Why Oracle Shares Are Trading Higher By Around 8%; Here Are 20 Stocks Moving Premarket

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Jun 12 2025

0mins

Source: Benzinga

Oracle Corporation Financial Results: Oracle's shares rose 7.6% in pre-market trading after reporting fourth-quarter revenue of $15.9 billion and adjusted earnings of $1.70 per share, both exceeding analyst expectations.

Pre-Market Stock Movements: Several stocks experienced significant changes in pre-market trading, with Healthcare Triangle, Inc. surging 141.3% and Intensity Therapeutics, Inc. plummeting 47.7% following their respective announcements.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy ORCL?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on ORCL

Wall Street analysts forecast ORCL stock price to rise

34 Analyst Rating

25 Buy

9 Hold

0 Sell

Moderate Buy

Current: 141.600

Low

180.00

Averages

309.59

High

400.00

Current: 141.600

Low

180.00

Averages

309.59

High

400.00

About ORCL

Oracle Corporation offers integrated suites of applications plus secure, autonomous infrastructure in the Oracle Cloud. The Company operates through three businesses: cloud and license, hardware and service. Its cloud and license business is engaged in the sale, marketing and delivery of its enterprise applications and infrastructure technologies through cloud and on-premise deployment models including its cloud services and license support offerings, and its cloud license and on-premise license offerings. Its hardware business provides infrastructure technologies including Oracle Engineered Systems, servers, storage, industry-specific hardware, operating systems, virtualization, management and other hardware-related software to support diverse IT environments. Its services business provides services to customers and partners to help maximize the performance of their investments in Oracle applications and infrastructure technologies.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Oracle Faces Customer Default Risks Amidst Massive Order Backlog

- Surging Order Backlog: Oracle's remaining performance obligations (RPO) have soared to $638 billion, a 363% year-over-year increase, indicating strong demand for its AI data centers, yet also raising concerns about customer payment capabilities.

- Customer Financial Risks: Approximately $300 billion of the RPO is attributed to OpenAI, which has only $25 billion in annual revenue and is currently operating at a loss, posing significant risks of non-performance that could lead to substantial downward revisions in Oracle's revenue expectations.

- Heavy Debt Burden: Oracle is currently carrying over $122 billion in long-term debt and plans to raise an additional $40 billion through a mix of debt and equity to fund its data center expansion, which could lead to a financial crisis if customer defaults occur under such high leverage.

- Dismal Revenue Conversion Outlook: Oracle expects to convert only about 12% of its RPO into revenue over the next 12 months, followed by another 34% in the subsequent 24 months, meaning that in the best-case scenario, less than half of its RPO will translate into actual revenue over the next three years, causing investor unease.

See More

AppLovin Shares Drop 16% Amid Software Sector Headwinds

- Stock Decline: AppLovin's shares fell 16% last month despite positive analyst notes, indicating the risks associated with its high valuation amid broader software sector pressures.

- Sector Impact: Disappointing earnings from companies like Salesforce, Adobe, and Oracle, coupled with AI disruption concerns, weighed on AppLovin, highlighting the stock's sensitivity to high-growth market dynamics.

- Competitive Pressure: The recent IPO of smaller rival Liftoff Mobile in early June may have prompted investors to rotate into that stock, increasing selling pressure on AppLovin and raising concerns about its future growth prospects.

- Analyst Support: Despite challenges, AppLovin received endorsements from Wall Street, with firms like Citigroup and Edgewater Research expressing optimism about its outlook, projecting a 54% revenue increase to $1.94 billion in Q2.

See More

AppLovin Stock Declines Amid Software Sector Headwinds

- Stock Decline: AppLovin's shares fell 16% last month despite positive analyst notes, indicating vulnerability in a high-valuation environment as broader software sector weaknesses weighed heavily on its performance.

- Sector Impact: Disappointing earnings from Salesforce, Adobe, and Oracle raised concerns about AI disruption, exacerbating negative sentiment around AppLovin, even though its business model differs significantly from traditional SaaS companies.

- Competitive Pressure: The public offering of rival Liftoff Mobile in June may have prompted investors to rotate towards that stock, increasing selling pressure on AppLovin and highlighting market sensitivity to new competitors.

- Growth Expectations: Despite these challenges, analysts project a 54% revenue increase for AppLovin in Q2 to $1.94 billion, with earnings per share expected to rise from $2.39 to $3.75, suggesting that if growth can be sustained, the stock may rebound in the future.

See More

US Stocks Decline as Oil Prices Surge

- Market Decline: The S&P 500 index fell by 0.79%, the Dow Jones Industrial Average dropped by 1.44%, and the Nasdaq 100 index decreased by 0.61%, reflecting heightened investor caution following President Trump's declaration that the ceasefire with Iran is over, prompting a flight to safety.

- Surge in Oil Prices: WTI crude oil prices surged over 7% to a two-week high as the US launched strikes against Iran, raising concerns about potential disruptions to energy supplies and pushing inflation expectations higher, which in turn lifted the 10-year Treasury note yield to a 1.5-month high of 4.59%.

- Mortgage Applications Decline: US MBA mortgage applications fell by 2.2% in the week ending July 3, with the purchase mortgage sub-index down 0.6% and the refinancing sub-index down 4.1%, indicating that high interest rates are negatively impacting housing demand and could further suppress the recovery in the real estate market.

- Optimistic Earnings Outlook: Bloomberg Intelligence forecasts a 23% increase in corporate earnings for Q2, close to the 30% growth seen in Q1, indicating that AI infrastructure stocks are expected to contribute nearly 60% of the S&P 500's earnings-per-share growth, suggesting a positive long-term outlook despite short-term market volatility.

See More

Analysis of Oracle's Significant Stock Decline

- Stock Price Decline: According to S&P Global Market Intelligence, Oracle's (ORCL) stock fell by 24.8% in the first half of 2026, mirroring Microsoft's (MSFT) decline, while Amazon and Alphabet showed positive performance, indicating varied market reactions.

- AI Infrastructure Investment Pressure: Despite rising forecasts for AI infrastructure construction in 2026, Oracle's increased capital spending requirements have pressured its stock, reflecting concerns about its future growth potential.

- Risk from OpenAI Partnership: Oracle's landmark $300 billion deal with OpenAI initially received a positive market response, but the bond market's increased pricing of default risk indicates investor concerns about Oracle's financial health.

- Uncertain Financial Outlook for OpenAI: OpenAI is projected to burn through over $650 billion in cash by 2030, and while it expects to generate $280 billion in revenue by then, skepticism about achieving these targets has negatively impacted Oracle and Microsoft's stock performance.

See More

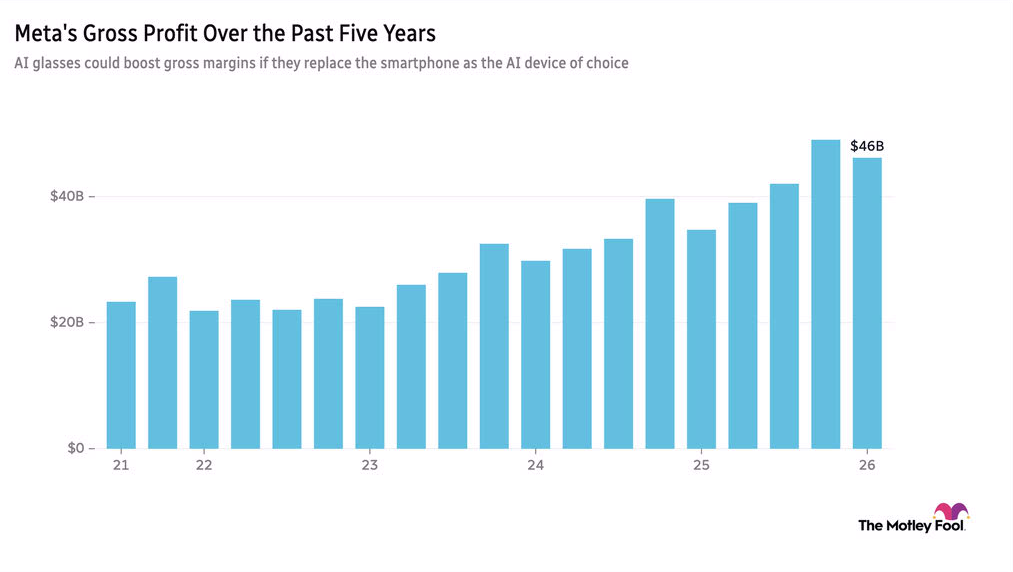

Meta Tests Next-Gen AI Glasses for Enhanced User Experience

- Product Testing: Meta's next-generation AI glasses have entered the prototype testing phase, designed to continuously track what the wearer sees and hears, with CEO Mark Zuckerberg stating that this technology will provide users with an all-day personal intelligence assistant, showcasing Meta's innovative potential in smart hardware.

- Privacy Concerns: The new glasses will not light up an LED when recording, raising privacy concerns, although proposals suggest only storing metadata and extracted images for AI queries, indicating Meta's efforts to balance technological advancement with user privacy.

- Escalating Chip Wars: DeepSeek is developing its own AI processor to reduce reliance on Nvidia and Huawei, aligning with Beijing's strategy to minimize dependence on critical U.S. semiconductor technology, highlighting the intensifying global tech competition and its potential impact on market dynamics.

- Market Dynamics Watch: Following powerful U.S. strikes against Iran, market sentiment has been affected, with S&P 500 and Nasdaq futures sliding about 1%, while Levi Strauss anticipates a 4%-5% revenue growth in Q2, reflecting resilience amid challenges in the consumer market.

See More

Oracle Faces Customer Default Risks Amidst Massive Order Backlog

- Surging Order Backlog: Oracle's remaining performance obligations (RPO) have soared to $638 billion, a 363% year-over-year increase, indicating strong demand for its AI data centers, yet also raising concerns about customer payment capabilities.

- Customer Financial Risks: Approximately $300 billion of the RPO is attributed to OpenAI, which has only $25 billion in annual revenue and is currently operating at a loss, posing significant risks of non-performance that could lead to substantial downward revisions in Oracle's revenue expectations.

- Heavy Debt Burden: Oracle is currently carrying over $122 billion in long-term debt and plans to raise an additional $40 billion through a mix of debt and equity to fund its data center expansion, which could lead to a financial crisis if customer defaults occur under such high leverage.

- Dismal Revenue Conversion Outlook: Oracle expects to convert only about 12% of its RPO into revenue over the next 12 months, followed by another 34% in the subsequent 24 months, meaning that in the best-case scenario, less than half of its RPO will translate into actual revenue over the next three years, causing investor unease.

See More

AppLovin Shares Drop 16% Amid Software Sector Headwinds

- Stock Decline: AppLovin's shares fell 16% last month despite positive analyst notes, indicating the risks associated with its high valuation amid broader software sector pressures.

- Sector Impact: Disappointing earnings from companies like Salesforce, Adobe, and Oracle, coupled with AI disruption concerns, weighed on AppLovin, highlighting the stock's sensitivity to high-growth market dynamics.

- Competitive Pressure: The recent IPO of smaller rival Liftoff Mobile in early June may have prompted investors to rotate into that stock, increasing selling pressure on AppLovin and raising concerns about its future growth prospects.

- Analyst Support: Despite challenges, AppLovin received endorsements from Wall Street, with firms like Citigroup and Edgewater Research expressing optimism about its outlook, projecting a 54% revenue increase to $1.94 billion in Q2.

See More

AppLovin Stock Declines Amid Software Sector Headwinds

- Stock Decline: AppLovin's shares fell 16% last month despite positive analyst notes, indicating vulnerability in a high-valuation environment as broader software sector weaknesses weighed heavily on its performance.

- Sector Impact: Disappointing earnings from Salesforce, Adobe, and Oracle raised concerns about AI disruption, exacerbating negative sentiment around AppLovin, even though its business model differs significantly from traditional SaaS companies.

- Competitive Pressure: The public offering of rival Liftoff Mobile in June may have prompted investors to rotate towards that stock, increasing selling pressure on AppLovin and highlighting market sensitivity to new competitors.

- Growth Expectations: Despite these challenges, analysts project a 54% revenue increase for AppLovin in Q2 to $1.94 billion, with earnings per share expected to rise from $2.39 to $3.75, suggesting that if growth can be sustained, the stock may rebound in the future.

See More

US Stocks Decline as Oil Prices Surge

- Market Decline: The S&P 500 index fell by 0.79%, the Dow Jones Industrial Average dropped by 1.44%, and the Nasdaq 100 index decreased by 0.61%, reflecting heightened investor caution following President Trump's declaration that the ceasefire with Iran is over, prompting a flight to safety.

- Surge in Oil Prices: WTI crude oil prices surged over 7% to a two-week high as the US launched strikes against Iran, raising concerns about potential disruptions to energy supplies and pushing inflation expectations higher, which in turn lifted the 10-year Treasury note yield to a 1.5-month high of 4.59%.

- Mortgage Applications Decline: US MBA mortgage applications fell by 2.2% in the week ending July 3, with the purchase mortgage sub-index down 0.6% and the refinancing sub-index down 4.1%, indicating that high interest rates are negatively impacting housing demand and could further suppress the recovery in the real estate market.

- Optimistic Earnings Outlook: Bloomberg Intelligence forecasts a 23% increase in corporate earnings for Q2, close to the 30% growth seen in Q1, indicating that AI infrastructure stocks are expected to contribute nearly 60% of the S&P 500's earnings-per-share growth, suggesting a positive long-term outlook despite short-term market volatility.

See More

Analysis of Oracle's Significant Stock Decline

- Stock Price Decline: According to S&P Global Market Intelligence, Oracle's (ORCL) stock fell by 24.8% in the first half of 2026, mirroring Microsoft's (MSFT) decline, while Amazon and Alphabet showed positive performance, indicating varied market reactions.

- AI Infrastructure Investment Pressure: Despite rising forecasts for AI infrastructure construction in 2026, Oracle's increased capital spending requirements have pressured its stock, reflecting concerns about its future growth potential.

- Risk from OpenAI Partnership: Oracle's landmark $300 billion deal with OpenAI initially received a positive market response, but the bond market's increased pricing of default risk indicates investor concerns about Oracle's financial health.

- Uncertain Financial Outlook for OpenAI: OpenAI is projected to burn through over $650 billion in cash by 2030, and while it expects to generate $280 billion in revenue by then, skepticism about achieving these targets has negatively impacted Oracle and Microsoft's stock performance.

See More

Meta Tests Next-Gen AI Glasses for Enhanced User Experience

- Product Testing: Meta's next-generation AI glasses have entered the prototype testing phase, designed to continuously track what the wearer sees and hears, with CEO Mark Zuckerberg stating that this technology will provide users with an all-day personal intelligence assistant, showcasing Meta's innovative potential in smart hardware.

- Privacy Concerns: The new glasses will not light up an LED when recording, raising privacy concerns, although proposals suggest only storing metadata and extracted images for AI queries, indicating Meta's efforts to balance technological advancement with user privacy.

- Escalating Chip Wars: DeepSeek is developing its own AI processor to reduce reliance on Nvidia and Huawei, aligning with Beijing's strategy to minimize dependence on critical U.S. semiconductor technology, highlighting the intensifying global tech competition and its potential impact on market dynamics.

- Market Dynamics Watch: Following powerful U.S. strikes against Iran, market sentiment has been affected, with S&P 500 and Nasdaq futures sliding about 1%, while Levi Strauss anticipates a 4%-5% revenue growth in Q2, reflecting resilience amid challenges in the consumer market.

See More