Wells Fargo Optimistic on Chip Equipment Makers' Outlook

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 1 hour ago

0mins

Source: seekingalpha

- Positive Market Outlook: Wells Fargo anticipates continued strong performance for semiconductor equipment manufacturers in Q2 2026, particularly for ASML, raising its 2027 Wafer Fab Equipment market estimate from $180 billion to $190 billion, reflecting confidence in industry recovery.

- Accelerating Demand: Analysts noted that despite recent stock fluctuations, investors remain optimistic about semiconductor capital equipment stocks, with ASML's year-to-date performance (+80%) seen as a potential catch-up trade compared to the peer average (+127%).

- Forecast Updates: Wells Fargo also increased its 2028 Wafer Fab Equipment market estimate from $191 billion to $216 billion, indicating strong expectations for advanced foundry and DRAM demand, with Lam Research and KLA likely to raise their 2026 outlook as well.

- Confidence in Technical Capacity: Analysts emphasized that ASML is expected to reiterate its low-NA tool capacity for 2027, projecting support for at least 60 tools in 2026 and at least 80 in 2027, showcasing the company's robust capability to meet market demand.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy ASML?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on ASML

Wall Street analysts forecast ASML stock price to fall

12 Analyst Rating

12 Buy

0 Hold

0 Sell

Strong Buy

Current: 1929.680

Low

1385

Averages

1583

High

1911

Current: 1929.680

Low

1385

Averages

1583

High

1911

About ASML

ASML Holding N.V. is a holding company based in the Netherlands. The Company operates through its subsidiaries in the Netherlands, the United States, Italy, France, Germany, the United Kingdom, Ireland, Belgium, South Korea, Taiwan, Singapore, China, Hong Kong, Japan, Malaysia and Israel. The Company operates through one business segment which is engage in development, production, marketing, sales, upgrading and servicing of advanced semiconductor equipment systems, consisting of lithography, metrology and inspection systems. The Company offers TWINSCAN systems, equipped with lithography system with a mercury lamp as light source (i-line), Krypton Fluoride (KrF) and Argon Fluoride (ArF) light sources for processing wafers for manufacturing environments for which imaging at a small resolution is required. TWINSCAN systems also include immersion lithography systems (TWINSCAN immersion systems).

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

ASML Expected to Outperform Amid Surge in Semiconductor Orders

- Surge in Orders: Bank of America indicates that ASML's semiconductor fabrication business is likely to see a significant influx of orders due to rising demand for more powerful memory solutions, reinforcing its market position.

- Price Target Increase: The bank raised ASML's stock price target to $2,345, suggesting nearly a 22% upside from Thursday's close, reflecting strong confidence in the company's future growth prospects.

- Technological Edge: ASML has industrialized next-gen Extreme Ultraviolet (EUV) lithography technology, which is expected to drive many disruptive trends this decade, particularly in artificial intelligence and dynamic random access memory sectors.

- Market Expectations: ASML is anticipated to report a full order book through 2027 in its upcoming earnings report, further validating its leadership in the rapidly growing semiconductor market, with all 19 analysts covering the stock rating it as a buy or strong buy.

See More

Wells Fargo Optimistic on Chip Equipment Makers' Outlook

- Positive Market Outlook: Wells Fargo anticipates continued strong performance for semiconductor equipment manufacturers in Q2 2026, particularly for ASML, raising its 2027 Wafer Fab Equipment market estimate from $180 billion to $190 billion, reflecting confidence in industry recovery.

- Accelerating Demand: Analysts noted that despite recent stock fluctuations, investors remain optimistic about semiconductor capital equipment stocks, with ASML's year-to-date performance (+80%) seen as a potential catch-up trade compared to the peer average (+127%).

- Forecast Updates: Wells Fargo also increased its 2028 Wafer Fab Equipment market estimate from $191 billion to $216 billion, indicating strong expectations for advanced foundry and DRAM demand, with Lam Research and KLA likely to raise their 2026 outlook as well.

- Confidence in Technical Capacity: Analysts emphasized that ASML is expected to reiterate its low-NA tool capacity for 2027, projecting support for at least 60 tools in 2026 and at least 80 in 2027, showcasing the company's robust capability to meet market demand.

See More

ASML Investment Returns 230%, Future Growth Expected

- Significant Investment Returns: Since investing in ASML in early 2021, the investor has realized an unrealized gain of approximately 230%, with the position accounting for 5% of their portfolio, reflecting the company's robust performance in the semiconductor sector.

- Market Dominance: ASML is the world's only producer of extreme ultraviolet (EUV) lithography machines, with prices ranging from $200 million to $400 million, and its strong pricing power and market moat have driven gross margins from 48.6% in 2020 to 52.8% by 2025.

- Sustained Growth Drivers: Despite macro challenges such as the pandemic, supply chain disruptions, and inflation, ASML's revenue and EPS have grown at CAGRs of 18% and 24% from 2020 to 2025, underscoring its critical role in the global semiconductor market.

- Optimistic Future Outlook: Analysts expect ASML's revenue and EPS to grow at CAGRs of 18% and 27% from 2025 to 2028, particularly driven by increasing demand for its high-NA EUV systems in the booming AI market.

See More

Market Dynamics and Corporate Mergers Overview

- Muted Market Start: The new trading week begins with the S&P 500 indicated flat while the tech-heavy Nasdaq shows slight gains, and WTI crude oil is trading around $76.50 per barrel, reflecting cautious market sentiment regarding economic outlook.

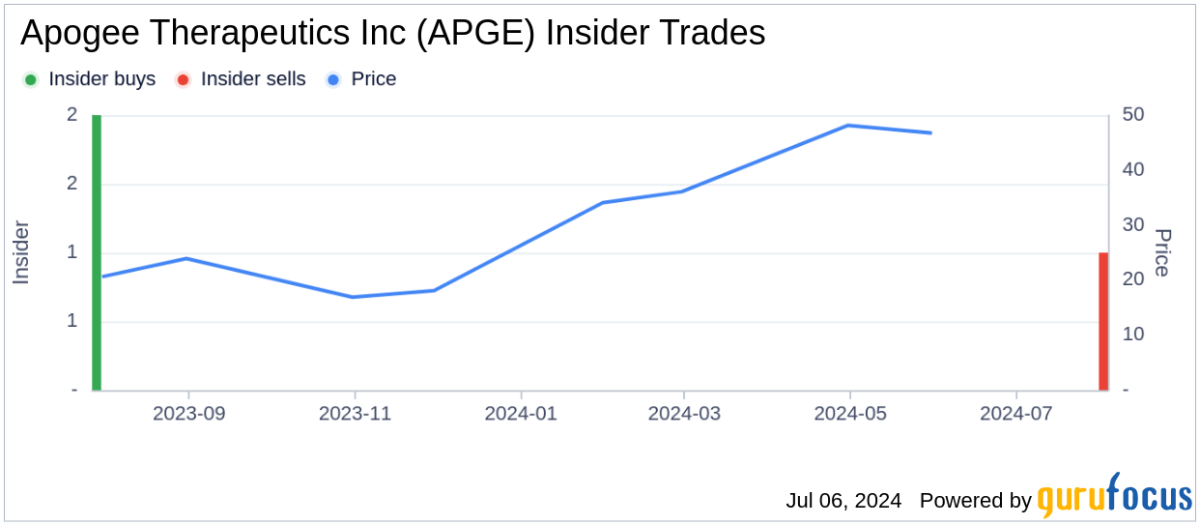

- Abbvie Acquires Apogee: Abbvie is acquiring Apogee Therapeutics for $10.9 billion to strengthen its immunology portfolio, particularly competing with Johnson & Johnson's Tremfya through its top drug Skyrizi, which is expected to enhance Abbvie's competitive edge in the biopharmaceutical market.

- CRH Acquires Arcosa: CRH is acquiring Arcosa for $8.5 billion, stating that the acquisition is highly complementary amid growing demand for energy and utility infrastructure, which is expected to further solidify CRH's position in the construction materials market.

- Estee Lauder Buy Rating Reinstated: Goldman Sachs has reinstated a buy rating for Estee Lauder with a price target of $100, as analysts believe the market is underestimating the company's growth momentum, especially after it walked away from merger talks with Spanish beauty peer Puig.

See More

BofA Raises ASML Price Target to $2,345 Amid Bullish Outlook

- Strong Order Expectations: BofA anticipates ASML's order book will be fully booked for 2027, a forecast that could shift investor focus towards 2028 earnings expectations, thereby enhancing market confidence.

- Price Target Increase: BofA raised ASML's price target from $2,268 to $2,345, implying a 22% upside potential from Thursday's closing price, reflecting strong confidence in the company's future earnings power.

- Outstanding Market Performance: ASML has added nearly $331 billion to its market capitalization in 2026 so far, with shares rising nearly 1% in Monday's pre-market trading, indicating investor optimism about its long-term growth.

- Robust Industry Demand: Analysts are becoming increasingly bullish on ASML, primarily due to sustained demand for extreme ultraviolet (EUV) lithography systems, which further solidifies the positive outlook for the semiconductor capital equipment sector.

See More

Nvidia Calls Marvell Next Trillion-Dollar Semiconductor Stock

- Investment and Partnership: Nvidia's $2 billion investment in Marvell earlier this year, coupled with a partnership to streamline integration for Marvell's custom chip customers like Amazon via NVLink Fusion, enhances Marvell's competitive edge in the semiconductor market.

- Revenue Growth Expectations: Marvell anticipates a 40% revenue increase this year to $11.5 billion, with interconnect revenue soaring by 70%, indicating strong growth potential in the rapidly expanding AI data center market.

- Market Challenges: Despite Marvell's robust performance in custom chips, it faces competition from Taiwanese semiconductor firm AIchip, which may jeopardize its leading role in future iterations of its Trainium chips, posing a threat to its market share.

- Industry Outlook: With a market cap below $250 billion and a frothy forward P/E ratio nearing 70 times, Marvell must achieve significant growth to reach a $1 trillion valuation in the coming years, which is a critical point of concern for investors.

See More

ASML Expected to Outperform Amid Surge in Semiconductor Orders

- Surge in Orders: Bank of America indicates that ASML's semiconductor fabrication business is likely to see a significant influx of orders due to rising demand for more powerful memory solutions, reinforcing its market position.

- Price Target Increase: The bank raised ASML's stock price target to $2,345, suggesting nearly a 22% upside from Thursday's close, reflecting strong confidence in the company's future growth prospects.

- Technological Edge: ASML has industrialized next-gen Extreme Ultraviolet (EUV) lithography technology, which is expected to drive many disruptive trends this decade, particularly in artificial intelligence and dynamic random access memory sectors.

- Market Expectations: ASML is anticipated to report a full order book through 2027 in its upcoming earnings report, further validating its leadership in the rapidly growing semiconductor market, with all 19 analysts covering the stock rating it as a buy or strong buy.

See More

Wells Fargo Optimistic on Chip Equipment Makers' Outlook

- Positive Market Outlook: Wells Fargo anticipates continued strong performance for semiconductor equipment manufacturers in Q2 2026, particularly for ASML, raising its 2027 Wafer Fab Equipment market estimate from $180 billion to $190 billion, reflecting confidence in industry recovery.

- Accelerating Demand: Analysts noted that despite recent stock fluctuations, investors remain optimistic about semiconductor capital equipment stocks, with ASML's year-to-date performance (+80%) seen as a potential catch-up trade compared to the peer average (+127%).

- Forecast Updates: Wells Fargo also increased its 2028 Wafer Fab Equipment market estimate from $191 billion to $216 billion, indicating strong expectations for advanced foundry and DRAM demand, with Lam Research and KLA likely to raise their 2026 outlook as well.

- Confidence in Technical Capacity: Analysts emphasized that ASML is expected to reiterate its low-NA tool capacity for 2027, projecting support for at least 60 tools in 2026 and at least 80 in 2027, showcasing the company's robust capability to meet market demand.

See More

ASML Investment Returns 230%, Future Growth Expected

- Significant Investment Returns: Since investing in ASML in early 2021, the investor has realized an unrealized gain of approximately 230%, with the position accounting for 5% of their portfolio, reflecting the company's robust performance in the semiconductor sector.

- Market Dominance: ASML is the world's only producer of extreme ultraviolet (EUV) lithography machines, with prices ranging from $200 million to $400 million, and its strong pricing power and market moat have driven gross margins from 48.6% in 2020 to 52.8% by 2025.

- Sustained Growth Drivers: Despite macro challenges such as the pandemic, supply chain disruptions, and inflation, ASML's revenue and EPS have grown at CAGRs of 18% and 24% from 2020 to 2025, underscoring its critical role in the global semiconductor market.

- Optimistic Future Outlook: Analysts expect ASML's revenue and EPS to grow at CAGRs of 18% and 27% from 2025 to 2028, particularly driven by increasing demand for its high-NA EUV systems in the booming AI market.

See More

Market Dynamics and Corporate Mergers Overview

- Muted Market Start: The new trading week begins with the S&P 500 indicated flat while the tech-heavy Nasdaq shows slight gains, and WTI crude oil is trading around $76.50 per barrel, reflecting cautious market sentiment regarding economic outlook.

- Abbvie Acquires Apogee: Abbvie is acquiring Apogee Therapeutics for $10.9 billion to strengthen its immunology portfolio, particularly competing with Johnson & Johnson's Tremfya through its top drug Skyrizi, which is expected to enhance Abbvie's competitive edge in the biopharmaceutical market.

- CRH Acquires Arcosa: CRH is acquiring Arcosa for $8.5 billion, stating that the acquisition is highly complementary amid growing demand for energy and utility infrastructure, which is expected to further solidify CRH's position in the construction materials market.

- Estee Lauder Buy Rating Reinstated: Goldman Sachs has reinstated a buy rating for Estee Lauder with a price target of $100, as analysts believe the market is underestimating the company's growth momentum, especially after it walked away from merger talks with Spanish beauty peer Puig.

See More

BofA Raises ASML Price Target to $2,345 Amid Bullish Outlook

- Strong Order Expectations: BofA anticipates ASML's order book will be fully booked for 2027, a forecast that could shift investor focus towards 2028 earnings expectations, thereby enhancing market confidence.

- Price Target Increase: BofA raised ASML's price target from $2,268 to $2,345, implying a 22% upside potential from Thursday's closing price, reflecting strong confidence in the company's future earnings power.

- Outstanding Market Performance: ASML has added nearly $331 billion to its market capitalization in 2026 so far, with shares rising nearly 1% in Monday's pre-market trading, indicating investor optimism about its long-term growth.

- Robust Industry Demand: Analysts are becoming increasingly bullish on ASML, primarily due to sustained demand for extreme ultraviolet (EUV) lithography systems, which further solidifies the positive outlook for the semiconductor capital equipment sector.

See More

Nvidia Calls Marvell Next Trillion-Dollar Semiconductor Stock

- Investment and Partnership: Nvidia's $2 billion investment in Marvell earlier this year, coupled with a partnership to streamline integration for Marvell's custom chip customers like Amazon via NVLink Fusion, enhances Marvell's competitive edge in the semiconductor market.

- Revenue Growth Expectations: Marvell anticipates a 40% revenue increase this year to $11.5 billion, with interconnect revenue soaring by 70%, indicating strong growth potential in the rapidly expanding AI data center market.

- Market Challenges: Despite Marvell's robust performance in custom chips, it faces competition from Taiwanese semiconductor firm AIchip, which may jeopardize its leading role in future iterations of its Trainium chips, posing a threat to its market share.

- Industry Outlook: With a market cap below $250 billion and a frothy forward P/E ratio nearing 70 times, Marvell must achieve significant growth to reach a $1 trillion valuation in the coming years, which is a critical point of concern for investors.

See More