeal: All three MLPs offer yields exceeding market averages, with Energy Transfer leveraging scale and data center growth potential, MPLX excelling in consistent execution and distribution growth, while Kimbell stands out with the highest yield and tax-advantaged distribution structure.

See More

High-Yield Dividend Stocks Attract Investor Attention

- Kimbell Royalty Partners Performance: Kimbell Royalty Partners reported a run-rate daily production of 25,627 Boe/d in Q4 2025, generating $76 million in oil, natural gas, and liquids revenue, with total revenue of $82.5 million reflecting over 23% year-over-year growth, exceeding forecasts by $5.36 million, indicating strong performance in the energy sector.

- Cash Distribution and Dividends: By the end of Q4 2025, Kimbell had $46.84 million available for distribution, supporting a dividend of $0.37 per share, which annualizes to $1.48, yielding 10%, providing investors with a reliable income stream amidst market volatility.

- One Liberty Properties Strategy: One Liberty Properties acquired 13 industrial properties for $188 million in 2025, reflecting its strategic shift towards an industrial-heavy portfolio, which is expected to drive earnings growth and enhance market competitiveness.

- Dividends and Market Expectations: One Liberty's quarterly dividend is set at $0.45 per share, annualizing to $1.80, with a forward yield of 8.2%, and combined with analysts' buy ratings, suggests a potential total return of 33% over the next year.

See More

Kimbell Royalty Partners Upgraded to Overweight by KeyBanc

- Stock Price Surge: Kimbell Royalty Partners (KRP) rose 3.7% in Thursday's trading, reflecting market optimism following KeyBanc's upgrade from Sector Weight to Overweight with a $17 price target, indicating strong future performance expectations.

- Increased Yield Forecast: KeyBanc analyst Tim Rezvan now projects a near-term yield of 13.5% for KRP units, significantly up from the previous 10.5%, driven by revised oil and gas price forecasts amid ongoing Middle East disruptions affecting global crude and refined products.

- Acquisition Strategy Shift: KRP management expressed equal interest in assets in the Eagle Ford, Mid-Con, and Haynesville regions, demonstrating a pragmatic approach to seeking deals outside the competitive Permian Basin, which may lead to higher M&A accretion.

- Market Environment Impact: Rezvan noted that the oil price rally should alleviate concerns about declining activity in the Lower 48, while a stronger oil price outlook may attract sellers for bolt-on acquisitions, further strengthening KRP's market position.

See More

Kimbell Royalty Partners to Release Q1 2026 Financial Results

- Earnings Release Schedule: Kimbell Royalty Partners is set to announce its Q1 2026 financial results on May 7, 2026, before market open, alongside its quarterly distribution, reflecting the company's commitment to transparency and shareholder returns.

- Conference Call Details: The company will host a conference call at 10:00 a.m. Central (11:00 a.m. Eastern) on the same day, providing a live webcast to enhance investor communication and market engagement.

- Replay Availability: A replay of the conference call will be accessible until May 14, allowing investors who missed the live event to dial 201-612-7415 with conference ID 13759315# to catch up on critical information.

- Company Overview: Kimbell Royalty Partners holds mineral and royalty interests in over 133,000 gross wells across 28 states, covering more than 17 million gross acres, showcasing its significant presence and influence in the oil and gas sector.

See More

Kimbell Royalty Partners to Release Q1 2026 Financial Results

- Earnings Release Schedule: Kimbell Royalty Partners is set to announce its Q1 2026 financial results on May 7, 2026, before market opening, alongside its quarterly distribution, which is expected to positively influence investor confidence.

- Conference Call Details: The company will host a conference call at 10:00 a.m. Central (11:00 a.m. Eastern) on the same day, with investors able to join by dialing 201-389-0869, and a replay available until May 14, enhancing information transparency.

- Webcast Access: Investors can participate in the live webcast via Kimbell's Investor Relations website, requiring a login at least 10 minutes in advance to ensure smooth access, thereby improving engagement with stakeholders.

- Company Background: Kimbell Royalty Partners holds mineral and royalty interests in over 133,000 gross wells across 28 states, covering more than 17 million gross acres, underscoring its significant position and market influence in the oil and gas sector.

See More

Analysis of Investment Opportunities in Energy Infrastructure

- Energy Transition Potential: Energy Transfer (ET) has a market cap of $65 billion with a quarterly distribution of $0.335 per unit, yielding approximately 7.2%; despite missing EPS estimates, its revenue grew 29.6% year-over-year, indicating strong potential in the energy transition.

- Stable Distribution Growth: MPLX (MPLX) offers a quarterly distribution of $1.0765 per unit, yielding around 7.4%, with a 13.78% increase in net income for 2025 and a consistent 12.5% distribution hike for two consecutive years, showcasing its stable cash flow and distribution policy.

- No Capital Expenditure Risk: Kimbell Royalty Partners (KRP) leads with a quarterly distribution of $0.37 per unit and a yield of 10.7%, benefiting from a royalty model that eliminates capital expenditure risk, while its net income surged 713.27% in 2025, demonstrating strong profitability.

- Market Competitive Advantage: All three MLPs offer yields significantly above market averages, with Energy Transfer enhancing scale through data center growth strategies, MPLX standing out for consistent execution and clear distribution growth trajectory, and Kimbell maintaining a unique position with high yields and tax advantages.

See More

Analysis of Three Key MLP Energy Partnerships

- Energy Transition Potential: Energy Transfer, with a market cap of $65 billion, offers a quarterly distribution of $0.335 per unit, implying a yield of approximately 7.2%; despite missing EPS estimates, its natural gas supply agreements and expansion plans indicate strong growth potential.

- Stable Distribution Growth: MPLX's quarterly distribution stands at $1.0765 per unit, yielding around 7.4%, and has raised its distribution by 12.5% for the second consecutive year, with a 13.78% increase in full-year net income, showcasing robust capital return performance.

- No Capital Expenditure Risk: Kimbell Royalty Partners provides a quarterly distribution of $0.37 per unit, yielding 10.7%, and its unique royalty model entirely eliminates capital expenditure risk, with a staggering 713.27% surge in net income for 2025, reflecting strong profitability.

- Market Appeal: All three MLPs offer yields exceeding market averages, with Energy Transfer leveraging scale and data center growth potential, MPLX excelling in consistent execution and distribution growth, while Kimbell stands out with the highest yield and tax-advantaged distribution structure.

See More