SM Energy Rating Upgraded to Outperform by Raymond James

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 1 hour ago

0mins

Should l Buy SM?

Source: seekingalpha

- Rating Upgrade: Raymond James has upgraded SM Energy's rating from Underperform to Outperform with a price target of $55, highlighting that the stock has been one of the biggest beneficiaries of rising oil prices since the onset of the Iran war.

- Cash Flow Improvement: Following its merger with Civitas, SM Energy has successfully reduced its debt by approximately $700 million, leading analysts to predict that leverage will fall below 1x by Q4 or earlier, thereby enhancing the company's financial stability.

- Future Growth Potential: Analysts foresee further shareholder return opportunities for SM Energy during 2026-27, assuming steady production performance, particularly if the company meets its goals of lower leverage and higher free cash flow.

- Valuation Advantage: SM Energy's estimated 2027 free cash flow/enterprise value and enterprise value/EBITDA ratios are approximately 14% and 3x, respectively, compared to about 9% and 3.5x for its peer group, indicating its investment attractiveness.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy SM?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on SM

Wall Street analysts forecast SM stock price to fall

8 Analyst Rating

4 Buy

4 Hold

0 Sell

Moderate Buy

Current: 34.320

Low

23.00

Averages

30.00

High

42.00

Current: 34.320

Low

23.00

Averages

30.00

High

42.00

About SM

SM Energy Company is an independent energy company engaged in the acquisition, exploration, development, and production of crude oil, natural gas, and natural gas liquids (NGLs) in Colorado, New Mexico, Texas and Utah. The Company's Permian Basin assets cover approximately 250,000 net acres. The Permian Basin is a large sedimentary basin in western Texas and southeastern New Mexico, United States, noted for its petroleum, natural gas, and potassium deposits. The Company's South Texas assets combine the prolific Eagle Ford natural gas play with the high liquids content Austin Chalk. Located in far South Texas, the Maverick Basin is a Cretaceous-aged foreland basin. Located predominantly in the core, over-pressured oil window of the region, the Uinta Basin adds substantial scale with approximately 63,300 net acres and high oil-content production. The Company's Denver–Julesburg (DJ) Basin assets span approximately 238,000 net acres.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

SM Energy Rating Upgraded to Outperform by Raymond James

- Rating Upgrade: Raymond James has upgraded SM Energy's rating from Underperform to Outperform with a price target of $55, highlighting that the stock has been one of the biggest beneficiaries of rising oil prices since the onset of the Iran war.

- Cash Flow Improvement: Following its merger with Civitas, SM Energy has successfully reduced its debt by approximately $700 million, leading analysts to predict that leverage will fall below 1x by Q4 or earlier, thereby enhancing the company's financial stability.

- Future Growth Potential: Analysts foresee further shareholder return opportunities for SM Energy during 2026-27, assuming steady production performance, particularly if the company meets its goals of lower leverage and higher free cash flow.

- Valuation Advantage: SM Energy's estimated 2027 free cash flow/enterprise value and enterprise value/EBITDA ratios are approximately 14% and 3x, respectively, compared to about 9% and 3.5x for its peer group, indicating its investment attractiveness.

See More

Latest Wall Street Rating Updates

- Goldman Sachs Reiterates Buy on Broadcom: Goldman raised Broadcom's price target from $480 to $500, anticipating strong CapEx spending patterns from key customers, indicating that the upcoming earnings report may exceed market expectations.

- Oppenheimer Upgrades Rubrik: Oppenheimer upgraded Rubrik from Perform to Outperform with a price target of $85, based on strong checks from value-added resellers, highlighting the product's competitive strength in the market.

- UBS Upgrades Packaging Corp: UBS upgraded Packaging Corp from Neutral to Buy, expecting the $50/ton price hike to stick, which, combined with high utilization and prior capacity cuts, could add approximately $290 million in annualized EBITDA.

- Deutsche Bank Upgrades Humana: Deutsche Bank believes there is still time to buy shares of Humana, upgrading its rating to Buy, as it anticipates a new rally in managed care organizations that is just beginning.

See More

SM Energy Boosted by Rising Oil Prices Amid Iran War

- Oil Price Impact: SM Energy has emerged as one of the biggest beneficiaries of the oil price surge linked to the Iran war, with analysts projecting a 60% upside potential and a price target of $55, reflecting strong market confidence.

- Strong Stock Performance: The stock has surged 84% year-to-date, closely following rising crude prices, with WTI futures up 76% in 2026 and currently trading around $100 per barrel, indicating robust market demand.

- Improved Financial Health: The company has leveraged an “oil-driven cash flow windfall” to clean up its post-merger balance sheet, reducing debt by approximately $700 million, with expectations of leverage falling below 1x by Q4, enhancing financial stability.

- Divergent Market Expectations: Despite differing views on SM Energy, among 14 analysts, 6 have buy ratings while 7 hold, indicating a split sentiment regarding the stock's future performance.

See More

SM Energy Company Q1 2026 Earnings Call Highlights

- Merger Synergies: SM Energy achieved approximately $300 million in merger synergies just two months post-merger, raising the target to $375 million by year-end 2026, indicating significant cost savings and operational efficiency gains from the merger.

- Debt Reduction and Buyback Plans: The South Texas asset sale generated about $900 million in net proceeds, fully directed towards debt reduction, and as leverage declines, the company expects to commence share buybacks in Q2, enhancing shareholder returns.

- Production and Financial Outlook: The company raised its full-year production midpoint from 410,000 to 420,000 barrels, with ongoing production growth expected to drive future revenue, while maintaining capital expenditure guidance between $2.65 billion and $2.85 billion.

- Free Cash Flow Performance: Despite facing approximately $180 million in one-time integration and transaction cash costs, SM Energy still delivered $20 million in adjusted free cash flow, demonstrating its strong cash generation capability and financial resilience.

See More

AVUV ETF 52-Week Price Fluctuation Analysis

- Price Range Analysis: The AVUV ETF has a 52-week low of $82.205 and a high of $120.46, with the latest trade at $119.16, indicating stability near its high point, which may attract investor interest in its price movements.

- Technical Analysis Tool: Comparing the latest share price to the 200-day moving average can provide valuable insights for investors, helping to assess market trends and potential buy or sell opportunities.

- ETF Trading Mechanism: Exchange-traded funds (ETFs) trade like stocks, where investors are buying and selling 'units' that can be created or destroyed based on investor demand, impacting the fund's liquidity and market performance.

- Inflows and Outflows Monitoring: Weekly monitoring of changes in shares outstanding for ETFs helps identify those experiencing significant inflows or outflows, where inflows necessitate purchasing underlying assets, while outflows may lead to selling, thus affecting individual stock performance.

See More

SM Energy Stock Surges 40.9% in Six Months

- Outstanding Stock Performance: SM Energy's stock price has surged 40.9% over the past six months, reaching $29.29 per share, reflecting strong investor confidence in the company's future and potentially attracting more attention from investors.

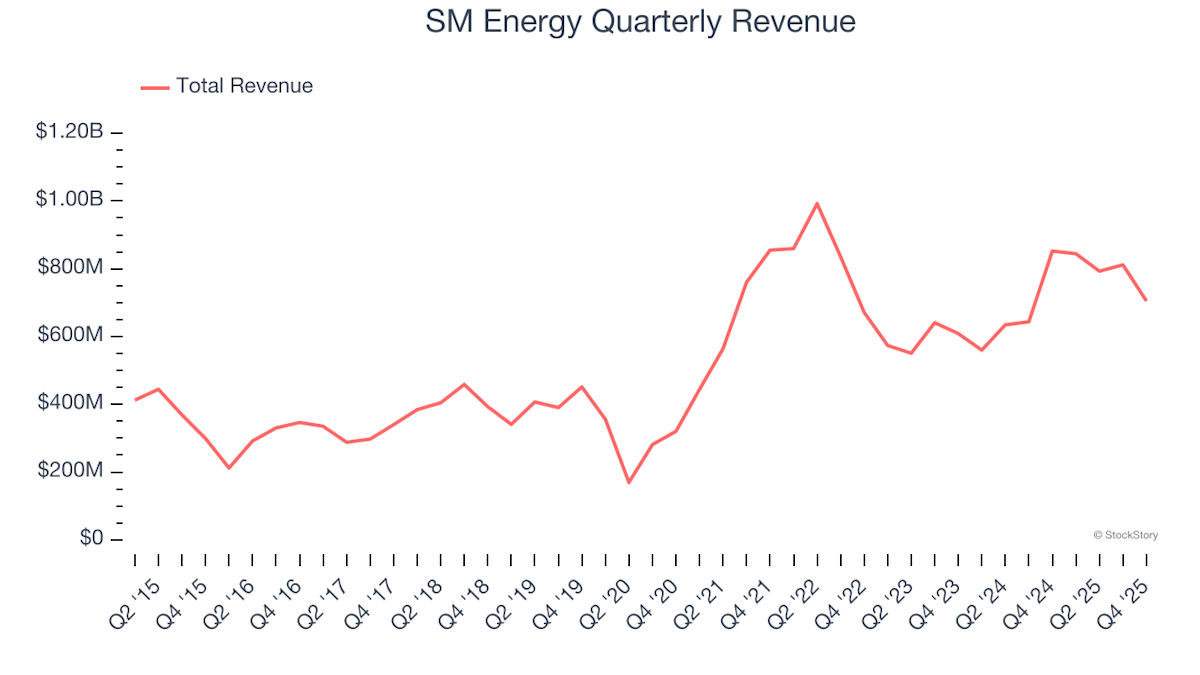

- Strong Revenue Growth: The company has achieved a remarkable 22.9% compounded annual growth rate over the past five years, surpassing industry averages, indicating strong market resonance of its offerings and enhancing its market position.

- Elite Gross Margin: With an average gross margin of 88.3% over the last five years, SM Energy demonstrates the ability to remain profitable even in low commodity price environments, further solidifying its competitive advantage in the energy sector.

- Excellent Free Cash Flow: SM Energy's free cash flow margin averaged 20% over the past five years, enabling effective reinvestment and capital returns to investors, thereby strengthening the company's competitive edge.

See More

SM Energy Rating Upgraded to Outperform by Raymond James

- Rating Upgrade: Raymond James has upgraded SM Energy's rating from Underperform to Outperform with a price target of $55, highlighting that the stock has been one of the biggest beneficiaries of rising oil prices since the onset of the Iran war.

- Cash Flow Improvement: Following its merger with Civitas, SM Energy has successfully reduced its debt by approximately $700 million, leading analysts to predict that leverage will fall below 1x by Q4 or earlier, thereby enhancing the company's financial stability.

- Future Growth Potential: Analysts foresee further shareholder return opportunities for SM Energy during 2026-27, assuming steady production performance, particularly if the company meets its goals of lower leverage and higher free cash flow.

- Valuation Advantage: SM Energy's estimated 2027 free cash flow/enterprise value and enterprise value/EBITDA ratios are approximately 14% and 3x, respectively, compared to about 9% and 3.5x for its peer group, indicating its investment attractiveness.

See More

Latest Wall Street Rating Updates

- Goldman Sachs Reiterates Buy on Broadcom: Goldman raised Broadcom's price target from $480 to $500, anticipating strong CapEx spending patterns from key customers, indicating that the upcoming earnings report may exceed market expectations.

- Oppenheimer Upgrades Rubrik: Oppenheimer upgraded Rubrik from Perform to Outperform with a price target of $85, based on strong checks from value-added resellers, highlighting the product's competitive strength in the market.

- UBS Upgrades Packaging Corp: UBS upgraded Packaging Corp from Neutral to Buy, expecting the $50/ton price hike to stick, which, combined with high utilization and prior capacity cuts, could add approximately $290 million in annualized EBITDA.

- Deutsche Bank Upgrades Humana: Deutsche Bank believes there is still time to buy shares of Humana, upgrading its rating to Buy, as it anticipates a new rally in managed care organizations that is just beginning.

See More

SM Energy Boosted by Rising Oil Prices Amid Iran War

- Oil Price Impact: SM Energy has emerged as one of the biggest beneficiaries of the oil price surge linked to the Iran war, with analysts projecting a 60% upside potential and a price target of $55, reflecting strong market confidence.

- Strong Stock Performance: The stock has surged 84% year-to-date, closely following rising crude prices, with WTI futures up 76% in 2026 and currently trading around $100 per barrel, indicating robust market demand.

- Improved Financial Health: The company has leveraged an “oil-driven cash flow windfall” to clean up its post-merger balance sheet, reducing debt by approximately $700 million, with expectations of leverage falling below 1x by Q4, enhancing financial stability.

- Divergent Market Expectations: Despite differing views on SM Energy, among 14 analysts, 6 have buy ratings while 7 hold, indicating a split sentiment regarding the stock's future performance.

See More

SM Energy Company Q1 2026 Earnings Call Highlights

- Merger Synergies: SM Energy achieved approximately $300 million in merger synergies just two months post-merger, raising the target to $375 million by year-end 2026, indicating significant cost savings and operational efficiency gains from the merger.

- Debt Reduction and Buyback Plans: The South Texas asset sale generated about $900 million in net proceeds, fully directed towards debt reduction, and as leverage declines, the company expects to commence share buybacks in Q2, enhancing shareholder returns.

- Production and Financial Outlook: The company raised its full-year production midpoint from 410,000 to 420,000 barrels, with ongoing production growth expected to drive future revenue, while maintaining capital expenditure guidance between $2.65 billion and $2.85 billion.

- Free Cash Flow Performance: Despite facing approximately $180 million in one-time integration and transaction cash costs, SM Energy still delivered $20 million in adjusted free cash flow, demonstrating its strong cash generation capability and financial resilience.

See More

AVUV ETF 52-Week Price Fluctuation Analysis

- Price Range Analysis: The AVUV ETF has a 52-week low of $82.205 and a high of $120.46, with the latest trade at $119.16, indicating stability near its high point, which may attract investor interest in its price movements.

- Technical Analysis Tool: Comparing the latest share price to the 200-day moving average can provide valuable insights for investors, helping to assess market trends and potential buy or sell opportunities.

- ETF Trading Mechanism: Exchange-traded funds (ETFs) trade like stocks, where investors are buying and selling 'units' that can be created or destroyed based on investor demand, impacting the fund's liquidity and market performance.

- Inflows and Outflows Monitoring: Weekly monitoring of changes in shares outstanding for ETFs helps identify those experiencing significant inflows or outflows, where inflows necessitate purchasing underlying assets, while outflows may lead to selling, thus affecting individual stock performance.

See More

SM Energy Stock Surges 40.9% in Six Months

- Outstanding Stock Performance: SM Energy's stock price has surged 40.9% over the past six months, reaching $29.29 per share, reflecting strong investor confidence in the company's future and potentially attracting more attention from investors.

- Strong Revenue Growth: The company has achieved a remarkable 22.9% compounded annual growth rate over the past five years, surpassing industry averages, indicating strong market resonance of its offerings and enhancing its market position.

- Elite Gross Margin: With an average gross margin of 88.3% over the last five years, SM Energy demonstrates the ability to remain profitable even in low commodity price environments, further solidifying its competitive advantage in the energy sector.

- Excellent Free Cash Flow: SM Energy's free cash flow margin averaged 20% over the past five years, enabling effective reinvestment and capital returns to investors, thereby strengthening the company's competitive edge.

See More