Snap Investors Face Tough Challenges Amid Low Growth

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 53 minutes ago

0mins

Should l Buy SNAP?

Source: Fool

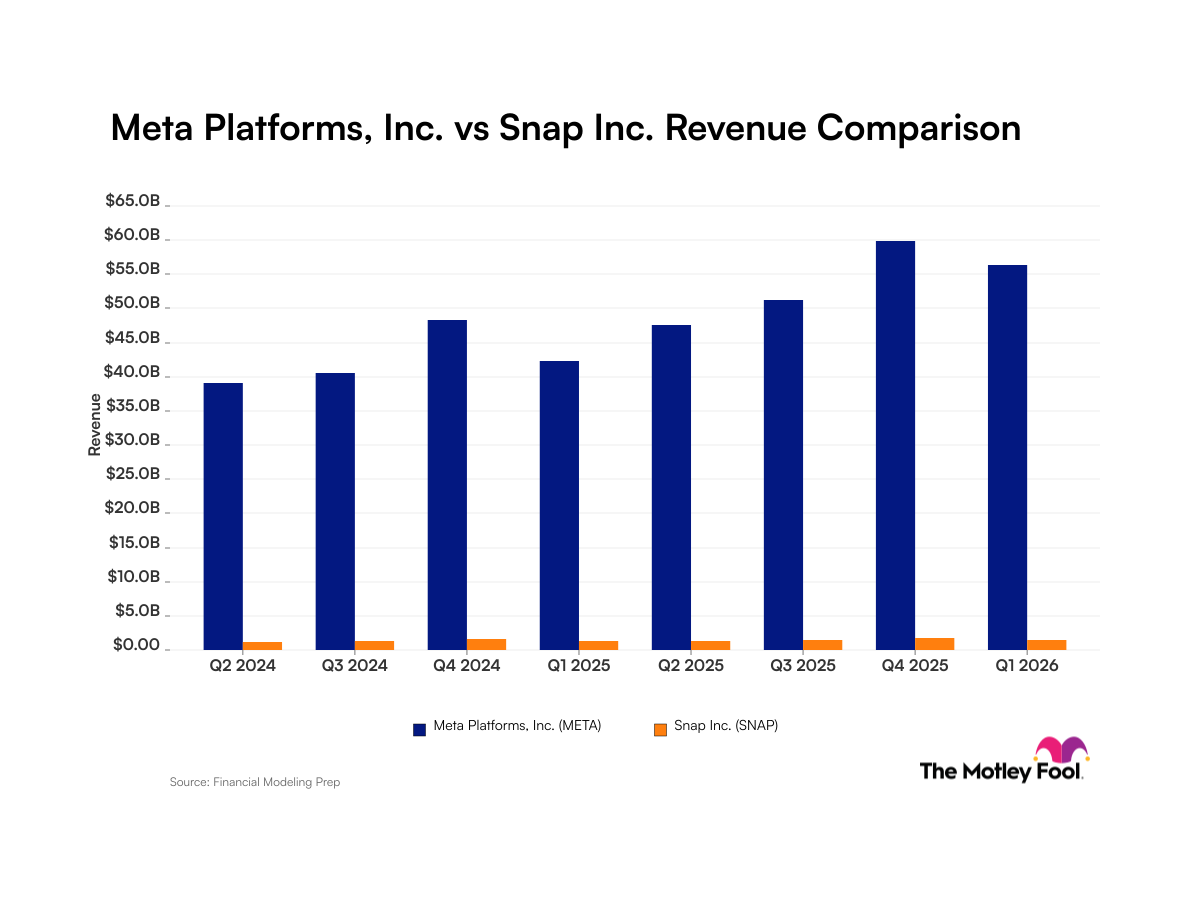

- Weak Revenue Growth: Snap's annualized revenue growth rate of 8.8% over the past three years starkly contrasts with Meta's 19.9%, raising investor concerns about Snap's future profitability and potentially prompting a shift to other investment opportunities.

- Stagnant User Growth: Although Snap reported a 5% increase in monthly active users to 956 million in Q1, the lack of significant improvement in average revenue per user indicates challenges in maintaining its growth stock status.

- Intensifying Competition: Snap faces fierce competition from social media giants like Instagram and TikTok, with users and advertisers increasingly gravitating towards these platforms, further eroding Snap's market share and profit outlook.

- Poor Financial Performance: Snap reported a net loss of $89 million in Q1, and while it anticipates Q2 revenue of $1.535 billion, reflecting a 14.6% year-over-year increase, the flat sequential growth suggests a lack of momentum in revenue generation.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy SNAP?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on SNAP

Wall Street analysts forecast SNAP stock price to rise

28 Analyst Rating

2 Buy

24 Hold

2 Sell

Hold

Current: 5.360

Low

7.00

Averages

9.57

High

13.00

Current: 5.360

Low

7.00

Averages

9.57

High

13.00

About SNAP

Snap Inc. is a technology company. Its flagship product, Snapchat, is a visual messaging application that enhances relationships with friends, family, and the world. Snapchat is the Company's core mobile device application and contains five tabs, complemented by additional tools that function outside the application. Snapchatters can interact with any or all the five tabs. Additionally, it offers Snapchat+, its subscription product that provides subscribers access to exclusive, experimental, and pre-release features. Snapchat+ offers a range of features, from allowing Snapchatters to customize the look and feel of their application, to giving special insights into their friendships. The Company also offers Snapchat for Web, a browser-based product that brings Snapchats calling and messaging capabilities to the Web. Its advertising products include AR Ads and Snap Ads. Snap Ads include Single Image or Video Ads, Story Ads, Collection Ads, Dynamic Ads, Commercials, and Sponsored Snaps.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Snap Investors Face Tough Challenges Amid Low Growth

- Weak Revenue Growth: Snap's annualized revenue growth rate of 8.8% over the past three years starkly contrasts with Meta's 19.9%, raising investor concerns about Snap's future profitability and potentially prompting a shift to other investment opportunities.

- Stagnant User Growth: Although Snap reported a 5% increase in monthly active users to 956 million in Q1, the lack of significant improvement in average revenue per user indicates challenges in maintaining its growth stock status.

- Intensifying Competition: Snap faces fierce competition from social media giants like Instagram and TikTok, with users and advertisers increasingly gravitating towards these platforms, further eroding Snap's market share and profit outlook.

- Poor Financial Performance: Snap reported a net loss of $89 million in Q1, and while it anticipates Q2 revenue of $1.535 billion, reflecting a 14.6% year-over-year increase, the flat sequential growth suggests a lack of momentum in revenue generation.

See More

YouTube and Snap Settle Lawsuit Over Youth Mental Health Crisis Costs

- Settlement Reached: YouTube and Snap have settled a lawsuit in federal court in Oakland, California, resolving claims from the Breathitt County School District in Kentucky, which alleged that social media platforms exacerbated a youth mental health crisis, although the terms of the settlement remain undisclosed.

- Litigation Context: The Breathitt School District is seeking over $60 million to address the impact of social media on students' mental health and to fund a 15-year mental health program, highlighting the significant repercussions social media has on educational institutions.

- Current Legal Landscape: Over 3,300 lawsuits involving addiction claims are pending in California, with an additional 2,400 cases centralized in federal court, indicating the increasing legal pressure on social media companies.

- Landmark Case Impact: A Los Angeles jury found Meta and Alphabet's Google negligent for designing harmful social media platforms, awarding $6 million in damages on March 25, which may serve as a critical reference point for future similar cases.

See More

Meta and Snap Revenue Growth Analysis

- Meta Revenue Surge: Meta's Q1 2026 revenue reached $56.3 billion, marking a 33% year-over-year increase, indicating the effectiveness of its business strategies, particularly in AI investments that have bolstered its advertising revenue and virtual reality hardware performance.

- Snap Revenue Fluctuations: Snap reported Q1 2026 revenue of $1.5 billion, a 12% year-over-year increase, but its net loss of $89 million raises concerns about profitability, especially given the high costs associated with AI technology implementation.

- Partnership Expansion: Meta's expanded infrastructure partnership with Broadcom aims to develop custom hardware, enhancing operational efficiency and market competitiveness, reflecting the company's commitment to technological innovation.

- User Growth Comparison: Snap's daily active users grew by 5% year-over-year, indicating user base expansion; however, compared to Meta's robust sales growth, the sustainability of Snap's revenue growth remains concerning, making its investment appeal relatively low.

See More

Tech Giants' CEOs to Return for Congressional Hearing

- Congressional Hearing Scheduled: CEOs of Meta, Alphabet, TikTok, and Snap have been invited to return to Capitol Hill in June for a broad oversight hearing, indicating ongoing governmental scrutiny of the tech industry.

- Regulatory Environment Shift: The hearing aims to examine the responsibilities of tech companies regarding data privacy, content management, and market competition, potentially leading to stricter regulations that could impact their operational models.

- Industry Impact Assessment: As the hearing approaches, tech companies may need to adjust their policies and practices to address potential legal and public opinion pressures, which could affect their market performance and investor confidence.

- Increased Public Attention: The upcoming hearing reflects public concern over the influence of tech companies, potentially prompting these firms to adopt more proactive measures in transparency and social responsibility to maintain their brand image.

See More

Microsoft's Strategic Battle with OpenAI

- Early Concerns: Microsoft CEO Satya Nadella expressed worries in April 2022 about OpenAI potentially supplanting Microsoft in the tech hierarchy, emphasizing the need for substantial agency in their intellectual property agreement to avoid a fate similar to IBM's.

- Investment Scale: By June 2026, Microsoft is projected to have spent over $100 billion on OpenAI, including investment commitments and infrastructure costs, highlighting its strategic focus on AI and cloud computing markets.

- Market Competition: Despite establishing a significant position in AI infrastructure, Microsoft's stock has dropped 16% this year, indicating competitive pressures in the AI product market, particularly from OpenAI and other emerging rivals.

- Strategic Adjustments: In 2024, Microsoft began viewing OpenAI as a competitor and formed alliances with other AI model developers, demonstrating its adaptability and diversified strategy in the rapidly evolving AI landscape.

See More

Microsoft's Strategic Battle with OpenAI Revealed

- Executive Concerns: Microsoft CEO Satya Nadella expressed worries as early as April 2022 that OpenAI could supplant Microsoft in the tech hierarchy, highlighting the company's acute awareness of competitive pressures in the AI market.

- Investment and Returns: By June 2026, Microsoft is projected to spend over $100 billion on OpenAI, including investment commitments and infrastructure costs, underscoring its strategic focus on AI infrastructure and market positioning.

- Agreement Changes: The partnership agreement between Microsoft and OpenAI has undergone multiple revisions, with the latest in April 2023 capping revenue share payments and allowing OpenAI to serve products to other cloud providers, indicating competitive pressures faced by Microsoft.

- Intensifying Market Competition: Despite establishing a significant position in AI infrastructure, Microsoft's stock has dropped 16% this year, reflecting its struggles in the AI product market, particularly in competition with OpenAI and other rivals.

See More

Snap Investors Face Tough Challenges Amid Low Growth

- Weak Revenue Growth: Snap's annualized revenue growth rate of 8.8% over the past three years starkly contrasts with Meta's 19.9%, raising investor concerns about Snap's future profitability and potentially prompting a shift to other investment opportunities.

- Stagnant User Growth: Although Snap reported a 5% increase in monthly active users to 956 million in Q1, the lack of significant improvement in average revenue per user indicates challenges in maintaining its growth stock status.

- Intensifying Competition: Snap faces fierce competition from social media giants like Instagram and TikTok, with users and advertisers increasingly gravitating towards these platforms, further eroding Snap's market share and profit outlook.

- Poor Financial Performance: Snap reported a net loss of $89 million in Q1, and while it anticipates Q2 revenue of $1.535 billion, reflecting a 14.6% year-over-year increase, the flat sequential growth suggests a lack of momentum in revenue generation.

See More

YouTube and Snap Settle Lawsuit Over Youth Mental Health Crisis Costs

- Settlement Reached: YouTube and Snap have settled a lawsuit in federal court in Oakland, California, resolving claims from the Breathitt County School District in Kentucky, which alleged that social media platforms exacerbated a youth mental health crisis, although the terms of the settlement remain undisclosed.

- Litigation Context: The Breathitt School District is seeking over $60 million to address the impact of social media on students' mental health and to fund a 15-year mental health program, highlighting the significant repercussions social media has on educational institutions.

- Current Legal Landscape: Over 3,300 lawsuits involving addiction claims are pending in California, with an additional 2,400 cases centralized in federal court, indicating the increasing legal pressure on social media companies.

- Landmark Case Impact: A Los Angeles jury found Meta and Alphabet's Google negligent for designing harmful social media platforms, awarding $6 million in damages on March 25, which may serve as a critical reference point for future similar cases.

See More

Meta and Snap Revenue Growth Analysis

- Meta Revenue Surge: Meta's Q1 2026 revenue reached $56.3 billion, marking a 33% year-over-year increase, indicating the effectiveness of its business strategies, particularly in AI investments that have bolstered its advertising revenue and virtual reality hardware performance.

- Snap Revenue Fluctuations: Snap reported Q1 2026 revenue of $1.5 billion, a 12% year-over-year increase, but its net loss of $89 million raises concerns about profitability, especially given the high costs associated with AI technology implementation.

- Partnership Expansion: Meta's expanded infrastructure partnership with Broadcom aims to develop custom hardware, enhancing operational efficiency and market competitiveness, reflecting the company's commitment to technological innovation.

- User Growth Comparison: Snap's daily active users grew by 5% year-over-year, indicating user base expansion; however, compared to Meta's robust sales growth, the sustainability of Snap's revenue growth remains concerning, making its investment appeal relatively low.

See More

Tech Giants' CEOs to Return for Congressional Hearing

- Congressional Hearing Scheduled: CEOs of Meta, Alphabet, TikTok, and Snap have been invited to return to Capitol Hill in June for a broad oversight hearing, indicating ongoing governmental scrutiny of the tech industry.

- Regulatory Environment Shift: The hearing aims to examine the responsibilities of tech companies regarding data privacy, content management, and market competition, potentially leading to stricter regulations that could impact their operational models.

- Industry Impact Assessment: As the hearing approaches, tech companies may need to adjust their policies and practices to address potential legal and public opinion pressures, which could affect their market performance and investor confidence.

- Increased Public Attention: The upcoming hearing reflects public concern over the influence of tech companies, potentially prompting these firms to adopt more proactive measures in transparency and social responsibility to maintain their brand image.

See More

Microsoft's Strategic Battle with OpenAI

- Early Concerns: Microsoft CEO Satya Nadella expressed worries in April 2022 about OpenAI potentially supplanting Microsoft in the tech hierarchy, emphasizing the need for substantial agency in their intellectual property agreement to avoid a fate similar to IBM's.

- Investment Scale: By June 2026, Microsoft is projected to have spent over $100 billion on OpenAI, including investment commitments and infrastructure costs, highlighting its strategic focus on AI and cloud computing markets.

- Market Competition: Despite establishing a significant position in AI infrastructure, Microsoft's stock has dropped 16% this year, indicating competitive pressures in the AI product market, particularly from OpenAI and other emerging rivals.

- Strategic Adjustments: In 2024, Microsoft began viewing OpenAI as a competitor and formed alliances with other AI model developers, demonstrating its adaptability and diversified strategy in the rapidly evolving AI landscape.

See More

Microsoft's Strategic Battle with OpenAI Revealed

- Executive Concerns: Microsoft CEO Satya Nadella expressed worries as early as April 2022 that OpenAI could supplant Microsoft in the tech hierarchy, highlighting the company's acute awareness of competitive pressures in the AI market.

- Investment and Returns: By June 2026, Microsoft is projected to spend over $100 billion on OpenAI, including investment commitments and infrastructure costs, underscoring its strategic focus on AI infrastructure and market positioning.

- Agreement Changes: The partnership agreement between Microsoft and OpenAI has undergone multiple revisions, with the latest in April 2023 capping revenue share payments and allowing OpenAI to serve products to other cloud providers, indicating competitive pressures faced by Microsoft.

- Intensifying Market Competition: Despite establishing a significant position in AI infrastructure, Microsoft's stock has dropped 16% this year, reflecting its struggles in the AI product market, particularly in competition with OpenAI and other rivals.

See More