The Rise of AI Infrastructure

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Apr 30 2026

0mins

Should l Buy VRT?

Source: NASDAQ.COM

- Liquid Cooling Solutions: Vertiv's liquid cooling solutions are nearly twice as efficient as traditional air cooling, with the global data center liquid cooling market expected to grow at an average annual rate of over 18% through 2035, highlighting its critical role in AI data centers.

- Digital Transformation: DigitalOcean served over 640,000 paying customers last year, generating $900 million in revenue, a 15% increase, with revenue from large clients growing by 106%, indicating its strong competitive position in the AI infrastructure market.

- Power Self-Sufficiency: Hut 8 is transforming its Bitcoin mining infrastructure into AI data centers, managing over 1,000 megawatts of power production and planning to build an additional 300 megawatts, aiming to reduce reliance on utility companies and enhance self-sufficiency.

- Optimistic Industry Outlook: According to Technavio, the global AI infrastructure market is expected to grow at an average annual rate of nearly 25% through 2030, and despite challenges, the demand for AI technology remains strong, driving continued growth for related companies.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy VRT?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on VRT

Wall Street analysts forecast VRT stock price to fall

17 Analyst Rating

15 Buy

2 Hold

0 Sell

Strong Buy

Current: 340.010

Low

195.00

Averages

206.07

High

230.00

Current: 340.010

Low

195.00

Averages

206.07

High

230.00

About VRT

Vertiv Holdings Co. provides mission-critical digital infrastructure technologies and lifecycle services primarily for data centers, communication networks, and commercial and industrial environments. The Company operates in three business segments: the Americas; Asia Pacific, and Europe, Middle East & Africa. The Company's offerings include alternate current (AC) and direct current (DC) power management, thermal management, low/medium voltage switchgear, busbar, air cooled and liquid cooled thermal management products, integrated modular solutions, racks, single phase UPS, rack power distribution, rack thermal systems, configurable integrated solutions, energy storage solutions, hardware, software for managing IT equipment, management systems for monitoring and controlling digital infrastructure, and services. It also provides preventative maintenance, acceptance testing, engineering and consulting, remote monitoring, training, spare parts, specialized fluid management, and others.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

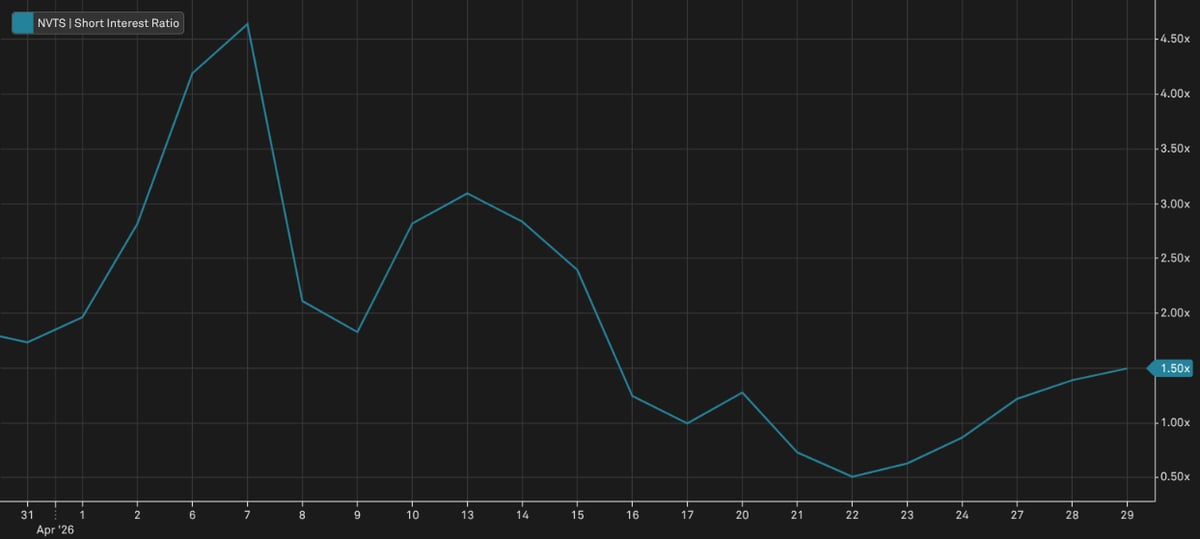

Navitas Semiconductor Stock Soars 121% Amid AI Investment Surge

- Stock Surge: Navitas Semiconductor's stock has surged 121% in 2026, with an impressive 88.1% increase in April alone, reflecting strong market confidence in its potential within the AI investment cycle, particularly as short sellers were forced to cover their positions, driving the price sharply higher.

- Market Trends: The Philadelphia Semiconductor Index rose 38% in April, indicating ongoing robust demand for AI-related investments, and Navitas, as a leading manufacturer of gallium nitride and silicon carbide chips, is well-positioned to benefit from this trend, with management shifting focus towards data centers and high-performance computing.

- Technological Innovation: In mid-March, Navitas announced its latest power delivery board capable of direct conversion from 800 V to 6 V, a critical component of the 800 VDC data center technology being developed by Nvidia, further solidifying its position in the industry.

- Profitability Outlook: With the continued growth in data center investments, Navitas could potentially become profitable and cash-generative in the coming years, especially as companies like GE Vernova raise their full-year guidance, creating optimistic expectations for Navitas's future performance.

See More

Vertiv Stock Soars 121.5% Amid Strong AI Data Center Demand

- Significant Stock Surge: Vertiv's stock has surged 121.5% in 2026, with a remarkable 31.1% increase in April alone, reflecting strong investor confidence in its role within the AI data center infrastructure sector.

- Earnings Beat Expectations: The company raised its full-year net sales guidance to $13.5 billion to $14 billion from a previous range of $13.25 billion to $13.75 billion, indicating robust business growth momentum.

- Increased Profit Forecast: The adjusted full-year earnings per share (EPS) expectation has risen from $6.02 to $6.35, showcasing the company's optimistic outlook for the second half of the year, with the CEO highlighting sustained strong demand for data centers.

- Collaboration with Nvidia: Vertiv's partnership with Nvidia is advancing the development of 800 VDC data center power infrastructure, focusing on power and cooling solutions compatible with AI architecture, thereby solidifying its position in the rapidly evolving AI market.

See More

Vertiv Upgrades Guidance Amid Strong AI Demand

- Guidance Upgrade: Vertiv's first-quarter earnings exceeded expectations, prompting an upgrade in full-year guidance, which indicates robust growth in data center demand, with the CEO emphasizing a focus on capacity expansion and supply chain capabilities.

- Stock Surge: Vertiv's stock has skyrocketed by 121.5% in 2026, with a 31.1% increase in April alone, reflecting optimistic market sentiment towards AI data center infrastructure and rising investor expectations for long-term growth.

- Strategic Partnership: The partnership with Nvidia strengthens Vertiv's role in developing power and cooling solutions compatible with Nvidia's AI architecture, highlighting the company's critical position in AI infrastructure development.

- Improving Market Conditions: With companies like GE Vernova reporting increased demand for gas turbines, the spending environment for AI data centers is improving, driving stock prices higher for companies like Vertiv and indicating signs of industry recovery.

See More

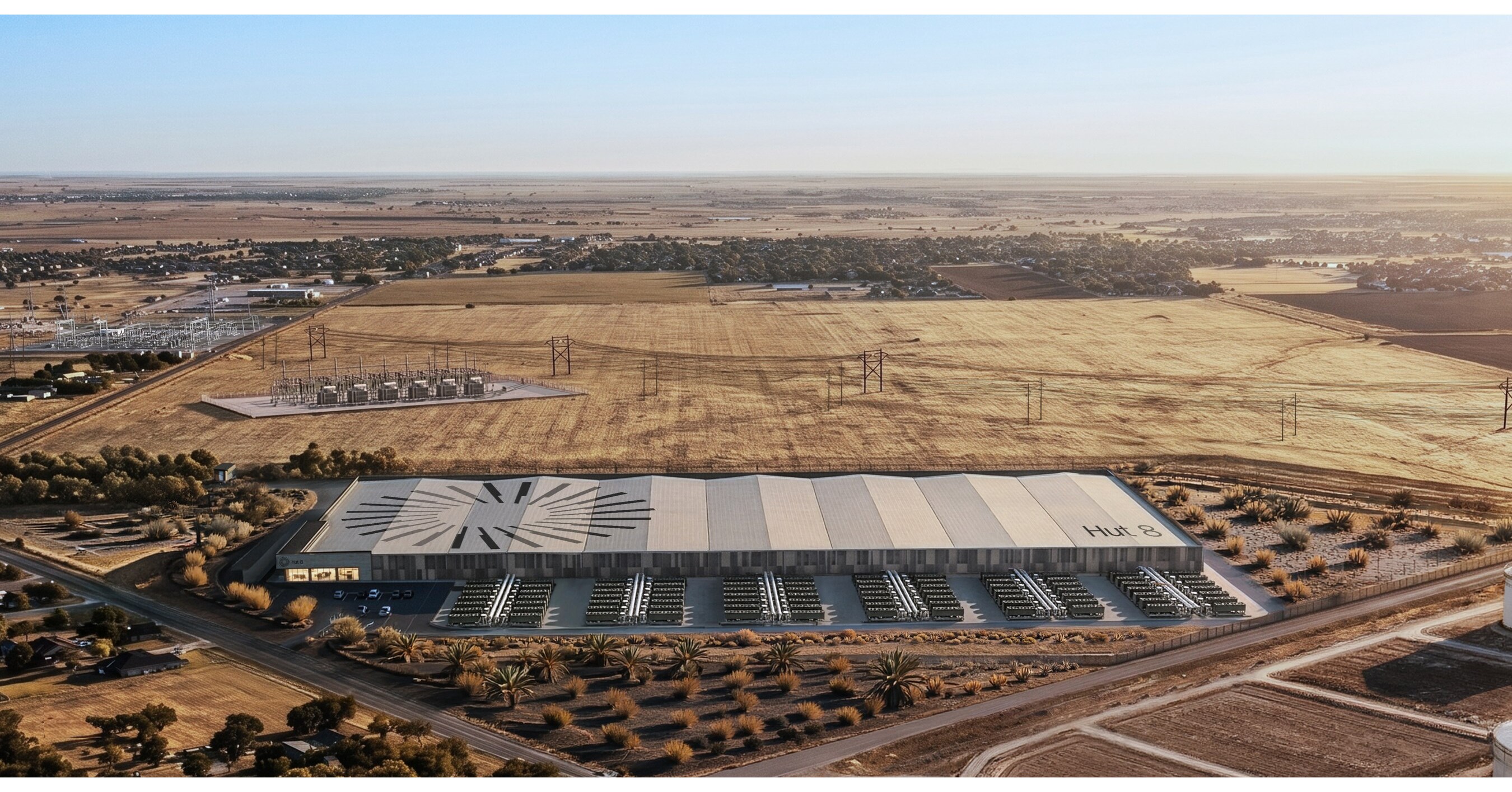

Hut 8 Signs $9.8 Billion Lease for AI Data Center

- Long-Term Lease Agreement: Hut 8 has signed a 15-year lease worth $9.8 billion with an undisclosed tenant, indicating rising demand for AI model infrastructure and expected future revenue growth for the company.

- Capacity Expansion: The agreement covers 352 megawatts of initial project capacity, increasing Hut 8's total contracted AI data center capacity to 597 megawatts and raising the total contract value to approximately $16.8 billion, showcasing the company's strong growth potential in the AI sector.

- Project Construction Timeline: The project, located in Nueces County, Texas, is expected to connect power in early 2027, with the first building scheduled for completion later that year, indicating Hut 8's strategic positioning to meet the growing computing and energy needs of AI firms.

- Strategic Partnerships: The project is being built in collaboration with partners including American Electric Power, Vertiv, and Jacobs, utilizing Nvidia's latest data center systems, reflecting intensified competition in AI infrastructure and Hut 8's proactive expansion in the market.

See More

Hut 8 Signs $25.1 Billion Lease with High-Investment-Grade Tenant

- Significant Lease Value: Hut 8's 15-year lease with a high-investment-grade tenant is valued at $9.8 billion, potentially reaching $25.1 billion if all renewal options are exercised, significantly enhancing the company's financial stability and market competitiveness.

- Data Center Expansion: This transaction increases Hut 8's total contracted AI data center capacity to 597 MW, with an aggregate base-term contract value of approximately $16.8 billion, and an expected annual net operating income of about $1.1 billion, further solidifying its leadership in AI infrastructure.

- Flexible Development Model: Hut 8's power-first development model repositioned the site originally designed for American Bitcoin Corp. to AI infrastructure, showcasing the company's flexibility and innovative capacity in responding to evolving market demands.

- Strategic Partnerships: Hut 8 collaborates with top-tier partners like NVIDIA, Jacobs, and Vertiv to develop Beacon Point, ensuring efficient execution in technology, engineering, and critical systems delivery, thereby enhancing the company's market reputation and execution capabilities.

See More

Hut 8 Signs $9.8 Billion Lease with High-Investment-Grade Tenant

- Lease Scale: Hut 8 has signed a 15-year lease valued at $9.8 billion with a high-investment-grade tenant for 352 MW of IT capacity, which is expected to significantly enhance the company's revenue streams and market position.

- Data Center Expansion: This transaction increases Hut 8's total contracted AI data center capacity to 597 MW, with an aggregate contract value of approximately $16.8 billion, indicating strong performance in the rapidly growing AI infrastructure market.

- Technical Collaboration: Hut 8 will deliver a 352 MW AI factory designed to NVIDIA's DSX reference architecture, showcasing the company's technical capabilities and market adaptability in high-performance computing, likely attracting more high-end clients.

- Sustainability Strategy: The initial delivery of the project is expected in Q3 2027, and Hut 8 ensures efficient execution and long-term sustainability through collaboration with Tier 1 partners, further solidifying its leadership position in the energy infrastructure sector.

See More

Navitas Semiconductor Stock Soars 121% Amid AI Investment Surge

- Stock Surge: Navitas Semiconductor's stock has surged 121% in 2026, with an impressive 88.1% increase in April alone, reflecting strong market confidence in its potential within the AI investment cycle, particularly as short sellers were forced to cover their positions, driving the price sharply higher.

- Market Trends: The Philadelphia Semiconductor Index rose 38% in April, indicating ongoing robust demand for AI-related investments, and Navitas, as a leading manufacturer of gallium nitride and silicon carbide chips, is well-positioned to benefit from this trend, with management shifting focus towards data centers and high-performance computing.

- Technological Innovation: In mid-March, Navitas announced its latest power delivery board capable of direct conversion from 800 V to 6 V, a critical component of the 800 VDC data center technology being developed by Nvidia, further solidifying its position in the industry.

- Profitability Outlook: With the continued growth in data center investments, Navitas could potentially become profitable and cash-generative in the coming years, especially as companies like GE Vernova raise their full-year guidance, creating optimistic expectations for Navitas's future performance.

See More

Vertiv Stock Soars 121.5% Amid Strong AI Data Center Demand

- Significant Stock Surge: Vertiv's stock has surged 121.5% in 2026, with a remarkable 31.1% increase in April alone, reflecting strong investor confidence in its role within the AI data center infrastructure sector.

- Earnings Beat Expectations: The company raised its full-year net sales guidance to $13.5 billion to $14 billion from a previous range of $13.25 billion to $13.75 billion, indicating robust business growth momentum.

- Increased Profit Forecast: The adjusted full-year earnings per share (EPS) expectation has risen from $6.02 to $6.35, showcasing the company's optimistic outlook for the second half of the year, with the CEO highlighting sustained strong demand for data centers.

- Collaboration with Nvidia: Vertiv's partnership with Nvidia is advancing the development of 800 VDC data center power infrastructure, focusing on power and cooling solutions compatible with AI architecture, thereby solidifying its position in the rapidly evolving AI market.

See More

Vertiv Upgrades Guidance Amid Strong AI Demand

- Guidance Upgrade: Vertiv's first-quarter earnings exceeded expectations, prompting an upgrade in full-year guidance, which indicates robust growth in data center demand, with the CEO emphasizing a focus on capacity expansion and supply chain capabilities.

- Stock Surge: Vertiv's stock has skyrocketed by 121.5% in 2026, with a 31.1% increase in April alone, reflecting optimistic market sentiment towards AI data center infrastructure and rising investor expectations for long-term growth.

- Strategic Partnership: The partnership with Nvidia strengthens Vertiv's role in developing power and cooling solutions compatible with Nvidia's AI architecture, highlighting the company's critical position in AI infrastructure development.

- Improving Market Conditions: With companies like GE Vernova reporting increased demand for gas turbines, the spending environment for AI data centers is improving, driving stock prices higher for companies like Vertiv and indicating signs of industry recovery.

See More

Hut 8 Signs $9.8 Billion Lease for AI Data Center

- Long-Term Lease Agreement: Hut 8 has signed a 15-year lease worth $9.8 billion with an undisclosed tenant, indicating rising demand for AI model infrastructure and expected future revenue growth for the company.

- Capacity Expansion: The agreement covers 352 megawatts of initial project capacity, increasing Hut 8's total contracted AI data center capacity to 597 megawatts and raising the total contract value to approximately $16.8 billion, showcasing the company's strong growth potential in the AI sector.

- Project Construction Timeline: The project, located in Nueces County, Texas, is expected to connect power in early 2027, with the first building scheduled for completion later that year, indicating Hut 8's strategic positioning to meet the growing computing and energy needs of AI firms.

- Strategic Partnerships: The project is being built in collaboration with partners including American Electric Power, Vertiv, and Jacobs, utilizing Nvidia's latest data center systems, reflecting intensified competition in AI infrastructure and Hut 8's proactive expansion in the market.

See More

Hut 8 Signs $25.1 Billion Lease with High-Investment-Grade Tenant

- Significant Lease Value: Hut 8's 15-year lease with a high-investment-grade tenant is valued at $9.8 billion, potentially reaching $25.1 billion if all renewal options are exercised, significantly enhancing the company's financial stability and market competitiveness.

- Data Center Expansion: This transaction increases Hut 8's total contracted AI data center capacity to 597 MW, with an aggregate base-term contract value of approximately $16.8 billion, and an expected annual net operating income of about $1.1 billion, further solidifying its leadership in AI infrastructure.

- Flexible Development Model: Hut 8's power-first development model repositioned the site originally designed for American Bitcoin Corp. to AI infrastructure, showcasing the company's flexibility and innovative capacity in responding to evolving market demands.

- Strategic Partnerships: Hut 8 collaborates with top-tier partners like NVIDIA, Jacobs, and Vertiv to develop Beacon Point, ensuring efficient execution in technology, engineering, and critical systems delivery, thereby enhancing the company's market reputation and execution capabilities.

See More

Hut 8 Signs $9.8 Billion Lease with High-Investment-Grade Tenant

- Lease Scale: Hut 8 has signed a 15-year lease valued at $9.8 billion with a high-investment-grade tenant for 352 MW of IT capacity, which is expected to significantly enhance the company's revenue streams and market position.

- Data Center Expansion: This transaction increases Hut 8's total contracted AI data center capacity to 597 MW, with an aggregate contract value of approximately $16.8 billion, indicating strong performance in the rapidly growing AI infrastructure market.

- Technical Collaboration: Hut 8 will deliver a 352 MW AI factory designed to NVIDIA's DSX reference architecture, showcasing the company's technical capabilities and market adaptability in high-performance computing, likely attracting more high-end clients.

- Sustainability Strategy: The initial delivery of the project is expected in Q3 2027, and Hut 8 ensures efficient execution and long-term sustainability through collaboration with Tier 1 partners, further solidifying its leadership position in the energy infrastructure sector.

See More