AI Stocks Face Fatigue but Hold Long-Term Promise

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Apr 10 2026

0mins

Should l Buy NVDA?

Source: Fool

- Market Fatigue: While AI stocks were a hot investment in 2023, recent market enthusiasm has waned, indicating potential investor fatigue; however, experts believe AI stocks will remain among the best performers over the next decade, reflecting long-term confidence in the sector.

- Nvidia's Growth Potential: As the market leader in AI computing chips, Nvidia is projected to achieve a 71% revenue growth in 2023, and its strong market position coupled with ongoing AI infrastructure development makes it a solid long-term investment choice, underscoring its significance in the industry.

- Broadcom's Custom Chip Opportunity: Broadcom focuses on developing application-specific integrated circuits (ASICs), with expectations that this market could reach $100 billion by 2027, showcasing significant growth potential in the AI chip sector, even though its products cannot replace Nvidia's GPUs.

- TSMC's Production Expansion: Taiwan Semiconductor Manufacturing Company anticipates AI chip revenue to grow at a mid- to high-50% CAGR and plans to invest $52 billion to $56 billion in 2023 to expand production capacity, indicating its critical role and future success potential in the global AI market.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy NVDA?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on NVDA

Wall Street analysts forecast NVDA stock price to rise

41 Analyst Rating

39 Buy

1 Hold

1 Sell

Strong Buy

Current: 198.350

Low

200.00

Averages

264.97

High

352.00

Current: 198.350

Low

200.00

Averages

264.97

High

352.00

About NVDA

NVIDIA Corporation is an artificial intelligence (AI) infrastructure company. The Company is engaged in accelerated computing to help solve the challenging computational problems. Its segments include Compute & Networking and Graphics. The Compute & Networking segment includes its Data Center accelerated computing and networking platforms and AI solutions and software, and automotive platforms and autonomous and electric vehicle solutions, including software. The Graphics segment includes GeForce GPUs for gaming and personal computers (PCs), and Quadro/NVIDIA RTX GPUs for enterprise workstation graphics. Its technology stack includes the foundational NVIDIA CUDA development platform that runs on all NVIDIA GPUs, as well as hundreds of domain-specific software libraries, frameworks, algorithms, software development kits (SDKs), and application programming interfaces (APIs). Its platforms address four markets, which include Data Center, Gaming, Professional Visualization, and Automotive.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Nvidia's Stock Underperformance Despite Rapid Revenue Growth

- Significant Revenue Growth: Nvidia reported $68.1 billion in revenue for Q4 FY2026, a 73% increase year-over-year, with data center sales contributing $62.3 billion, up 75%, highlighting strong demand and market position in the AI sector.

- Capital Expenditure Commitments: The 'Magnificent Seven', including Alphabet, Microsoft, Amazon, and Meta, announced up to $700 billion in capital expenditures for 2023, which, while not all directed to Nvidia, will drive demand for its GPUs and impact future performance.

- Market Capitalization vs. Valuation: Despite Nvidia's market capitalization soaring to the highest in the past two years, its forward P/E ratio stands at 23.9, significantly below the three-year average of 79, indicating that the market may be underestimating its future growth potential, presenting a possible investment opportunity.

- Future Growth Expectations: CEO Jensen Huang forecasts that Nvidia could achieve $1 trillion in AI revenue by 2027, compared to just $215.9 billion in 2025, suggesting the company is on a trajectory of rapid growth that investors should closely monitor.

See More

Microsoft Stock Rebounds, Long-Term Outlook Positive

- Stock Rebound: Since the beginning of April, Microsoft's stock has surged over 14%, although it remains down more than 20% from its all-time high in October 2025, indicating strong market confidence in its long-term value.

- AI Threat Mitigation: By integrating the AI assistant Copilot into its productivity suite, Microsoft demonstrates a robust culture of innovation and strong enterprise relationships, effectively countering potential threats posed by AI and maintaining its core market share.

- Economic Resilience: A significant portion of Microsoft's revenue comes from subscription services, providing strong resilience during economic downturns, while its pricing power allows it to maintain its customer base even amid rising costs, further solidifying its market position.

- Reasonable Valuation: Despite the recent stock price increase, Microsoft's forward P/E ratio remains lower than the average of the

See More

Microsoft's Resilience Amid AI Revolution

- Stock Recovery: Since the beginning of April, Microsoft's shares have surged over 14%, although they remain down more than 20% from their all-time high in October 2025, indicating market confidence in its long-term potential.

- AI Threat Mitigation: By integrating the Copilot AI assistant into its productivity suite, Microsoft demonstrates a strong culture of innovation and deep relationships with enterprises, enabling it to effectively address the challenges posed by AI and maintain its core market share.

- Stable Revenue Streams: A significant portion of Microsoft's revenue comes from subscription services, allowing it to maintain stable cash flow during economic downturns, while its pricing power enables it to pass on cost increases to customers.

- Dividend Growth Potential: Over the past decade, Microsoft has increased its dividends by nearly 153%, providing stable returns during market volatility, and combined with its AAA credit rating and strong free cash flow, it positions itself as a quality investment choice now.

See More

Rocket Lab Stock Up Nearly 250%: A Buy-and-Hold Space Investment?

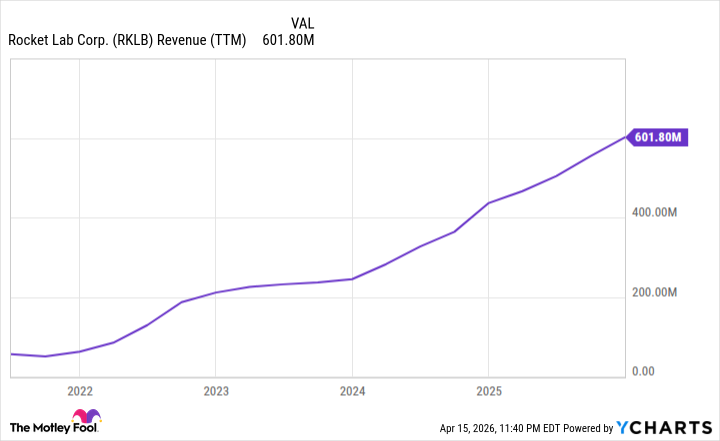

- Significant Revenue Growth: Rocket Lab achieved record revenue of $602 million in 2025, marking a 38% year-over-year increase, while its backlog surged by 73% to nearly $1.9 billion, indicating strong demand and growth potential in the aerospace market.

- Success Rate and Contracts: The company executed 21 missions last year with a 100% success rate, which helped secure an $816 million contract from the Space Development Agency, further solidifying its leadership position in the aerospace sector.

- Competitive New Rocket: The upcoming Neutron medium-lift rocket will enable Rocket Lab to compete directly with SpaceX's Falcon 9 at a launch price of approximately $15 million less, expected to significantly enhance the company's market share and profitability.

- Investment Risks and Opportunities: Although the stock is trading at about 66 times sales and the company reported a nearly $200 million loss in 2025, the improving margins and potential success of Neutron present substantial growth opportunities, especially in light of SpaceX's IPO plans.

See More

Nvidia Stock Pullback Yet Optimistic Outlook Persists

- Market Performance Retreat: Nvidia's stock has retreated nearly 4% over the past six months, dropping from a 52-week high to a market cap of $4.8 trillion, despite the company continuing to deliver remarkable growth each quarter, indicating a lack of market confidence in its future.

- Analyst Optimism: With a median 12-month price target of $267.50 from 70 analysts, which is 33% higher than Friday's closing price, Nvidia's market cap could rise to $6.5 trillion if this target is met, reflecting strong expectations for its future growth.

- Earnings Growth Potential: Nvidia is expected to achieve a 34% earnings growth in fiscal 2028, significantly above the S&P 500's 17%, making its forward P/E ratio of 24 appear justified, especially given the robust demand for its AI data center processors.

- Strong Revenue Projections: The company anticipates generating up to $1 trillion in revenue from its Blackwell and Vera Rubin data center lines in 2026 and 2027, exceeding analysts' expectations for the next two years, indicating substantial future growth potential.

See More

Nvidia Stock Pullback but Optimistic Outlook Ahead

- Market Performance Decline: Nvidia's stock has retreated nearly 4% over the past six months from its 52-week high in October, which is surprising given the company's continued impressive quarterly growth, reflecting market caution regarding its future prospects.

- Analyst Optimism: With a 12-month median price target of $267.50 from 70 analysts, which is 33% higher than last Friday's closing price, Nvidia's market cap could rise to $6.5 trillion if this target is met, indicating strong confidence in its future performance.

- Earnings Growth Potential: Nvidia is expected to achieve a 34% earnings growth in fiscal 2028, significantly above the 17% average for S&P 500 companies, suggesting that the company deserves a premium valuation due to strong demand for its AI data center processors.

- Strong Revenue Forecast: Nvidia anticipates generating up to $1 trillion in revenue from its Blackwell and Vera Rubin data center lines in 2026 and 2027, exceeding analysts' expectations for the next two years, highlighting its substantial growth potential.

See More

Nvidia's Stock Underperformance Despite Rapid Revenue Growth

- Significant Revenue Growth: Nvidia reported $68.1 billion in revenue for Q4 FY2026, a 73% increase year-over-year, with data center sales contributing $62.3 billion, up 75%, highlighting strong demand and market position in the AI sector.

- Capital Expenditure Commitments: The 'Magnificent Seven', including Alphabet, Microsoft, Amazon, and Meta, announced up to $700 billion in capital expenditures for 2023, which, while not all directed to Nvidia, will drive demand for its GPUs and impact future performance.

- Market Capitalization vs. Valuation: Despite Nvidia's market capitalization soaring to the highest in the past two years, its forward P/E ratio stands at 23.9, significantly below the three-year average of 79, indicating that the market may be underestimating its future growth potential, presenting a possible investment opportunity.

- Future Growth Expectations: CEO Jensen Huang forecasts that Nvidia could achieve $1 trillion in AI revenue by 2027, compared to just $215.9 billion in 2025, suggesting the company is on a trajectory of rapid growth that investors should closely monitor.

See More

Microsoft Stock Rebounds, Long-Term Outlook Positive

- Stock Rebound: Since the beginning of April, Microsoft's stock has surged over 14%, although it remains down more than 20% from its all-time high in October 2025, indicating strong market confidence in its long-term value.

- AI Threat Mitigation: By integrating the AI assistant Copilot into its productivity suite, Microsoft demonstrates a robust culture of innovation and strong enterprise relationships, effectively countering potential threats posed by AI and maintaining its core market share.

- Economic Resilience: A significant portion of Microsoft's revenue comes from subscription services, providing strong resilience during economic downturns, while its pricing power allows it to maintain its customer base even amid rising costs, further solidifying its market position.

- Reasonable Valuation: Despite the recent stock price increase, Microsoft's forward P/E ratio remains lower than the average of the

See More

Microsoft's Resilience Amid AI Revolution

- Stock Recovery: Since the beginning of April, Microsoft's shares have surged over 14%, although they remain down more than 20% from their all-time high in October 2025, indicating market confidence in its long-term potential.

- AI Threat Mitigation: By integrating the Copilot AI assistant into its productivity suite, Microsoft demonstrates a strong culture of innovation and deep relationships with enterprises, enabling it to effectively address the challenges posed by AI and maintain its core market share.

- Stable Revenue Streams: A significant portion of Microsoft's revenue comes from subscription services, allowing it to maintain stable cash flow during economic downturns, while its pricing power enables it to pass on cost increases to customers.

- Dividend Growth Potential: Over the past decade, Microsoft has increased its dividends by nearly 153%, providing stable returns during market volatility, and combined with its AAA credit rating and strong free cash flow, it positions itself as a quality investment choice now.

See More

Rocket Lab Stock Up Nearly 250%: A Buy-and-Hold Space Investment?

- Significant Revenue Growth: Rocket Lab achieved record revenue of $602 million in 2025, marking a 38% year-over-year increase, while its backlog surged by 73% to nearly $1.9 billion, indicating strong demand and growth potential in the aerospace market.

- Success Rate and Contracts: The company executed 21 missions last year with a 100% success rate, which helped secure an $816 million contract from the Space Development Agency, further solidifying its leadership position in the aerospace sector.

- Competitive New Rocket: The upcoming Neutron medium-lift rocket will enable Rocket Lab to compete directly with SpaceX's Falcon 9 at a launch price of approximately $15 million less, expected to significantly enhance the company's market share and profitability.

- Investment Risks and Opportunities: Although the stock is trading at about 66 times sales and the company reported a nearly $200 million loss in 2025, the improving margins and potential success of Neutron present substantial growth opportunities, especially in light of SpaceX's IPO plans.

See More

Nvidia Stock Pullback Yet Optimistic Outlook Persists

- Market Performance Retreat: Nvidia's stock has retreated nearly 4% over the past six months, dropping from a 52-week high to a market cap of $4.8 trillion, despite the company continuing to deliver remarkable growth each quarter, indicating a lack of market confidence in its future.

- Analyst Optimism: With a median 12-month price target of $267.50 from 70 analysts, which is 33% higher than Friday's closing price, Nvidia's market cap could rise to $6.5 trillion if this target is met, reflecting strong expectations for its future growth.

- Earnings Growth Potential: Nvidia is expected to achieve a 34% earnings growth in fiscal 2028, significantly above the S&P 500's 17%, making its forward P/E ratio of 24 appear justified, especially given the robust demand for its AI data center processors.

- Strong Revenue Projections: The company anticipates generating up to $1 trillion in revenue from its Blackwell and Vera Rubin data center lines in 2026 and 2027, exceeding analysts' expectations for the next two years, indicating substantial future growth potential.

See More

Nvidia Stock Pullback but Optimistic Outlook Ahead

- Market Performance Decline: Nvidia's stock has retreated nearly 4% over the past six months from its 52-week high in October, which is surprising given the company's continued impressive quarterly growth, reflecting market caution regarding its future prospects.

- Analyst Optimism: With a 12-month median price target of $267.50 from 70 analysts, which is 33% higher than last Friday's closing price, Nvidia's market cap could rise to $6.5 trillion if this target is met, indicating strong confidence in its future performance.

- Earnings Growth Potential: Nvidia is expected to achieve a 34% earnings growth in fiscal 2028, significantly above the 17% average for S&P 500 companies, suggesting that the company deserves a premium valuation due to strong demand for its AI data center processors.

- Strong Revenue Forecast: Nvidia anticipates generating up to $1 trillion in revenue from its Blackwell and Vera Rubin data center lines in 2026 and 2027, exceeding analysts' expectations for the next two years, highlighting its substantial growth potential.

See More