Hedge Fund Favorites Outperform the Market, with Tesla Joining the Ranks for the First Time in Three Years.

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Aug 21 2025

0mins

Should l Buy GOOGL?

Source: MarketWatch

Hedge Fund Performance: Hedge fund favorite stocks have outperformed the broader market in 2023, with a notable return of 15% compared to 11% for the S&P 500.

Tesla's Comeback: For the first time since 2022, Tesla has made it onto the list of favored stocks by hedge funds, according to an analysis by Goldman Sachs.

Goldman Sachs Analysis: The findings are based on 13-F filings submitted to the Securities and Exchange Commission, highlighting the performance of what Goldman refers to as its “hedge fund VIP” list.

ETF Wrapper: The "hedge fund VIP" list is available through an ETF called GVIP, which tracks these high-performing stocks.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy GOOGL?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on GOOGL

Wall Street analysts forecast GOOGL stock price to rise

33 Analyst Rating

26 Buy

7 Hold

0 Sell

Strong Buy

Current: 302.060

Low

305.00

Averages

374.25

High

400.00

Current: 302.060

Low

305.00

Averages

374.25

High

400.00

About GOOGL

Alphabet Inc. is a holding company. The Company's segments include Google Services, Google Cloud, and Other Bets. The Google Services segment includes products and services such as ads, Android, Chrome, devices, Google Maps, Google Play, Search, and YouTube. The Google Cloud segment includes infrastructure and platform services, collaboration tools, and other services for enterprise customers. Its Other Bets segment is engaged in the sale of healthcare-related services and Internet services. Its Google Cloud provides enterprise-ready cloud services, including Google Cloud Platform and Google Workspace. Google Cloud Platform provides access to solutions such as artificial intelligence (AI) offerings, including its AI infrastructure, Vertex AI platform, and Gemini for Google Cloud; cybersecurity, and data and analytics. Google Workspace includes cloud-based communication and collaboration tools for enterprises, such as Calendar, Gmail, Docs, Drive, and Meet.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

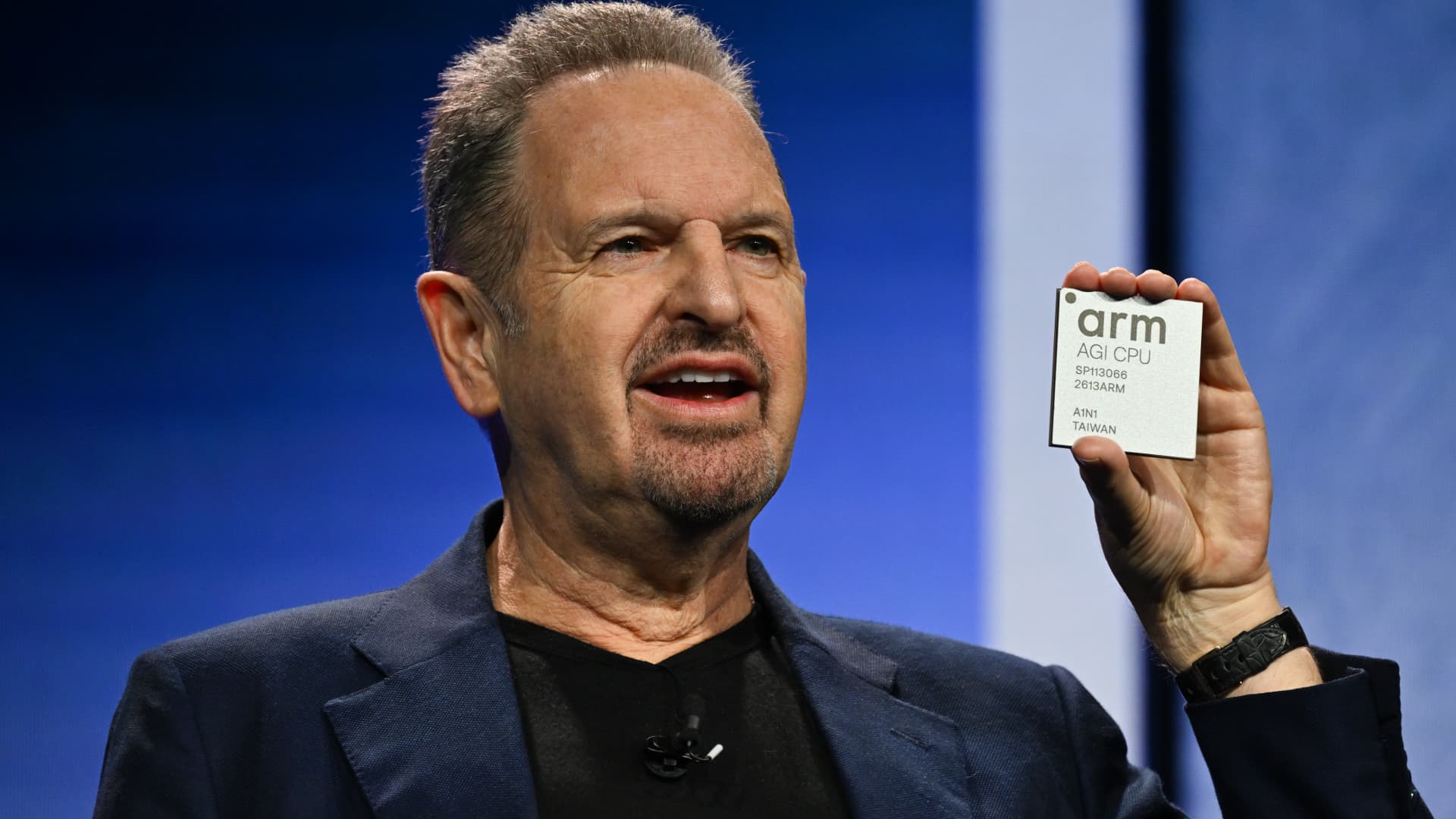

Arm Holdings Launches In-House CPU Amid AI Boom, Shares Surge 13%

- In-House Chip Launch: Arm Holdings unveiled its first in-house central processing unit, the AGI CPU, designed to meet the inference needs of AI data centers, with an expected incremental revenue of approximately $1 billion through fiscal year 2028, potentially growing to $15 billion by fiscal year 2031, indicating strong market potential.

- Rating Upgrade: Raymond James upgraded Arm's rating from market perform to outperform, setting a price target of $166, suggesting a 23% upside, reflecting confidence in the company's new business model that includes a fabless semiconductor element.

- Surging Market Demand: With hyperscalers like Alphabet, Microsoft, Meta, and Amazon committing nearly $700 billion in capital expenditures, Arm's AGI CPU is positioned to meet the booming demand for AI hardware, further solidifying its market position.

- Industry-Leading Performance: The AGI CPU claims to deliver twice the performance of x86 CPUs in high-end configurations, featuring superior bandwidth and execution thread capabilities, attracting interest from companies like Meta, showcasing its broad applicability in AI applications.

See More

Arm's New Chip Expected to Generate $15 Billion in Annual Revenue by 2031

- Chip Launch: Arm unveiled its first internal AGI CPU chip in San Francisco, specifically designed for AI inference in data centers, with an expected annual revenue of $15 billion by 2031, showcasing the company's strong competitive position in the rapidly growing AI market.

- Customer Base Expansion: Major clients such as Meta, OpenAI, Cloudflare, and SAP are among the first users of the new chip, indicating strong market demand for Arm's latest product and reflecting the company's strategic positioning in the AI sector.

- Significant Revenue Projections: Arm anticipates total annual revenue reaching $25 billion by 2031, a sixfold increase from $4 billion in 2025, with CEO Rene Haas stating that this forecast will drive earnings per share to $9, significantly boosting investor confidence.

- Positive Market Reaction: Arm's stock rose approximately 13.2% in premarket trading, with analysts calling the announcement the most significant shift in the company's history, projecting $7.5 billion in incremental gross profit and $5 billion in operating profit, further solidifying its market position.

See More

Arm's New Chip Expected to Generate $15 Billion Revenue by 2031

- Chip Launch: Arm unveiled its first in-house chip, the AGI CPU, in San Francisco, projecting $15 billion in revenue by 2031, showcasing the company's strong potential in the AI inference market and solidifying its position in the semiconductor industry.

- Revenue Expectations Surge: Arm anticipates total annual revenue of $25 billion, a sixfold increase from $4 billion in 2025, demonstrating the company's competitiveness and profitability in the rapidly growing AI market.

- Positive Market Reaction: Following the chip announcement, Arm's stock rose approximately 13.2% in premarket trading, reflecting investor optimism about the company's future growth prospects, despite a 1.5% decline on Tuesday.

- Expanded Customer Base: Meta is the first official customer for Arm's new chip, with Arm's cloud AI head noting a $1 trillion market size, indicating that the chip will attract more customers opting for its solutions over in-house alternatives, thereby expanding the company's market share and profit opportunities.

See More

Alphabet Shares Near Bear Market Threshold After Significant Decline

- Significant Stock Drop: Alphabet (GOOG) shares fell over 3% on Tuesday to around $290, marking the lowest close since November and indicating growing market concerns about its future performance.

- Near Bear Market: The stock is now approximately 17% below its February peak of $350, nearing the 20% threshold that typically defines a bear market, reflecting a notable shift in investor sentiment.

- Market Environment Impact: Amid broader weakness in U.S. equities, rising bond yields and escalating geopolitical tensions have led investors to reassess high-growth tech stocks, putting additional pressure on Alphabet.

- Increased Regulatory Scrutiny: With rising concerns over the costs associated with scaling artificial intelligence infrastructure and ongoing regulatory scrutiny, Alphabet faces heightened uncertainty, further impacting investor confidence.

See More

Billionaire Ackman Bets Big on AI Stocks

- Portfolio Focus: Billionaire Bill Ackman has concentrated 55% of his $15.5 billion portfolio in four AI stocks through Pershing Square Capital Management, reflecting strong confidence in the artificial intelligence sector.

- Stock Allocation: Ackman's investments include Uber (15.9%), Amazon (14.28%), Alphabet (13.83%), and Meta (11.37%), all of which possess sustainable competitive advantages, indicating his focus on AI applications.

- Significant Sales Growth: Amazon Web Services (AWS) and Google Cloud achieved sales growth of 24% and 48% respectively in the fourth quarter, demonstrating the positive impact of AI integration on their businesses and further solidifying their market leadership.

- Attractive Valuations: Ackman sees value in Uber's forward P/E ratio of 17 and Amazon's projected cash flow P/E ratio of just 9.6, indicating that these stocks offer high investment potential in the current market environment.

See More

Billionaire Ackman Bets Big on AI Investments

- Portfolio Focus: Billionaire Bill Ackman has allocated over 55% of his $15.5 billion portfolio, approximately $8.6 billion, to AI application companies, reflecting strong confidence in the AI sector and potentially driving long-term growth for his investments.

- Cloud Service Growth: Amazon Web Services (AWS) achieved a 24% sales growth in Q4, while Google Cloud's revenue surged 48% year-over-year, indicating that AI integration has significantly enhanced their competitive edge in the cloud services market, solidifying their leadership positions.

- Valuation Advantage: Uber's forward P/E ratio stands at 17, while Amazon's projected cash flow P/E is only 9.6, highlighting the relative undervaluation of these companies in the current market, which may attract more investor interest and drive stock price increases.

- Advertising Pricing Power: Meta Platforms attracted an average of 3.58 billion daily users to its apps, far exceeding other social media platforms, which grants it exceptional pricing power in advertising, likely boosting its revenue and market share further.

See More

Arm Holdings Launches In-House CPU Amid AI Boom, Shares Surge 13%

- In-House Chip Launch: Arm Holdings unveiled its first in-house central processing unit, the AGI CPU, designed to meet the inference needs of AI data centers, with an expected incremental revenue of approximately $1 billion through fiscal year 2028, potentially growing to $15 billion by fiscal year 2031, indicating strong market potential.

- Rating Upgrade: Raymond James upgraded Arm's rating from market perform to outperform, setting a price target of $166, suggesting a 23% upside, reflecting confidence in the company's new business model that includes a fabless semiconductor element.

- Surging Market Demand: With hyperscalers like Alphabet, Microsoft, Meta, and Amazon committing nearly $700 billion in capital expenditures, Arm's AGI CPU is positioned to meet the booming demand for AI hardware, further solidifying its market position.

- Industry-Leading Performance: The AGI CPU claims to deliver twice the performance of x86 CPUs in high-end configurations, featuring superior bandwidth and execution thread capabilities, attracting interest from companies like Meta, showcasing its broad applicability in AI applications.

See More

Arm's New Chip Expected to Generate $15 Billion in Annual Revenue by 2031

- Chip Launch: Arm unveiled its first internal AGI CPU chip in San Francisco, specifically designed for AI inference in data centers, with an expected annual revenue of $15 billion by 2031, showcasing the company's strong competitive position in the rapidly growing AI market.

- Customer Base Expansion: Major clients such as Meta, OpenAI, Cloudflare, and SAP are among the first users of the new chip, indicating strong market demand for Arm's latest product and reflecting the company's strategic positioning in the AI sector.

- Significant Revenue Projections: Arm anticipates total annual revenue reaching $25 billion by 2031, a sixfold increase from $4 billion in 2025, with CEO Rene Haas stating that this forecast will drive earnings per share to $9, significantly boosting investor confidence.

- Positive Market Reaction: Arm's stock rose approximately 13.2% in premarket trading, with analysts calling the announcement the most significant shift in the company's history, projecting $7.5 billion in incremental gross profit and $5 billion in operating profit, further solidifying its market position.

See More

Arm's New Chip Expected to Generate $15 Billion Revenue by 2031

- Chip Launch: Arm unveiled its first in-house chip, the AGI CPU, in San Francisco, projecting $15 billion in revenue by 2031, showcasing the company's strong potential in the AI inference market and solidifying its position in the semiconductor industry.

- Revenue Expectations Surge: Arm anticipates total annual revenue of $25 billion, a sixfold increase from $4 billion in 2025, demonstrating the company's competitiveness and profitability in the rapidly growing AI market.

- Positive Market Reaction: Following the chip announcement, Arm's stock rose approximately 13.2% in premarket trading, reflecting investor optimism about the company's future growth prospects, despite a 1.5% decline on Tuesday.

- Expanded Customer Base: Meta is the first official customer for Arm's new chip, with Arm's cloud AI head noting a $1 trillion market size, indicating that the chip will attract more customers opting for its solutions over in-house alternatives, thereby expanding the company's market share and profit opportunities.

See More

Alphabet Shares Near Bear Market Threshold After Significant Decline

- Significant Stock Drop: Alphabet (GOOG) shares fell over 3% on Tuesday to around $290, marking the lowest close since November and indicating growing market concerns about its future performance.

- Near Bear Market: The stock is now approximately 17% below its February peak of $350, nearing the 20% threshold that typically defines a bear market, reflecting a notable shift in investor sentiment.

- Market Environment Impact: Amid broader weakness in U.S. equities, rising bond yields and escalating geopolitical tensions have led investors to reassess high-growth tech stocks, putting additional pressure on Alphabet.

- Increased Regulatory Scrutiny: With rising concerns over the costs associated with scaling artificial intelligence infrastructure and ongoing regulatory scrutiny, Alphabet faces heightened uncertainty, further impacting investor confidence.

See More

Billionaire Ackman Bets Big on AI Stocks

- Portfolio Focus: Billionaire Bill Ackman has concentrated 55% of his $15.5 billion portfolio in four AI stocks through Pershing Square Capital Management, reflecting strong confidence in the artificial intelligence sector.

- Stock Allocation: Ackman's investments include Uber (15.9%), Amazon (14.28%), Alphabet (13.83%), and Meta (11.37%), all of which possess sustainable competitive advantages, indicating his focus on AI applications.

- Significant Sales Growth: Amazon Web Services (AWS) and Google Cloud achieved sales growth of 24% and 48% respectively in the fourth quarter, demonstrating the positive impact of AI integration on their businesses and further solidifying their market leadership.

- Attractive Valuations: Ackman sees value in Uber's forward P/E ratio of 17 and Amazon's projected cash flow P/E ratio of just 9.6, indicating that these stocks offer high investment potential in the current market environment.

See More

Billionaire Ackman Bets Big on AI Investments

- Portfolio Focus: Billionaire Bill Ackman has allocated over 55% of his $15.5 billion portfolio, approximately $8.6 billion, to AI application companies, reflecting strong confidence in the AI sector and potentially driving long-term growth for his investments.

- Cloud Service Growth: Amazon Web Services (AWS) achieved a 24% sales growth in Q4, while Google Cloud's revenue surged 48% year-over-year, indicating that AI integration has significantly enhanced their competitive edge in the cloud services market, solidifying their leadership positions.

- Valuation Advantage: Uber's forward P/E ratio stands at 17, while Amazon's projected cash flow P/E is only 9.6, highlighting the relative undervaluation of these companies in the current market, which may attract more investor interest and drive stock price increases.

- Advertising Pricing Power: Meta Platforms attracted an average of 3.58 billion daily users to its apps, far exceeding other social media platforms, which grants it exceptional pricing power in advertising, likely boosting its revenue and market share further.

See More