AstraZeneca Secures FDA Approval for Enhertu in First-Line Breast Cancer, Triggers $150M Milestone Payment

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Dec 23 2025

0mins

Should l Buy AZN?

Source: NASDAQ.COM

- FDA Approval: AstraZeneca and its partner Daiichi Sankyo's antibody-drug conjugate Enhertu has received FDA approval for first-line treatment of unresectable or metastatic HER2-positive breast cancer, marking a significant milestone in the U.S. market.

- Clinical Trial Results: The DESTINY-Breast09 study demonstrated that the Enhertu-Perjeta combination achieved a median progression-free survival of 40.7 months, a 51.5% improvement over the 26.9 months seen with the standard taxane chemotherapy, highlighting its superior efficacy.

- Financial Impact: This approval triggers a $150 million milestone payment from AstraZeneca to Daiichi Sankyo, further solidifying their global partnership and providing a new revenue growth avenue for AstraZeneca.

- Market Performance: Over the past year, AstraZeneca's stock has surged by 36.3%, significantly outperforming the industry average growth of 12.1%, reflecting strong market confidence in its newly approved drug and future growth potential.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy AZN?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on AZN

Wall Street analysts forecast AZN stock price to rise

14 Analyst Rating

13 Buy

0 Hold

1 Sell

Strong Buy

Current: 204.800

Low

157.61

Averages

213.64

High

252.18

Current: 204.800

Low

157.61

Averages

213.64

High

252.18

About AZN

AstraZeneca PLC is a United Kingdom-based science-led biopharmaceutical company. The Company focuses on the discovery, development, and commercialization of prescription medicines. The Company operates across therapy areas, including Oncology; Cardiovascular, Renal and Metabolism (CVRM); Respiratory and Immunology (R&I); Vaccines and Immune Therapies (V&I), and Rare Disease. In the Oncology area, its key products include Tagrisso, Imfinzi, Calquence, Lynparza, and Enhertu. The key products of CVRM area include Farxiga/Forxiga, Brilinta/Brilique, Crestor, and Lokelma. In the R&I area, the key products are Symbicort, Fasenra, Breztri/Trixeo, and Tezspire. In the V&I Therapies area, the products are Beyfortus and FluMist. The products in the Rare Disease area are Ultomiris, Soliris, Strensiq, and Koselugo. It has about 191 projects in its development pipeline, including 19 new molecular entities (NMEs) in the late-stage pipeline. The Company distributes its products in over 125 countries.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

AstraZeneca's Antibody Therapy Achieves Late-Stage Trial Success

- Trial Success: AstraZeneca announced a successful late-stage trial of its antibody therapy tozorakimab in the Phase 3 MIRANDA trial for chronic obstructive pulmonary disease (COPD), significantly reducing the annualized rate of moderate-to-severe exacerbations with both statistical and clinical significance.

- Broad Applicability: The therapy demonstrated efficacy across both former and current smokers, indicating its effectiveness regardless of lung function severity and blood eosinophil counts, thereby enhancing its market potential.

- Study Design: The 52-week study evaluated tozorakimab 300 mg administered biweekly against a placebo, aiming to assess its additional efficacy on top of standard inhaled therapy, further validating its clinical application value.

- Favorable Safety Profile: AstraZeneca noted that tozorakimab was generally well tolerated with a safety profile consistent with prior trials, and plans to submit the results to global regulators and present them at future medical events, facilitating its market introduction.

See More

AstraZeneca's IL-33-targeting Biologic Achieves Success in Phase III Trials

- Clinical Trial Results: AstraZeneca's IL-33-targeting biologic tozorakimab demonstrated significant efficacy in the Phase III MIRANDA trial, showing a meaningful reduction in the annualized rate of moderate-to-severe COPD exacerbations, particularly among former smokers, indicating its potential first-in-class status in COPD treatment.

- Patient Recruitment: The MIRANDA trial enrolled 1,454 patients, all of whom received tozorakimab 300mg alongside standard care, with results highlighting the drug's important clinical benefits for patients still experiencing exacerbations, thus addressing a critical need in COPD management.

- Safety Profile: Tozorakimab was generally well tolerated with a favorable safety profile consistent with previous trials, providing strong support for its future regulatory approval and the potential to offer new treatment options for COPD patients.

- Market Potential: With COPD being the third leading cause of death globally, affecting nearly 400 million people, the success of tozorakimab could significantly enhance patient quality of life and further bolster AstraZeneca's leadership position in the respiratory therapeutics market.

See More

Pictet North America Advisors Increases Stake in MercadoLibre

- Share Increase: On April 14, 2026, Pictet North America Advisors SA disclosed an increase of 3,529 shares in MercadoLibre, with an estimated transaction value of $6.81 million, indicating confidence in the company's future growth prospects.

- Stake Growth: Following this purchase, Pictet's stake in MercadoLibre rose to 2.21%, reflecting its emphasis on the company within its portfolio, particularly as MercadoLibre's market capitalization reached $92.87 billion.

- Financial Performance: Despite achieving a 44% revenue growth in 2025, MercadoLibre's net income only increased by 5% due to heightened competition and rising non-performing loans, indicating some profitability pressures.

- Market Outlook: Although facing short-term challenges, MercadoLibre is expected to maintain long-term growth potential due to its market leadership in Latin America and robust revenue growth, suggesting that Pictet's decision to increase its holdings may be based on confidence in this outlook.

See More

AbbVie Ventures into Weight Loss Market with Promising Drug

- Clinical Trial Results: AbbVie's March 9 announcement of ABBV-295's clinical trial results indicates that patients receiving weekly treatment lost an average of 7.75% to 9.79% of their weight over 12 weeks, while those on biweekly or monthly regimens lost between 7.86% and 9.73% over 13 weeks, suggesting strong potential for the drug in the weight loss market.

- Competitive Market Pressure: Despite the promising initial data for ABBV-295, AbbVie faces intense competition in the weight loss market from companies like Eli Lilly, which have several late-stage obesity drugs, indicating that the market will become increasingly crowded before AbbVie can launch its product.

- Core Business Stability: AbbVie's primary therapeutic area remains immunology, with projected sales for Skyrizi and Rinvoq exceeding $31 billion in 2023, significantly surpassing Humira's peak sales, demonstrating the company's robust performance and growth potential in this sector.

- Optimistic Pipeline Outlook: Even if ABBV-295 fails in clinical trials, AbbVie has a deep pipeline of investigational products, including the ongoing ABBV-383 cancer treatment, which is expected to provide significant support for the company's future financial performance and further solidify its leadership in the pharmaceutical industry.

See More

Rapid Growth of GLP-1 Drug Market

- Market Surge: According to Markets and Markets, the GLP-1 agonist market grew from $53.74 billion in 2024 to $64.42 billion in 2025, with projections reaching $170.75 billion by 2033, indicating a robust demand for obesity and diabetes treatments.

- New Drug Approval: In 2025, Novo Nordisk's Wegovy received FDA approval as the first oral GLP-1 weight-loss medication, marking a significant breakthrough in treatment options, particularly for those with trypanophobia, which is expected to further drive market demand.

- Top-Selling Drugs: In 2025, Mounjaro led the GLP-1 drug market with $22.97 billion in sales, followed by Ozempic and Zepbound with $20 billion and $13.54 billion, respectively, showcasing the strong appeal of GLP-1 therapies globally.

- Patent Protection and Competition: While Ozempic and Wegovy are protected by patents in the U.S. until around 2032, generics have already launched in India and are expected in China, intensifying market competition and potentially impacting the market share of original branded drugs.

See More

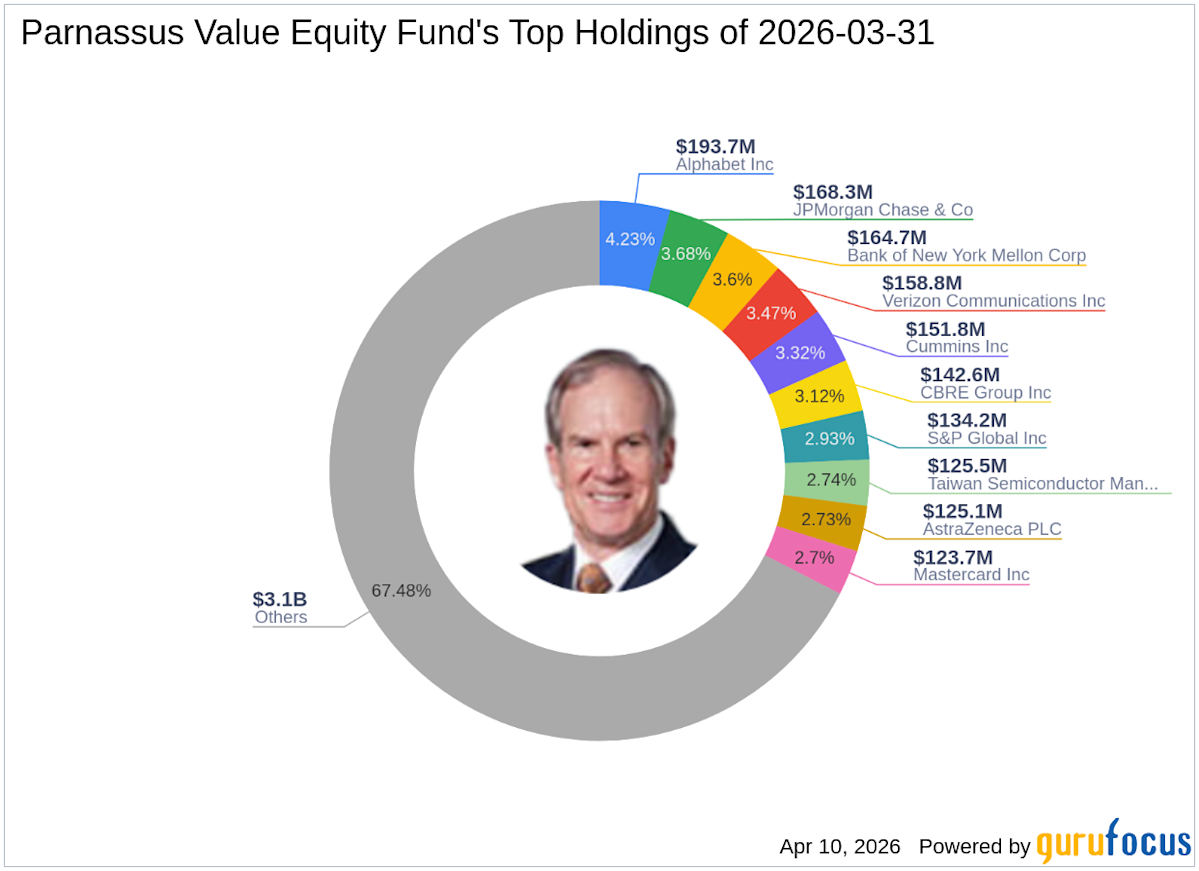

Parnassus Value Equity Fund's Q1 2026 Strategic Investment Moves

- New Investment Highlights: In Q1 2026, Parnassus Value Equity Fund added 634,492 shares of AstraZeneca (NYSE:AZN), representing 2.73% of the portfolio with a total value of $125.13 million, indicating confidence in the biopharmaceutical sector.

- Key Stock Increases: The fund increased its stake in JPMorgan Chase & Co by 72,858 shares, a 14.59% rise, bringing total holdings to 572,217 shares, reflecting optimism in the financial services industry with a current total value of $168.32 million.

- Strategic Reductions: The fund completely exited its position in AstraZeneca by selling 1,227,628 shares, resulting in a -2.37% impact on the portfolio, showcasing its agility in responding to market dynamics.

- Industry Concentration Analysis: As of Q1 2026, the fund's portfolio included 45 stocks, primarily concentrated in 10 industries such as Financial Services, Technology, and Healthcare, indicating a strategic approach to diversified investments.

See More

AstraZeneca's Antibody Therapy Achieves Late-Stage Trial Success

- Trial Success: AstraZeneca announced a successful late-stage trial of its antibody therapy tozorakimab in the Phase 3 MIRANDA trial for chronic obstructive pulmonary disease (COPD), significantly reducing the annualized rate of moderate-to-severe exacerbations with both statistical and clinical significance.

- Broad Applicability: The therapy demonstrated efficacy across both former and current smokers, indicating its effectiveness regardless of lung function severity and blood eosinophil counts, thereby enhancing its market potential.

- Study Design: The 52-week study evaluated tozorakimab 300 mg administered biweekly against a placebo, aiming to assess its additional efficacy on top of standard inhaled therapy, further validating its clinical application value.

- Favorable Safety Profile: AstraZeneca noted that tozorakimab was generally well tolerated with a safety profile consistent with prior trials, and plans to submit the results to global regulators and present them at future medical events, facilitating its market introduction.

See More

AstraZeneca's IL-33-targeting Biologic Achieves Success in Phase III Trials

- Clinical Trial Results: AstraZeneca's IL-33-targeting biologic tozorakimab demonstrated significant efficacy in the Phase III MIRANDA trial, showing a meaningful reduction in the annualized rate of moderate-to-severe COPD exacerbations, particularly among former smokers, indicating its potential first-in-class status in COPD treatment.

- Patient Recruitment: The MIRANDA trial enrolled 1,454 patients, all of whom received tozorakimab 300mg alongside standard care, with results highlighting the drug's important clinical benefits for patients still experiencing exacerbations, thus addressing a critical need in COPD management.

- Safety Profile: Tozorakimab was generally well tolerated with a favorable safety profile consistent with previous trials, providing strong support for its future regulatory approval and the potential to offer new treatment options for COPD patients.

- Market Potential: With COPD being the third leading cause of death globally, affecting nearly 400 million people, the success of tozorakimab could significantly enhance patient quality of life and further bolster AstraZeneca's leadership position in the respiratory therapeutics market.

See More

Pictet North America Advisors Increases Stake in MercadoLibre

- Share Increase: On April 14, 2026, Pictet North America Advisors SA disclosed an increase of 3,529 shares in MercadoLibre, with an estimated transaction value of $6.81 million, indicating confidence in the company's future growth prospects.

- Stake Growth: Following this purchase, Pictet's stake in MercadoLibre rose to 2.21%, reflecting its emphasis on the company within its portfolio, particularly as MercadoLibre's market capitalization reached $92.87 billion.

- Financial Performance: Despite achieving a 44% revenue growth in 2025, MercadoLibre's net income only increased by 5% due to heightened competition and rising non-performing loans, indicating some profitability pressures.

- Market Outlook: Although facing short-term challenges, MercadoLibre is expected to maintain long-term growth potential due to its market leadership in Latin America and robust revenue growth, suggesting that Pictet's decision to increase its holdings may be based on confidence in this outlook.

See More

AbbVie Ventures into Weight Loss Market with Promising Drug

- Clinical Trial Results: AbbVie's March 9 announcement of ABBV-295's clinical trial results indicates that patients receiving weekly treatment lost an average of 7.75% to 9.79% of their weight over 12 weeks, while those on biweekly or monthly regimens lost between 7.86% and 9.73% over 13 weeks, suggesting strong potential for the drug in the weight loss market.

- Competitive Market Pressure: Despite the promising initial data for ABBV-295, AbbVie faces intense competition in the weight loss market from companies like Eli Lilly, which have several late-stage obesity drugs, indicating that the market will become increasingly crowded before AbbVie can launch its product.

- Core Business Stability: AbbVie's primary therapeutic area remains immunology, with projected sales for Skyrizi and Rinvoq exceeding $31 billion in 2023, significantly surpassing Humira's peak sales, demonstrating the company's robust performance and growth potential in this sector.

- Optimistic Pipeline Outlook: Even if ABBV-295 fails in clinical trials, AbbVie has a deep pipeline of investigational products, including the ongoing ABBV-383 cancer treatment, which is expected to provide significant support for the company's future financial performance and further solidify its leadership in the pharmaceutical industry.

See More

Rapid Growth of GLP-1 Drug Market

- Market Surge: According to Markets and Markets, the GLP-1 agonist market grew from $53.74 billion in 2024 to $64.42 billion in 2025, with projections reaching $170.75 billion by 2033, indicating a robust demand for obesity and diabetes treatments.

- New Drug Approval: In 2025, Novo Nordisk's Wegovy received FDA approval as the first oral GLP-1 weight-loss medication, marking a significant breakthrough in treatment options, particularly for those with trypanophobia, which is expected to further drive market demand.

- Top-Selling Drugs: In 2025, Mounjaro led the GLP-1 drug market with $22.97 billion in sales, followed by Ozempic and Zepbound with $20 billion and $13.54 billion, respectively, showcasing the strong appeal of GLP-1 therapies globally.

- Patent Protection and Competition: While Ozempic and Wegovy are protected by patents in the U.S. until around 2032, generics have already launched in India and are expected in China, intensifying market competition and potentially impacting the market share of original branded drugs.

See More

Parnassus Value Equity Fund's Q1 2026 Strategic Investment Moves

- New Investment Highlights: In Q1 2026, Parnassus Value Equity Fund added 634,492 shares of AstraZeneca (NYSE:AZN), representing 2.73% of the portfolio with a total value of $125.13 million, indicating confidence in the biopharmaceutical sector.

- Key Stock Increases: The fund increased its stake in JPMorgan Chase & Co by 72,858 shares, a 14.59% rise, bringing total holdings to 572,217 shares, reflecting optimism in the financial services industry with a current total value of $168.32 million.

- Strategic Reductions: The fund completely exited its position in AstraZeneca by selling 1,227,628 shares, resulting in a -2.37% impact on the portfolio, showcasing its agility in responding to market dynamics.

- Industry Concentration Analysis: As of Q1 2026, the fund's portfolio included 45 stocks, primarily concentrated in 10 industries such as Financial Services, Technology, and Healthcare, indicating a strategic approach to diversified investments.

See More