Spotify's Profit Forecast Falls Short of Expectations

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Apr 28 2026

0mins

Source: Fool

- Ad Revenue Decline: Spotify's ad-supported revenue fell by 5% year-over-year, causing the stock to drop over 9% ahead of market open, reflecting concerns about growth, particularly in major markets like the U.S.

- Disappointing Profit Guidance: While overall revenue grew by 10%, the outlook for operating income and premium subscriber growth for the upcoming quarter disappointed investors, indicating challenges in major markets.

- User Growth Drivers: All key performance indicators met or exceeded expectations, with advanced AI-powered personalization tools and enhancements to the mobile free tier driving accelerated user growth, despite a weak overall growth outlook.

- Strong Market Performance: Since January 2022, Spotify's stock has outperformed the S&P 500 by 78%, demonstrating robust performance under specific market conditions, even as current profit forecasts raise investor concerns.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy MSFT?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on MSFT

Wall Street analysts forecast MSFT stock price to rise

34 Analyst Rating

32 Buy

2 Hold

0 Sell

Strong Buy

Current: 421.060

Low

500.00

Averages

631.36

High

678.00

Current: 421.060

Low

500.00

Averages

631.36

High

678.00

About MSFT

Microsoft Corporation is a technology company. The Company develops and supports software, services, devices, and solutions. The Company’s segments include Productivity and Business Processes, Intelligent Cloud, and More Personal Computing. The Productivity and Business Processes segment consists of products and services in its portfolio of productivity, communication, and information services. This segment primarily comprises: Office Commercial, Office Consumer, LinkedIn, and Dynamics business solutions. The Intelligent Cloud segment consists of server products and cloud services, including Azure and other cloud services, SQL Server, Windows Server, Visual Studio, System Center, and related Client Access Licenses (CALs), and Nuance and GitHub; and Enterprise Services, including enterprise support services, industry solutions and Nuance professional services. The More Personal Computing segment primarily comprises Windows, Devices, Gaming, and search and news advertising.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Microsoft's AI Investments Drive Strong Growth

- Surge in Capital Expenditure: Microsoft plans to ramp up capital expenditures to $190 billion in the second half of 2026, which has pressured stock prices; however, the company's strong returns on invested capital indicate significant long-term growth potential.

- Azure Revenue Growth: Azure's revenue surged 40% in the most recent quarter, driven by both AI and non-AI services, demonstrating the company's sustained competitiveness in the cloud computing market.

- Strong Microsoft 365 Performance: Commercial software sales rose 19% year-over-year, while consumer version revenue increased by 33%, and Copilot user additions soared 250%, highlighting robust market demand and growth potential for the product.

- Analysts' Optimistic Outlook: Despite shares trading at about 25 times forward earnings expectations, analysts foresee a 30% increase in Microsoft's stock over the next year, reflecting confidence in its ongoing profitability and investment returns.

See More

OpenAI Expected to File for IPO Soon

- Upcoming IPO Filing: OpenAI is expected to file for its initial public offering (IPO) in the coming days or weeks, backed by Microsoft, indicating strong growth potential in the AI sector.

- Valuation Surge: The latest funding round has propelled OpenAI's valuation to $852 billion, with a monthly revenue of $2 billion, showcasing the success of its business model and robust market demand.

- Industry Impact: This news comes just two days after OpenAI CEO Sam Altman won a lawsuit against Tesla CEO Elon Musk, further solidifying its market position.

- Market Frenzy: With OpenAI and Anthropic preparing for IPOs, the investment frenzy in the AI sector is intensifying, attracting increased attention from investors.

See More

US Stocks Edge Up as Economic Data Shows Stability

- Economic Stability: US weekly initial unemployment claims fell by 3,000 to 209,000, close to the expected 210,000, indicating stability in the labor market and boosting investor confidence in economic recovery.

- Manufacturing Expansion: The May S&P manufacturing PMI unexpectedly rose by 0.8 to 55.3, surpassing expectations of 53.8, marking the strongest pace of expansion in four years, which could drive investment and growth in related sectors.

- Oil Price Volatility: WTI crude oil prices retreated after an initial 4% gain, influenced by market reactions to the situation in Iran, highlighting the uncertainty in the energy market that may impact the overall economy.

- Corporate Earnings Performance: So far, 83% of the 466 S&P 500 companies have beaten earnings estimates, with Q1 earnings projected to climb 12% year-over-year, providing support for the stock market despite a slowdown in the tech sector.

See More

Trump Delays Signing of AI Executive Order

- Ceremony Postponed: President Trump announced the delay of the AI executive order signing ceremony originally scheduled for Thursday afternoon, citing dissatisfaction with certain aspects, indicating a strong focus on policy details.

- U.S. Leading Position: Trump emphasized that the U.S. is ahead of China and other nations in AI, stating he does not want any measures to hinder this lead, reflecting a commitment to national competitiveness.

- Policy Implications: The executive order aims to empower the government to pre-evaluate AI models for security vulnerabilities, indicating a growing concern over potential risks associated with AI technology, which may influence future industry regulations.

- Market Reaction: Despite global economic challenges due to geopolitical tensions like the Iran war, massive investments by tech giants in the AI sector continue to drive stock market gains, demonstrating strong market confidence in AI technology.

See More

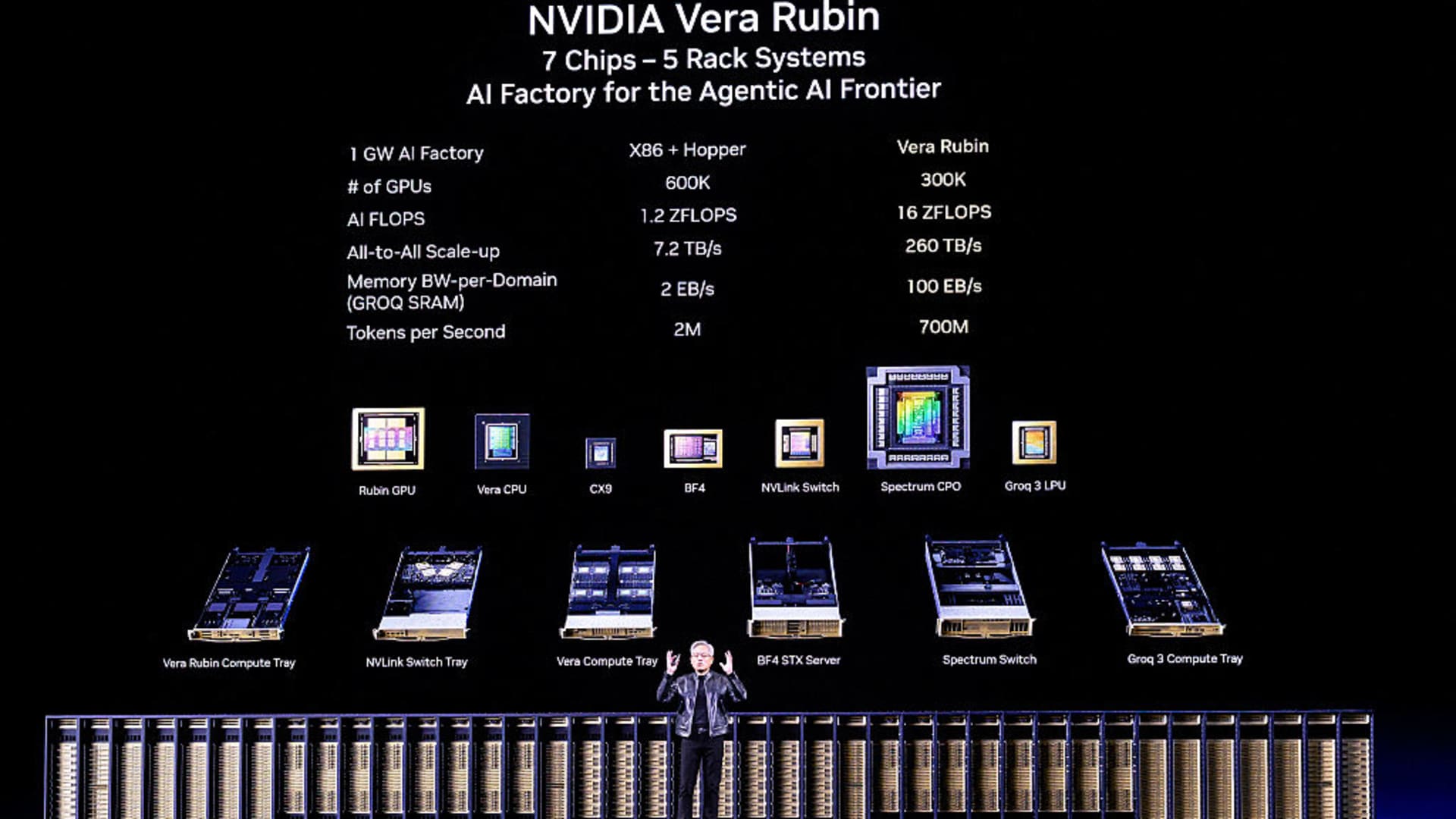

Nvidia Unveils Next-Gen AI Data Center Platform

- AI Capital Expenditure Forecast: Nvidia CEO Jensen Huang predicts AI capital expenditures could reach $3 to $4 trillion, significantly exceeding Wall Street estimates, indicating strong confidence in AI infrastructure demand that may drive future revenue growth for the company.

- Hyperscale Capex Surge: CFO Colette Kress highlights that hyperscale capital expenditures are expected to exceed $1 trillion by 2027, suggesting an acceleration in AI infrastructure investment that further solidifies Nvidia's dominant position in the AI chip market.

- Cloud Revenue Growth: Quarterly revenues from Alphabet, AWS, and Microsoft surpassed expectations, growing 63%, 28%, and 40% respectively, indicating robust performance in the cloud computing market that will support Nvidia's business and expand its market share.

- Productivity Consensus Missing: Despite the potential for substantial returns on AI investments, economists remain cautious about AI's long-term profitability and productivity impact, with JPMorgan estimating a need for $650 billion in annual revenue by 2030, reflecting market concerns over the actual benefits of AI.

See More

NextEra and Dominion Announce $67 Billion Merger Deal

- Merger Scale: NextEra Energy announced an all-stock acquisition of Dominion Energy valued at approximately $67 billion, with a projected combined enterprise value of $420 billion if regulatory approval is obtained, potentially reshaping the U.S. utility landscape.

- Regulatory Challenges: Despite the massive scale of the deal, analysts highlight NextEra's poor track record with regulatory approvals, suggesting it may face stringent scrutiny from the Federal Energy Regulatory Commission and various state commissions, increasing the deal's uncertainty.

- Market Reaction: The market's response to the merger is mixed, with Jefferies analysts suggesting that investors may pivot towards safer investments like Duke Energy and Southern Company to mitigate potential risks and uncertainties surrounding the deal.

- LNG Outlook: In the liquefied natural gas sector, Energy Secretary Chris Wright indicated that China is set to become a significant buyer of U.S. crude oil, and Louisiana's ample natural gas supply can support the growth of LNG exports, showcasing the industry's robust development potential.

See More

Microsoft's AI Investments Drive Strong Growth

- Surge in Capital Expenditure: Microsoft plans to ramp up capital expenditures to $190 billion in the second half of 2026, which has pressured stock prices; however, the company's strong returns on invested capital indicate significant long-term growth potential.

- Azure Revenue Growth: Azure's revenue surged 40% in the most recent quarter, driven by both AI and non-AI services, demonstrating the company's sustained competitiveness in the cloud computing market.

- Strong Microsoft 365 Performance: Commercial software sales rose 19% year-over-year, while consumer version revenue increased by 33%, and Copilot user additions soared 250%, highlighting robust market demand and growth potential for the product.

- Analysts' Optimistic Outlook: Despite shares trading at about 25 times forward earnings expectations, analysts foresee a 30% increase in Microsoft's stock over the next year, reflecting confidence in its ongoing profitability and investment returns.

See More

OpenAI Expected to File for IPO Soon

- Upcoming IPO Filing: OpenAI is expected to file for its initial public offering (IPO) in the coming days or weeks, backed by Microsoft, indicating strong growth potential in the AI sector.

- Valuation Surge: The latest funding round has propelled OpenAI's valuation to $852 billion, with a monthly revenue of $2 billion, showcasing the success of its business model and robust market demand.

- Industry Impact: This news comes just two days after OpenAI CEO Sam Altman won a lawsuit against Tesla CEO Elon Musk, further solidifying its market position.

- Market Frenzy: With OpenAI and Anthropic preparing for IPOs, the investment frenzy in the AI sector is intensifying, attracting increased attention from investors.

See More

US Stocks Edge Up as Economic Data Shows Stability

- Economic Stability: US weekly initial unemployment claims fell by 3,000 to 209,000, close to the expected 210,000, indicating stability in the labor market and boosting investor confidence in economic recovery.

- Manufacturing Expansion: The May S&P manufacturing PMI unexpectedly rose by 0.8 to 55.3, surpassing expectations of 53.8, marking the strongest pace of expansion in four years, which could drive investment and growth in related sectors.

- Oil Price Volatility: WTI crude oil prices retreated after an initial 4% gain, influenced by market reactions to the situation in Iran, highlighting the uncertainty in the energy market that may impact the overall economy.

- Corporate Earnings Performance: So far, 83% of the 466 S&P 500 companies have beaten earnings estimates, with Q1 earnings projected to climb 12% year-over-year, providing support for the stock market despite a slowdown in the tech sector.

See More

Trump Delays Signing of AI Executive Order

- Ceremony Postponed: President Trump announced the delay of the AI executive order signing ceremony originally scheduled for Thursday afternoon, citing dissatisfaction with certain aspects, indicating a strong focus on policy details.

- U.S. Leading Position: Trump emphasized that the U.S. is ahead of China and other nations in AI, stating he does not want any measures to hinder this lead, reflecting a commitment to national competitiveness.

- Policy Implications: The executive order aims to empower the government to pre-evaluate AI models for security vulnerabilities, indicating a growing concern over potential risks associated with AI technology, which may influence future industry regulations.

- Market Reaction: Despite global economic challenges due to geopolitical tensions like the Iran war, massive investments by tech giants in the AI sector continue to drive stock market gains, demonstrating strong market confidence in AI technology.

See More

Nvidia Unveils Next-Gen AI Data Center Platform

- AI Capital Expenditure Forecast: Nvidia CEO Jensen Huang predicts AI capital expenditures could reach $3 to $4 trillion, significantly exceeding Wall Street estimates, indicating strong confidence in AI infrastructure demand that may drive future revenue growth for the company.

- Hyperscale Capex Surge: CFO Colette Kress highlights that hyperscale capital expenditures are expected to exceed $1 trillion by 2027, suggesting an acceleration in AI infrastructure investment that further solidifies Nvidia's dominant position in the AI chip market.

- Cloud Revenue Growth: Quarterly revenues from Alphabet, AWS, and Microsoft surpassed expectations, growing 63%, 28%, and 40% respectively, indicating robust performance in the cloud computing market that will support Nvidia's business and expand its market share.

- Productivity Consensus Missing: Despite the potential for substantial returns on AI investments, economists remain cautious about AI's long-term profitability and productivity impact, with JPMorgan estimating a need for $650 billion in annual revenue by 2030, reflecting market concerns over the actual benefits of AI.

See More

NextEra and Dominion Announce $67 Billion Merger Deal

- Merger Scale: NextEra Energy announced an all-stock acquisition of Dominion Energy valued at approximately $67 billion, with a projected combined enterprise value of $420 billion if regulatory approval is obtained, potentially reshaping the U.S. utility landscape.

- Regulatory Challenges: Despite the massive scale of the deal, analysts highlight NextEra's poor track record with regulatory approvals, suggesting it may face stringent scrutiny from the Federal Energy Regulatory Commission and various state commissions, increasing the deal's uncertainty.

- Market Reaction: The market's response to the merger is mixed, with Jefferies analysts suggesting that investors may pivot towards safer investments like Duke Energy and Southern Company to mitigate potential risks and uncertainties surrounding the deal.

- LNG Outlook: In the liquefied natural gas sector, Energy Secretary Chris Wright indicated that China is set to become a significant buyer of U.S. crude oil, and Louisiana's ample natural gas supply can support the growth of LNG exports, showcasing the industry's robust development potential.

See More