Walmart Shares Hit Record High Ahead of Earnings

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 42 minutes ago

0mins

Should l Buy WMT?

Source: stocktwits

- Record High Stock Price: Walmart (WMT) shares reached $134.71 on Tuesday, climbing 37% over the past 12 months, reflecting strong investor confidence ahead of its upcoming quarterly earnings report.

- Strong Revenue Expectations: Analysts project Q1 FY2026 revenue at $186.3 billion, a 12% year-over-year increase, indicating Walmart's robust growth potential despite declining U.S. consumer sentiment, showcasing its competitive market position.

- Optimistic Analyst Ratings: UBS and TD Cowen maintained 'Buy' ratings with price targets of $147 and $150 respectively, indicating a positive outlook on Walmart's profitability despite challenges like high fuel prices.

- Positive Retail Sentiment: According to Koyfin, 43 analysts have an average 12-month price target of $137.78, suggesting a 3% upside, while retail sentiment on Stocktwits remains 'bullish', indicating strong investor confidence in Walmart's future performance.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy WMT?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on WMT

Wall Street analysts forecast WMT stock price to fall

26 Analyst Rating

25 Buy

1 Hold

0 Sell

Strong Buy

Current: 133.340

Low

119.00

Averages

125.75

High

136.00

Current: 133.340

Low

119.00

Averages

125.75

High

136.00

About WMT

Walmart Inc. is a technology-powered omnichannel retailer. The Company is engaged in the operation of retail and wholesale stores and clubs, as well as eCommerce Websites and mobile applications, located throughout the United States (U.S.), Africa, Canada, Central America, Chile, China, India and Mexico. It operates in three reportable segments: Walmart U.S., Walmart International and Sam's Club U.S. The Walmart U.S. segment includes the Company's mass merchandising concept in the U.S., as well as eCommerce, which includes omni-channel initiatives and certain other business offerings such as advertising services. The Walmart International segment consists of the Company's operations outside of the U.S. through its subsidiaries, as well as eCommerce and omni-channel initiatives. The Sam's Club U.S. segment includes the warehouse membership clubs in the U.S., as well as samsclub.com and omni-channel initiatives.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Walmart's Fiscal Q1 2027 Earnings Preview

- Stock Performance: As of now, Walmart's stock has risen nearly 18% in 2026, recently hitting a 52-week high of $134.69, significantly outperforming the S&P 500's 6% increase, indicating high market expectations for its future performance.

- Revenue Growth: In fiscal Q4 2026, Walmart's revenue grew by 5.6% year-over-year, with global e-commerce sales increasing by 24% and U.S. e-commerce by 27%, while the advertising business surged by 37% globally, driving overall profitability.

- Operating Income Outlook: Although management anticipates that fiscal Q1 2027 operating income growth will be the lowest of the year due to tariff impacts, the projected net sales growth of 3.5% to 4.5% remains noteworthy, especially in high-margin sectors.

- Leadership Transition: New CEO John Furner took over on February 1, and while he has over three decades of experience at Walmart, this leadership change introduces uncertainty, prompting investors to approach the upcoming earnings report with caution.

See More

Walmart Shares Hit Record High Ahead of Earnings

- Record High Stock Price: Walmart (WMT) shares reached $134.71 on Tuesday, climbing 37% over the past 12 months, reflecting strong investor confidence ahead of its upcoming quarterly earnings report.

- Strong Revenue Expectations: Analysts project Q1 FY2026 revenue at $186.3 billion, a 12% year-over-year increase, indicating Walmart's robust growth potential despite declining U.S. consumer sentiment, showcasing its competitive market position.

- Optimistic Analyst Ratings: UBS and TD Cowen maintained 'Buy' ratings with price targets of $147 and $150 respectively, indicating a positive outlook on Walmart's profitability despite challenges like high fuel prices.

- Positive Retail Sentiment: According to Koyfin, 43 analysts have an average 12-month price target of $137.78, suggesting a 3% upside, while retail sentiment on Stocktwits remains 'bullish', indicating strong investor confidence in Walmart's future performance.

See More

Walmart's E-commerce Sales Surge 24% Amidst Strategic Shifts

- E-commerce Growth: Walmart's latest report indicates a 24% year-over-year increase in global e-commerce sales, with U.S. e-commerce sales rising 27%, showcasing the company's significant progress in digital transformation and enhancing its market competitiveness.

- Advertising and Membership Revenue Contribution: The advertising business grew 37% globally, while membership fee revenue increased by 15.1%, with these two high-margin segments together accounting for nearly a third of fourth-quarter operating income, demonstrating Walmart's success in diversifying its revenue streams.

- Operating Income Growth: Walmart's adjusted operating income grew 10.5% in constant currency during the reporting period, significantly outpacing total revenue growth, indicating effective strategies in cost control and efficiency enhancement.

- Cautious Future Outlook: Despite strong business momentum, management anticipates that first-quarter operating income growth will be the lowest of the year, and the transition under the new CEO may introduce uncertainties, prompting investors to adopt a cautious stance.

See More

Walmart vs. Costco: A Competitive Analysis

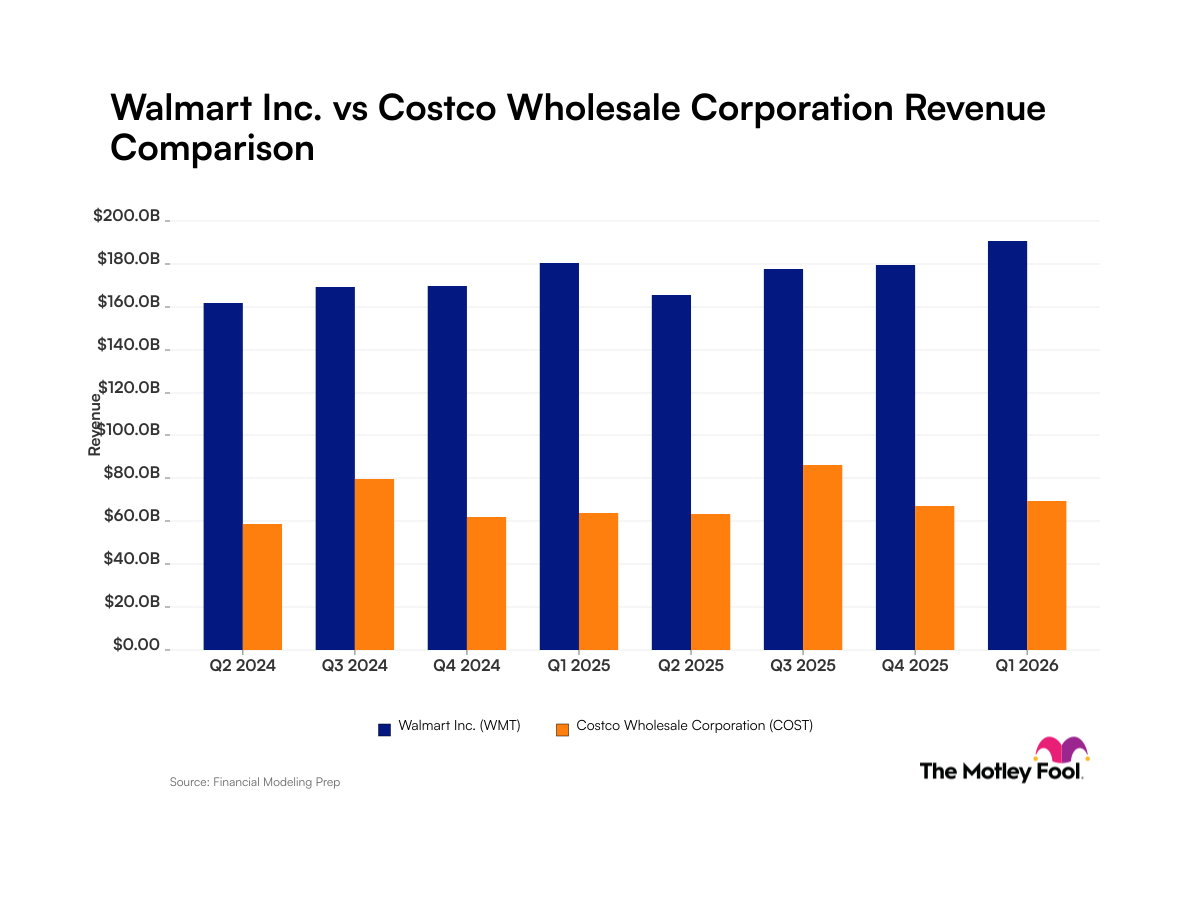

- Revenue Comparison: Walmart reported $161.5 billion in revenue for Q2 2024, while Costco generated $58.5 billion in the same period; despite Costco's impressive 9.2% year-over-year growth, Walmart's scale advantage leads to superior market performance.

- Technology Investments: Walmart is undertaking a massive store remodeling initiative aimed at enhancing customer experience and driving future sales growth, whereas Costco is rolling out membership card scanners nationwide to improve operational efficiency, highlighting their differing technological focuses.

- Net Margin Differences: As of January 2026, Walmart's net income margin stands at 2.3%, slightly lower than Costco's 2.9%; however, Walmart's stock has surged 115% over the past two years, significantly outperforming Costco's 30% return.

- Future Outlook: With increased investments in AI and e-commerce, Walmart's AI shopping assistant Sparky is already driving higher order values, while Costco is also striving to enhance checkout speed and employee productivity through digital initiatives, making technological leverage crucial for both companies in the next five years.

See More

Financial Comparison Analysis of Walmart and Costco

- Revenue Gap Analysis: Walmart generates significantly higher total revenue than Costco across all historical periods, although Costco's recent quarterly sales growth of 9.2% outpaced Walmart's 5.6%, Walmart's scale and revenue advantage have led to superior stock performance over the past two years.

- Technology Investment Trends: Both companies are increasing investments in artificial intelligence to enhance operational efficiency and customer experience, with Walmart's AI shopping assistant Sparky driving higher order values, while Costco focuses on digital investments to improve checkout speed and employee productivity.

- Net Margin Comparison: As of January 31, 2026, Walmart reported a net income margin of 2.3%, while Costco's margin was 2.9% as of February 15, 2026; despite Costco's higher margin, its shareholder returns have lagged behind Walmart's.

- Future Outlook: Investors should monitor how both companies leverage technology to close the revenue gap, with Walmart's remodeling plan and Costco's nationwide rollout of membership card scanners potentially impacting market performance in the coming years.

See More

Walmart Thrives Amid Economic Challenges with Strategic Investments

- Significant Sales Growth: Walmart's sales increased by 4.7% to $174.95 billion in the fiscal year ending January 31, significantly outperforming competitors like Target, which saw a 1.7% decline, and Kroger, which remained flat, demonstrating Walmart's strong appeal during economic hardships.

- Stable Profit Margins: Despite tariff pressures, Walmart maintained an operating margin of 4.2%, attributed to its scale advantages and emerging high-margin revenue streams, such as advertising and membership fees, which accounted for 27% of operating profits, up from 9% in 2021.

- E-commerce Explosion: Walmart's online sales surged by 24% over the past year, rising from $121 billion to $150.4 billion, representing 21.3% of total sales, showcasing its robust performance in e-commerce, surpassing Amazon's 9% growth.

- Competitive Market Advantage: Walmart's 4,600 U.S. stores serve as distribution centers, giving it an edge in grocery sales over Amazon, particularly in cold chain distribution, enhancing market efficiency and customer satisfaction.

See More

Walmart's Fiscal Q1 2027 Earnings Preview

- Stock Performance: As of now, Walmart's stock has risen nearly 18% in 2026, recently hitting a 52-week high of $134.69, significantly outperforming the S&P 500's 6% increase, indicating high market expectations for its future performance.

- Revenue Growth: In fiscal Q4 2026, Walmart's revenue grew by 5.6% year-over-year, with global e-commerce sales increasing by 24% and U.S. e-commerce by 27%, while the advertising business surged by 37% globally, driving overall profitability.

- Operating Income Outlook: Although management anticipates that fiscal Q1 2027 operating income growth will be the lowest of the year due to tariff impacts, the projected net sales growth of 3.5% to 4.5% remains noteworthy, especially in high-margin sectors.

- Leadership Transition: New CEO John Furner took over on February 1, and while he has over three decades of experience at Walmart, this leadership change introduces uncertainty, prompting investors to approach the upcoming earnings report with caution.

See More

Walmart Shares Hit Record High Ahead of Earnings

- Record High Stock Price: Walmart (WMT) shares reached $134.71 on Tuesday, climbing 37% over the past 12 months, reflecting strong investor confidence ahead of its upcoming quarterly earnings report.

- Strong Revenue Expectations: Analysts project Q1 FY2026 revenue at $186.3 billion, a 12% year-over-year increase, indicating Walmart's robust growth potential despite declining U.S. consumer sentiment, showcasing its competitive market position.

- Optimistic Analyst Ratings: UBS and TD Cowen maintained 'Buy' ratings with price targets of $147 and $150 respectively, indicating a positive outlook on Walmart's profitability despite challenges like high fuel prices.

- Positive Retail Sentiment: According to Koyfin, 43 analysts have an average 12-month price target of $137.78, suggesting a 3% upside, while retail sentiment on Stocktwits remains 'bullish', indicating strong investor confidence in Walmart's future performance.

See More

Walmart's E-commerce Sales Surge 24% Amidst Strategic Shifts

- E-commerce Growth: Walmart's latest report indicates a 24% year-over-year increase in global e-commerce sales, with U.S. e-commerce sales rising 27%, showcasing the company's significant progress in digital transformation and enhancing its market competitiveness.

- Advertising and Membership Revenue Contribution: The advertising business grew 37% globally, while membership fee revenue increased by 15.1%, with these two high-margin segments together accounting for nearly a third of fourth-quarter operating income, demonstrating Walmart's success in diversifying its revenue streams.

- Operating Income Growth: Walmart's adjusted operating income grew 10.5% in constant currency during the reporting period, significantly outpacing total revenue growth, indicating effective strategies in cost control and efficiency enhancement.

- Cautious Future Outlook: Despite strong business momentum, management anticipates that first-quarter operating income growth will be the lowest of the year, and the transition under the new CEO may introduce uncertainties, prompting investors to adopt a cautious stance.

See More

Walmart vs. Costco: A Competitive Analysis

- Revenue Comparison: Walmart reported $161.5 billion in revenue for Q2 2024, while Costco generated $58.5 billion in the same period; despite Costco's impressive 9.2% year-over-year growth, Walmart's scale advantage leads to superior market performance.

- Technology Investments: Walmart is undertaking a massive store remodeling initiative aimed at enhancing customer experience and driving future sales growth, whereas Costco is rolling out membership card scanners nationwide to improve operational efficiency, highlighting their differing technological focuses.

- Net Margin Differences: As of January 2026, Walmart's net income margin stands at 2.3%, slightly lower than Costco's 2.9%; however, Walmart's stock has surged 115% over the past two years, significantly outperforming Costco's 30% return.

- Future Outlook: With increased investments in AI and e-commerce, Walmart's AI shopping assistant Sparky is already driving higher order values, while Costco is also striving to enhance checkout speed and employee productivity through digital initiatives, making technological leverage crucial for both companies in the next five years.

See More

Financial Comparison Analysis of Walmart and Costco

- Revenue Gap Analysis: Walmart generates significantly higher total revenue than Costco across all historical periods, although Costco's recent quarterly sales growth of 9.2% outpaced Walmart's 5.6%, Walmart's scale and revenue advantage have led to superior stock performance over the past two years.

- Technology Investment Trends: Both companies are increasing investments in artificial intelligence to enhance operational efficiency and customer experience, with Walmart's AI shopping assistant Sparky driving higher order values, while Costco focuses on digital investments to improve checkout speed and employee productivity.

- Net Margin Comparison: As of January 31, 2026, Walmart reported a net income margin of 2.3%, while Costco's margin was 2.9% as of February 15, 2026; despite Costco's higher margin, its shareholder returns have lagged behind Walmart's.

- Future Outlook: Investors should monitor how both companies leverage technology to close the revenue gap, with Walmart's remodeling plan and Costco's nationwide rollout of membership card scanners potentially impacting market performance in the coming years.

See More

Walmart Thrives Amid Economic Challenges with Strategic Investments

- Significant Sales Growth: Walmart's sales increased by 4.7% to $174.95 billion in the fiscal year ending January 31, significantly outperforming competitors like Target, which saw a 1.7% decline, and Kroger, which remained flat, demonstrating Walmart's strong appeal during economic hardships.

- Stable Profit Margins: Despite tariff pressures, Walmart maintained an operating margin of 4.2%, attributed to its scale advantages and emerging high-margin revenue streams, such as advertising and membership fees, which accounted for 27% of operating profits, up from 9% in 2021.

- E-commerce Explosion: Walmart's online sales surged by 24% over the past year, rising from $121 billion to $150.4 billion, representing 21.3% of total sales, showcasing its robust performance in e-commerce, surpassing Amazon's 9% growth.

- Competitive Market Advantage: Walmart's 4,600 U.S. stores serve as distribution centers, giving it an edge in grocery sales over Amazon, particularly in cold chain distribution, enhancing market efficiency and customer satisfaction.

See More