Stitch Fix Q2 Earnings Beat Expectations

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 3 hours ago

0mins

Should l Buy SFIX?

Source: seekingalpha

- Earnings Highlights: Stitch Fix reported a Q2 GAAP EPS of -$0.02, beating expectations by $0.03, with revenue of $341.3 million reflecting a 9.4% year-over-year increase, surpassing estimates by $8.51 million, indicating resilience and growth potential in the market.

- Future Outlook: The company projects Q3 2026 net revenue between $330 million and $335 million, representing a year-over-year growth of 1.5% to 3.1%, with adjusted EBITDA expected to range from $7 million to $10 million, showcasing confidence in future growth.

- Annual Forecast: Stitch Fix has updated its financial outlook for FY 2026, anticipating net revenue between $1.33 billion and $1.35 billion, with a year-over-year growth of 5% to 6.5%, and adjusted EBITDA projected at $42 million to $50 million, reflecting ongoing improvements in revenue and profitability.

- Cash Flow Position: The company expects a gross margin for FY 2026 between 43% and 44%, with advertising expenses as a percentage of revenue between 9% and 10%, and anticipates being free cash flow positive for the full year, indicating robust financial management.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy SFIX?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on SFIX

Wall Street analysts forecast SFIX stock price to rise

4 Analyst Rating

1 Buy

2 Hold

1 Sell

Hold

Current: 3.465

Low

3.00

Averages

5.00

High

6.00

Current: 3.465

Low

3.00

Averages

5.00

High

6.00

About SFIX

Stitch Fix, Inc. is an online personalized styling service company. The Company has operations in the United States. It is focused on creating a client-first styling experience, offering an alternative to impersonal, time-consuming and inconvenient traditional shopping. The Company’s Fix is a Stitch Fix-branded box containing a personalized assortment of apparel, shoes, and accessories informed by its algorithms and sent by StitchFix stylists and delivered to the clients. The Company offers two types of fix scheduling: Auto-ship, where clients can elect to receive fixes at a regular cadence aligned to their style needs. On-demand, where clients can choose to schedule a one-time fix at any time. Its clients can engage in receiving a personalized shipment of items informed by its algorithms and sent by a Stitch Fix stylist (a Fix). Its clients can purchase directly from its Website or mobile app based on a personalized assortment of outfit and item recommendations.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Stitch Fix Q2 Earnings Announcement Scheduled

- Earnings Release Date: Stitch Fix is set to announce its Q2 earnings on March 11 after market close, with consensus EPS estimate at -$0.04 and revenue expected at $332.79 million, reflecting a 6.6% year-over-year growth, which could significantly impact the company's market performance.

- Historical Performance Review: Over the past year, Stitch Fix has beaten EPS estimates 50% of the time and revenue estimates 75% of the time, indicating a certain level of capability in managing market expectations.

- Estimate Revision Dynamics: In the last three months, there has been one upward revision for EPS estimates and two downward revisions for revenue estimates, reflecting a cautious market sentiment regarding the company's future performance, which may affect investor confidence.

- Market Focus: Despite challenges in profitability, analysts remain attentive to the company's turnaround momentum, emphasizing the need for fundamental improvements to attract more investor interest.

See More

Stitch Fix (SFIX) Q2 2026 Earnings Call Transcript

See More

Stitch Fix Reports 9.4% Revenue Growth in Q2 Amid AI Adoption

- Revenue Growth: Stitch Fix generated $341.3 million in revenue during the fiscal second quarter, reflecting a 9.4% year-over-year increase, despite a slight decline in active clients, indicating enhanced competitiveness in the apparel and accessories market.

- Increased Customer Value: Net revenue per client rose by 7.4% to $577, even with a 0.8% drop in active clients, as the company improved customer spending through a personalized shopping experience.

- Cash Flow Improvement: The company reported free cash flow of $3.35 million in the second quarter, a significant turnaround from negative free cash flow of $19.4 million a year ago, indicating a notable improvement in financial health.

- Future Outlook: Although the revenue guidance for Q3 falls short of market consensus, Stitch Fix anticipates FY26 net revenue growth of 5% to 6.5% and has raised its adjusted EBITDA guidance to between $42 million and $50 million, reflecting confidence in future growth.

See More

Stitch Fix Q2 Earnings Beat Expectations

- Earnings Highlights: Stitch Fix reported a Q2 GAAP EPS of -$0.02, beating expectations by $0.03, with revenue of $341.3 million reflecting a 9.4% year-over-year increase, surpassing estimates by $8.51 million, indicating resilience and growth potential in the market.

- Future Outlook: The company projects Q3 2026 net revenue between $330 million and $335 million, representing a year-over-year growth of 1.5% to 3.1%, with adjusted EBITDA expected to range from $7 million to $10 million, showcasing confidence in future growth.

- Annual Forecast: Stitch Fix has updated its financial outlook for FY 2026, anticipating net revenue between $1.33 billion and $1.35 billion, with a year-over-year growth of 5% to 6.5%, and adjusted EBITDA projected at $42 million to $50 million, reflecting ongoing improvements in revenue and profitability.

- Cash Flow Position: The company expects a gross margin for FY 2026 between 43% and 44%, with advertising expenses as a percentage of revenue between 9% and 10%, and anticipates being free cash flow positive for the full year, indicating robust financial management.

See More

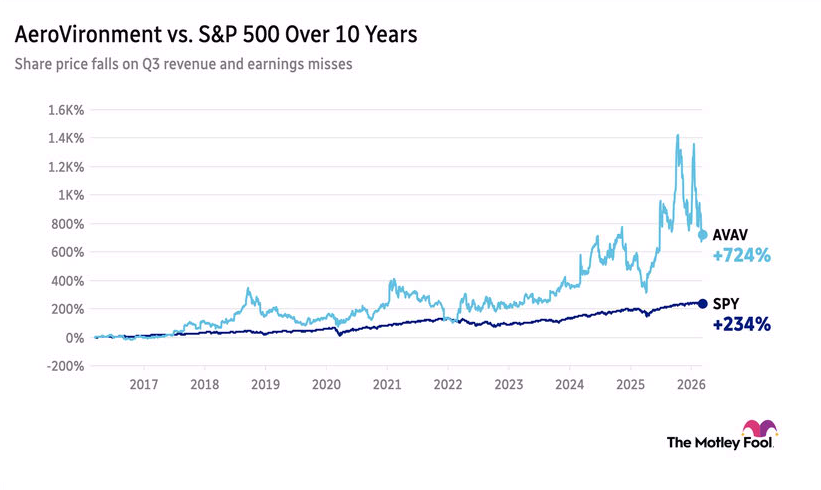

AeroVironment's Earnings Miss Expectations Amid Contract Pause

- Earnings Decline: AeroVironment (AVAV) saw a 10% drop in stock price after its Q3 results, despite a 143% year-over-year revenue increase to $408 million, which fell short of Wall Street's $484 million expectations, undermining market confidence.

- Guidance Adjustment: Following the pause of a key U.S. Space Force contract, the company revised its fiscal 2026 revenue guidance down to $1.85-1.95 billion from the previous $1.95-2.0 billion, anticipating a $151 million goodwill impairment as a result.

- Core Business Resilience: CEO Wahid Nawabi emphasized strong demand for the company's Autonomous Systems despite challenges, indicating that the core business remains robust in a competitive landscape.

- Market Uncertainty: The uncertainty surrounding government contracts poses a significant risk to the company's future growth, potentially impacting its competitiveness in a rapidly evolving market environment.

See More

Upcoming Key Market Events Preview

- Earnings Reports: Next week will see earnings results from Hewlett Packard Enterprise (HPE), Kohl's (KSS), Oracle (ORCL), and Adobe (ADBE), which are expected to significantly impact market sentiment, particularly as investors closely monitor performance in the tech and retail sectors amid the current economic climate.

- CPI Data Release: The Consumer Price Index (CPI) results for February will be released, with the market keenly observing changes in inflation trends that will provide crucial insights for the Federal Reserve's monetary policy decisions, potentially influencing interest rate expectations and stock market performance.

- NFIB Optimism Index: The latest readings on the NFIB Optimism Index will be published, reflecting small business owners' confidence in the economic outlook; strong data could boost market sentiment and affect related stock performance.

- Existing Home Sales Data: The latest data on existing home sales in the U.S. will also be released, with the market closely watching the health of the real estate sector, especially against a backdrop of rising interest rates, which could impact consumer confidence and spending.

See More

Stitch Fix Q2 Earnings Announcement Scheduled

- Earnings Release Date: Stitch Fix is set to announce its Q2 earnings on March 11 after market close, with consensus EPS estimate at -$0.04 and revenue expected at $332.79 million, reflecting a 6.6% year-over-year growth, which could significantly impact the company's market performance.

- Historical Performance Review: Over the past year, Stitch Fix has beaten EPS estimates 50% of the time and revenue estimates 75% of the time, indicating a certain level of capability in managing market expectations.

- Estimate Revision Dynamics: In the last three months, there has been one upward revision for EPS estimates and two downward revisions for revenue estimates, reflecting a cautious market sentiment regarding the company's future performance, which may affect investor confidence.

- Market Focus: Despite challenges in profitability, analysts remain attentive to the company's turnaround momentum, emphasizing the need for fundamental improvements to attract more investor interest.

See More

Stitch Fix (SFIX) Q2 2026 Earnings Call Transcript

See More

Stitch Fix Reports 9.4% Revenue Growth in Q2 Amid AI Adoption

- Revenue Growth: Stitch Fix generated $341.3 million in revenue during the fiscal second quarter, reflecting a 9.4% year-over-year increase, despite a slight decline in active clients, indicating enhanced competitiveness in the apparel and accessories market.

- Increased Customer Value: Net revenue per client rose by 7.4% to $577, even with a 0.8% drop in active clients, as the company improved customer spending through a personalized shopping experience.

- Cash Flow Improvement: The company reported free cash flow of $3.35 million in the second quarter, a significant turnaround from negative free cash flow of $19.4 million a year ago, indicating a notable improvement in financial health.

- Future Outlook: Although the revenue guidance for Q3 falls short of market consensus, Stitch Fix anticipates FY26 net revenue growth of 5% to 6.5% and has raised its adjusted EBITDA guidance to between $42 million and $50 million, reflecting confidence in future growth.

See More

Stitch Fix Q2 Earnings Beat Expectations

- Earnings Highlights: Stitch Fix reported a Q2 GAAP EPS of -$0.02, beating expectations by $0.03, with revenue of $341.3 million reflecting a 9.4% year-over-year increase, surpassing estimates by $8.51 million, indicating resilience and growth potential in the market.

- Future Outlook: The company projects Q3 2026 net revenue between $330 million and $335 million, representing a year-over-year growth of 1.5% to 3.1%, with adjusted EBITDA expected to range from $7 million to $10 million, showcasing confidence in future growth.

- Annual Forecast: Stitch Fix has updated its financial outlook for FY 2026, anticipating net revenue between $1.33 billion and $1.35 billion, with a year-over-year growth of 5% to 6.5%, and adjusted EBITDA projected at $42 million to $50 million, reflecting ongoing improvements in revenue and profitability.

- Cash Flow Position: The company expects a gross margin for FY 2026 between 43% and 44%, with advertising expenses as a percentage of revenue between 9% and 10%, and anticipates being free cash flow positive for the full year, indicating robust financial management.

See More

AeroVironment's Earnings Miss Expectations Amid Contract Pause

- Earnings Decline: AeroVironment (AVAV) saw a 10% drop in stock price after its Q3 results, despite a 143% year-over-year revenue increase to $408 million, which fell short of Wall Street's $484 million expectations, undermining market confidence.

- Guidance Adjustment: Following the pause of a key U.S. Space Force contract, the company revised its fiscal 2026 revenue guidance down to $1.85-1.95 billion from the previous $1.95-2.0 billion, anticipating a $151 million goodwill impairment as a result.

- Core Business Resilience: CEO Wahid Nawabi emphasized strong demand for the company's Autonomous Systems despite challenges, indicating that the core business remains robust in a competitive landscape.

- Market Uncertainty: The uncertainty surrounding government contracts poses a significant risk to the company's future growth, potentially impacting its competitiveness in a rapidly evolving market environment.

See More

Upcoming Key Market Events Preview

- Earnings Reports: Next week will see earnings results from Hewlett Packard Enterprise (HPE), Kohl's (KSS), Oracle (ORCL), and Adobe (ADBE), which are expected to significantly impact market sentiment, particularly as investors closely monitor performance in the tech and retail sectors amid the current economic climate.

- CPI Data Release: The Consumer Price Index (CPI) results for February will be released, with the market keenly observing changes in inflation trends that will provide crucial insights for the Federal Reserve's monetary policy decisions, potentially influencing interest rate expectations and stock market performance.

- NFIB Optimism Index: The latest readings on the NFIB Optimism Index will be published, reflecting small business owners' confidence in the economic outlook; strong data could boost market sentiment and affect related stock performance.

- Existing Home Sales Data: The latest data on existing home sales in the U.S. will also be released, with the market closely watching the health of the real estate sector, especially against a backdrop of rising interest rates, which could impact consumer confidence and spending.

See More