Valuation Analysis of Bristol Myers Squibb Stock

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 3 days ago

0mins

Source: Fool

- Valuation Appeal: Bristol Myers Squibb (BMS) has a forward P/E ratio of 9.4, significantly lower than the healthcare sector average of 17.3, indicating its stock may attract value investors, especially with a market cap of around $120 billion.

- Growth Prospects Challenges: Despite BMS's appealing growth potential, the looming patent cliff poses a significant risk for revenue decline in the coming years, particularly as its top drugs, Eliquis and Opdivo, face patent expiration in 2028, which could severely impact total revenue.

- Dividend Attraction: With a forward dividend yield of 4.3% and a record of increasing dividends for 17 consecutive years, BMS remains attractive to income investors, who may prioritize steady cash flow over growth concerns.

- Competitor Comparison: Compared to competitors like Pfizer (PFE) and AbbVie, BMS's lower valuation may not be enough to offset the competitive pressure, as AbbVie appears more attractively valued when considering growth projections over the next five years.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy BMY?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on BMY

Wall Street analysts forecast BMY stock price to fall

20 Analyst Rating

8 Buy

11 Hold

1 Sell

Moderate Buy

Current: 57.590

Low

37.00

Averages

55.86

High

68.00

Current: 57.590

Low

37.00

Averages

55.86

High

68.00

About BMY

Bristol-Myers Squibb Company is a global biopharmaceutical company. It is engaged in the discovery, development, and delivery of transformational medicines for patients facing serious diseases in areas: oncology, hematology, immunology, cardiovascular, neuroscience and other areas. Its growth portfolio includes Opdivo (nivolumab), Opdivo Qvantig (nivolumab and hyaluronidase-nvhy), Orencia (abatacept), Yervoy (ipilimumab), Reblozyl (luspatercept-aamt), Breyanzi (lisocabtagene maraleucel), Opdualag (nivolumab and relatlimab-rmbw), Camzyos (mavacamten), Zeposia (ozanimod), Abecma (idecabtagene vicleucel), Sotyktu (deucravacitinib), Krazati (adagrasib), and Cobenfy (xanomeline and trospium chloride). Its other growth products include Augtyro, Onureg, Inrebic, Nulojix, and Empliciti. Its legacy portfolio includes Eliquis (apixaban), Revlimid (lenalidomide), Pomalyst/Imnovid (pomalidomide), Sprycel (dasatinib), and Abraxane (paclitaxel albumin-bound particles for injectable suspension).

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Bristol-Myers Squibb Expected to Report Decline in Q1 Earnings and Revenue

- Earnings Decline Expected: Bristol-Myers Squibb is projected to report a 21.1% drop in earnings to $1.42 per share and a 2.5% decrease in revenue to $10.92 billion in its upcoming Q1 results on April 30, indicating significant market challenges.

- Estimate Revision Trends: Over the past three months, EPS estimates have seen 4 upward revisions and 7 downward adjustments, while revenue estimates experienced 7 upward revisions and 1 downward move, reflecting analyst uncertainty regarding the company's future performance.

- Analyst Rating Upgrade: Ahead of the earnings report, analyst Terry Chrisomalis assigned a Strong Buy rating to the stock, citing robust growth portfolio expansion and strategic pipeline execution, which bolsters market confidence in the company.

- Growth Potential Realized: Chrisomalis noted that nearly 60% of Bristol-Myers Squibb's total revenues now come from its growth portfolio, suggesting that the company is on the right track to meet its strategic goal of mitigating the impact of key product patent expirations.

See More

Bristol-Myers Squibb Q1 Earnings Beat Expectations

- Strong Financial Performance: Bristol-Myers Squibb reported $11.5 billion in revenue for Q1 2026, reflecting a ~3% year-over-year growth that exceeded market expectations by $580 million, demonstrating the company's financial resilience amid challenges.

- Growth Portfolio Outperformance: The growth portfolio contributed $6.2 billion in revenue with ~12% year-over-year growth, driven by cancer therapy Opdivo and rheumatoid arthritis drug Orencia generating $2.1 billion and $818 million, respectively, indicating strong market acceptance of new product lines.

- Legacy Product Decline: Despite the strong performance of the growth portfolio, the legacy product line contracted ~6% year-over-year, generating $5.3 billion, highlighting the impact of generics on other products and the need for a faster transition to maintain competitive positioning.

- Reaffirmed Full-Year Outlook: The company reaffirmed its full-year revenue guidance of $46.0 billion to $47.5 billion and adjusted EPS of $6.05 to $6.35, aligning with market consensus, reflecting management's confidence in future performance.

See More

Bristol-Myers Squibb Exceeds Earnings Expectations

- Strong Earnings Report: Bristol-Myers Squibb reported a non-GAAP EPS of $1.58 for Q1, surpassing expectations by $0.16, which demonstrates robust profitability and boosts investor confidence.

- Revenue Growth: The company achieved $11.5 billion in revenue for the first quarter, exceeding forecasts by $580 million, indicating sustained growth in its product portfolio and reinforcing its market position.

- Growth Potential: Despite facing patent expiration challenges, Bristol-Myers Squibb's growth portfolio remains undervalued by the market, with analysts suggesting that upcoming milestones could significantly enhance the company's prospects.

- Market Reaction: The better-than-expected earnings report may prompt investors to reassess the stock's value, likely resulting in a positive impact on the share price and further enhancing the company's competitiveness in the biopharmaceutical sector.

See More

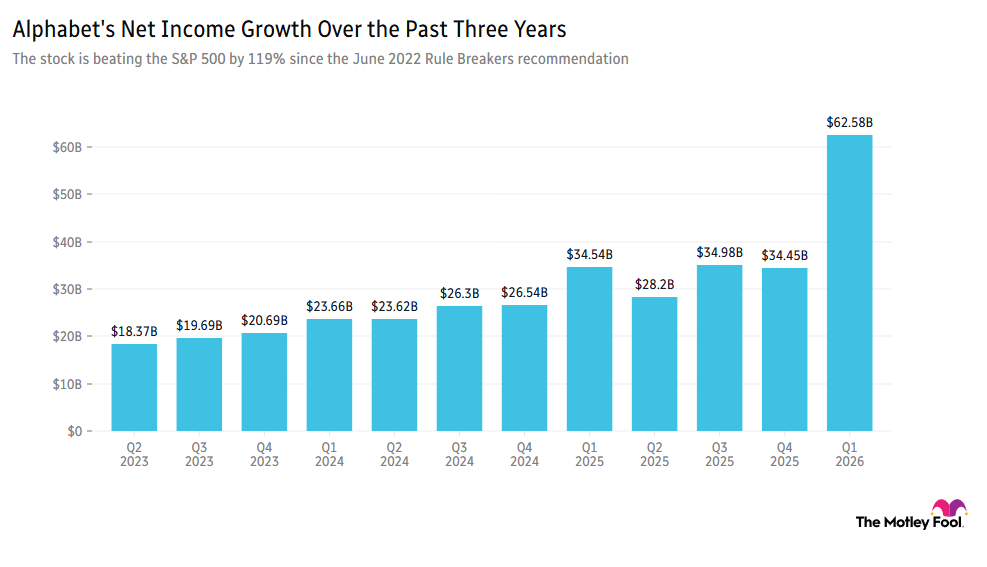

Alphabet CEO Highlights Significant AI Investment Payoff

- Earnings Beat Expectations: Alphabet's Q1 earnings report revealed a 63% year-over-year increase in cloud revenue and an 81% rise in net income, with CEO Sundar Pichai stating that the full-stack approach to AI investments is driving strong performance.

- Consumer Subscription Surge: The adoption of the Gemini app reached an all-time high, indicating robust demand for consumer subscription AI plans, with analyst Sanmeet Deo noting that Alphabet's substantial investments in AI are translating into impressive financial returns, boosting investor confidence.

- Positive Market Reaction: Ahead of the earnings release, Alphabet's stock surged over 7%, reflecting investor optimism about the company's future, particularly its potential to dominate the AI revolution.

- Clear Strategic Positioning: Analysts believe that Alphabet's AI investments not only enhance current performance but also lay the groundwork for future market competition, ensuring the company's leadership in the rapidly evolving AI landscape.

See More

Bristol Myers Squibb Reports Q1 2026 Financial Results

- Earnings Release: Bristol Myers Squibb reported its Q1 2026 financial results on April 30, 2026, highlighting the company's ongoing commitment to innovative drug development, although specific financial metrics have yet to be disclosed, keeping the market attentive to its future performance.

- Investor Call: The company will host a conference call for analysts and investors at 8:00 a.m. ET on the same day as the earnings release, where executives are expected to discuss financial results and future outlook, enhancing communication with investors.

- Webcast Replay: A replay of the earnings call will be available approximately three hours after the conclusion of the meeting on the company's Investor Relations website, ensuring that investors who could not participate live can access key information.

- Corporate Mission: Bristol Myers Squibb is dedicated to transforming patients' lives through science, focusing on discovering, developing, and delivering innovative medicines to help patients overcome serious diseases, showcasing its strategic positioning in the biopharmaceutical sector.

See More

Bristol-Myers Squibb Q1 Earnings Exceed Expectations

- Earnings Beat: Bristol-Myers Squibb reported a Q1 non-GAAP EPS of $1.58, exceeding expectations by $0.16, reflecting strong profitability that boosts investor confidence.

- Revenue Growth: The company achieved $11.5 billion in revenue for Q1, a 2.7% year-over-year increase, surpassing market expectations by $580 million, indicating sustained demand and competitiveness in its product offerings.

- Guidance Reaffirmed: Bristol-Myers Squibb reaffirmed its 2026 financial guidance with projected revenues of $46 billion to $47.5 billion, compared to a consensus of $47.12 billion, demonstrating confidence in future growth.

- EPS Outlook: The company anticipates a non-GAAP EPS range of $6.05 to $6.35 for 2026, against a consensus of $6.26, highlighting its potential for profitability and stability moving forward.

See More

Bristol-Myers Squibb Expected to Report Decline in Q1 Earnings and Revenue

- Earnings Decline Expected: Bristol-Myers Squibb is projected to report a 21.1% drop in earnings to $1.42 per share and a 2.5% decrease in revenue to $10.92 billion in its upcoming Q1 results on April 30, indicating significant market challenges.

- Estimate Revision Trends: Over the past three months, EPS estimates have seen 4 upward revisions and 7 downward adjustments, while revenue estimates experienced 7 upward revisions and 1 downward move, reflecting analyst uncertainty regarding the company's future performance.

- Analyst Rating Upgrade: Ahead of the earnings report, analyst Terry Chrisomalis assigned a Strong Buy rating to the stock, citing robust growth portfolio expansion and strategic pipeline execution, which bolsters market confidence in the company.

- Growth Potential Realized: Chrisomalis noted that nearly 60% of Bristol-Myers Squibb's total revenues now come from its growth portfolio, suggesting that the company is on the right track to meet its strategic goal of mitigating the impact of key product patent expirations.

See More

Bristol-Myers Squibb Q1 Earnings Beat Expectations

- Strong Financial Performance: Bristol-Myers Squibb reported $11.5 billion in revenue for Q1 2026, reflecting a ~3% year-over-year growth that exceeded market expectations by $580 million, demonstrating the company's financial resilience amid challenges.

- Growth Portfolio Outperformance: The growth portfolio contributed $6.2 billion in revenue with ~12% year-over-year growth, driven by cancer therapy Opdivo and rheumatoid arthritis drug Orencia generating $2.1 billion and $818 million, respectively, indicating strong market acceptance of new product lines.

- Legacy Product Decline: Despite the strong performance of the growth portfolio, the legacy product line contracted ~6% year-over-year, generating $5.3 billion, highlighting the impact of generics on other products and the need for a faster transition to maintain competitive positioning.

- Reaffirmed Full-Year Outlook: The company reaffirmed its full-year revenue guidance of $46.0 billion to $47.5 billion and adjusted EPS of $6.05 to $6.35, aligning with market consensus, reflecting management's confidence in future performance.

See More

Bristol-Myers Squibb Exceeds Earnings Expectations

- Strong Earnings Report: Bristol-Myers Squibb reported a non-GAAP EPS of $1.58 for Q1, surpassing expectations by $0.16, which demonstrates robust profitability and boosts investor confidence.

- Revenue Growth: The company achieved $11.5 billion in revenue for the first quarter, exceeding forecasts by $580 million, indicating sustained growth in its product portfolio and reinforcing its market position.

- Growth Potential: Despite facing patent expiration challenges, Bristol-Myers Squibb's growth portfolio remains undervalued by the market, with analysts suggesting that upcoming milestones could significantly enhance the company's prospects.

- Market Reaction: The better-than-expected earnings report may prompt investors to reassess the stock's value, likely resulting in a positive impact on the share price and further enhancing the company's competitiveness in the biopharmaceutical sector.

See More

Alphabet CEO Highlights Significant AI Investment Payoff

- Earnings Beat Expectations: Alphabet's Q1 earnings report revealed a 63% year-over-year increase in cloud revenue and an 81% rise in net income, with CEO Sundar Pichai stating that the full-stack approach to AI investments is driving strong performance.

- Consumer Subscription Surge: The adoption of the Gemini app reached an all-time high, indicating robust demand for consumer subscription AI plans, with analyst Sanmeet Deo noting that Alphabet's substantial investments in AI are translating into impressive financial returns, boosting investor confidence.

- Positive Market Reaction: Ahead of the earnings release, Alphabet's stock surged over 7%, reflecting investor optimism about the company's future, particularly its potential to dominate the AI revolution.

- Clear Strategic Positioning: Analysts believe that Alphabet's AI investments not only enhance current performance but also lay the groundwork for future market competition, ensuring the company's leadership in the rapidly evolving AI landscape.

See More

Bristol Myers Squibb Reports Q1 2026 Financial Results

- Earnings Release: Bristol Myers Squibb reported its Q1 2026 financial results on April 30, 2026, highlighting the company's ongoing commitment to innovative drug development, although specific financial metrics have yet to be disclosed, keeping the market attentive to its future performance.

- Investor Call: The company will host a conference call for analysts and investors at 8:00 a.m. ET on the same day as the earnings release, where executives are expected to discuss financial results and future outlook, enhancing communication with investors.

- Webcast Replay: A replay of the earnings call will be available approximately three hours after the conclusion of the meeting on the company's Investor Relations website, ensuring that investors who could not participate live can access key information.

- Corporate Mission: Bristol Myers Squibb is dedicated to transforming patients' lives through science, focusing on discovering, developing, and delivering innovative medicines to help patients overcome serious diseases, showcasing its strategic positioning in the biopharmaceutical sector.

See More

Bristol-Myers Squibb Q1 Earnings Exceed Expectations

- Earnings Beat: Bristol-Myers Squibb reported a Q1 non-GAAP EPS of $1.58, exceeding expectations by $0.16, reflecting strong profitability that boosts investor confidence.

- Revenue Growth: The company achieved $11.5 billion in revenue for Q1, a 2.7% year-over-year increase, surpassing market expectations by $580 million, indicating sustained demand and competitiveness in its product offerings.

- Guidance Reaffirmed: Bristol-Myers Squibb reaffirmed its 2026 financial guidance with projected revenues of $46 billion to $47.5 billion, compared to a consensus of $47.12 billion, demonstrating confidence in future growth.

- EPS Outlook: The company anticipates a non-GAAP EPS range of $6.05 to $6.35 for 2026, against a consensus of $6.26, highlighting its potential for profitability and stability moving forward.

See More